TDUP - ThredUp Q4 2022 Earnings Release: A Nice Reprieve For Investors

2023-03-08 05:58:06 ET

Summary

- ThredUp announced financial results covering the fourth quarter of the company's 2022 fiscal year that exceeded expectations.

- This, combined with strong guidance for 2023, sent shares roaring higher after months of declines.

- This is great to see and the company is doing better than in the past, but it's not exactly a great prospect right now.

March 7th proved to be a fantastic day for shareholders of ThredUp ( TDUP ). For those not familiar, the company operates as one of the world's largest resale platforms for women's and kid's apparel, shoes, and accessories. You might think that this unique sort of platform would be a hit with the market. But over the past year, shares of the enterprise have taken a beating. However, investors received something of a reprieve on March 7th when, after the company reported financial results covering the final quarter of its 2022 fiscal year one day earlier, the stock shot up 51.2%. Fundamentally, the business still has some meaningful problems to deal with. But between beating guidance on both the top and bottom lines, and guidance for the 2023 fiscal year that shows the picture is improving drastically, I think it could make for an appealing opportunity for investors who don't mind some long-term risk.

A new look for ThredUp

As I mentioned already, shares of ThredUp shot up 51.2% on March 7th. This marks a significant reprieve for investors who have been in the company for the past year. For instance, in early May of 2022, I wrote an article wherein I said that growth continued at a nice pace even in spite of bottom line losses the enterprise was experiencing. I noted that when you took a closer look at the data, things didn't look all that bad. But because of the overall financial condition of the business, I had no choice but to rate the business nothing better than a ‘hold’. Unfortunately, the share price situation from that point on deteriorated significantly. Even with the 51.2% increase that the firm saw on March 7th, shares are still down 59.3% since the publication of that article compared to the 2.3% drop seen by the S&P 500.

{kind=link}

Author - SEC EDGAR Data

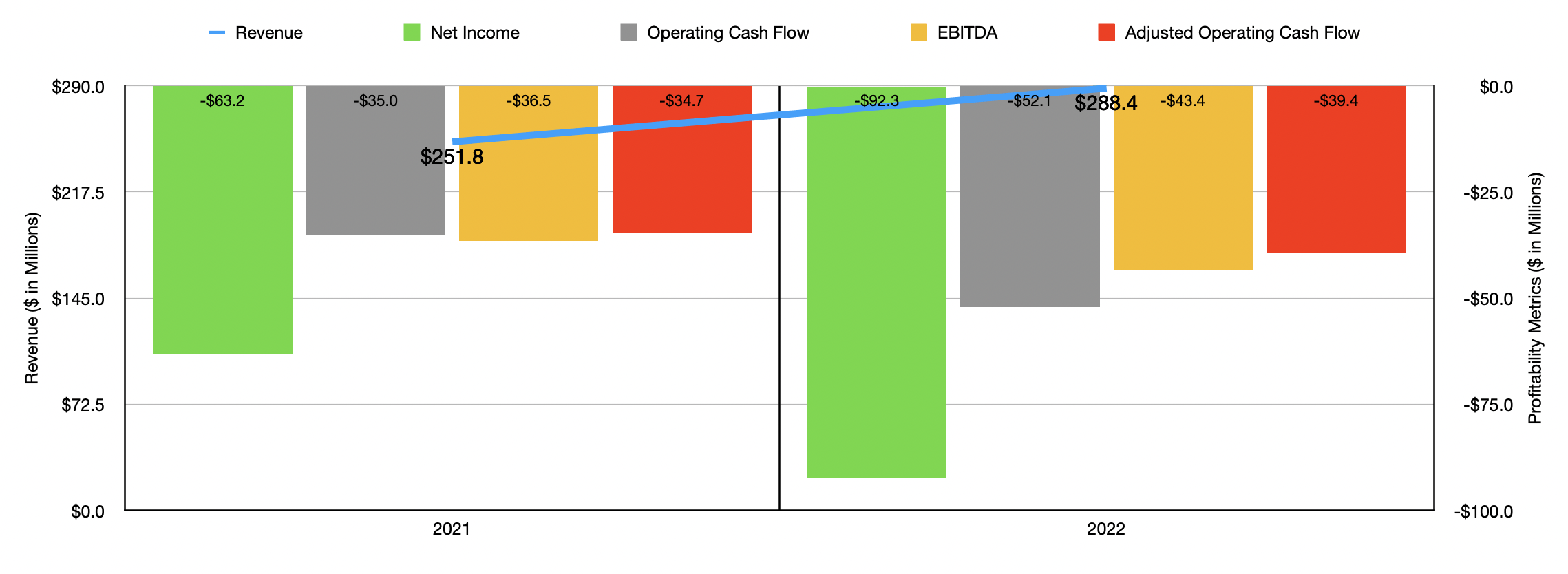

To understand why ThredUp has seen such a beating, we really only need to talk about the financial performance of the business. Consider how the firm fared for the 2022 fiscal year. Sales for that time did come in fairly strong, totaling $288.4 million. That's 14.5% higher than the $251.8 million reported for the 2021 fiscal year. From 2021 to 2022, the number of active buyers on the company's platform actually declined from 1.69 million to 1.65 million. However, the number of orders placed by these customers spiked 22.1% from 5.33 million to 6.51 million. Interestingly during this time, the firm did see its consignment revenue drop, falling about 6% from $186.1 million to $175 million. This decline, management said, was largely because of the decrease in active buyers. There is a heavy correlation between those two factors. At the same time, however, product revenue for the company surged 72.6% from $65.7 million to $113.4 million. This was thanks primarily to the inclusion of the company's European operations that began in October of 2021.

On the bottom line, the picture for the company continued to worsen as well. The firm's net loss went from $63.2 million in 2021 to $92.3 million in 2022. Product revenue has lower gross profit margins than consignment revenue because of its very nature. This brought the company's gross profit margin down from 70.7% to 66.7%. Sadly, other profitability metrics for the company followed a similar trajectory. The firm went from generating operating cash outflows of $35 million in 2021 to $52.1 million in 2022. If we adjust for changes in working capital, cash outflows went from $34.7 million to $39.4 million. Meanwhile, EBITDA in 2022 was negative to the tune of $43.4 million. By comparison, in the 2021 fiscal year, it was negative to the tune of $36.5 million.

{kind=link}

Author - SEC EDGAR Data

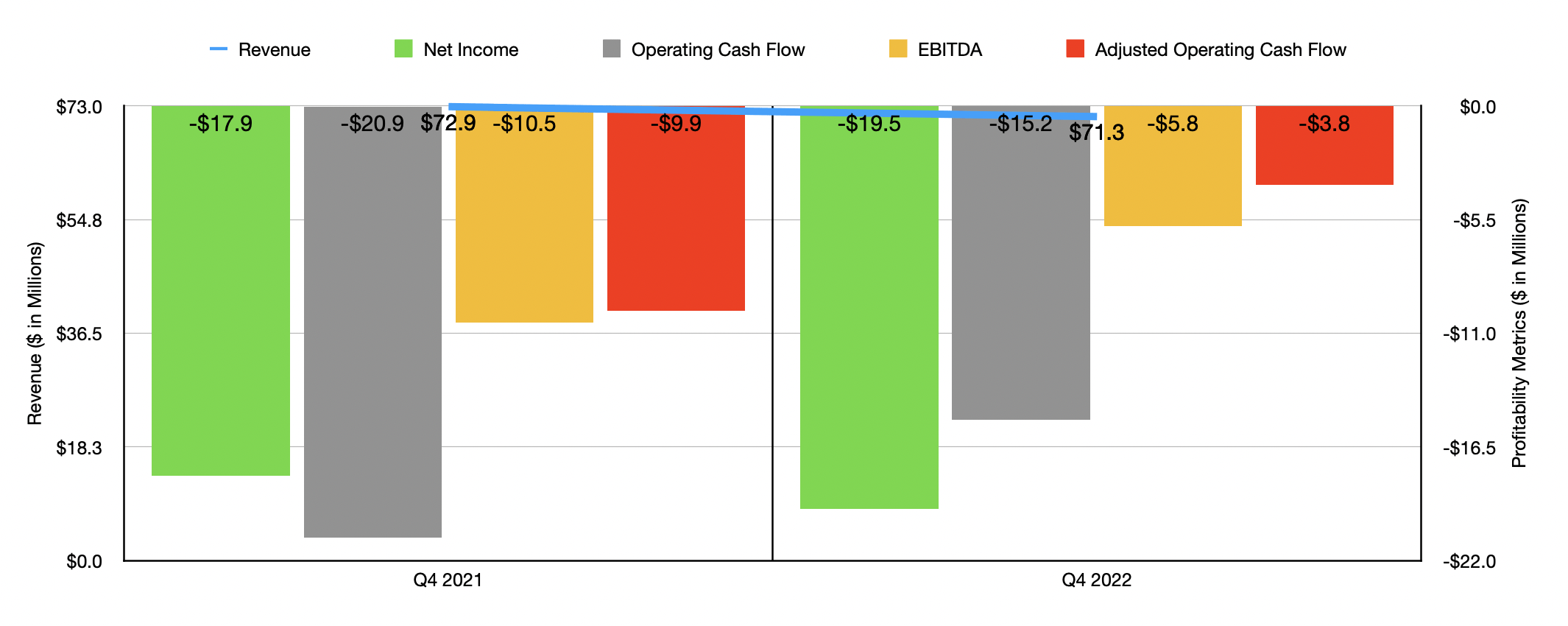

When it comes to the final quarter that the company just reported on March 6th, the picture was a bit less bearish. With consignment revenue falling 16.3% while product revenue grew about 20.4%, overall sales for the company during this time shrank from $72.9 million to $71.3 million. Although this is bearish in and of itself, it's important to note that sales exceeded analysts' expectations by $8.2 million. During the quarter, the company also generated a net loss per share of $0.19. While this is worse than the $0.18 per share loss experienced in the final quarter of 2021, it actually exceeded the expectations set by analysts by $0.01 per share. This translates to a net loss of $19.5 million compared to the net loss of $17.9 million reported one year earlier.

If you look solely at these numbers, it's clear that the picture for the company is looking better than analysts expected. At the same time, however, it still shows that the fundamental condition of the business is worsening. But not every metric showed a year-over-year decline. For instance, the operating cash outflow for the company in the final quarter of 2022 was $15.2 million. That's an improvement over the $20.9 million in outflow seen one year earlier. If we adjust for changes in working capital, the outflow would have gone from $9.9 million to $3.8 million. Meanwhile, EBITDA improved significantly as well, going from a negative $10.5 million to a negative $5.8 million. It's also important to note that the company ended the year with cash in excess of debt that totals about $75.3 million. This gives the firm a great deal of runway to work with moving forward.

{kind=link}

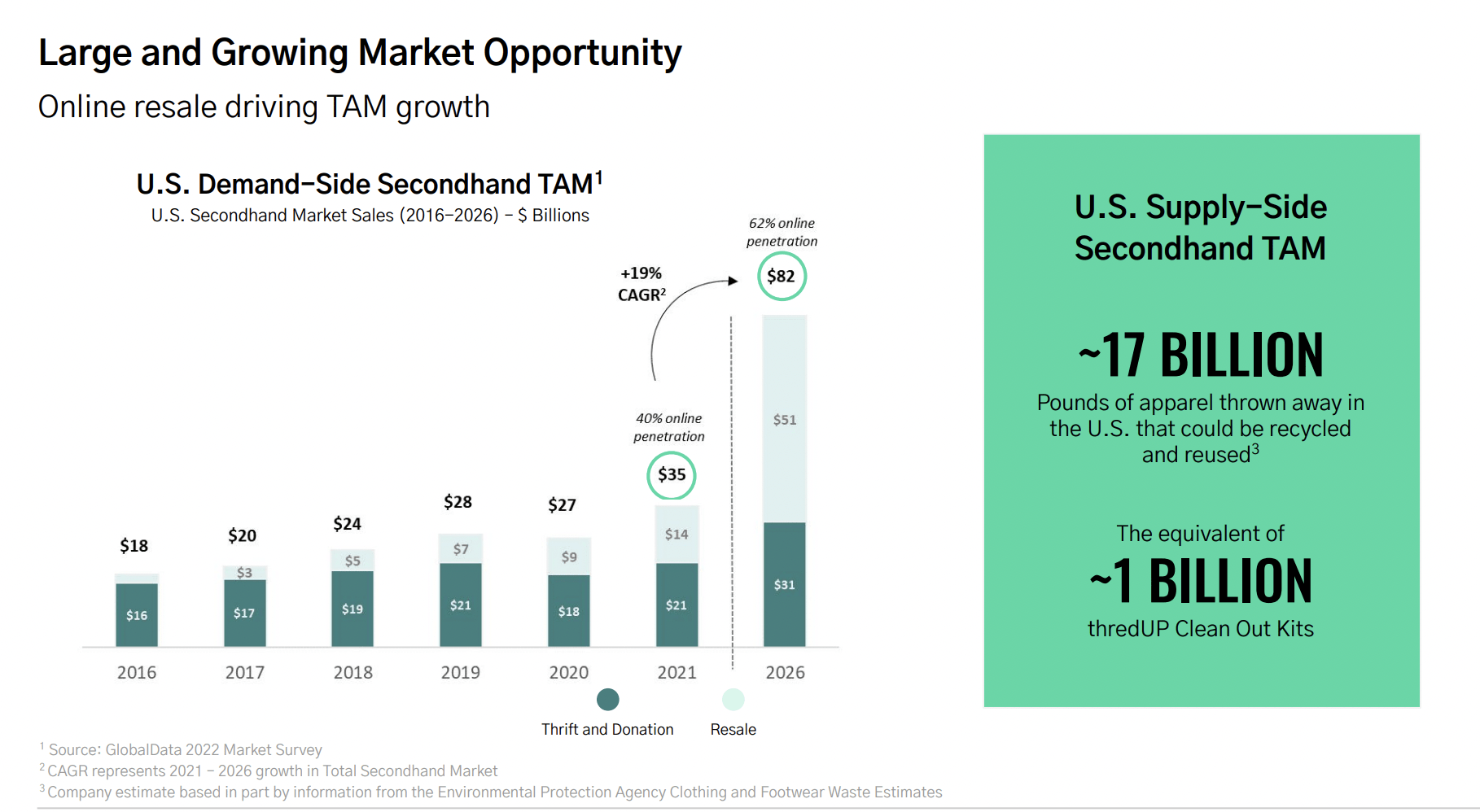

This data alone, in my opinion, is not enough to have pushed the stock up significantly. There was another positive driver behind this. That relates to guidance for the 2023 fiscal year. Revenue is expected to come in at between $310 million and $320 million. Based on the earnings call transcript from the company, it looks as though a great deal of growth seen year over year will relate to product revenue as opposed to consignment revenue growth. It's also worth noting that the firm is optimistic about its RaaS (Resale-as-a-Service) activities. With 42 different brands under its belt and ‘a lot of that RaaS supply’ to burn through, it does seem as though a lot of the growth on the product side of things will relate to those activities. On the bottom line, meanwhile, the company says that its EBITDA margin will be negative by between 6% and 8%. At the midpoint for both that and revenue, we would get EBITDA coming in negative to the tune of $22.1 million. It's important to note that management has high expectations for its resale operations. While the thrift and donation market in the US is expected to hit only $31 billion by 2026 (up from $21 billion in 2021), the resale market should grow from $14 billion to $51 billion over the same period of time. With brand partnerships expanding on this front and the company intending for additional resale shop launches, it's clear that this is the growth engine the firm is betting on.

Because the company generates negative results, we can't really value it in a traditional sense. But we can ask ourselves what kind of cash flow it would need to generate in order to be at least fairly valued. From there, we can see how close it should be to that point. In the table below, you can see three hypothetical scenarios for both adjusted operating cash flow and EBITDA. In the first, you can see a scenario where the company would need to be trading at a multiple of 10 over these metrics. The second calls for a multiple of 20, while the third calls for a multiple of 30. It's difficult to imagine the company trading at the high end of this range. This is especially true when the number of active buyers has declined. But even if we assume that fair value would be a multiple of between 10 and 20, and consider management's guidance for 2023 compared to how the company performed in 2022, it's not unreasonable to think that in another year or so it could hit a rather appealing point.

{kind=link}

Author - SEC EDGAR Data

Takeaway

Based on all the data in front of me, I must say that I am impressed by the move higher that ThredUp experienced. Clearly, my call on the business previously was off. In the near term, because of the excess cash the business enjoys, the risk to shareholders of a permanent loss of capital is fairly low. But in the long run, if the company does not improve its bottom line drastically, that risk will increase. Fortunately, guidance for 2023 is looking up and shares are not so high that the company would not be able to justify its valuation if growth trends continue and margin improvements persist. I can definitely understand why some investors would be bullish about this name. For me, the picture is still not ideal to change my rating to something more bullish. But I do still think that the ‘hold’ rating I assigned the company previously is appropriate.

For further details see:

ThredUp Q4 2022 Earnings Release: A Nice Reprieve For Investors