TDUP - ThredUp: Softening Consumer Demand Expected (Rating Downgrade)

2023-11-29 17:22:03 ET

Summary

- ThredUp's stock price plunged in November after its CEO sold some shares, potentially causing concern among investors.

- In contrast, the company's recent financial results actually outperformed expectations, with 21% revenue growth in Q3 2023, robust gross margin and shrinking adjusted EBITDA loss margin.

- However, the outlook for 2024 remains muted with slowing US demand, and analysts predicting a revenue growth slowdown of 6.8%. This indicates limited upside to the stock for now.

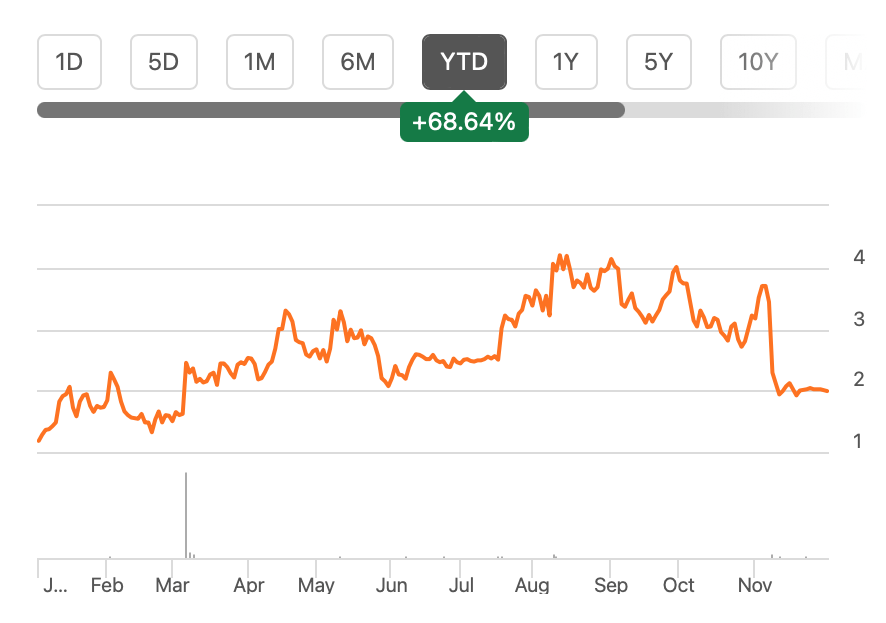

Since the last time , I wrote about the pre-loved clothes and accessories marketplace ThredUp ( TDUP ) in February this year, its price is up by 28%. And this is after it has seen quite a ride in the market this year. By August, it had risen by a huge 167% from the time I wrote. However, it fell off a cliff, as it were, this month.

{kind=link}

Price Chart (Source: Seeking Alpha)

This makes it a good time to revisit ThredUp to see what’s gone wrong and whether the latest dip might actually be a good time to buy it.

Why did the price fall?

Before anything else, let's look at the most recent development. The share price crash. At the end of October, the stock was still sitting pretty, having doubled since I last wrote.

Then on November 6, the company’s SEC filings revealed that its CEO, James Reinhart had been selling stock for the past three months. Following this, TDUP started tumbling, losing almost 40% of its value from the end of October to November 9. It has seen only a feeble recovery since.

A stock sale by the CEO, can of course serve as a confidence blow to investors since it might suggest that the future doesn’t look good. But at the same time, I do believe it needs to be looked at in perspective.

The holdings sold represent 7% of his total stock in the company at the time. Now, the amount sold isn’t a trivial figure. But it does show that he still maintains a significant proportion of his original holding in the stock. In other words, the recent sale might not imply very much. Especially not after the company’s latest results, which are discussed next.

A look back

To give some perspective on the latest numbers, here’s a quick look back at where the company was when I last checked. At the time, it was due for its fourth quarter (Q4 2022) and full-year 2022 results. With slowing down already visible in its numbers and a dim outlook, there was little to look forward to.

But compared to expectations, the numbers actually outperformed. Growth declined by just 2% year-on-year (YoY) in Q4 2022 compared to a forecast of a 13.6% fall. As a result, the full-year growth also came in at a stronger 15% compared to expectations of 11.2%.

2023 so far

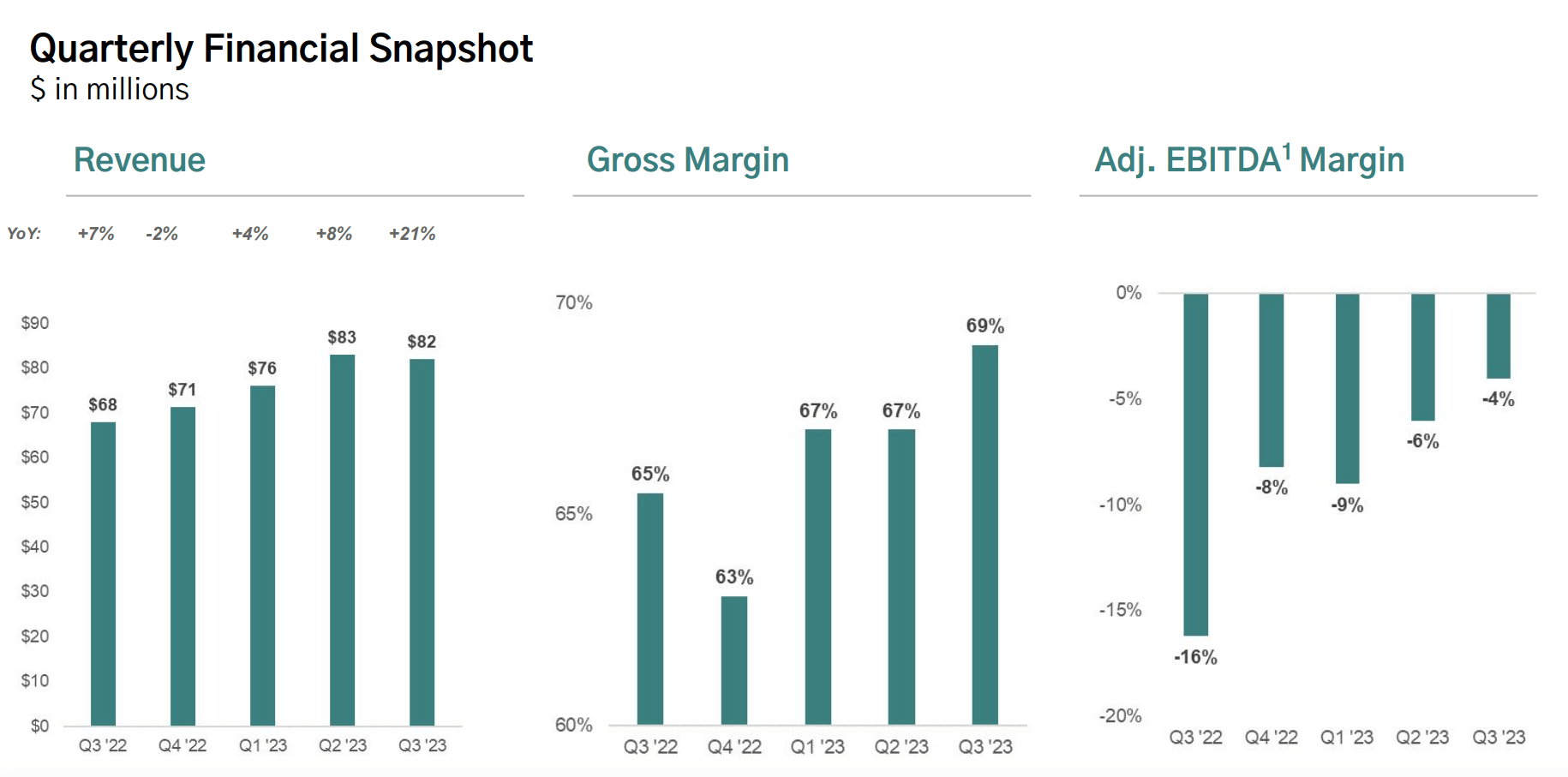

The outlook for 2023 was still muted, though. At the time, analysts had expected a further revenue growth slowdown in 2023 to 7.8%. ThredUp has done better than expectations so far though, with growth at 10.9% for the first nine months of the year (9M 2023). The growth in Q3 2023 is particularly notable at 21%, the fastest in five quarters.

At a very healthy 67.9%, the company’s gross margin has also stayed steady in 9M 2023 from the corresponding period of last year. Here too, Q3 2023 stands out with a 69% margin (Q3 2022: 65.5%). Its adjusted EBITDA loss margin has shrunk during the quarter too (see chart below), which indicates that it may just be getting closer to turning adjusted EBITDA profitable.

{kind=link}

Source: ThredUp

Positive outlook

ThredUp is also relatively upbeat about the final quarter of 2023 with expectations of 12.2% growth. This isn’t exactly a bullish forecast considering (1) that in Q4 2022 it actually saw a revenue decline and (2) in Q3 2023 it has seen 20%+ growth. But it’s still broadly in line with the rise seen so far this year.

If the revenue number in Q4 2023 comes in in line with expectations, the full-year figure would be at 11.2%, which is slightly higher than the growth seen so far. In other words, for the full-year 2023, ThredUp will likely exceed analysts' initial expectations by a small margin.

The market multiples

If growth does come in as expected, TDUP’s forward price-to-sales (P/S) is estimated at 0.68x, which is favourable compared with 0.84x for the consumer discretionary sector. Its trailing twelve months [TTM] at 0.67x is similarly lower than the 0.83x for the sector.

The TTM P/S has, however, risen from the 0.52x it was at when I last checked. It also stays ahead compared to its closest competitor, The RealReal ( REAL ), which is at 0.42x, although it too has risen from 0.22x in February. The gap between ThredUp and The RealReal is for good reason, though. The latter has seen a 4% decline in TTM revenues compared to a 7.6% increase for ThredUp.

For this reason, here I assess the potential for the stock based only on comparison with the sector. This indicates a 15-20% potential for price rise.

What can go wrong

Not so fast, however. With 2023 almost over, it's now time to look at the prospects for 2024 too. And they aren't the best. According to the IMF, the US economy is expected to slow down in 2024. As a consumer discretionary stock, ThredUp is vulnerable to slowing demand.

{kind=link}

Source: IMF

There's already a visible cooling off in the growth rate, as discussed above. And this is hardly just ThredUp's experience. From companies like apparel retailer and Zara owner Inditex ( IDEXY ) to the Swiss Cartier owner Richemont ( CFRUY ), there’s been a marked correction in the US market in comparison with other markets this year.

The bigger challenge with ThredUp is that as a US-focused company, it doesn’t have the cushion of potentially better performance in other markets. So it can be impacted far more. In fact, analysts pencil in revenue growth of 6.8% for 2024, a striking decline from the forecast for 2023.

What next?

Taking the risks into account indicates that there could be a smaller potential for price rise than indicated by the comparison with the sector multiples.

It’s not that there’s anything wrong with ThredUp, though. If anything, its growth so far this year has been better than expected. It’s just that where the US in particular is in the consumer cycle next year, isn’t to its advantage.

To answer the original question, this then isn't a good time to buy ThredUp. Not because the CEO has sold stock, but for more fundamental reasons. I'd wait for the macro cycle to show signs of an uptick again before considering buying it. Or at least I'd wait for next quarter's results, which would also have an outlook for 2024 before taking a call. I'm going with a Hold rating.

For further details see:

ThredUp: Softening Consumer Demand Expected (Rating Downgrade)