TNGRF - Thungela: The Canary Has Stopped Singing

Summary

- Multidecade low coal exports at Richards Bay explain why Thungela's latest production results were underwhelming.

- Export obstacles extend further than Eskom and wage strikes. Additionally, demand destruction from the Eurozone is likely en route.

- Although Thungela's Goedehoop mine continues to deliver robust results, most of its assets are underperforming.

- The stock's more than 35% ex-post dividend yield had many investors excited. Nevertheless, cyclicality could play its hand soon.

- The canary has sought new pastures.

We initiated coverage of Thungela Resources ( OTCPK:TNGRF ) in October of last year with a strong buy rating. Our analysis assumed that rising coal demand in the Eurozone would bolster Thungela's fundamental value, given the company's structural prowess. However, systemic risk has spoken. The South African coal export market is in dire straits, and the global energy supply is leveling.

We believe Thungela has reached its peak for the time being; here is why.

Operational Update

Thungela released its latest operational update in December, revealing subdued results.

Although coal prices have remained supportive, they exhibit severe volatility as the Russia-Ukraine war forced a new supply framework. Coal was a critical backstop to the Eurozone during the earlier stages of 2022, and momentum sustained into the latter stages of the year. Nonetheless, receding fossil fuel spot prices convey that leveling in supply/demand is occurring.

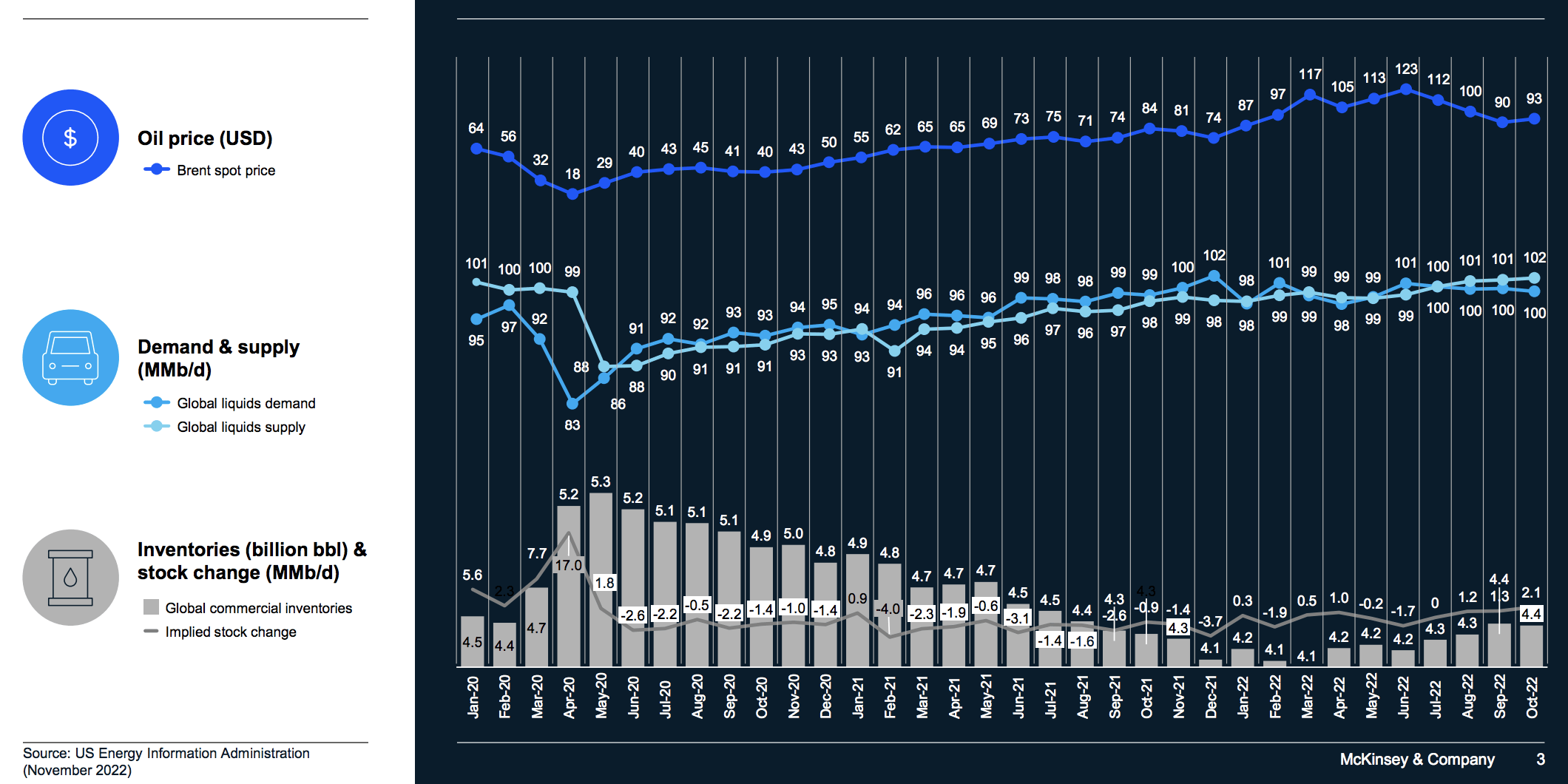

For interest's sake, recent data from McKinsey's (Exhibit 1) illustrates fossil supply/demand leveling.

{kind=link}

In Thungela's case, the company's coal has sold at a discount of approximately 15% to selective benchmarks. Moreover, the firm's lower grade coal is currently sold at a deeper discount.

A benchmark discount does not necessarily mean Thungela is suffering from slow demand. In fact, it might illustrate the company is competitive in the marketplace. Nevertheless, a broad-based drawdown in coal prices could severely compress the firm's profit margins.

{kind=link}

Thungela's Operations

Operational Headwinds

Before commencing to idiosyncrasies, it has to be said that the majority of Thungela's recent struggles have not been structural but instead systemic. For instance, the Richards Bay Terminal, which is South Africa's most significant coal export point, recorded its lowest traffic since 1993 . Many uninformed analysts will tell you that this is due to wage strikes from railway workers; however, based on our reasonable and objective basis, flowthrough to Richards Bay has been slow due to railway theft, abolishment, and general decay of infrastructure.

Furthermore, South Africa's energy crisis is a significant influencing factor. Eskom's inability to present power for longer than two-thirds of the day is damaging the prospects of South African miners, especially those that rely on exports like Thungela. In our humble opinion, Eskom's issues will persist into perpetuity as political games remain at fever pitch.

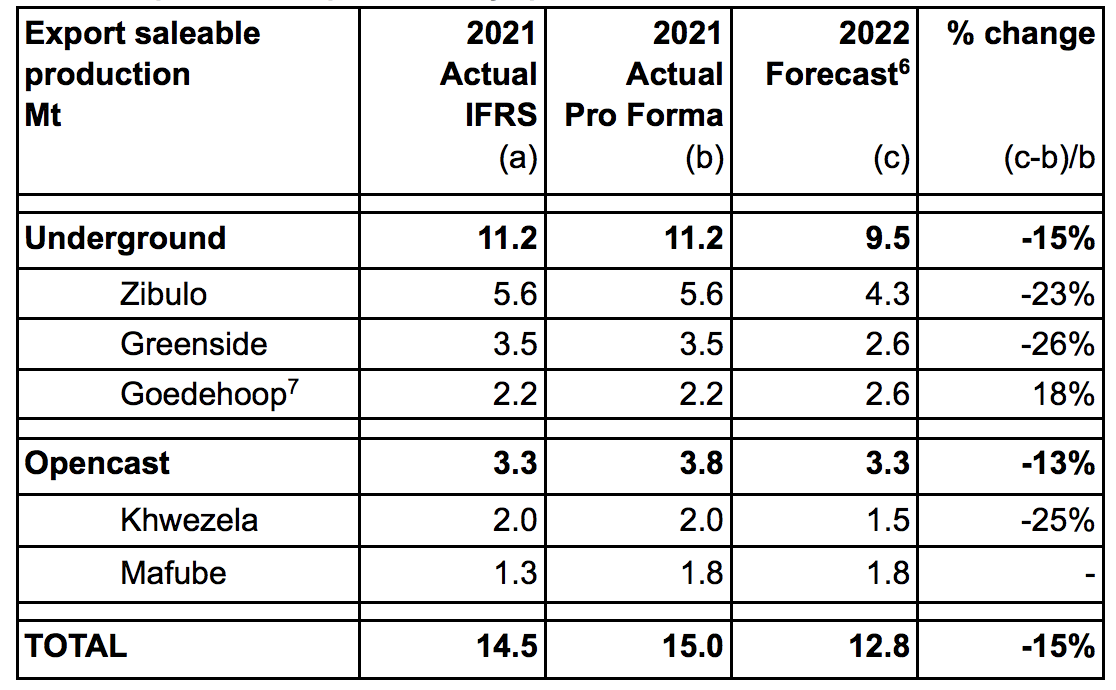

Underperforming Assets

Apart from a ramp-up at Goedehoop, all of Thungela's underground and opencast mines suffered from lower production in 2022. We believe much of the company's slump in production can be attributed to Eskom's woes. However, it must be considered that cyclical demand played its part, meaning Thungela probably tapered production with the expectation of lower future demand from the Eurozone.

Thungela is primarily an export-based company. Its Rietvlei operation is an exception, as it supplies locally to Eskom. Although Rietvlei is not faced with the same systemic issues as the company's export assets, it could find itself subject to demand destruction as Eskom continues to waver.

Exhibit 2. Note: Thungela's fiscal 2021 was during 2022. (Thungela)

{kind=link}

Valuation & Dividends

Thungela hosts various encouraging valuation metrics. For instance, the company's EV/EBITDA of 0.69 is impressive as an indicator of pre-depreciation value. Moreover, the stock is undervalued by 1.5 times its sales.

However, Thungela's price-to-book value of 1.2 presents an issue. Market participants often emphasize natural resource stocks' price-to-book ratios as they resemble the true worth of an asset-heavy business with quoted prices for its inventory. Therefore, an objective investor would have second thoughts before investing in this stock.

Furthermore, many investors may be overly emphasized on Thungela's retrospective dividend yield of 35.50% . Although its ex-post yield indicates shareholder proclivity, it does not determine Thungela's future payouts. In fact, we believe the possibility of receding coal prices and continuous operational risk could result in compressed profit margins, concurrently diminishing the stock's dividend yield.

A Glimmer of Hope

Despite all its temporary systemic headwinds, Thungela possesses scope for long-term success. The company operates low-cost mines with tremendous potential for ramp-ups. In our opinion, Anglo American ( OTCQX:AAUKF ) missed a trick by disposing of Thungela , as the company is extraordinarily well-managed and highly profitable.

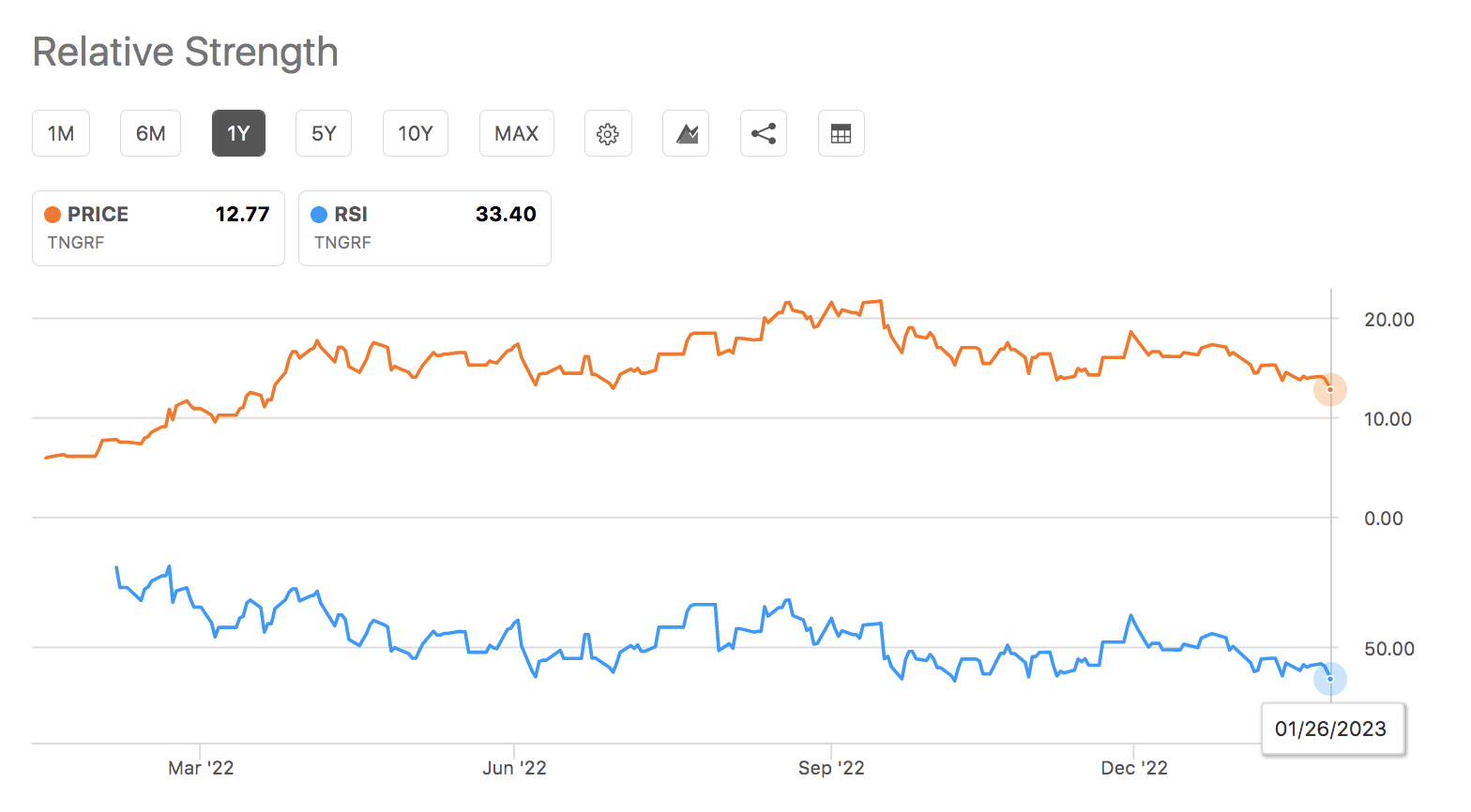

Furthermore, Thungela's recent drawdown could mean its stock has presented a value gap. With a 1-year RSI reading of merely 33.40, the Thungela's stock is near oversold territory, meaning a rebound is not out of the question.

{kind=link}

Final Word

We have decided to change our stance on Thungela Resources' stock. Based on our in-person observations and the company's latest production update, Thungela is up against it, with systemic risks being of primary concern. On top of that, a balancing act pertaining to energy supply in the Eurozone might taper the sporadic demand that coal received last year, consequently pegging back Thungela's valuation in the coming months.

- Sell Rating Assigned With A 6-Month Horizon.

For further details see:

Thungela: The Canary Has Stopped Singing