TWKS - Thoughtworks Sees Bigger 2023 Revenue Decline Amid Restructuring

2023-09-18 14:42:55 ET

Summary

- Thoughtworks Holding, Inc. provides IT consulting services globally and focuses on enterprise modernization, customer experience, data and AI, and digital transformation.

- The market for digital transformation strategy consulting is expected to reach $143 billion by 2025, driving growth for companies like Thoughtworks.

- Thoughtworks is being valued at a comparatively high multiple despite an expected decline in revenue.

- My outlook on Thoughtworks Holding, Inc. stock is to Sell.

A Quick Take On Thoughtworks

Thoughtworks Holding, Inc. ( TWKS ) provides a variety of IT consulting services to clients worldwide.

I previously wrote about Thoughtworks with a Hold outlook.

With management’s forward revenue expectations of an 11.5% decline in 2023, my outlook on TWKS is to Sell.

Thoughtworks Overview And Market

Chicago-based Thoughtworks has developed competencies to assist enterprises in evolving and modernizing their IT and digital infrastructures for their business goals.

Management is headed by President and CEO Guo Xiao, who has been with the company since 1999 and has worked in numerous roles within the company and its subsidiaries.

The firm’s primary offerings include:

-

Enterprise modernization

-

Customer experience

-

Data and AI

-

Digital transformation

Thoughtworks secures consulting and integration projects with enterprises via its direct sales & marketing efforts as well as through partner relationships.

According to a 2021 research report by 360 Market Updates, the worldwide market for digital transformation strategy consulting was approximately $58.2 billion in 2019 and is expected to reach $143 billion by 2025.

This represents a forecast CAGR of 16.2% from 2020 to 2025.

The main drivers for this expected growth are a transition from on-premises, legacy systems to cloud-based environments in public, private or hybrid architectures.

The recent pandemic has increased demand from organizations to create more capable enterprise IT systems. This has resulted in improved growth prospects for digital transformation consultancies.

Major competitive or other industry participants include:

-

Globant

-

EPAM

-

Slalom

-

Accenture

-

Deloitte Digital

-

McKinsey

-

BCG

-

Ideo

-

Cognizant Technology Solutions

-

Capgemini

-

Company in-house development effort

Thoughtworks’ Recent Financial Trends

-

Total revenue by quarter has trended lower in recent quarters; Operating income by quarter has also dropped sequentially recently.

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has risen slightly recently; Selling and G&A expenses as a percentage of total revenue by quarter have been trending generally lower in recent years.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) have generally remained negative but have been trending toward breakeven since mid-2021:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

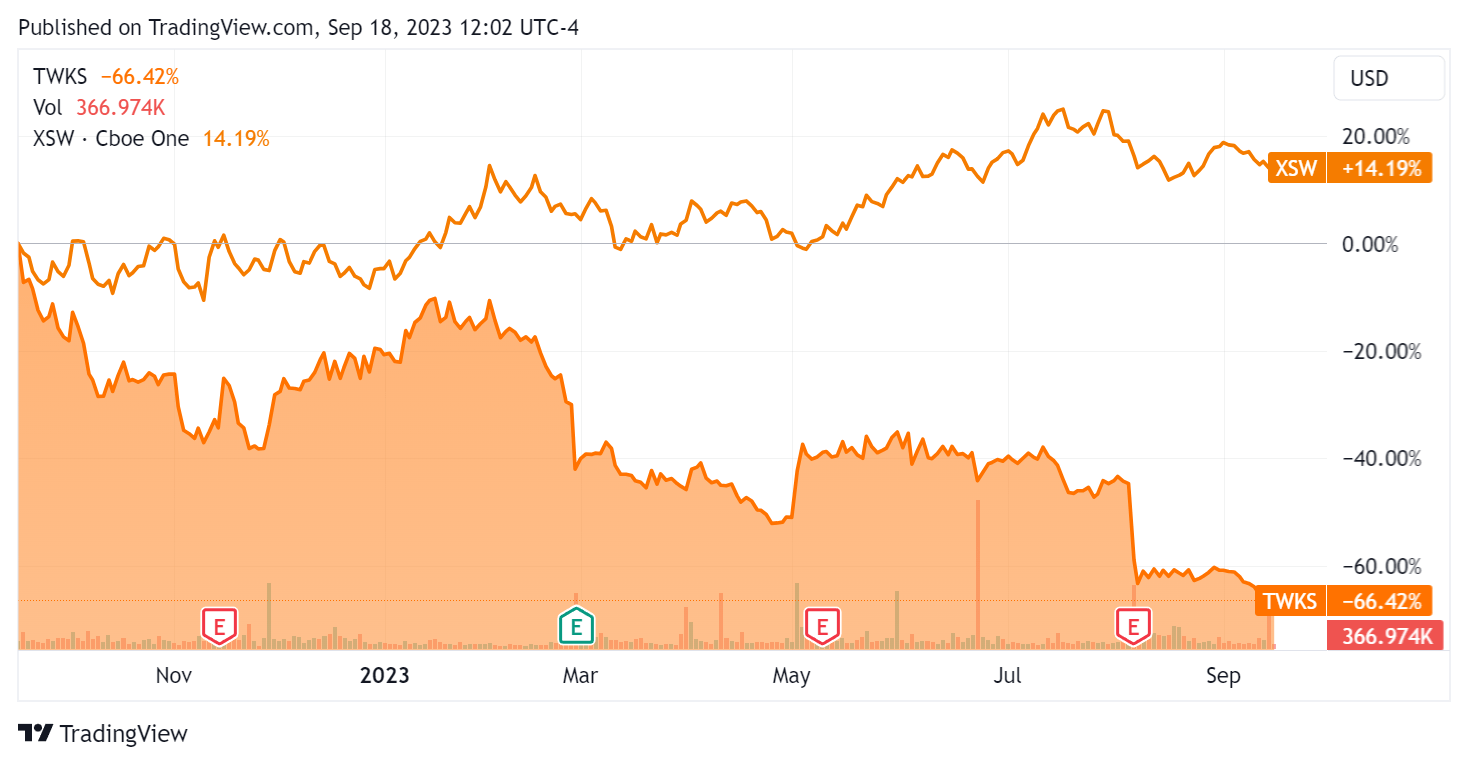

In the past 12 months, TWKS’s stock price has fallen 66.42% vs. that of the SPDR S&P Software & Services ETF’s ( XSW ) risen by 14.19%:

{kind=link}

For balance sheet results, the firm ended the quarter with $88.2 million in cash and equivalents and $296.6 million in total debt, of which $7.2 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $68.5 million, during which capital expenditures were $15.7 million. The company paid $116.6 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Thoughtworks

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 1.3 |

| Enterprise Value / EBITDA |

| 30.1 |

| Price / Sales |

| 1.1 |

| Revenue Growth Rate |

| 1.0% |

| Net Income Margin |

| -3.5% |

| EBITDA % |

| 4.5% |

| Market Capitalization |

| $1,410,000,000 |

| Enterprise Value |

| $1,660,000,000 |

| Operating Cash Flow |

| $84,160,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.12 |

(Source - Seeking Alpha.)

Compared to the Seeking Alpha IT Consulting & Other Services industry average EV/EBITDA multiple of 14.65x, the firm is currently being valued by the market at a multiple of 30.1x, more than double the industry index.

While the firm is expected to generate a forward twelve-month revenue decline of 12.0%, the IT Consulting & Other Services index expects to grow by an average 8.2%.

So, the company is being valued by the market at a large premium to the industry average, despite an expected decline in revenue in 2023.

Sentiment Analysis

I’ve prepared a chart showing the frequency of some key terms in the recent earnings call transcript:

Earnings Transcript Key Terms Frequency (Seeking Alpha)

The results show that the company is facing significant challenges with top clients amid an uncertain macroeconomic environment.

Analysts asked management about its demand-generation efforts. Leadership said that it is focusing its outbound efforts on more demand-resilient industries, such as the public sector, healthcare and automotive.

Management was also questioned about employee utilization, and they responded that the firm is seeing greater offshore utilization than onshore.

Commentary On Thoughtworks

In its last earnings call (Source - Seeking Alpha ), covering Q2 2023’s results, management highlighted its recent restructuring efforts to centralize functions and cut costs.

With the 5% - 6% global headcount reductions, it expects to generate up to $85 million in annual cost savings, with most of that achieved by the end of 2023.

Management believes that centralizing its operations will ‘reduce overall costs, better align resources to strategic priorities, right-size operations and increase operational efficiencies.’

Time will tell, as other consulting firms have retained their diverse structure while allowing normal attrition to occur and retaining capacity in certain areas, especially AI consulting, without resorting to layoffs.

Total revenue for Q2 2023 has fallen 13.% YoY while gross profit margin has improved by 7.1% versus Q2 2022.

Selling and G&A expenses as a percentage of revenue slid 0.3% year-over-year while operating income was nearly breakeven in the current quarter.

The company's financial position is reasonably strong, with ample free cash flow generation over the past 12 months.

Looking ahead, management expects full-year 2023 revenue to contract by approximately 11.5% versus 2022.

If achieved, this would represent a sharp reversal in revenue growth rate versus 2022’s growth rate of 21.13% over 2021.

A potential upside catalyst to the stock could include demand pull-through from prospects and clients seeking AI-enabled technology projects.

However, the technology consulting industry is highly competitive and is suffering from client project delays or cancellations for discretionary projects.

Given the firm’s revenue contraction outlook and worsening macroeconomic conditions, my near-term outlook on Thoughtworks Holding, Inc. stock is to Sell.

For further details see:

Thoughtworks Sees Bigger 2023 Revenue Decline Amid Restructuring