TWKS - Thoughtworks Reduces Headcount As Revenue To Drop In 2023

2023-06-05 14:30:52 ET

Summary

- Thoughtworks Holding, Inc. reported its Q1 2023 financial results on May 9, 2023.

- The firm provides an array of IT consulting services worldwide.

- Thoughtworks Holding has guided to revenue decline in 2023 as clients scrutinize project spending and delay activity due to macroeconomic uncertainties.

- I'm Neutral [Hold] on Thoughtworks Holding, Inc. in the near term.

A Quick Take On Thoughtworks

Thoughtworks Holding, Inc. ( TWKS ) published its Q1 2023 financial results on May 9, 2023, beating revenue but missing earnings per share consensus estimates.

The firm provides a wide range of IT consulting services to clients worldwide.

With management guiding 2023 revenue to decline 2% versus 2022's revenue growth of over 21% and ongoing budget scrutiny and reductions by clients, it is difficult to see an organic upside catalyst to the stock for the remainder of the year and the stock appears to have stabilized at its current level.

Accordingly, my outlook on TWKS is Neutral (Hold) for the near term.

Thoughtworks Overview

Chicago, Illinois-based Thoughtworks Holding, Inc. was founded to develop a set of competencies to enable enterprises to evolve and modernize their IT and digital infrastructures for their business goals.

Management is headed by President and Chief Executive Officer, Guo Xiao, who has been with the firm since 1999 and previously worked in numerous roles within the company and its subsidiaries.

The company's primary offerings include:

-

Enterprise modernization

-

Customer experience

-

Data and AI

-

Digital transformation

The firm seeks consulting and integration relationships with enterprises via its direct sales & marketing efforts as well as through partner relationships.

Thoughtworks' Market & Competition

According to a 2021 market research report by 360 Market Updates, the global market for digital transformation strategy consulting was an estimated $58.2 billion in 2019 and is forecast to reach $143 billion by 2025.

This represents a forecast CAGR of 16.2% from 2020 to 2025.

The main drivers for this expected growth are a large transition from on-premises, legacy systems to cloud-based environments with complex architectures.

Also, the COVID-19 pandemic has likely pulled forward significant demand to modernize enterprise systems, resulting in increased growth prospects for digital transformation consultancies.

Major competitive or other industry participants include:

-

Globant

-

EPAM

-

Slalom

-

Accenture

-

Deloitte Digital

-

McKinsey

-

BCG

-

Ideo

-

Cognizant Technology Solutions

-

Capgemini

-

Company in-house development effort

Thoughtworks' Recent Financial Trends

-

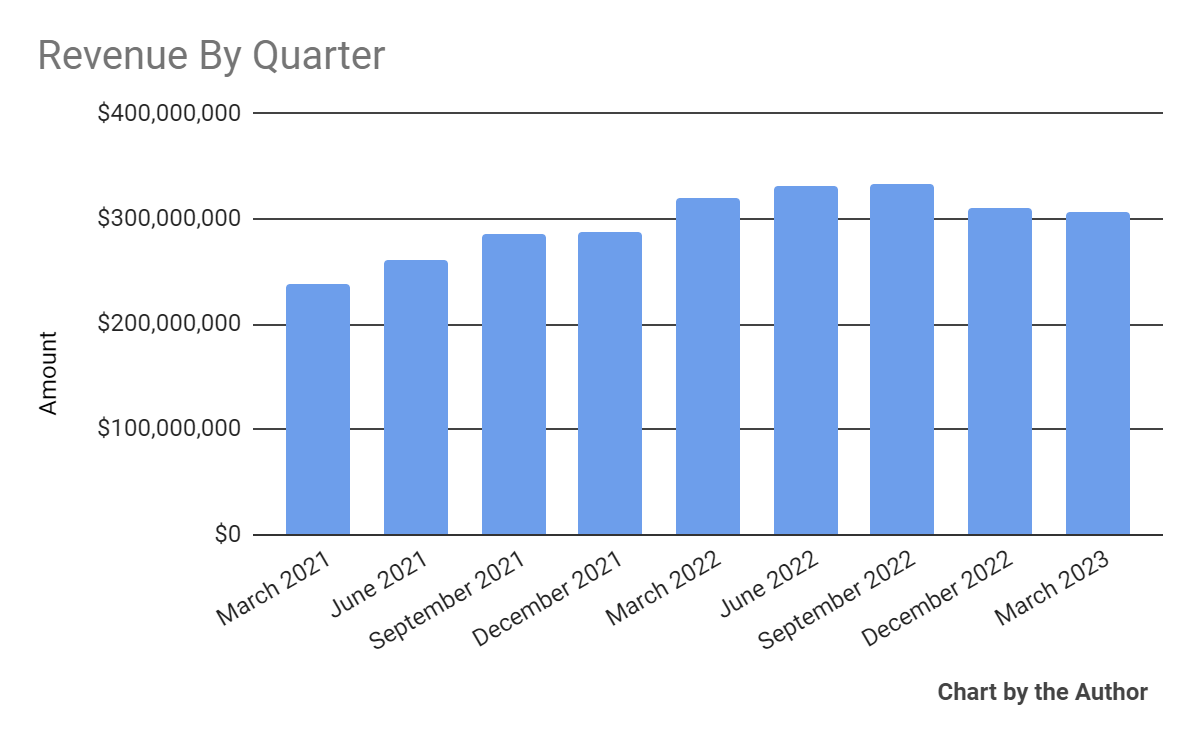

Total revenue by quarter has fallen noticeably:

{kind=link}

-

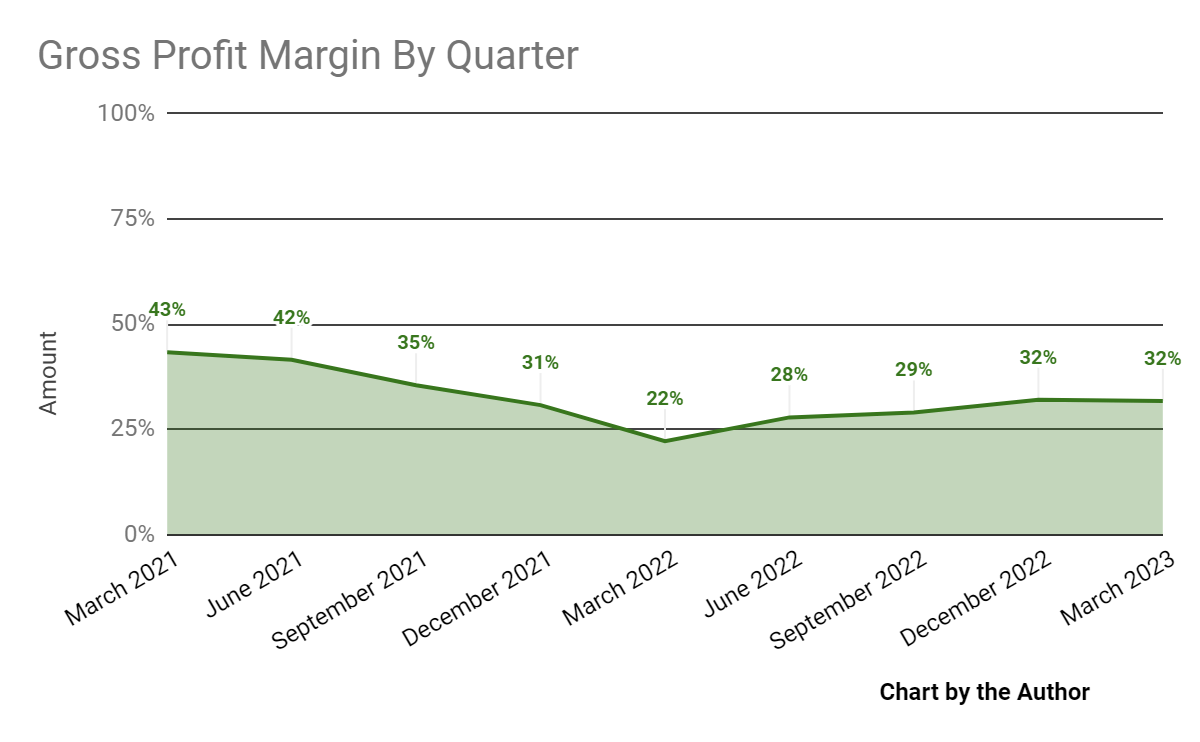

Gross profit margin by quarter has trended higher more recently:

{kind=link}

-

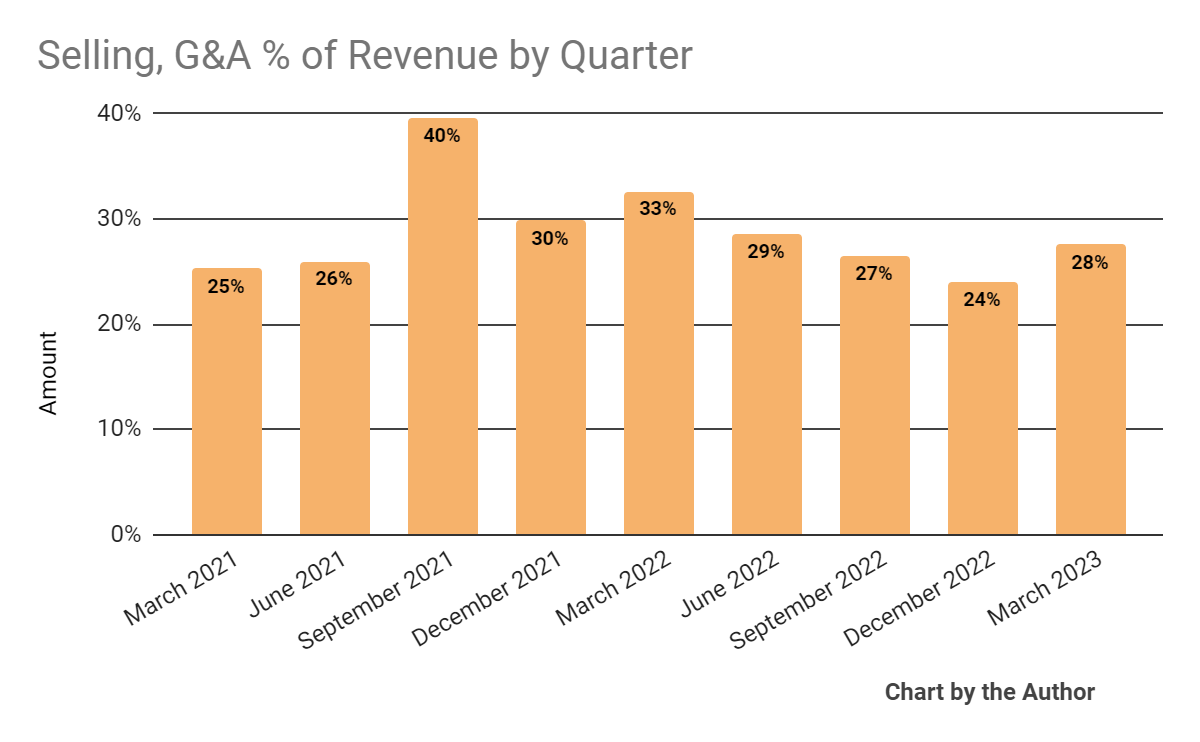

Selling, G&A expenses as a percentage of total revenue by quarter have produced no obvious trend:

{kind=link}

-

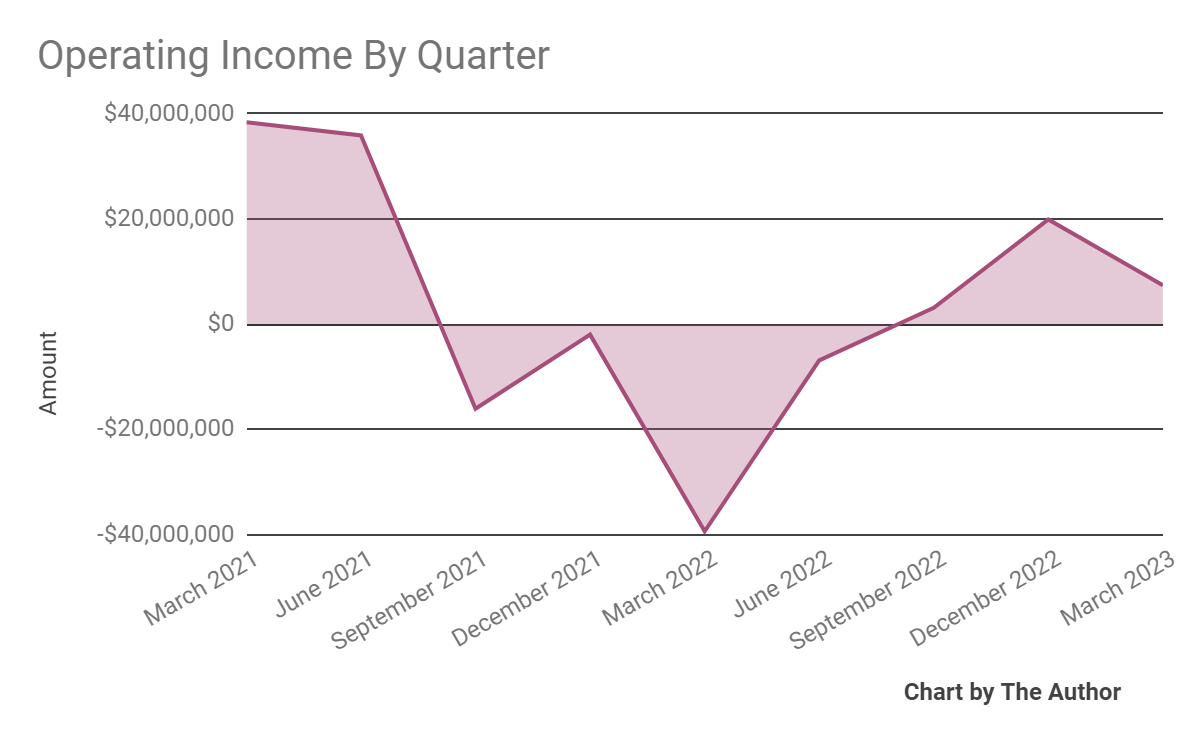

Operating income by quarter has been quite volatile in recent quarters:

{kind=link}

-

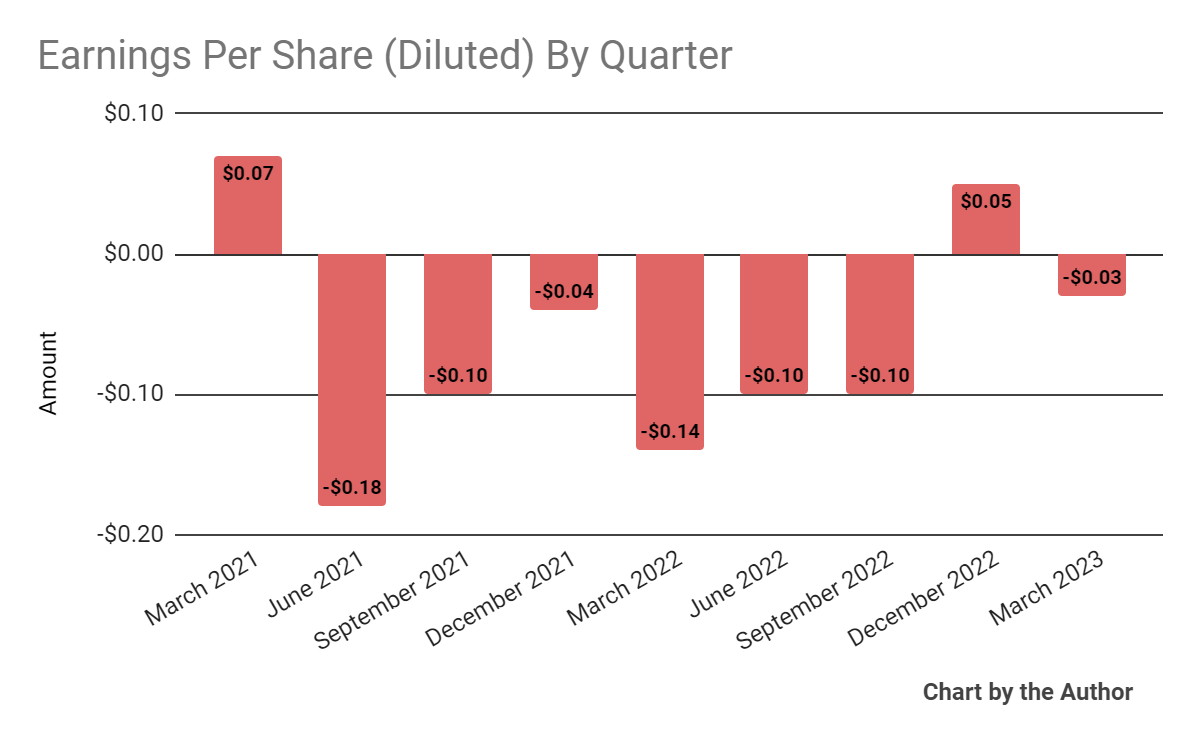

Earnings per share (Diluted) have turned negative in the most recent quarter:

{kind=link}

(All data in the above charts is GAAP)

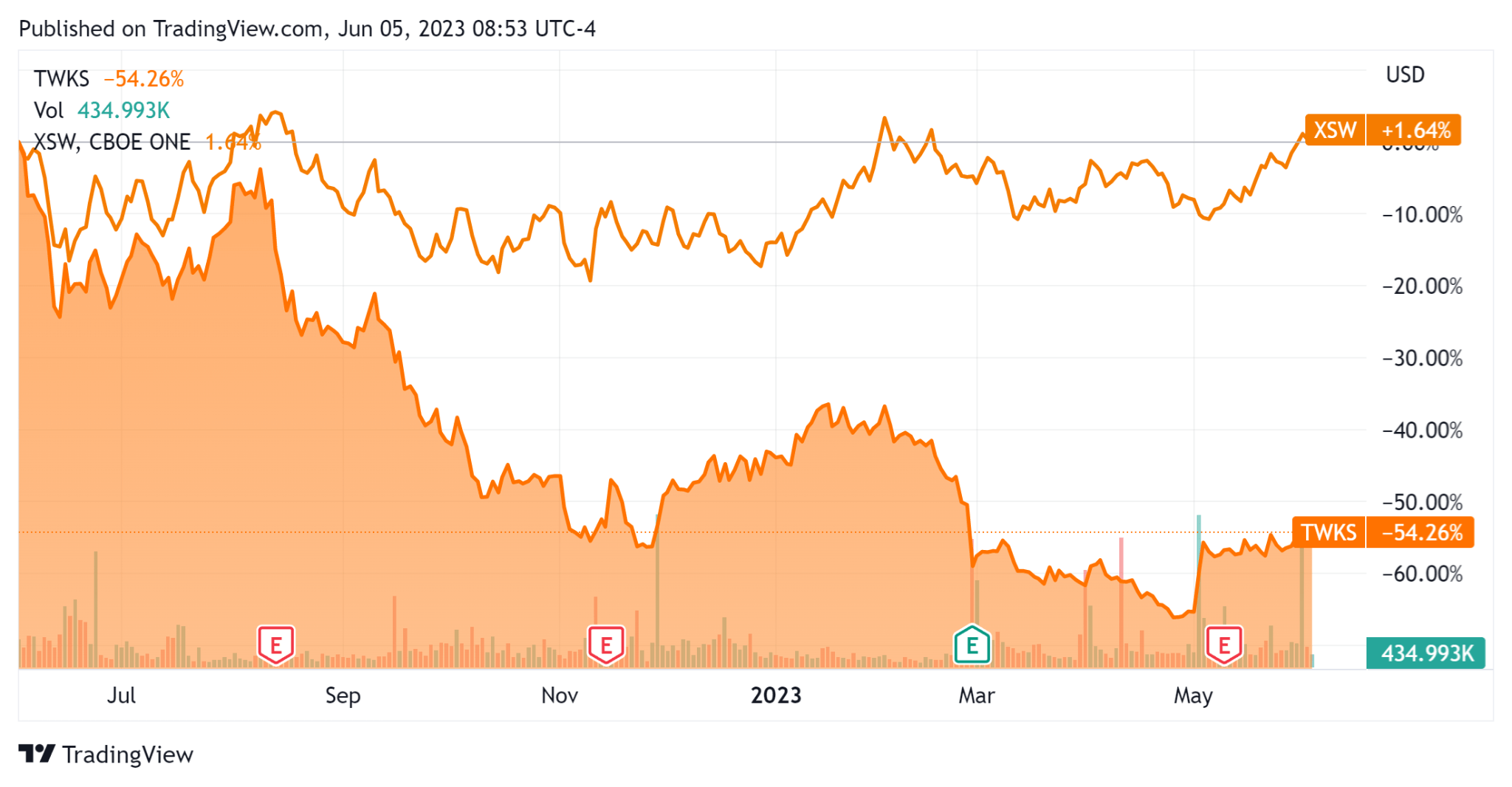

In the past 12 months, TWKS's stock price has fallen 54.26% vs. that of the SPDR® S&P Software & Services ETF ( XSW ) rise of 1.64%, as the chart indicates below:

{kind=link}

For the balance sheet , the firm ended the quarter with $109.3 million in cash and equivalents and $298.3 million in total debt, of which $7.2 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $107.5 million, of which capital expenditures accounted for $21.0 million. The company paid $168.0 million in stock-based compensation in the last four quarters, substantially lower than in recent quarters.

Valuation And Other Metrics For Thoughtworks

Below is a table of relevant capitalization and valuation figures for the company:

| Measure ((TTM)) |

| Amount |

| Enterprise Value/Sales |

| 2.2 |

| Enterprise Value/EBITDA ((FWD)) |

| 13.2 |

| Price/Sales |

| 2.0 |

| Revenue Growth Rate |

| 11.2% |

| Net Income Margin |

| -5.5% |

| EBITDA % |

| 2.6% |

| Net Debt To Annual EBITDA |

| 5.7 |

| Market Capitalization |

| $2,600,000,000 |

| Enterprise Value |

| $2,840,000,000 |

| Operating Cash Flow |

| $128,530,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.18 |

(Source - Seeking Alpha)

Compared to the Seeking Alpha IT Consulting & Other Services industry average EV/EBITDA multiple of 16.56x, the firm is currently being valued by the market at a multiple of 13.2x, a discount to the industry index.

While the firm posted trailing twelve-month revenue growth of 11.2%, the IT Consulting & Other Services index averaged 16.66%.

So, the company is being valued by the market at around less than the industry average, apparently in line with a lower EV/EBITDA multiple when compared to the industry index.

Commentary On Thoughtworks

In its last earnings call ( Source - Seeking Alpha ), covering Q1 2023's results, management highlighted the addition of 47 new clients during the quarter, and a total of 39 clients generated over $10 million in annual revenue, a 26% increase year-over-year.

However, the firm implemented a 4% reduction in workforce during the quarter but is continuing to hire for specific skills still needed.

The company is also focused on integrating AI and machine learning into its various practices and services, noting the strong usage of these technologies among automotive use cases, among other client types.

Notably, management is focused on increasing its development of go-to-market capabilities with the addition of new major partnerships with hyperscale cloud providers, including AWS (Amazon), GCP (Google), and Azure (Microsoft).

Leadership has set a goal of generating 25% of revenue growth from working with partners. This is a strategy that I see from other IT consulting companies as they seek to scale growth more efficiently in a higher labor cost environment.

Total revenue for Q1 2023 dropped by 4.3% year-over-year, while gross profit margin increased by 9.6%.

Selling, G&A expenses as a percentage of revenue fell by 5.1% YoY, and operating income moderated sequentially but remained positive at $7.4 million for the quarter.

Looking ahead, for full-year 2023, management guided to revenue decline of 2% at the midpoint of the range and adjusted diluted EPS of $0.325 at the midpoint.

The company's financial position is moderate, with ample liquidity, nearly $300 million in total debt but trailing twelve-month free cash flow of $107.5 million; its net debt-to-EBITDA multiple is 5.7x, which is fairly high, but management said it 'continued to reduce (its) outstanding term loan, which stood at $301 million as of March 31, 2023, following a $100 million prepayment in February.'

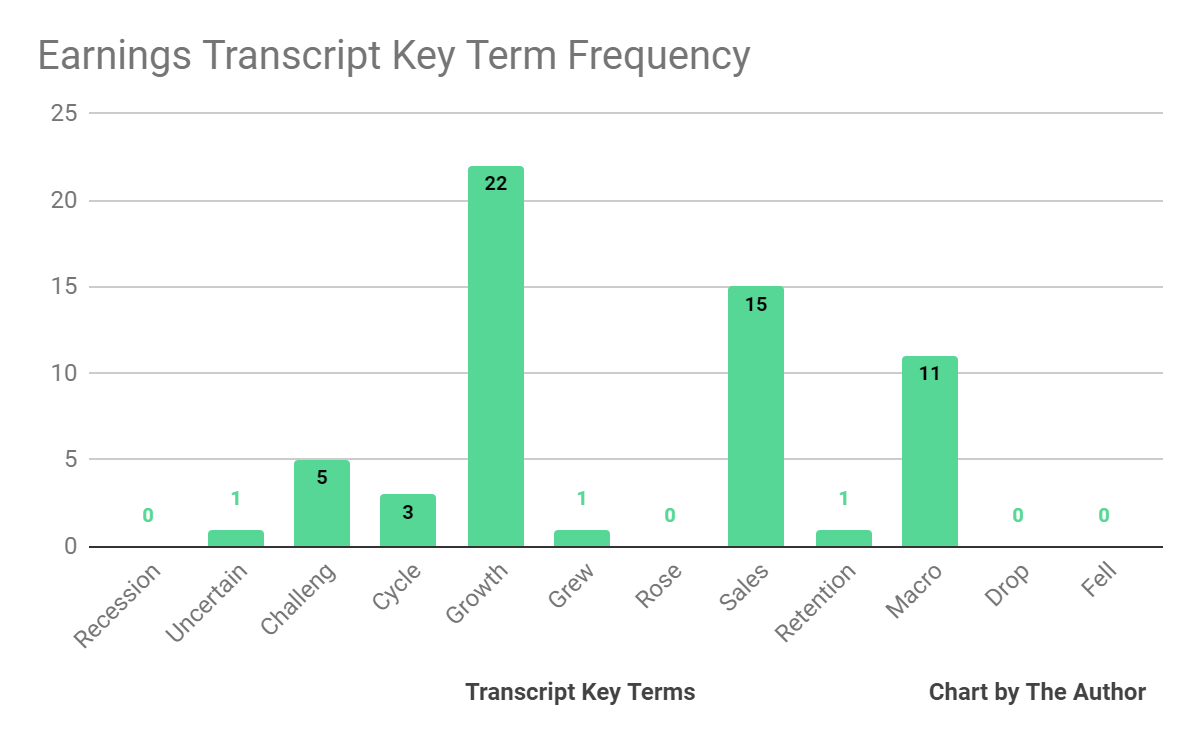

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

{kind=link}

I'm most interested in the frequency of potentially negative terms, so management or analyst questions cited "Uncertain" once, "Challeng(es)(ing)" five times, and "Macro" eleven times.

The negative terms refer to the uncertain macro environment management cited that its clients are facing, and the firm, by extension.

With Thoughtworks Holding, Inc. management guiding 2023 revenue to decline 2% versus 2022's revenue growth of over 21% and ongoing budget scrutiny and reductions by clients, it is difficult to see an organic upside catalyst to the stock for the remainder of the year, although TWKS stock appears to have stabilized at its current level.

Accordingly, my outlook on TWKS is Neutral (Hold) for the near term.

For further details see:

Thoughtworks Reduces Headcount As Revenue To Drop In 2023