HD - Tile Shop: A Mispriced Security

2023-05-01 09:05:46 ET

Summary

- Tile Shop trades at a significant discount to comps following events unrelated to underlying business operations.

- Based on the comp set currently, there is almost 3x upside potential in Tile Shop from re-rating to peers.

- With significantly higher product margins compared to peers in the flooring industry, continued focus on streamlining SG&A may be key in tapping into the operating leverage capabilities.

- It is expected that tile will continue increasing in popularity taking industry share from hardwood and carpet.

- Peter Kamin and Peter Jacullo are focused on returning capital to shareholders.

Thesis

I've developed my thesis for Tile Shop ( TTSH ) around the price/earnings framework to simply break down the potential upside for investors.

- Price: Tile Shop trades at a significant discount to comps following events unrelated to underlying business operations. After a surprise de-listing announcement from the board in October 2019, the stock fell 66% in a day, erasing ~$100mm in equity value. Based on the comp set currently, there is almost 3x upside potential in Tile Shop from re-rating to peers.

- Earnings: With significantly higher product margins compared to peers in the flooring industry, continued focus on streamlining SG&A may be key in tapping into the operating leverage capabilities. If OPEX efficiencies drive EBITDA margin uplift, I believe Tile Shop can re-rate to peers.

Business / Industry Overview

The Tile Shop is a specialty retailer with a specific focus on natural stone and man-made tiles. They offer over 6,000 products from around the world with the majority being sold under two proprietary brands, Rush River and Fired Earth. Tile products, accessories, and tools are purchased from a global network of suppliers while the company manufactures its own setting & maintenance materials. Tile Shop has grown revenues at an annual rate of 2.8% over the past 5 years relative to industry growth of 1.3% in the same period. 2x the industry growth can be chalked up to two specific competitive advantages for Tile Shop:

- Broad Product Assortment & Attractive Pricing: 6,000 different products that are priced attractively due to their economies of scale, direct tile purchasing, and manufacturing of setting & maintenance materials in-house. Tile Shop ranks #1 in the industry in terms of pricing.

- Customer Experience: By operating solely in tile, employees are trained exclusively in this niche allowing them to deliver a higher quality customer experience. Tile Shop differentiates itself from the competition by allocating the majority of store space to showrooms with up to 50 different vignettes of distinct rooms in a home. Couple the in-store experience with a website geared toward product & installation education, sampling, and a simple ordering process; The Tile Shop places itself to win customers in a space where tile purchases directly from homeowners are relatively infrequent.

{kind=link}

The retail flooring market is a highly fragmented industry. Floor & Decor ( FND ) is the largest player making up 8.8% of the revenue while large national home improvement centers like Home Depot ( HD ) and Lowe's ( LOW ) garner significant market share as well. The majority of sales are generated by local specialty flooring retailers, factory-direct stores, and single-site stores.

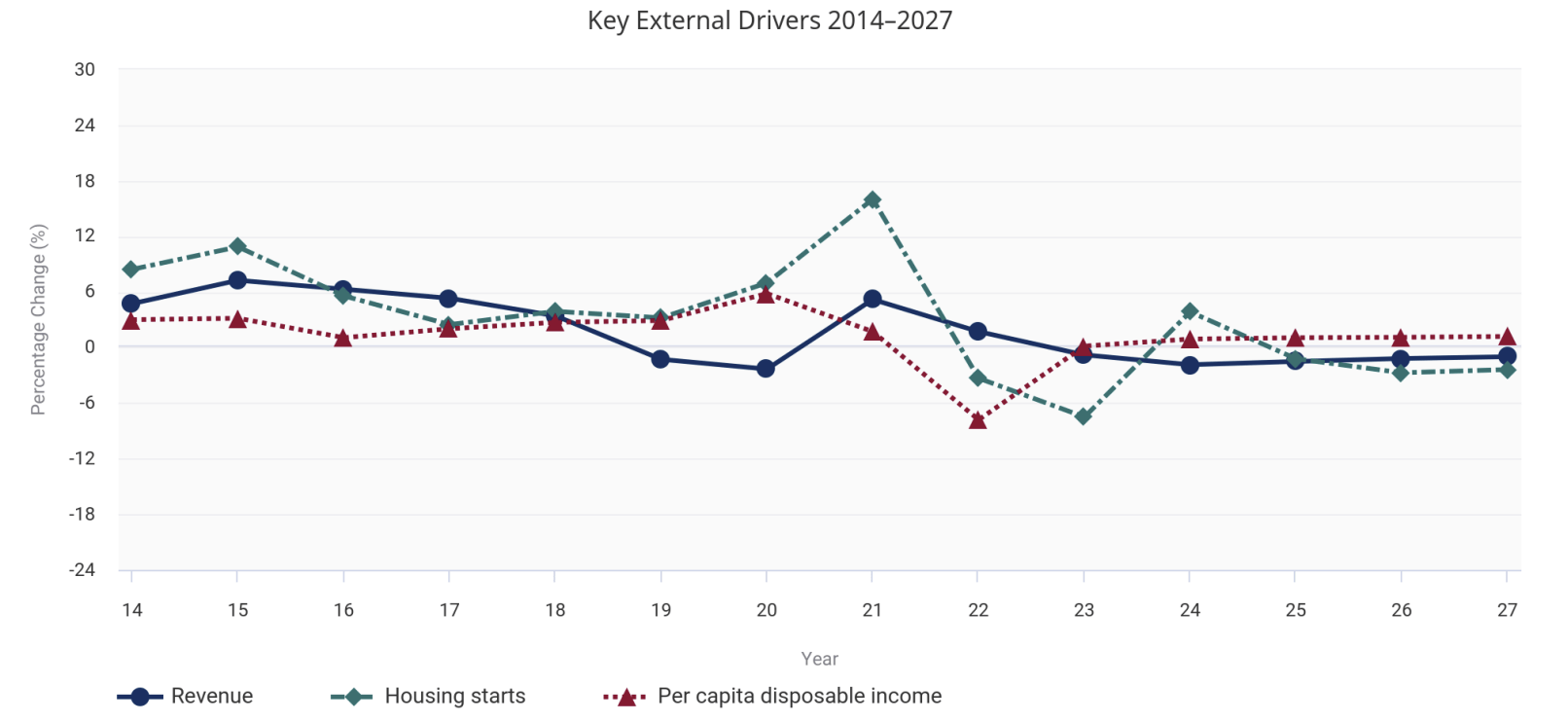

The flooring industry is heavily influenced by housing starts and per capita disposable income while other key drivers include the consumer confidence index, the value of private nonresidential construction, and private spending on home improvements. IBIS World expects the total flooring industry to contract by 1.3% annually over the next 5 years which may erode the total earnings potential for Tile Shop:

{kind=link}

Even with the total flooring industry expected to decline over the next 5 years, it is expected that tile will continue increasing in popularity taking industry share from hardwood and carpet.

Thesis Support

Price

According to my analysis, Tile Shop trades at a significant discount to fair value mostly attributed to 3 main reasons.

First, the stock has dealt with margin contraction in recent years driven by the disastrous implementation of a new enterprise resource system in 2019 and more recently inflationary pressures that were mismanaged. I will touch more on these points in the earnings section.

Second, in late 2019 two activist investors, Peter Kamin and Peter Jacullo, pushed the board into announcing the de-listing from the Nasdaq with their reasoning being cost-cutting initiatives from reduced reporting and disclosure requirements. Because mutual funds and other institutional investors have rules against owning OTC-traded stocks , the price drop was exacerbated. This is because large institutional investors with such rules were required to sell the stock forcing downward price pressure. Following the stock price rout, the two Peters increased their total stake from 17% to 30% of the outstanding shares which was soon followed by shareholder suits. I believe it will take time to rebuild public confidence in the stock following these events but based on underlying business operations The Tile Shop is mispriced.

Lastly, Tile Shop has no sell-side analyst coverage currently. The lack of coverage allows for greater mispricing of the stock as it is off of most investors' radars. This creates an opportunity prior to the company garnering coverage in the future which may spark a re-rating closer to its peer group. ( Re-rating in this case means the market will pay a higher EV/EBITDA multiple for the stock and that multiple may be more comparable with Tile Shop's peer group in the future.)

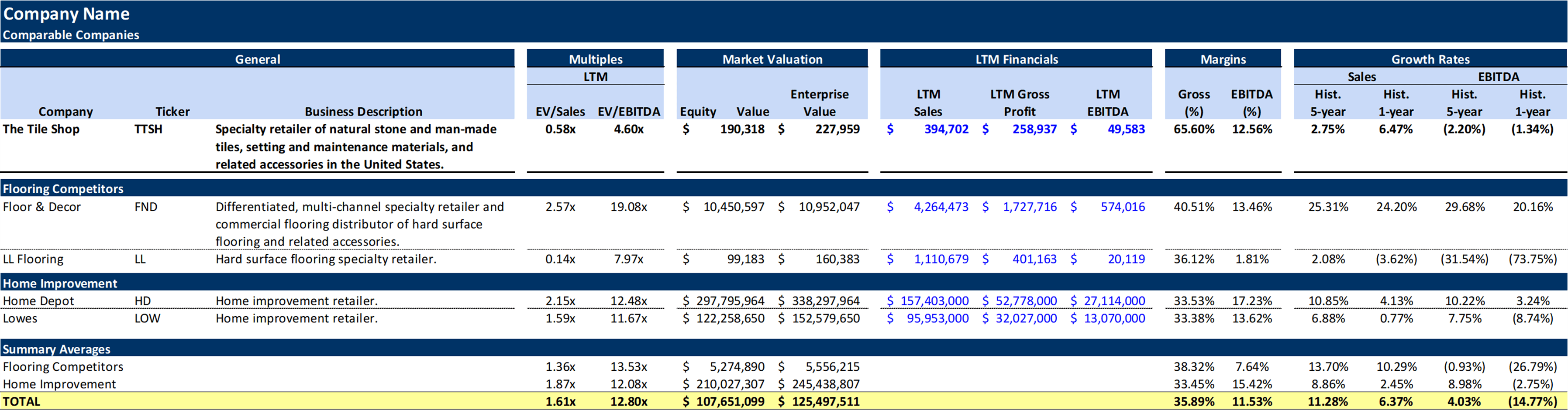

Below is the comp set for The Tile Shop:

{kind=link}

Based solely on the comp set and assuming EBITDA growth moving forward (see earnings section below), Tile Shop has a 2.8x upside.

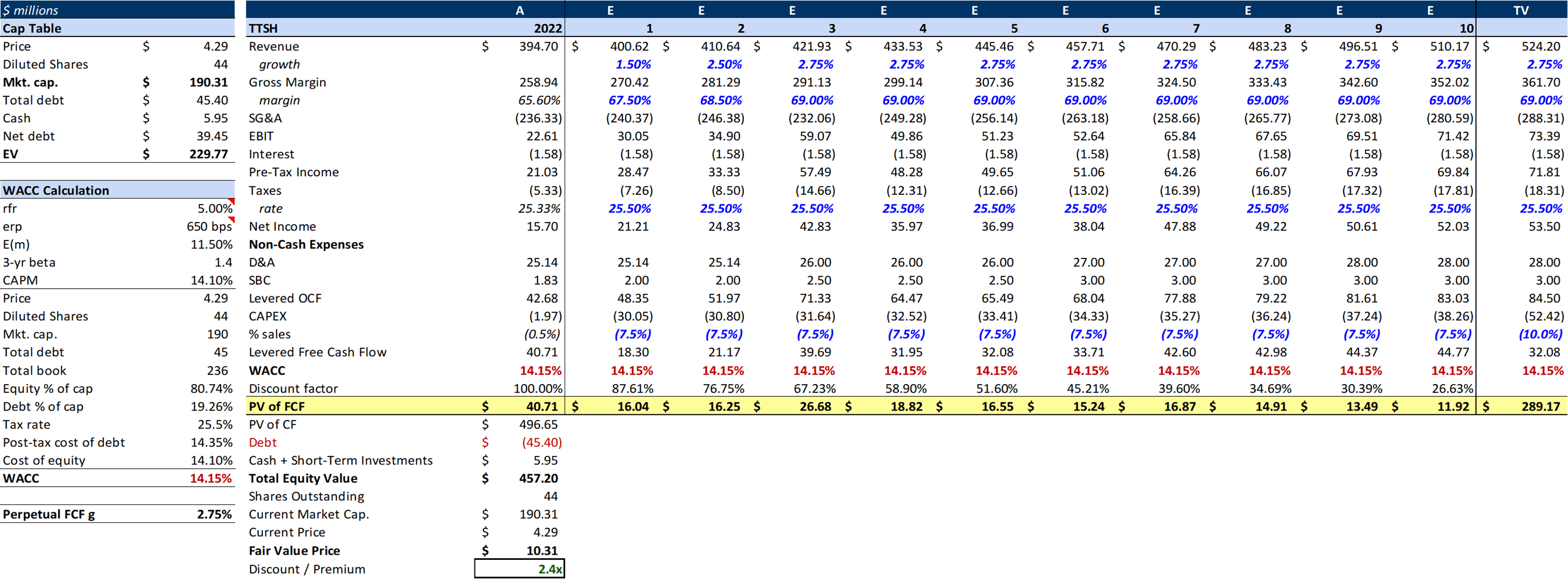

To get another sense of valuation I ran a 10-year DCF with conservative growth and margin estimates and increased perpetual CAPEX spending relative to years 1-10:

{kind=link}

Based on the DCF I conducted above, Tile Shop currently has a 2.4x upside.

Using a blend of comps and the DCF, I believe Tile Shop currently trades at a 62% discount to fair value.

Earnings

While the market may be discounting Tile Shop currently, earnings growth is vital to the return profile.

Margins

In recent history, Tile Shop has experienced margin contraction driven by a disastrous ERP implementation in 2019 and mismanagement of pricing during the inflationary uptick. The ERP transition impaired typical store operations leading to EBITDA margins contracting to their lowest levels on record by the end of the year (10.2%). While recovery was underway, margins declined YoY in 2022 due to conservative price hikes amid a challenging macro environment at the same time inventory prices skyrocketed.

With management signaling to international freight costs coming down and strong professional demand supporting further price hikes, we will see gross margins elevate in 2023. A historical average of ~4 inventory turns a year may allow Tile Shop to replenish more attractively priced inventory quickly. Holding OPEX constant from 2022 as a % of sales, we should see 250 - 350 basis points in EBITDA margin uplift from gross margins alone.

Following COVID, management was able to focus extensively on store efficiency since headcount was slashed and store hours were reduced significantly. During that time, The Tile Shop has effectively operated stores with fewer employees and focused their incentive structur e to reward staff based on performance properly.

Because Tile Shop works closely with designers to put out specialty products and lines, their SG&A costs will remain elevated compared to peers even though they have a superior product margin. With that in mind, I still believe Tile Shop can achieve an 18% EBITDA margin by 2025 based on gross margins normalizing, store efficiency, and a proper incentive structure.

Growth

Even as store count remained stagnant for the past 4 years, Tile Shop achieved record revenue in 2023 and comparable store sales grew 5.1% annually due to its broad product assortment, competitive prices, and expert employee base.

Tile Shop is reigniting growth through 2 new store openings and new product launches in 2023. As management continues focusing on professional sales to support consistent revenue and resilient coverings such as tile and vinyl continue to grow as a % of the total flooring market, I can confidently project stable revenue growth for the business moving forward.

Risks

With a position in Tile Shop, there are 3 main risks I consistently stay cognizant of:

- Macro Conditions: Declining housing starts and discretionary income may be significant headwinds for the entire flooring industry. These trends will be key to follow but a mitigant to an overall flooring decline is the specific growth of tile and vinyl.

- Competition: Specifically, Home Depot and Lowes may be worrisome as their immense economies of scale may allow them to price more attractively. The mitigant to competitive risks lies within their supplier relationships and the focus on the specific tile/vinyl niche.

- Public Perception: Following the de-listing scare, it was fair for markets to discount the stock. While I don't believe there is further risk around de-listing and board volatility, I do believe the stock may take time to be noticed especially with no sell-side coverage. Extended time to be noticed by market participants could lead to an erosion of IRR.

What Investors Need to Believe

I believe there are a select few points investors need to believe in to get comfortable with this investment.

- Management can successfully pass prices to customers without demand destruction

- Professionals and individuals continue to find value in a tile/vinyl-focused store due to expertise, pricing, and assortment

- Tile & vinyl growth will outweigh overall flooring headwinds

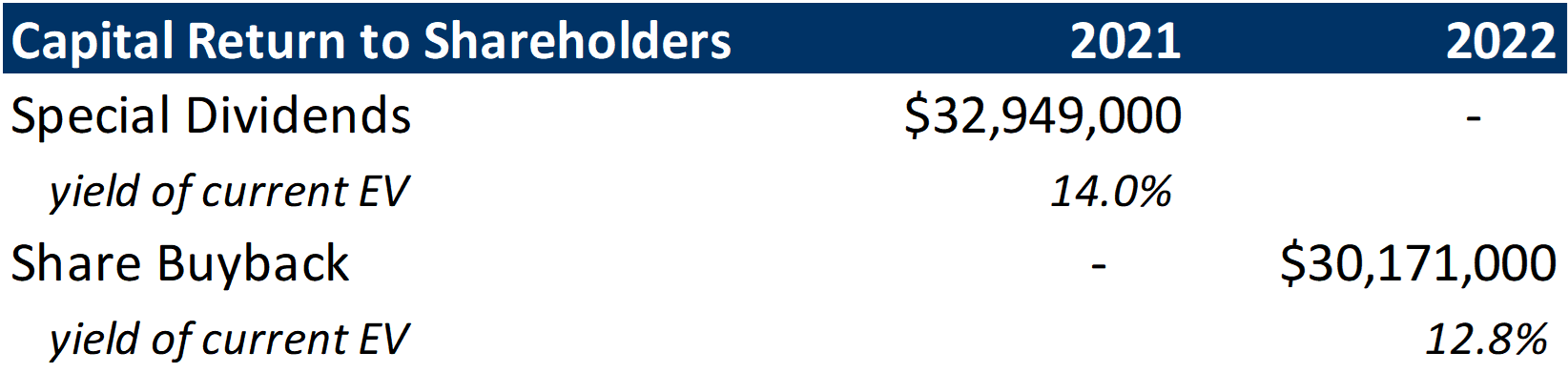

- Peter Jacullo and Peter Kamin continue returning capital to shareholders

If these points come to fruition coupled with the current price the business trades at, Tile Shop has excellent return potential.

Summary

Tile Shop is trading at a significant discount to peers and fair value. Margin expansion is very plausible through gross margin normalization and continued store efficiency. Combine that with steady growth prospects and I believe the market is significantly discounting future earnings potential for the company.

Tile Shop has a healthy balance sheet especially as the company plans to pay down a significant portion of the JPMorgan ( JPM ) facility ($45.4mm drawn at EOY '22) according to the last earnings call. Inventory levels remained elevated at year's end but should normalize as supply chain issues alleviate. With significant EBITDA potential, I'm not worried about current cash levels ($6mm) as the company is generating consistent cash flow. It's also reassuring knowing the company owns 4 out of its 5 distribution centers giving them optionality for sale-leasebacks if they ever got into a tough spot.

As a shareholder, I like having Peter Kamin and Peter Jacullo at the helm. They're clearly focused on returning capital to shareholders through the special dividend in 2021 and the share buyback in 2022. The current CEO, Cabell Lolmaugh is also a long-term Tile Shop store operator focused on store efficiency. While the recent mispricing amid the inflationary environment is seen as a blunder, I believe long-term this is the right team to execute and the right team to return capital to shareholders.

{kind=link}

For further details see:

Tile Shop: A Mispriced Security