TNGRF - Thungela: 200% Year-To-Date And Going

Summary

- Thungela's more than 200% year-to-date return and its 26.66% dividend yield seem justified.

- The company's profiting from an energy crisis, which has called on coal as a stopgap.

- Thungela runs a lean business model with a vertically integrated model.

- Its high-grade thermal coal sales has led to economies of scale.

- Railway issues persist. However, Thungela's set to steam through most systemic challenges.

Thungela Resources ( TNGRF ) is one of the most overlooked multi-baggers out there. The thermal coal miner is an Anglo American ( AAUKF ) spin-off that focuses on creating value by leveraging a vertically integrated business model. The company's CEO, July Ndlovu , is a savvy business person and a highly experienced coal miner.

Thungela's stock has skyrocketed by nearly 800% since its listing in 2021. We believe Thungela is one of the best energy stocks on the market; here's why.

Thungela's Tailwinds

The combination of global net zero ambitions and an energy crisis has led to a favorable arbitrage in the coal market. Many large-scale coal miners are offloading their assets to fund their go-green pivots, meaning the market's flooded with severely discounted acquisition opportunities. Why's this? Well, the long-term used case for coal is underestimated.

Secondly, a pending energy crisis has stimulated demand for coal. Thermal coal has been called back into action to backfill the energy shortages in Europe. Coal demand in the European Union jumped by 14% in 2021 and extended its run earlier this year.

Thungela has access to European market exports, and it's expected that the company will be one of the primary beneficiaries in the coming years as it produces low-cost/high-quality coal. Furthermore, Thungela hosts Eskom contracts , meaning it's a supplier to South Africa's state-owned energy producer. South Africa's energy mix is almost exclusively reliant on coal, making it the world's 8th largest coal consumer .

All of the above is parsimoniously conveyed by Thungela's illustrious profit margins and its robust return metrics. For example, the company's running on an EBIT margin of 54.19% , suggesting that it's achieved economies of scale, providing it with immense pricing power. Moreover, Thungela has an enormous return on invested capital ( 96.80% ), indicating that it holds a competitive advantage.

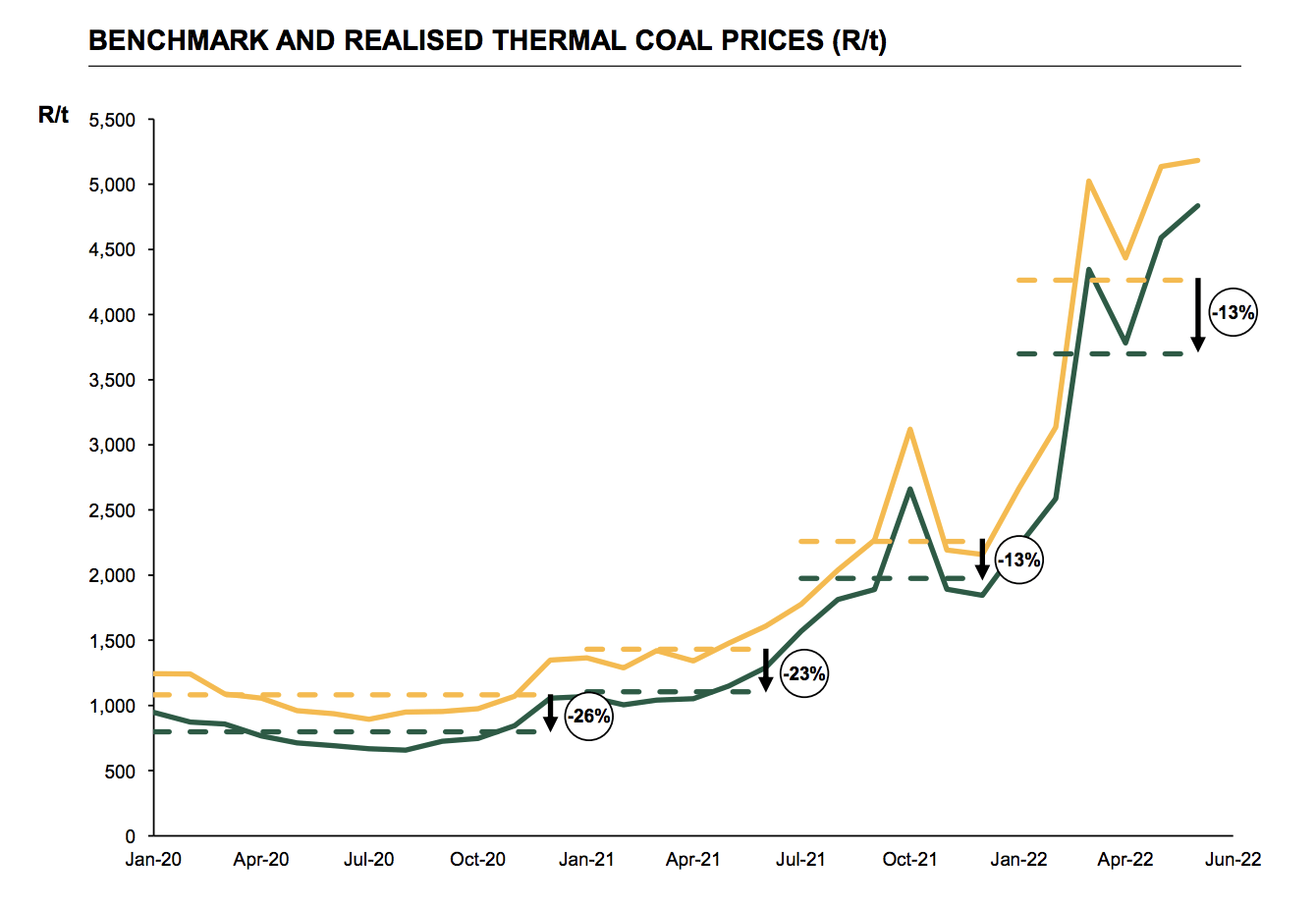

The last feature worth mentioning is the resilience of coal prices. It's probably trivial that proliferating demand will cause surging commodity prices. However, there's also a short supply in the energy arena, adding a secondary tailwind to coal prices.

{kind=link}

Operational Review

The company owns an interest in seven mines located in the Mpumalanga province of South Africa. Thungela operates both underground and opencast mines interlinked with processing facilities to establish a cost-effective, vertically integrated business model.

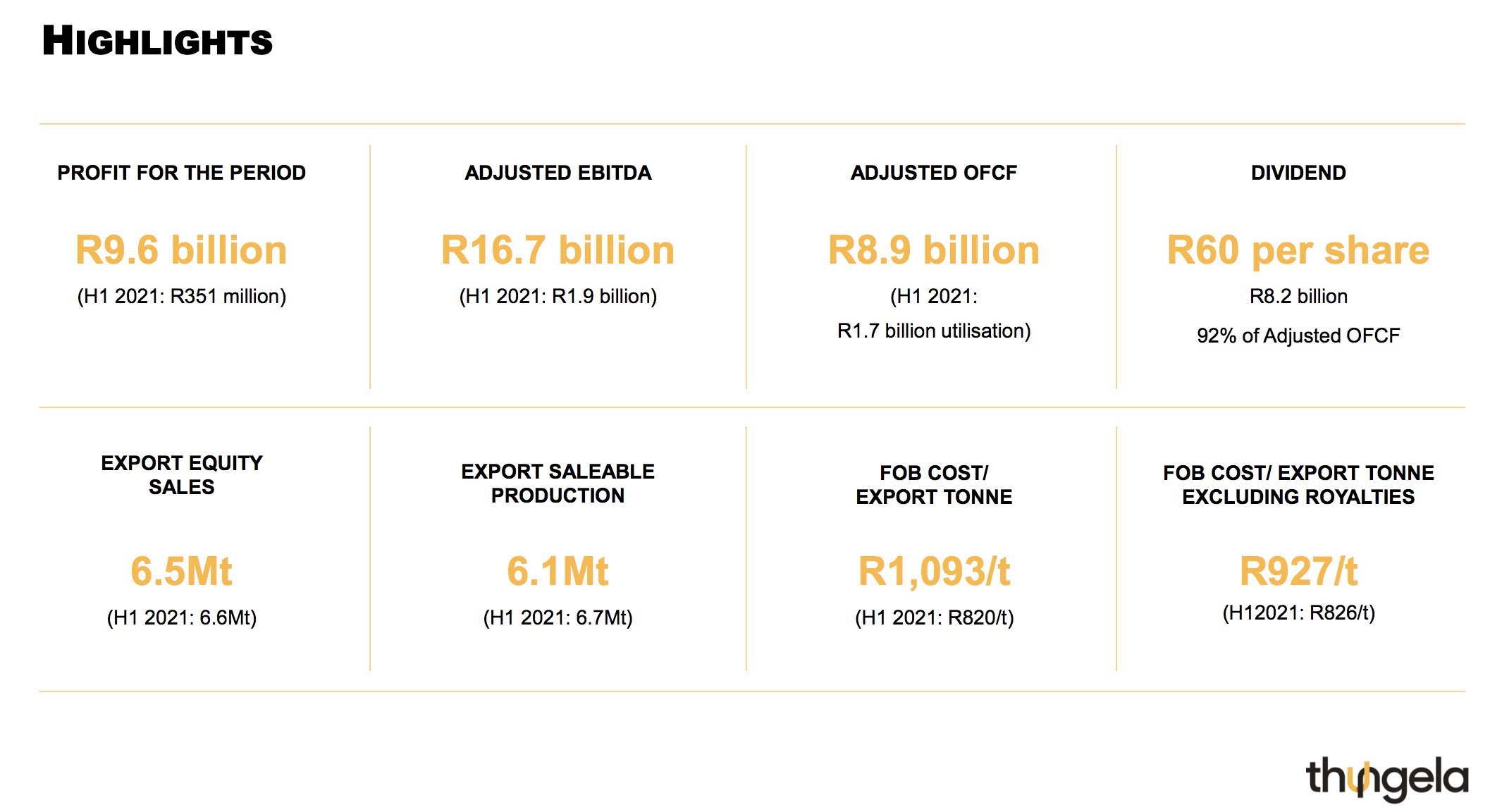

The company produced 6.1 megatonnes for exports during the first half of 2022, delivering operating free cash flow worth R8.9 billion (approximately $490 million). Moreover, Thungela delivered a promising outlook for its full-year 2022, stating that it expects export salable production to reach 13 megatonnes .

{kind=link}

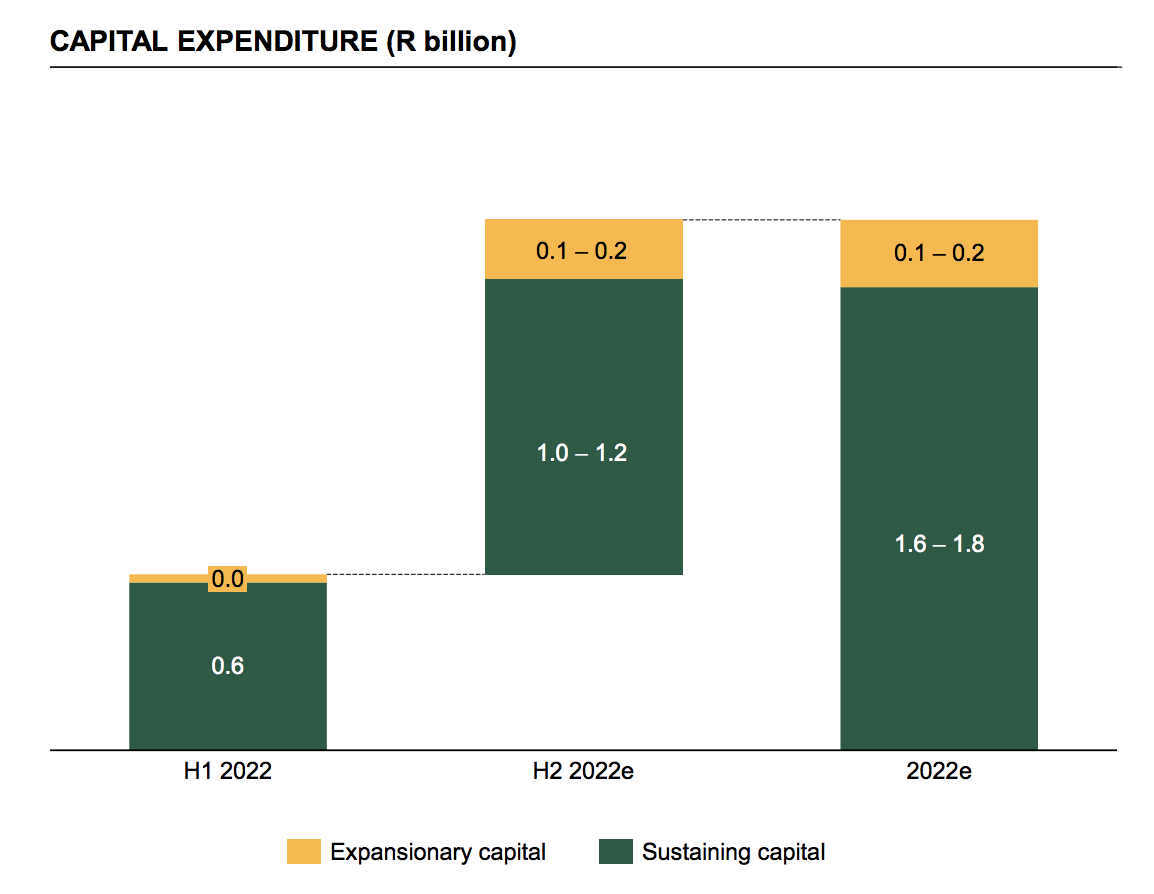

Furthermore, Thungela's attributing a portion of its CapEx to expansionary purposes, which relates to exploration and scientific feasibility studies. The majority of Thungela's recent CapEx was allocated toward sustaining costs. However, I believe this is temporary, as outlying inflationary pressure, opportunistic labor unions, and Covid-related maintenance costs wreaked havoc.

{kind=link}

Valuation & Dividends

Thungela's income-related price multiples suggest the stock's undervalued, as its price-to-sales and price-to-earnings ratios signal that the stock's trading at a significant discount. However, Thungela's is slightly overvalued on a price-to-book basis, which is something investors should consider unfavorable.

| price-to-earnings |

| 2.39x |

| price-to-book |

| 1.55x |

| price-to-sales |

| 0.85x |

Source: Seeking Alpha

The company's has a minimum 30% dividend guarantee (Adj. Operating FCF payout.) Therefore, it's safe to say that Thungela's enormous forward dividend yield of 26.66% could be sustained (for the time being). Additionally, Thungela holds cash per share of 6.99x, indicating that the stock's dividend safety is well-aligned.

| Dividend Yield (fwd) |

| 26.66% |

| Cash per Share |

| 6.99x |

Source: Seeking Alpha

Risks

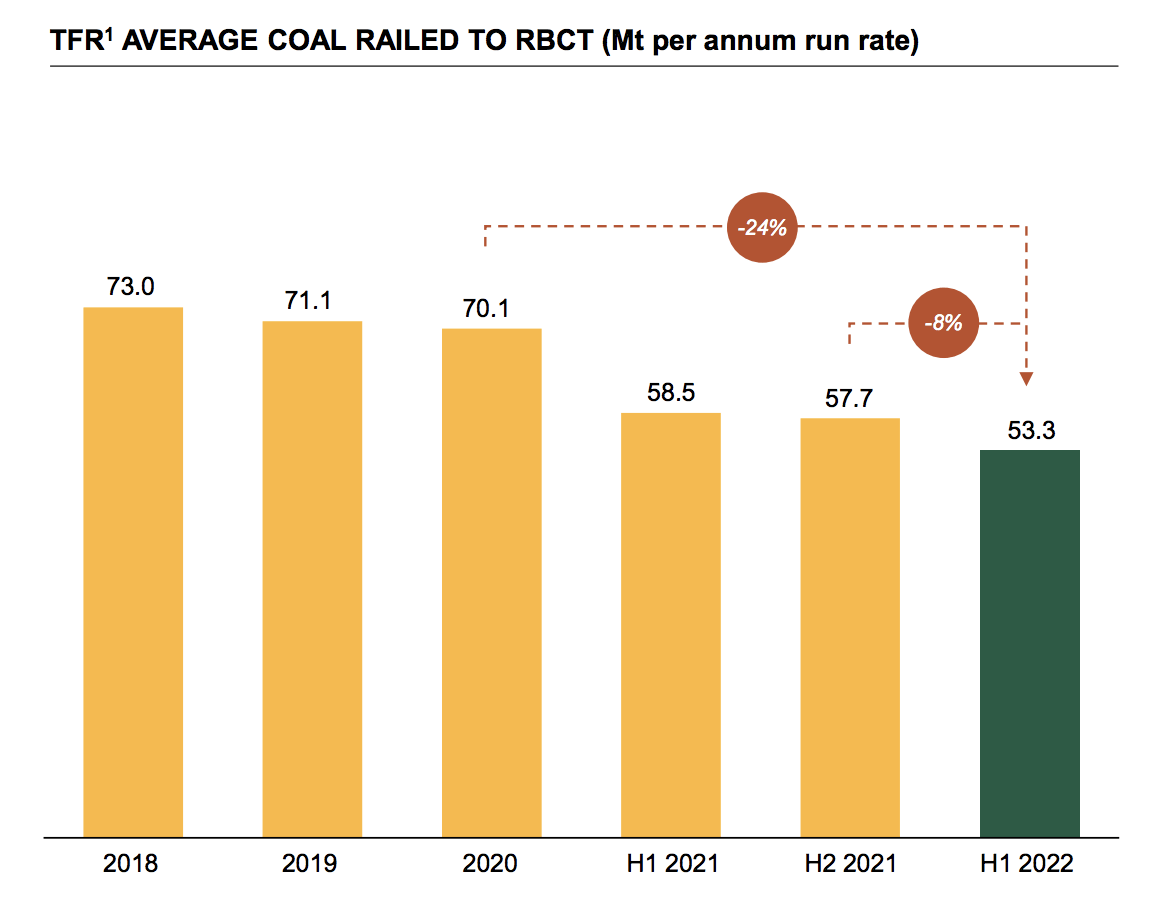

Thungela's risks are mainly systemic and beyond its own control. Many of South Africa's railways, ports, and logistical pipeline systems are defunct. According to PwC, South Africa could lose $4.5 billion in coal exports for the full-year 2022 due to theft and sabotage of railways. In addition, South Africa's national railway company's (Transnet) employees are currently on strike as inflationary pressure has lured demand for higher salaries.

The diagram below communicates the logistical issues, as the current run rate is approximately net 20% lower than it was before the country's mass looting in 2021 .

{kind=link}

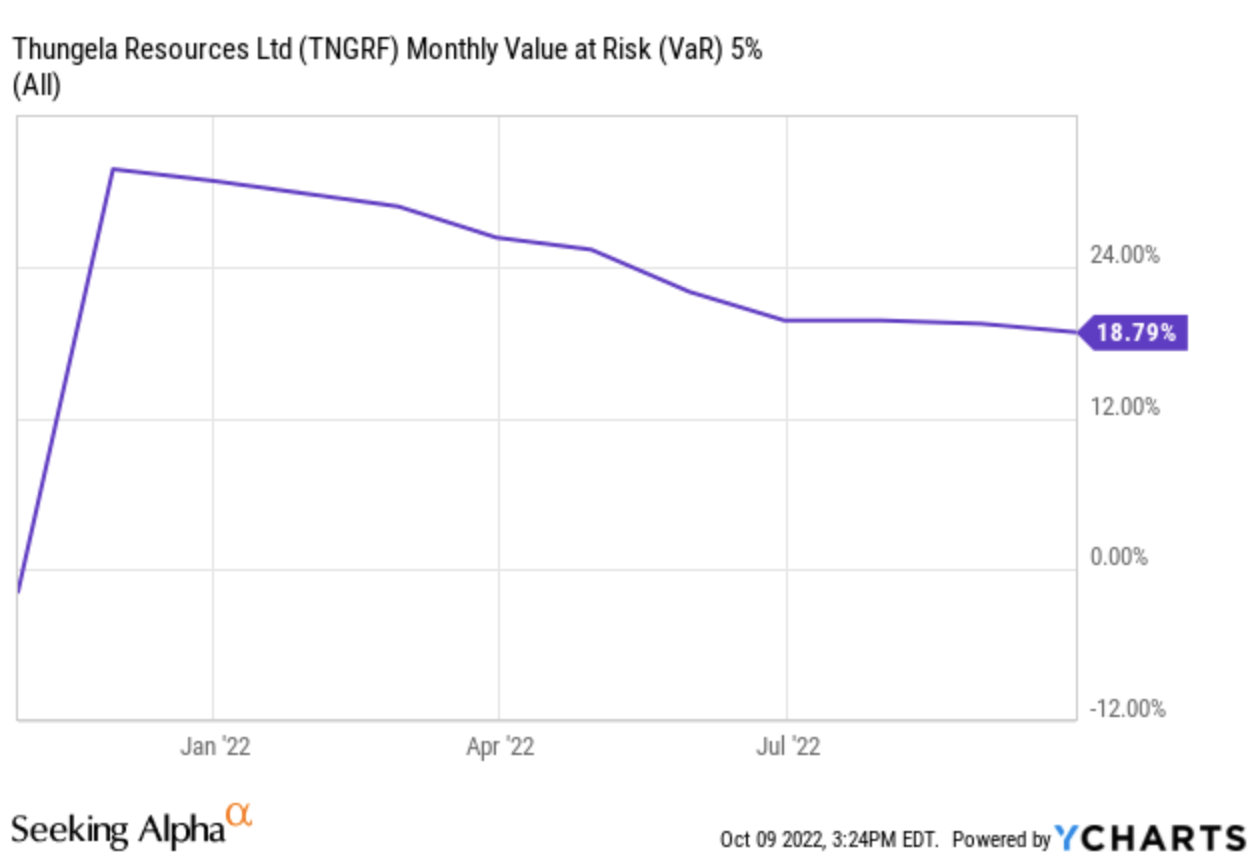

Furthermore, Thungela carries extensive market-based risk. The stock's 18.79% value at risk suggests it's likely to shed more than 18.79% of its value in 5% of its traded months, which is not what you want to see during a topsy-turvy market.

{kind=link}

Final Word

Thungela is one of the most overlooked energy penny stocks on the market. The Anglo American spin-off looks set to dominate South Africa's thermal coal market, with prospects of supplying European energy crisis with a vertically-integrated business model being a key tailwind. Moreover, Thungela holds a robust domestic sales footprint as a key supplier of state-owned energy producer, Eskom.

The stock's grossly undervalued and its surplus 30% dividend policy makes it an appealing bet in today's market climate.

For further details see:

Thungela: 200% Year-To-Date And Going