SPDV - Thriving In 2023: My Outlook And Strategy

Summary

- Predicting the market is hard and often somewhat pointless. In this article, I focus on the biggest trends that are most likely to unfold.

- I believe we're in a prolonged sideways trend, with room for the market to fall to the low 3,000 range before the Fed is forced to pivot.

- I'm increasing my savings rate and focusing on a few areas that, I believe, will offer value for investors in 2023 and beyond.

Introduction

This month, we've spent a lot of time discussing the outlook and state of various markets and industries. This includes agriculture , housing , and energy . Due to high demand and the general necessity of being prepared for what may happen, I'm writing this general outlook. We'll look into key (interrelated) market drivers, like the Federal Reserve policy path, economic growth, secular inflation, and what this might mean for markets. I will also tell you how I'm dealing with this situation and what my initial strategy will be when it comes to putting money to work.

I'll also present some investing ideas based on articles I wrote this month.

So, let's get to it!

Predicting The Future Is Tricky

I have realized that the past and future are real illusions, that they exist in the present, which is what there is and all there is. - Alan Watts

On the one hand, I'm not a big fan of longer-term outlooks. That's simply based on the extremely high likelihood that something completely different will happen. As Alan Watts often made the case, the future is nothing more than a prediction based on our past experiences.

Hence, as market drivers are almost exclusively events that break current trends, there's no surprise that most outlooks are flat-out terrible (what a way to start an outlook article...). In the not-too-distant past, these events were COVID, wars, and a mix of policy errors. 99.99% of market participants did not predict any of them.

To give you one of the best examples, the chart below shows past European Central Bank inflation predictions (not updated). One might assume that the smartest economists are good at this. Yet, it's just a highly flawed model that always ends up predicting the ECB's 2% inflation target.

Deutsche Bank

On the other hand, without an outlook, how do we build portfolios? Nobody has ever bought a stock without having some kind of expectation.

Hence, I like to focus on aspects with a high likelihood of occurring. These things include business cycles (easier to predict than certain events), political developments, and unavoidable situations (i.e., agriculture supply issues).

When combining this with stocks that investors understand, the odds turn in favor of investors - regardless of any black swan events.

With all of that said, let's start with the Fed.

What To Expect From The Fed?

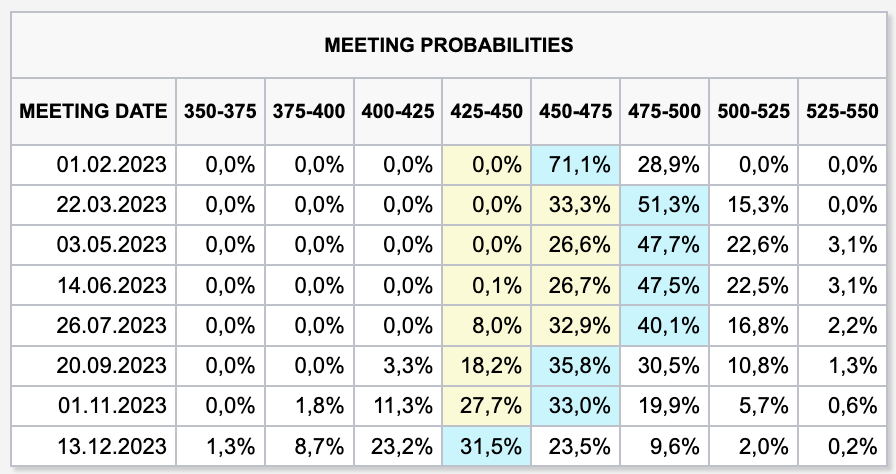

Two more rate hikes of 25 basis points to a Fed funds range of 475-500 basis points is what the market expects while I'm writing this. After that, the Fed is expected to maintain these rates until the first expected rate cut in September 2023.

{kind=link}

That's the consensus, meaning none of these future expected rate hikes should have a major influence on the stock market.

However, it needs to be said that the market is calling BS on the Fed's outlook. Market expectations are way more dovish than the Fed's dot plot, which looks for a terminal rate of at least 5.0%. Even in 2024, rates are not expected to come in (far) below 4.0%.

Wells Fargo

What matters are Fed comments. After all, these estimates are volatile and prone to big moves after economic data releases like inflation, unemployment, and related.

On December 14, I wrote an article titled "Buckle Up, It's A New Investment Era!".

The purpose of that article was to go beyond the short-term noise, as I looked at a changing long-term environment.

I believe that we're in a new long-term environment of above-average inflation, caused by secular changes like labor market dynamics, energy and commodity supply growth, and de-globalization (changing supply chains).

In that article, I quoted legendary investor Howard Marks' latest memo , which highlighted and compared major differences between now and the highly favorable period for stocks between 2009 and 2021.

{kind=link}

This is the part that stood out:

- While some recent inflation readings have been encouraging in this regard, the labor market is still very tight, wages are rising, and the economy is growing strongly.

- Globalization is slowing or reversing. If this trend continues, we will lose its significant deflationary influence. (Importantly, consumer durables prices declined by 40% over the years 1995-2020, no doubt thanks to less-expensive imports. I estimate that this took 0.6% per year off the rate of inflation.)

- Before declaring victory on inflation, the Fed will need to be convinced not only that inflation has settled near the 2% target, but also that inflationary psychology has been extinguished. To accomplish this, the Fed will likely want to see a positive real fed funds rate - at present, it's minus 2.2%.

- The Fed faces the question of what to do about its balance sheet, which grew from $4 trillion to almost $9 trillion due to its purchases of bonds. Allowing its holdings of bonds to mature and roll off (or, somewhat less likely, make sales) would withdraw significant liquidity from the economy, restricting growth.

Essentially, we're in a situation with two camps. On the one side, we have people that make the case that we're past peak inflation, with inflation being on its way to 0-2% due to the recession. They believe inflation was transitory after all.

On the other hand, we also have people that believe that we're past peak inflation. However, these people (I'm among them) believe that inflation will return in waves as higher economic demand will cause a quick upswing in prices again. This will likely be caused by the aforementioned issues and the fact that a dovish Fed will fuel rebounds in inflation.

It could look like something we witnessed in the 1970s and 1980s when inflation was volatile and prone to strong rebounds whenever the Fed took its foot off the brake.

{kind=link}

In other words, while I do believe that the Fed will eventually be forced to pivot, I do not see a return to accommodative central banks, the way we were used to between 2009 and 2021.

We also should not forget that while inflation has peaked, there is a lot more work to be done. Core service inflation is still close to 4%. When adding core goods, we get core inflation of almost 5%. That is barely below its peak.

Wells Fargo

The worst part is that the clock is ticking - at least until the first pivot. The Fed desperately needs inflation to come down to warrant lower rates.

As Lawrence McDonald says in a recent Fox Business interview , roughly $10 trillion in government bonds mature in 2023 and 2024. When adding higher interest rates, the cost of serving debt could rise from roughly $600 billion to more than a trillion! This will have a major impact on discretionary spending.

Especially as we head into the 2024 General Election, I have zero doubt that Democrats will be eager to spend big.

On top of that, a surge of roughly $400 billion in interest costs is bad for the budget in general. There is no time to waste for the Fed!

In other words, I can imagine we're in a long-term scenario that might look like this:

- The Fed is feeling tremendous pressure to control inflation. That makes sense as the US economy is consumer-driven. Also, high inflation can quickly turn into lasting above-average inflation once wages and spending habits adjust. That's a no-go!

- Hence, I believe that the Fed will not be scared to do damage to the US economy to achieve its target of lower inflation. This includes hurting housing demand/prices, unemployment, and consumer spending.

- Once the Fed pivots (I still believe it will happen in 2023), the economy will slowly adjust to lower rates. Demand will come back. So will inflation.

- Given the aforementioned secular factors, I believe we are in a prolonged period of Fed hikes and cuts at above-average rates (versus 2009-2021).

With all of this in mind, here's what I'm doing:

What This Means For The Market

While I am writing this, I have roughly 90% of my total net worth invested in the 24 stocks in my dividend growth portfolio (all of them are listed in my Seeking Alpha bio). That number used to be 94%. The decline is caused by my higher savings rate and the fact that I made a bit more money than usual in the past few months. I did not take any money out of my dividend stocks, and that's not going to change.

My goal is to maintain a higher savings ratio and a higher cash position in 2023. That is simply based on finding investment opportunities during market sell-offs.

After all, my thesis is based on economic weakness, which will likely come with some pain in the market.

Why?

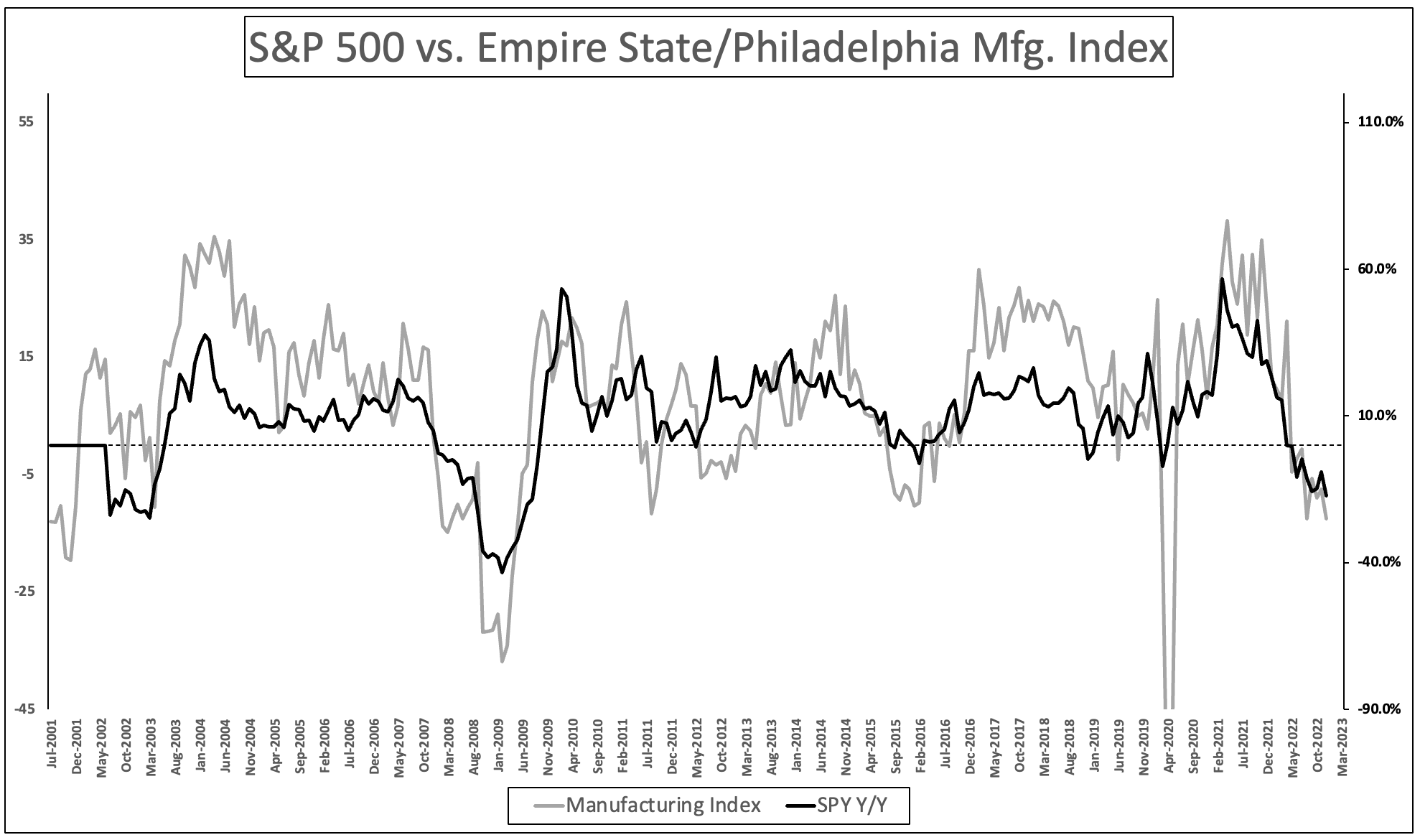

Because despite all the noise, the market is still driven by economic expectations. The S&P 500 continues to follow leading indicators like the Empire State and Philadelphia manufacturing surveys. And, for now, it looks like the economic downtrend is going to continue in the first months of 2023.

{kind=link}

The same can be said when looking at earnings expectations. If EPS estimates come down, the market suddenly won't look like a bargain anymore.

Bank of America

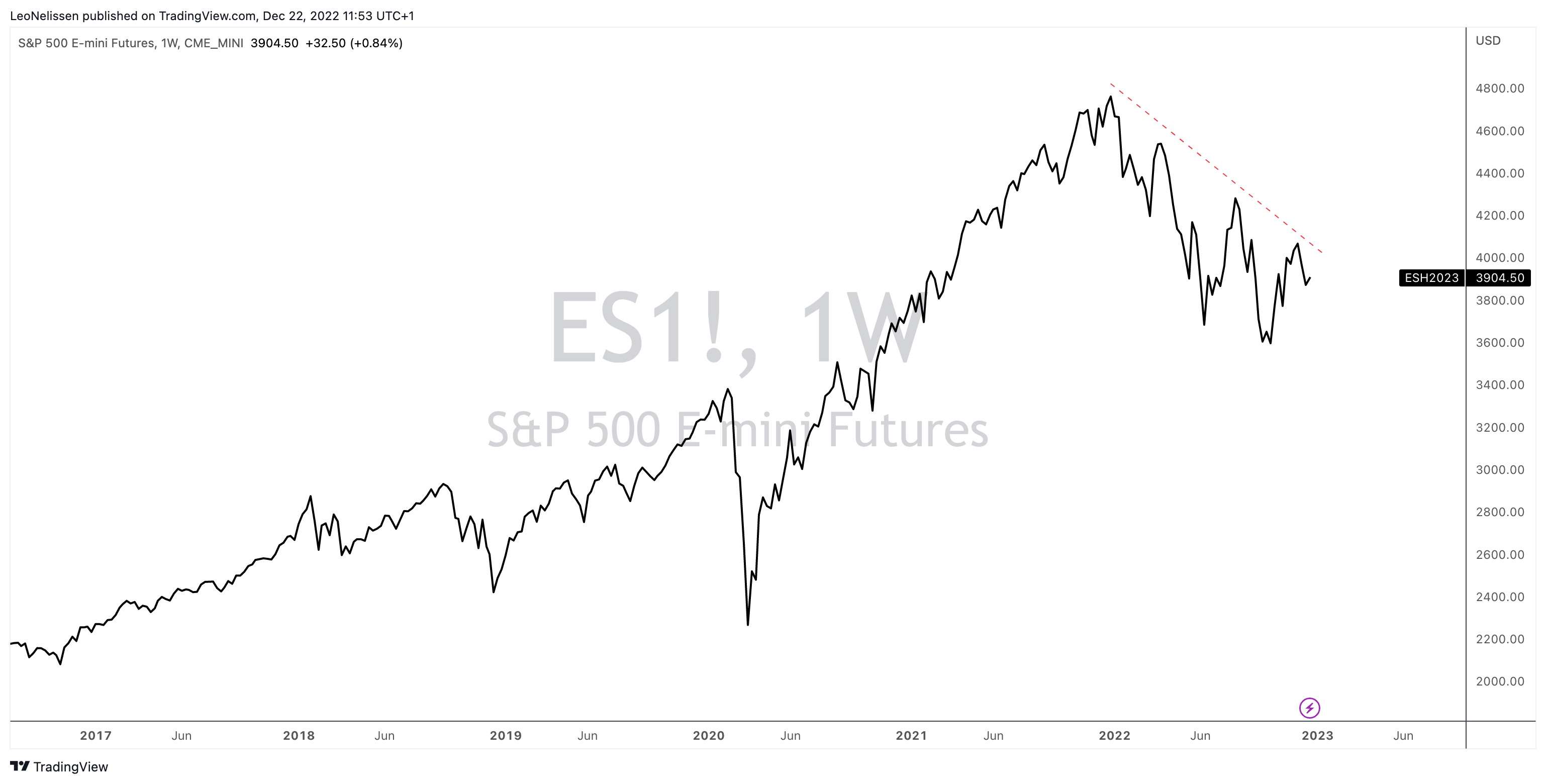

If I had to guess what everything we have discussed so far means in terms of market pain, I would say that I'm looking for a bottom in the low 3,000 points range. That would be a continuation of the ongoing downtrend, followed by more pain the moment the market realizes the Fed needs to see more pain before being able to pivot.

{kind=link}

However, when it comes to the end of the year, I have no idea where the market will end. After all, my thesis is a prolonged volatile sideways trend. On December 31, 2023, the market might trade anywhere between 3,000 and 4,800 points.

It isn't uncommon to see strong years in weaker long-term periods. After all, since 1928, the market had just four periods with consecutive down years.

- The Great Depression

- World War II

- 1970s Oil Crisis

- Dot-com

Bloomberg

In other words, when it comes to the market, I expect:

- More weakness in the first months (maybe quarters) of 2023 as slower economic growth and a hawkish mix pose a toxic mix. I think the low 3,000 might provide us with a bottom.

- A rebound once a potential pivot is positively impacting the demand side of the economy.

- A long-term volatile sideways trend for the market.

What I'm Doing

This has become a somewhat bearish article. However, I hold zero shorts, I'm not selling my long-term holdings, and I'm not going to bet against the market at any point.

After all, I am more afraid to miss market upside than to (maybe) make some money shorting derivatives.

My strategy remains to buy quality stocks on weakness. That's why I increased my savings rate and cash position as I already briefly mentioned.

Now, to give you some food for thought, let me provide you with a more detailed outlook and game plan (some food for thought)

Why I will stick to high-quality dividend growth stocks to protect my portfolio against recessions and other mayhem

In this article , I discussed the theory behind successful dividend growth investing. I also gave investors a model portfolio, which shows the fantastic benefits that come with a strategy like this. As my entire portfolio is based on that strategy, I will be adding to most of the stocks in that article in 2023 (whenever corrections occur).

Why I'm adding to energy stocks

In this article , (among many others), I explained why I believe that energy stocks are a great way to benefit from a long-term inflationary period. After all, it is caused by severe oil and gas supply issues, which keep prices high. Energy companies benefit from that as they shift their focus from production growth to shareholder distributions.

I'm looking for housing bargains

In this article , I discussed the housing outlook, the influence of the Fed, and why we're likely encountering highly attractive buying opportunities in 2023.

The housing market is showing cracks. I believe we're in a situation where we see gradual weakness in home prices and related economic indicators like GDP growth and unemployment. My view is that "smart" money is going to be right. We will likely encounter a situation where the Fed will be forced to pivot. That could be in the second half of 2023 if we assume that the Fed will keep hiking unless the economy becomes really weak.

At that point, we're likely dealing with higher unemployment and lower rates. That's when buying demand will come back roaring.

I'm a buyer of agricultural stocks on weakness

2022 was a terrific year for agriculture. I expect that to continue as I discussed in this article . Demand growth will be persistent, while supply growth is likely lower than expected. Add ongoing issues like fertilizer shortages, droughts, and an ongoing replacement cycle, and we get a great risk/reward for agriculture stocks. Hence, I will be adding to this industry during corrections as well.

I believe that we're in a new era for commodities. This includes energy, metals, and agricultural commodities. I do not think that the sudden upswing after 2020 will end in a sudden decline. I expect above-average prices on a long-term basis as supply growth is simply unable to meet demand.

Weather, lower fertilizer application rates, geopolitical tensions, and high operating costs will keep supply growth extremely subdued. Demand, on the other hand, will (more than likely) remain strong.

Takeaway

In this article, we discussed what I expect to happen in 2023 and beyond. I believe we're in for a bit more market weakness, followed by a prolonged sideways trend with volatile inflation, Fed rates, and a need for investors to buy/own high-quality dividend and value stocks.

Hence, in this article, I present a number of investment options I'm closely watching in 2023, as I still believe that it's too early to bet on the return to the market circumstances we enjoyed between 2009 and 2021.

The benefit of my strategy is that it's low-risk. It does not involve shorting anything. If I'm wrong and markets take off, I'm only missing out on some profits due to maintaining a higher savings rate. If I'm right and the market weakens, I get to buy more of my holdings at better prices.

Given that I have a long-term investment horizon, I'm very happy with this situation - at least given the circumstances.

Needless to say, I'll continue to update the situation as I'm sure the market will throw us some curveballs next year.

With that said, do you agree, or disagree? How are you preparing for 2023? Let us know in the comments!

For further details see:

Thriving In 2023: My Outlook And Strategy