TKAMY - thyssenkrupp: 54%+ RoR In Less Than 8 Months Time For A Revisit In 2023

Summary

- My article on thyssenkrupp was underfollowed, underappreciated and "underliked", by which I mean that it received only a 12/20 like/comment ratio.

- However, I was firm in my thesis, and this was rewarded with a market outperformance by factor of over 10x.

- In this article, I'm revisiting thyssenkrupp to show you what I expect from the company in 2023.

Dear readers/followers,

When I wrote my article on thyssenkrupp ( TKAMY ) ( TYEKF ), not many of you actually either responded or chose to follow me here. I'm not saying that I have a 1-4% exposure to the company either - though I did "BUY" a fair bit of shares that ensures that my current upside following the result since my last article, is anything but trivial. thyssenkrupp is certainly a part of why my portfolio performed so well during the last year. Whenever a company performs like this compared to the market, that's cause for celebration, and having done something "right".

thyssenkrupp Article RoR (Seeking Alpha)

So, 10x'ing the market is certainly not a bad return here. I was clear when I wrote that article - we were looking at a triple-digit, 160%+ upside, and there was a very reasonable path from A to Z.

Now, over 6 months later, we're in a position where we need to revisit our thesis for this new year to see what we can expect from thyssenkrupp.

Ready? Let's go.

The continued Upside for thyssenkrupp is now muted - but still there

So, the company is still qualitative, and as I said in my initial piece, thyssenkrupp is really more of a conglomerate of various businesses than it is a stand-alone sort of business. The company has a now 23-year tradition, and it controls over 500 global subsidiaries, in large part controlled by the traditional form found in Germany - the family foundation model, added to by a stake from Cevian Capital, backed in turn by Icahn.

{kind=link}

The tradition is part of why you may want to look at thyssenkrupp. Because it has over 200 years of history when considering Krupp , this company has been around for longer than most countries in their current geographical configuration. The company was a weapons manufacturer for the Prussian Empire, Bavaria, and other parts of Europe. Had it been in the US, it might have provided supplies and weapons for the Civil war.

Now, for the past two centuries, thyssenkrupp and its constituent historical businesses, have been busily expanding. The latest iteration of the company has good activity in areas of steel, industrial materials, supply chain services, ESG, Hydrogen, and other activities, which in turn are reported in 6 segments.

And as I said in my initial article - that restructuring is still unfinished here.

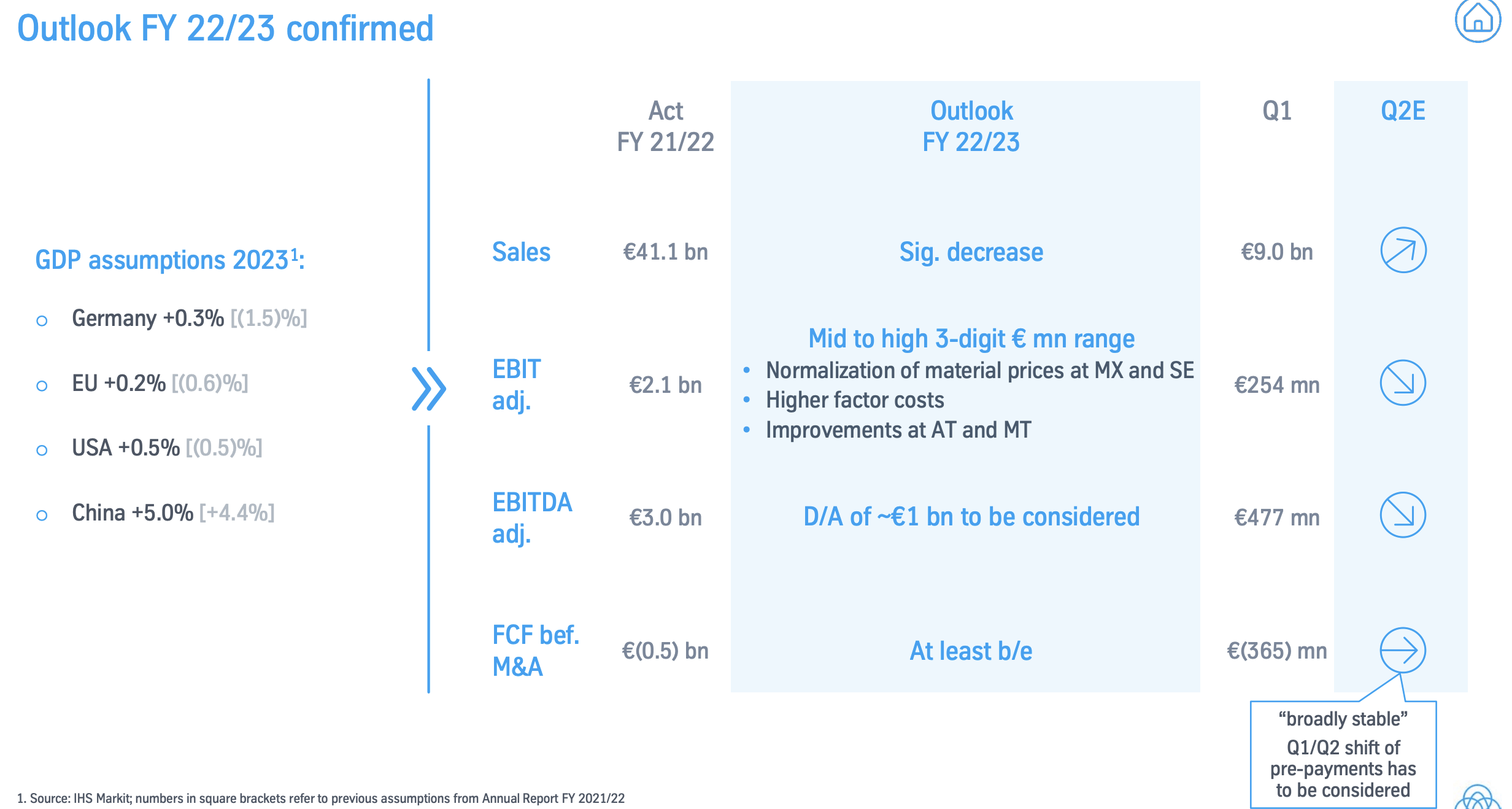

1Q22/23 is reported. The company continues to focus on strengthening its balance sheet, close to a 40% equity ratio, currently with a €3.7B net cash position and available liquidity of more than €7.5B. The company is in no way strapped for cash.

In terms of its business fundamentals, nothing has really changed. It's still an attractive set of operations with good assets, albeit located large parts in areas with elevated costs for energy and inflationary concerns.

{kind=link}

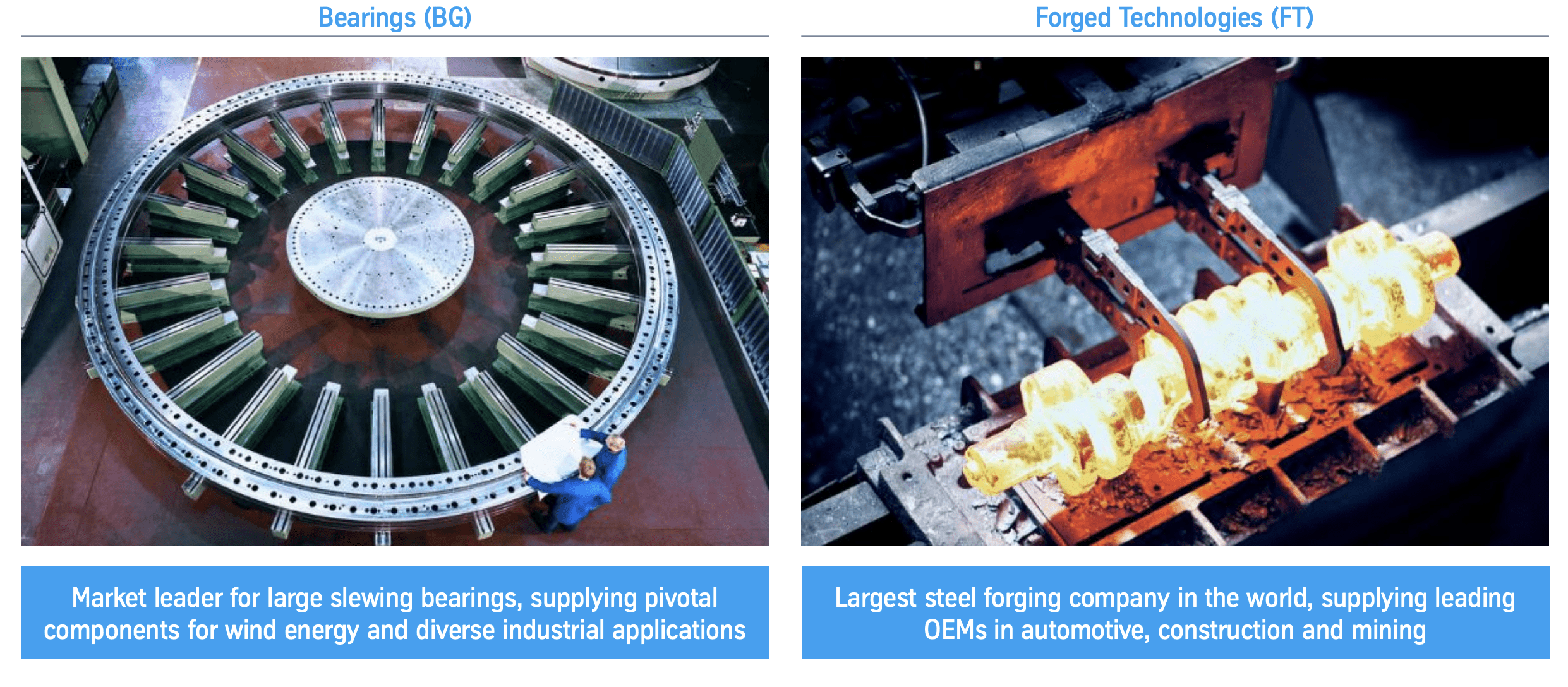

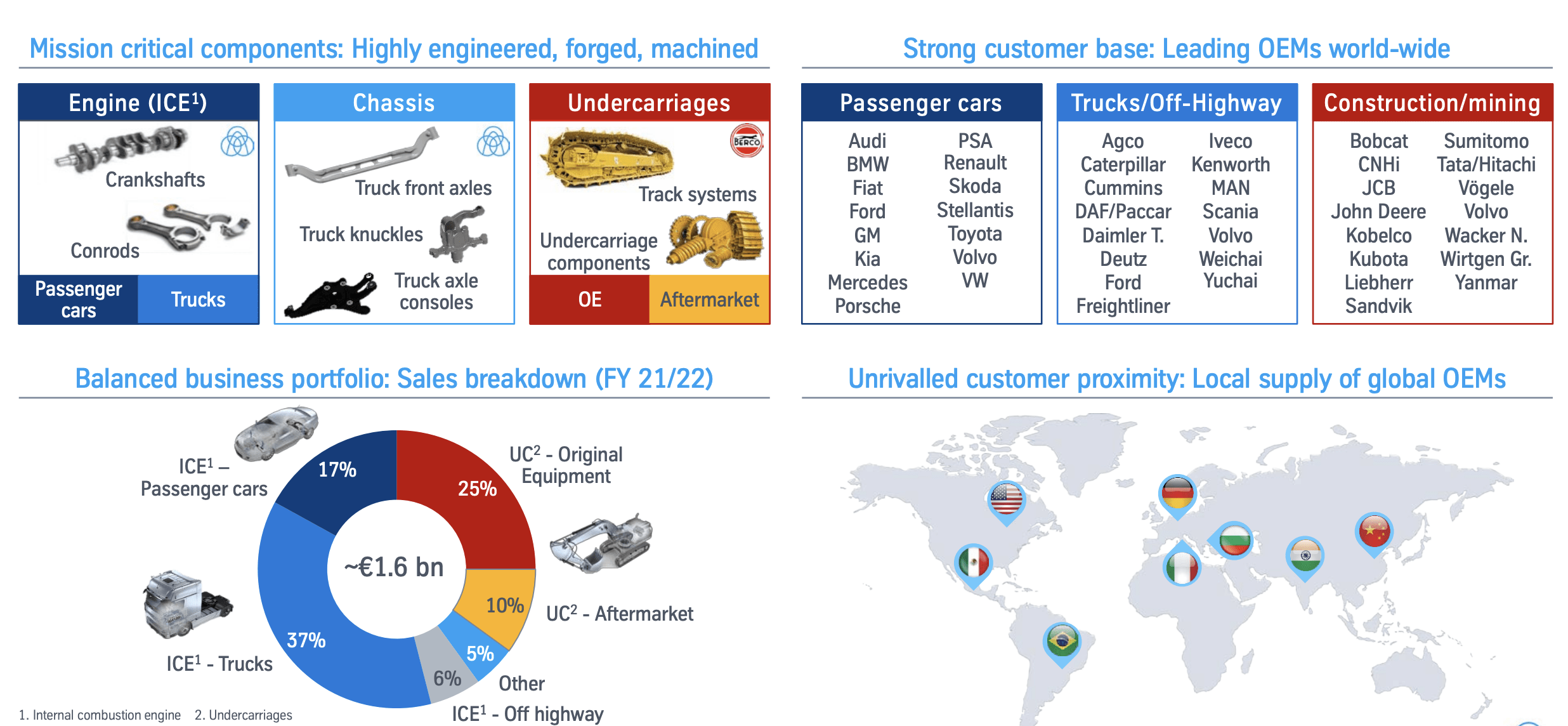

And these segments are in no way uninteresting. MX is a leading, mill-independent materials processor across the EU and NA with over 250k customers. IC is a market leader for slewing bearings of the large kind, which supplies renewables businesses as well as others, and with the largest steel forging company in the world that provides automotive OEMs, construction, and mining. AT is one of the leading suppliers to automotive, SE is the largest integrated European Steel Mill, with a leading role in decarbonization, and MS has a world-leading maritime portfolio. The list goes on.

My investment wasn't a "shot in the dark" - it was a calculated move on the basics of these businesses and the appeal they offer.

For the quarter, we saw a very nice growth in EBITDA (up 22% QoQ,) FCF up almost half a billion to positive, an 800+ bps in equity ratio, and a €2B reduction in pension liabilities. The company is considering its valuable stakes in Nucera and Elevator.

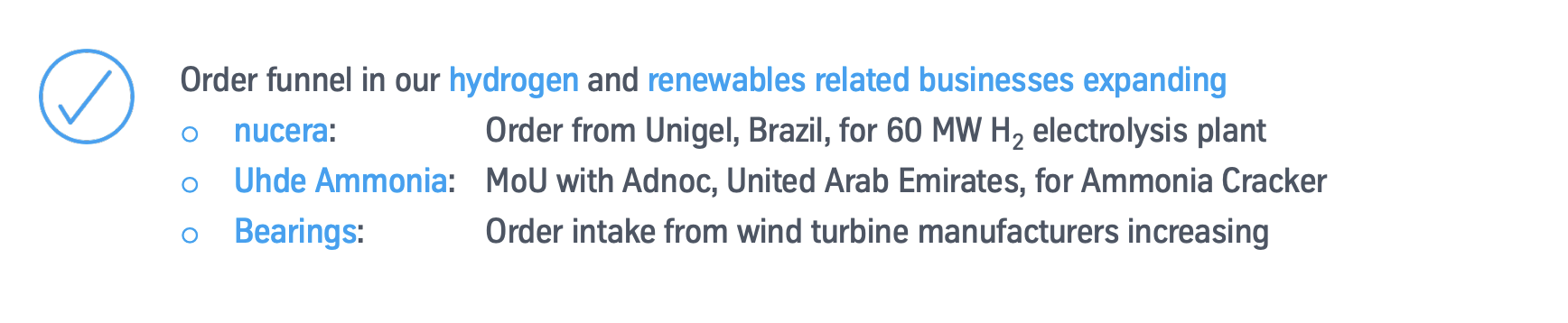

Transformation is still the buzzword that thyssenkrupp is continuing to use to describe its current operations. The company is working through the largest restructuring program ever handled in company history, with 10,000 FTEs already reduced, with significant, trackable performance initiatives both for the top and the bottom line. the company is working through its renewables expansions, with the following ambitions.

{kind=link}

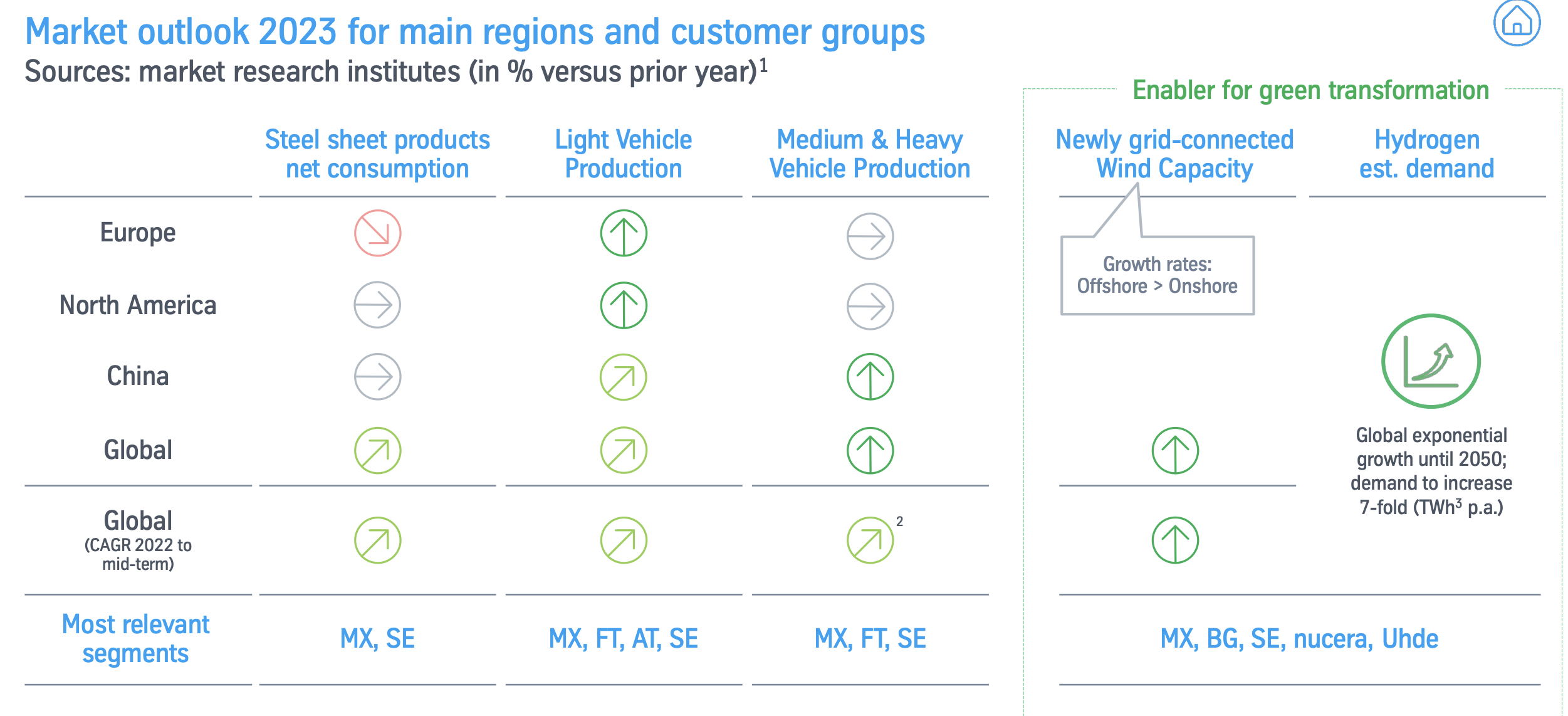

The company is already showing improvements here, with Net Working Capital at significantly lower levels than before due to a few reasons. FCF is good, and we're seeing early customer payments in most segments. Price normalization is ongoing for the company's various segments. The drawback of a company with so many segments is that various segments are going to be seeing wildly different trends - but generally, we're seeing higher costs, higher competition, inflation, and other issues. None of these challenges are unexpected or new as such, we've seen them across the business in all of Germany and Europe.

The outlook on a group-wide basis remains positive, even if Europe is more mixed.

{kind=link}

thyssenkrupp management expectations are in line with my own - the company expects slow macro stabilization in 1-2Q23, with a slow trend upward towards the second part of the year. China slowly normalizing, an auto sector that's working towards its backlog with SCM continuing to wind down in terms of challenges. Where I'm somewhat disagreeing with them is with energy price normalization. I don't believe we'll see that in Europe as quickly as estimates are saying here. So I'm forecasting that at a higher level. Also, I'm unsure how effectively thyssenkrupp and other companies will be able to pass along full cost increases to account for inflation and wage increases, given that there's a global competitive segment in many of these sectors.

To those things, we'll really have to wait and see what comes.

Still, thyssenkrupp has given us an outlook for the coming year, with the following targets.

{kind=link}

thyssenkrupp is expecting higher CapEx, though is careful to note that any spending will be restrictive given the current macro and implications here. The company is taking an approach though in that a chaotic macro can be a good thing, to capture potential opportunities - and this goes hand-in-hand with the company's history as a wartime manufacturer and supplier of products.

Examples include the strong USP in naval shipbuilding, taking the opportunities to more efficiently handle its global supply chain, adjust utilization to demand, and implement better processes. The high-level restructuring plan is going well according to the plan here as well, with 13,000 targets seeing 10,000 achieved, 6,000 of which are in the German geography alone.

There is also still a fair bit to go here.

{kind=link}

At times, it is very surprising to me that the company does not perform even far better than it is. I say this because of the degree and amount of mission-critical components across the board, that is being manufactured by the company. These are non-trivial things that cannot be matched by many other manufacturers on earth, and where thyssenkrupp has customers that include virtually every single company that matters on earth in their respective segments.

{kind=link}

And such graphs could be shown for virtually every single segment here. The macro remains problematic, but the company continues to produce vital components and is in the midst of a massive transformation.

Still, the risks are definitely still there. thyssenkrupp remains junk-rated at BB-, BB, and Baa3 from Fitch, Moody's, and Standard & Poor's respectively. The dividend policy/statement is somewhat disheartening as well, with a target to "Dividend payment as a clear target".

What can be stated as positive is that the company is expected to deliver positive EPS for the next few years, which should enable thyssenkrupp to also deliver a dividend payment to shareholders. However, having realized a massive RoR in my position, I'm not complaining here.

Let's look at the valuation and see what we can do here.

thyssenkrupp Valuation - the upside is still there

Now, to be clear. Analysts have shifted their targets downward. a €15/share native PT last year is now down to €10, with a weighted average of around €9.5 for the 9 analysts still following thyssenkrupp. I consider the company to be underfollowed and underappreciated.

5 Out of 9 of these analysts are considering the company a "BUY" or a similar rating, from a range of €6 on the low side to €17 on the high side. I am not changing my own PT from €15 here, because insofar as what has happened since I last wrote about the company, I don't believe anything has materially changed or is expected to change for thyssenkrupp in 2023. The company's various upsides that it points will likely be offset by the challenges we see from inflation and energy.

This still leaves us with an undervalued, global steel producer, and one of the most well-known names in Germany.

If you're in any way a long-term investor and willing to shoulder a bit of timing risk (in the sense that it's completely uncertain just when things will actually turn around), the potential returns you could generate from an investment in this company are nothing short of amazing. it's entirely possible that we'll see similar returns to the ones we saw the last 7-8 months.

Using peer-similar NAV multiples to evaluate the company fairly, as well as DCF is tricky since the company is in the middle of a sales, divestment, and IPO process. I believe it is better to use peer multiples and discount them, as well as to look at what is expected on a long-term basis, even if those long-term forecasts are also subject to extreme uncertainty.

You can compare this to peers like ArcelorMittal ( MT ), JSW Steel, Nippon Steel, Reliance Steel ( RS ), Gerdau ( GGB ), and others, many of which trade at revenue multiples close to 1-1.5X and EBITDA multiples that are closer to 5-7X, which is a significant premium to where the company currently is and was back when I wrote about it a few months back.

Consider for a second that thyssenkrupp has mostly realized its 2022E targets this year, and this discount will slowly cease to make sense - at least that is how I see it.

I'll still apply a discount to thyssenkrupp - 20% to reflect the company's Euro focus, which is under heavier fire and effects, but that still leaves an upside of almost 40% to any sort of conservative target, with an implied peer-based PT of €10.5/share. But that's just peer, not other targets, because thyssenkrupp to me, is clearly undervalued based on its positive earnings forecast and realistic expectations. In fact, in terms of working capital, the company did far better than I expected - even if inflation and energy came in worse than I expected back last year.

Nothing changes that we're picking up thyssenkrupp dirt-cheap. Because of its no-dividend, it's not a core investment for me, but it's a company that I very much consider a valid sort of "BUY" here.

Here is my thesis on TKA.

Thesis

- thyssenkrupp remains one of the more interesting global plays on steel, forging and the steel sector in Europe. While there are peers I've made money on that are not thyssenkrupp, like Gerdau and Arcelor, I consider this one, despite its 50% RoR in the last year, to still have an upside. I added to it not that long ago, and I will continue to hold and build my position in the business.

- thyssenkrupp is undervalued on the basis of NAV, Peers, and forecasts - because of that, my rating for 2023 for the company is a very clear "BUY".

- My PT for thyssenkrupp remains at €15/share native.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The only flaw with thyssenkrupp, aside from its credit rating, is the lack of a dividend. But in those case, I still consider it a "BUY" here.

For further details see:

thyssenkrupp: 54%+ RoR In Less Than 8 Months, Time For A Revisit In 2023