EVG - THW: Unsustainable Distribution; I Prefer THQ

Summary

- Tekla World Healthcare Fund is a healthcare-focused closed-end fund with $500 million in net assets.

- It pays a 9.2% market yield, or 10.6% of NAV yield.

- While there's no imminent risk to the distribution rate, there is a long-term gap between the fund's average annual total returns and its distribution rate. This causes long-term NAV declines.

- If investors can afford to accept a lower yield, I would recommend they switch to Tekla Healthcare Opportunities Fund, which pays a sustainable 6.8% market yield.

A few months ago, I wrote a cautious article on the Tekla World Healthcare Fund ( THW ), arguing that investors should look beyond its high distribution yield and focus on total returns. THW's strategies structurally trade off upside (by writing calls) in return for premiums that are paid out to shareholders as distribution. Therefore, THW's total returns underperform vanilla sector exchange-traded funds ("ETFs") like the Health Care Select Sector SPDR ETF ( XLV ).

While my concerns are valid, my thoughts on THW have changed in the last few months after conversing with many closed-end fund ("CEF") investors who hold the THW CEF and other similar high-yielding investments. For example, a retiree may be more concerned about high distribution yields to fund their retirement rather than maximizing total returns.

For those investors, I believe the most important aspect of analyzing a CEF like THW is not whether it generates the highest total return, but whether its high distribution rates are sustainable.

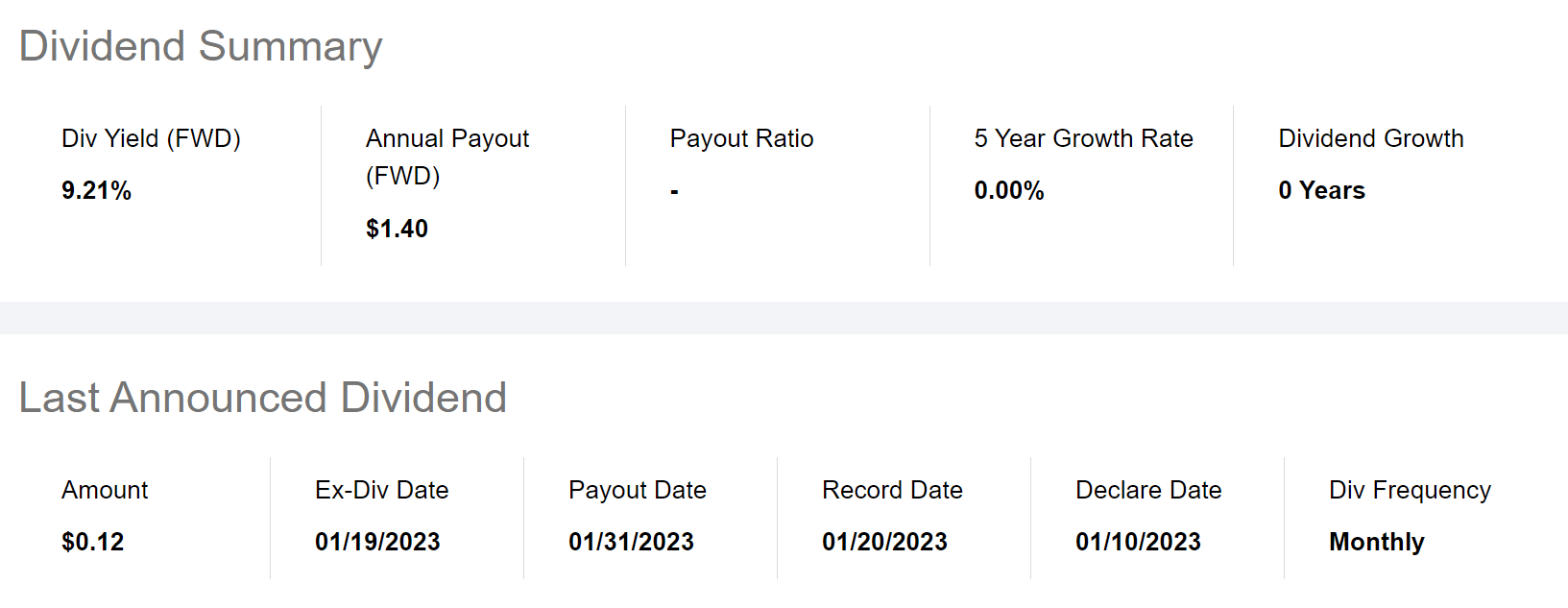

So, the purpose of this follow-up article is to assess whether THW's distribution, currently at $0.1167 / month or 9.2% current yield on market price or 10.6% on NAV, is sustainable (Figure 1).

{kind=link}

THW Uses Return Of Capital To Fund Distribution

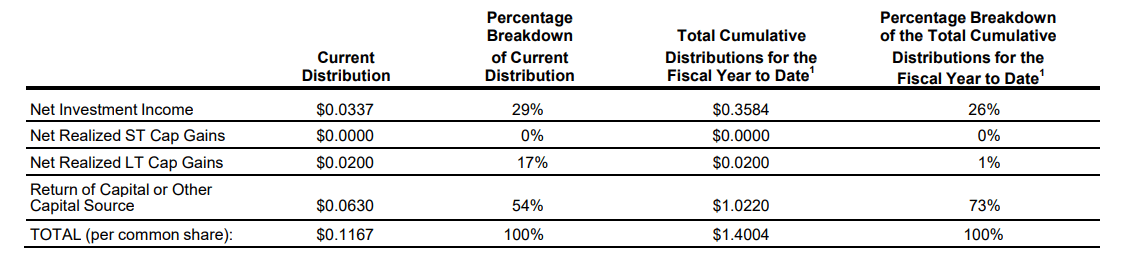

First, investors should note that THW's distribution, as I mentioned in my prior article, is not fully covered by its net investment income ("NII"). In fact, for the most recent fiscal year ended September 30, 2022, THW funded only 26% of its distribution from NII, while the rest was funded from capital gains and return of capital ("ROC") (Figure 2).

Figure 2 - THW funded distribution through ROC (THW September 2022 Section 19 notice)

{kind=link}

"Return of capital" is an accounting concept that tells the investor whether the fund generates sufficient income to fund its distributions. Funds like THW that hold some non-income producing assets like biotech stocks may not be able to fund distribution from NII alone. However, that does not necessarily mean its distribution is not sustainable. To determine if a distribution is sustainable, we need to consider the economic concept, "return of principal."

But Is It A Return Of Principal Fund?

In a paper titled " Return of Capital Demystified ," the investment firm Eaton Vance tried to dispel some common misconceptions regarding "return of capital." The following quote really resonated with me:

The best measure of whether a fund has earned its distributions is the change in its NAV net of distributions. Regardless of how distributions are characterized, if a fund's NAV increases, the fund earned its distribution. If not, the fund did not earn its distribution - the economic concept of return of principal

Unfortunately, the paper is no longer available , after I recently pointed out that Eaton Vance's Short Duration Diversified Income Fund ( EVG ) exhibited "return of principal" characteristics.

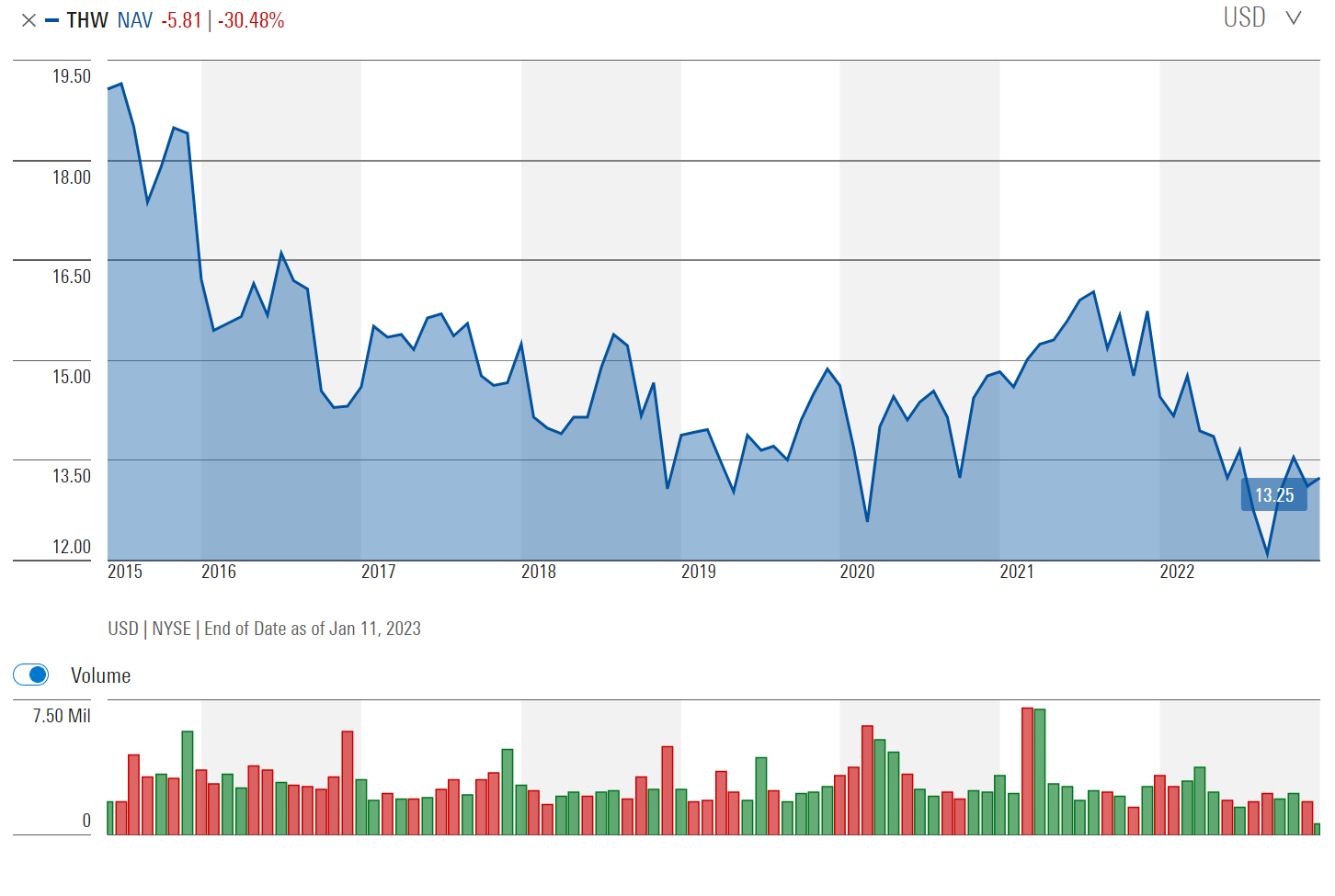

Using the long-term NAV metric, we see that THW's NAV has decline from $19 when the fund launched in 2015, to $13.25 most recently (Figure 3), or a CAGR decline of ~5%. This suggests that THW's distribution rate of $1.40 / year is not sustainable.

Figure 3 - THW's NAV has declined at 5% CAGR (morningstar.com)

{kind=link}

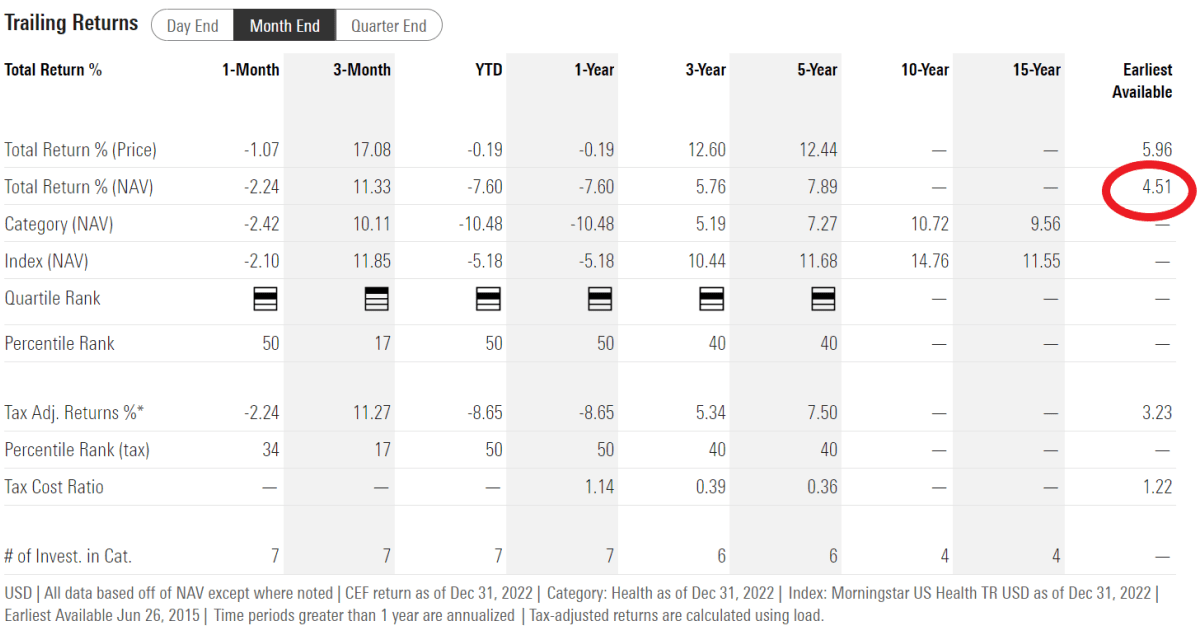

Another way to think about the sustainability issue is to look at THW's long-term average annual total returns. Since inception, THW's average annual total returns have been 4.5% of NAV (Figure 4).

{kind=link}

However, it is paying $1.40 / share annually in distributions, which equates to a yield of 7.4% of NAV when the fund was incepted to 10.6% of NAV at the most recent NAV of $13.25. Therefore, there has been a long-term shortfall in the fund's earnings (net income and/or capital gains), which resulted in long-term NAV decline used to finance the shortfall.

Since the fund's distribution rate has been kept constant from inception while its NAV has declined, the earnings shortfall burden has been increasing, year after year. While there is no imminent risk of a cut to THW's distribution, there is really only two long-term solutions to this problem. Either 1) THW increases its investment returns, or 2) THW amends the distribution rate.

THW vs. THQ

In a recent article , I reviewed the Tekla Healthcare Opportunities Fund ( THQ ). How does THW compare versus THQ? Does THQ also have a "return of principal" problem?

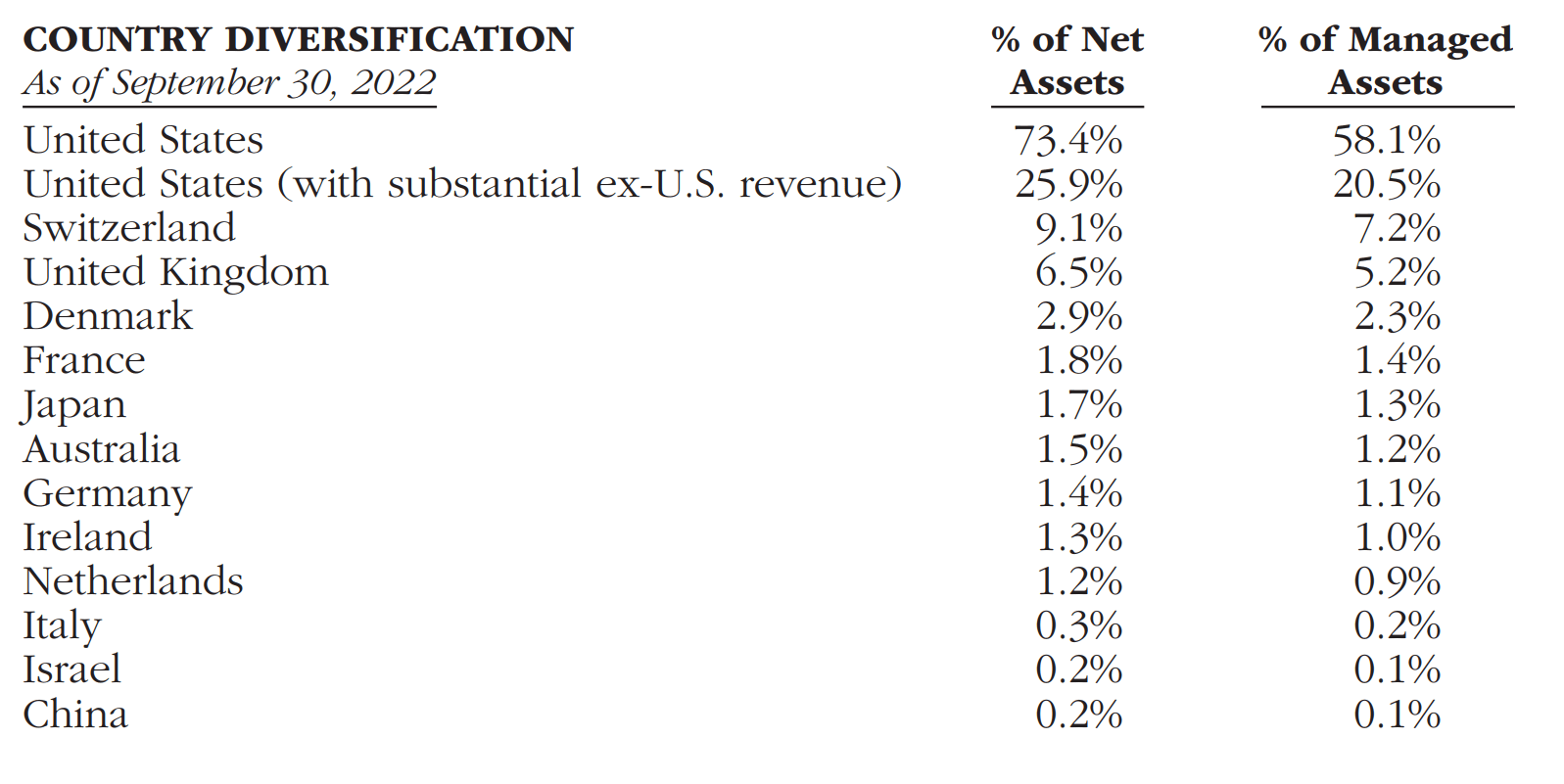

Both the THW and the THQ CEFs are managed by the same management team, led by Dr. Daniel Omstead. The key operational difference between the two funds is that THQ is a domestic U.S.-equities focused fund while THW has significant exposure to international equities and U.S. companies with substantial international revenues (Figure 5).

Figure 5 - THW has significant international exposure (THW 2022 annual report)

{kind=link}

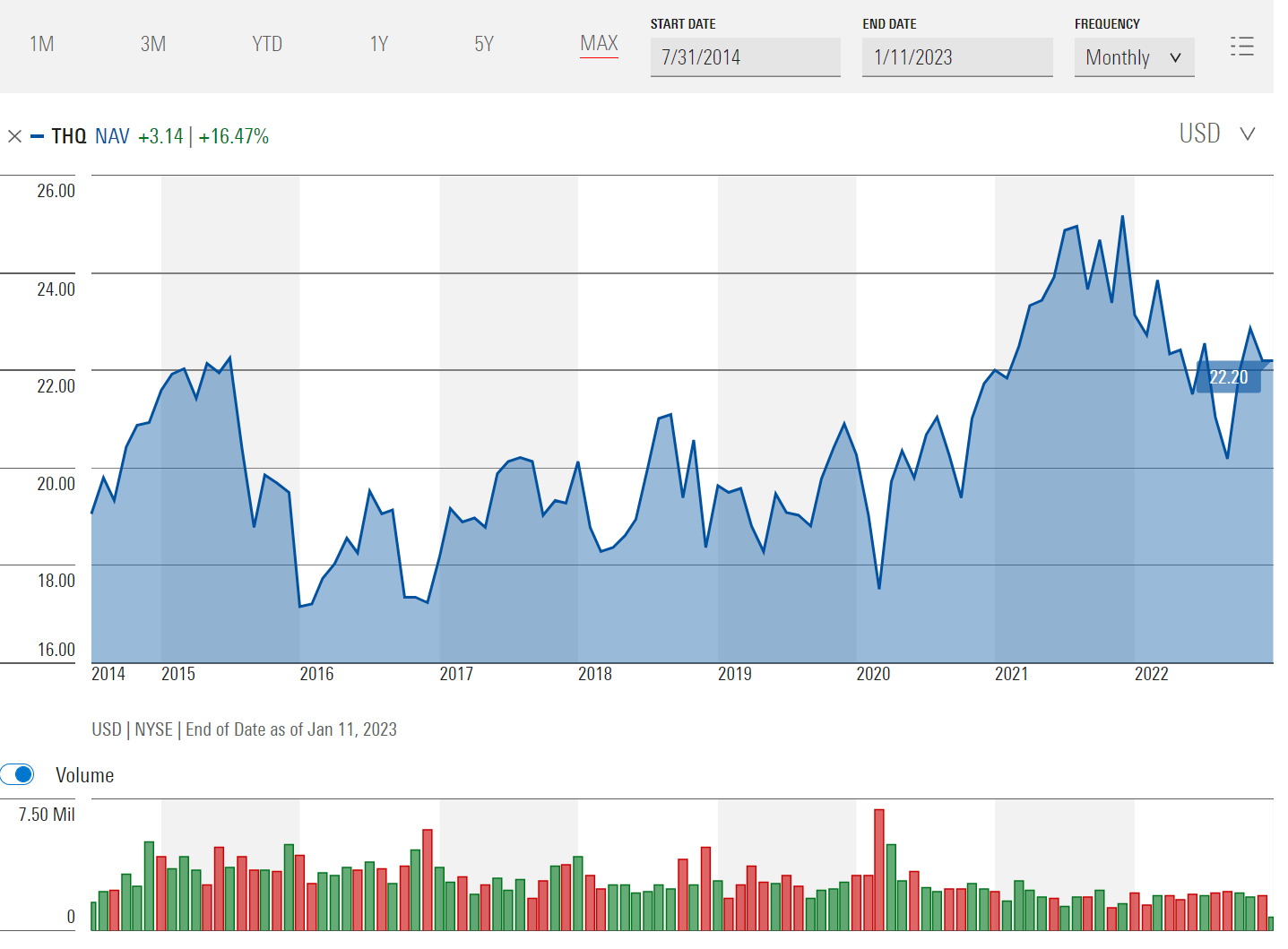

Figure 6 shows the historical performance of the THQ fund. Comparing figure 6 to figure 4 above, we can see that, historically, THQ has outperformed THW on all time frames.

Figure 6 - THQ historical returns (morningstar.com)

Another difference between the two funds is that THQ pays a distribution rate of $0.1125 / month, or a 6.8% yield on market price and 6.1% yield on NAV. In contrast to THW, I believe THQ's distribution rate is very sustainable because 1) it is struck at a lower rate than THW's, and 2) THQ has earned a higher average annual total return.

Visually, we can see that THQ's NAV has been steady to up since inception, indicating that its distribution rate is sustainable (Figure 7).

Figure 7 - THQ's NAV has increased since inception (morningstar.com)

{kind=link}

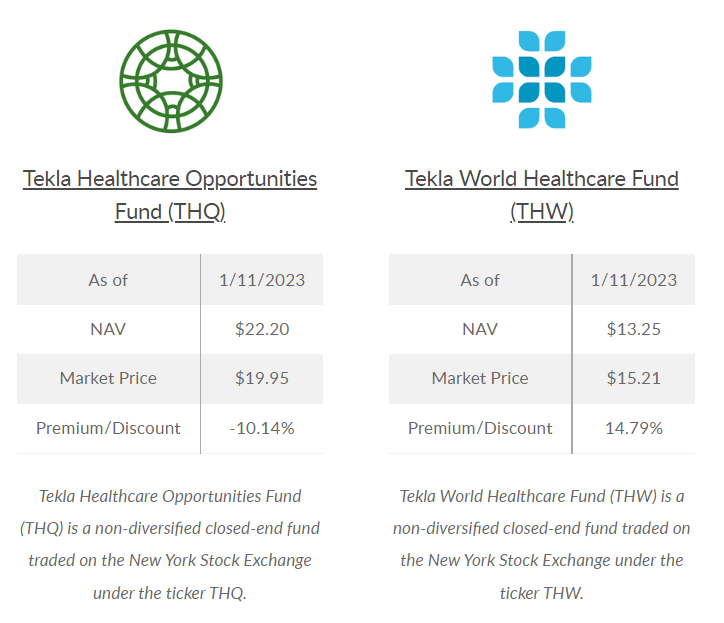

Finally, I should point out that the THW fund is trading at 15% premium to NAV while THQ is trading at a 10% discount to NAV (Figure 8).

{kind=link}

This was not always the case. Historically, both THQ and THW traded at discounts to NAV. However, sometime in 2020, THW caught on with investors and began trading at a premium (Figure 9).

Figure 9 - THW started to trade at a premium to NAV in 2020 (cefconnect.com)

{kind=link}

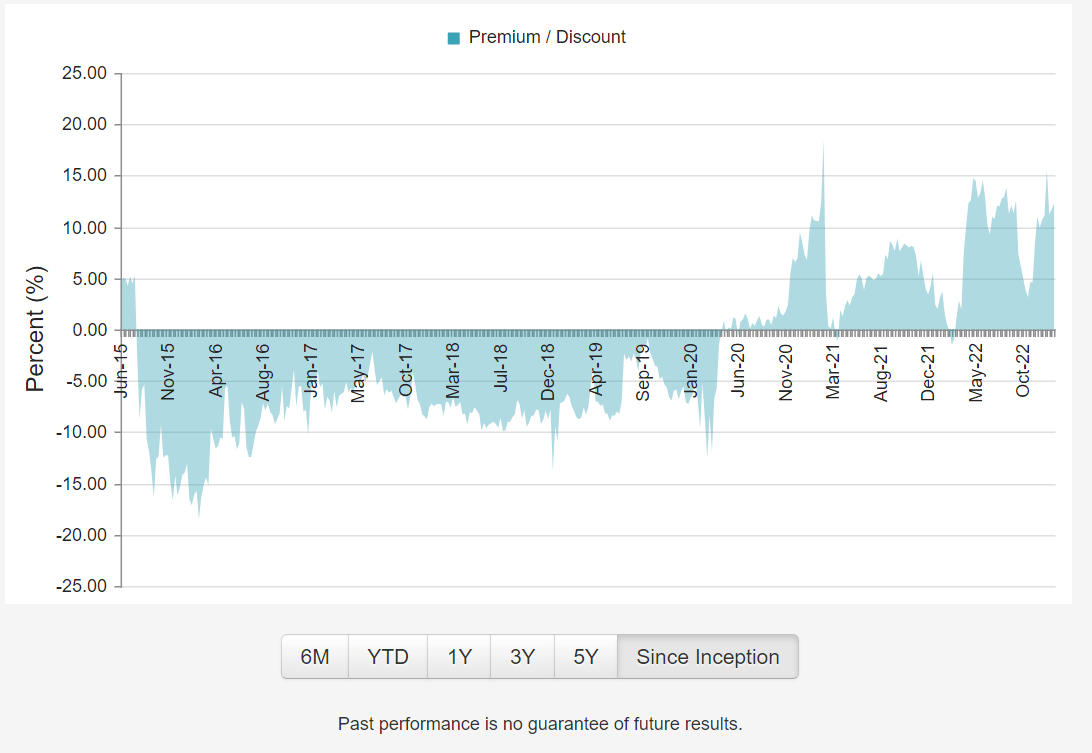

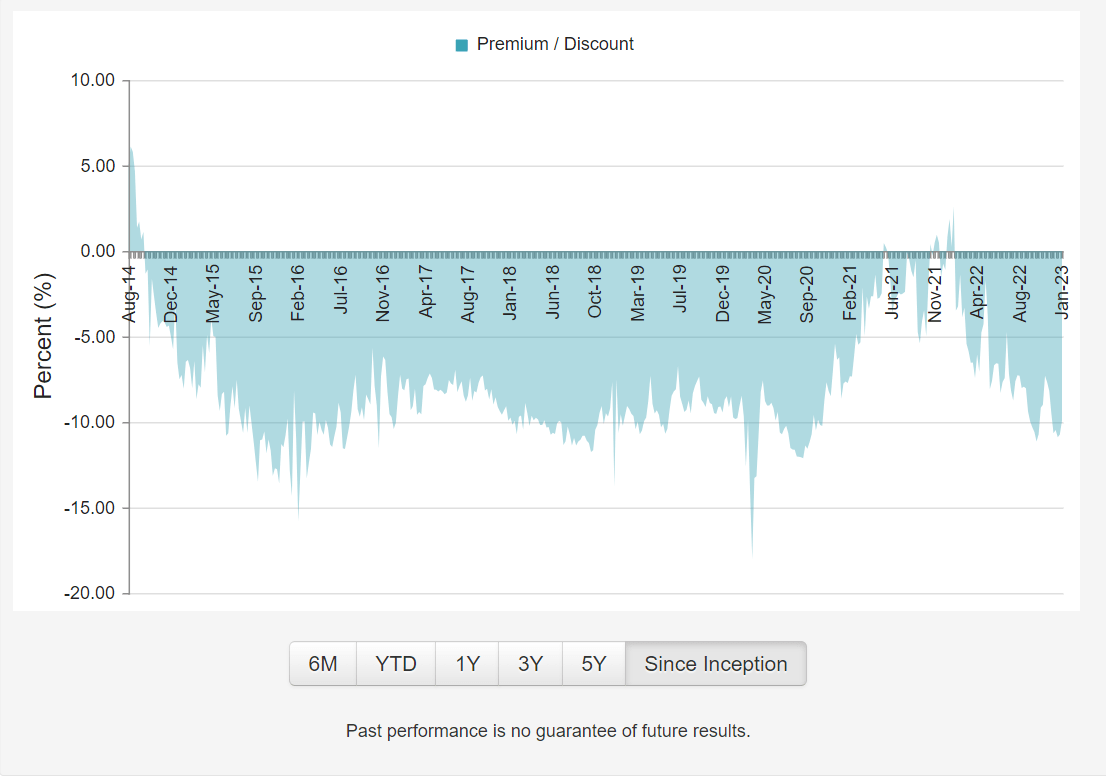

However, THQ remained trading at a discount (Figure 10).

Figure 10 - THQ continues to trade at a discount to NAV (cefconnect.com)

{kind=link}

While it is difficult to know when and if THQ's discount to NAV will be closed in the future, I think it is always better to buy a dollar's worth of assets for $0.90 instead of $1.15.

Conclusion

Looking through the lens of an income-oriented investor, I have concerns about the long-term sustainability of THW's high distribution, currently yielding 9.2% of market price or 10.6% of NAV. The main issue is that THW does not earn sufficient total returns, be it from income or capital gains, to fund its distribution rate. This leads to a negative spiral where its (earnings - distribution) burden gets heavier every year.

In contrast, the THQ fund, managed by the same management team, earns a higher return but pays a lower distribution yield, making its distribution long-term sustainable. Furthermore, the THQ fund is trading at a substantial discount while the THW is trading at a significant premium. Given the long-term risks to Tekla World Healthcare Fund's distribution from the (earnings - distribution) shortfall, I believe Tekla Healthcare Opportunities Fund is a better investment than THW.

For further details see:

THW: Unsustainable Distribution; I Prefer THQ