TLYS - Tilly's: Another Struggling Retailer With Little Hope

2023-05-31 11:10:53 ET

Summary

- Tilly's has grown at a CAGR of 4%, with an EBITDA-M of 4%.

- Competition has increased due to the rise of e-commerce, fast fashion, and social media marketing.

- We expect Tilly's to continue to struggle.

- Tilly's valuation is far too high for the ongoing struggles and lack of clear turnaround.

Investment thesis

Our current investment thesis is:

- Tilly's is a struggling retailer with no unique selling point to drive value.

- Tilly's financial performance is underwhelming and we see no real avenue for improvement.

- Retail is an incredibly competitive industry and we think Tilly's is continually losing ground.

Company description

Tilly's, Inc. ( TLYS ) is a specialty retailer in the United States that focuses on casual apparel, footwear, accessories, and hard goods for young men, women, boys, and girls.

Share price

Tilly's share price has overarchingly declined in the last decade, as changing industry dynamics have contributed to greater competition and relative underperformance.

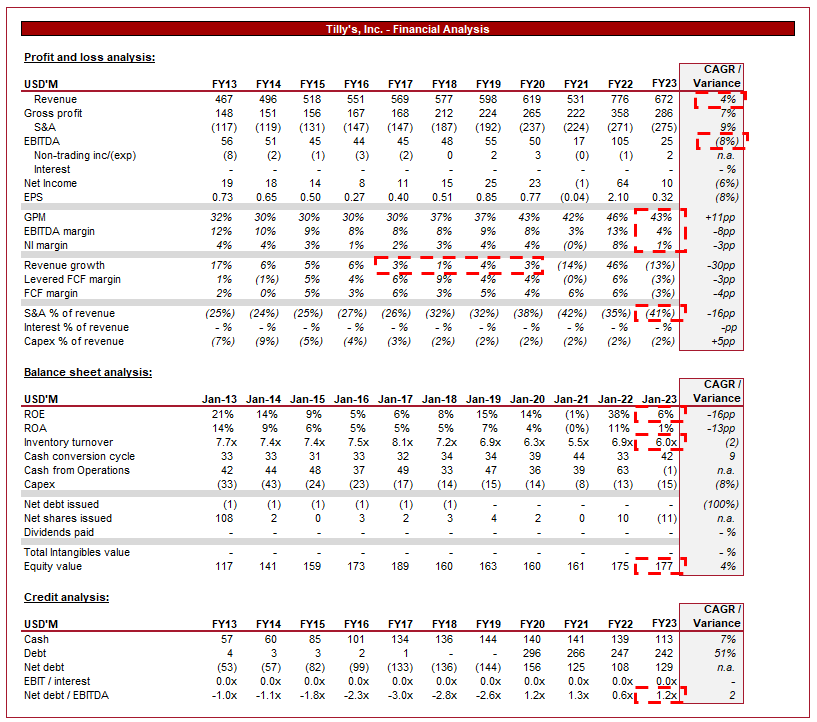

Financial analysis

{kind=link}

Tilly's financial performance (Tikr Terminal)

Presented above is Tilly's financial performance for the last decade.

Revenue

Revenue has grown at a CAGR of 4%, driven by improving retail spending and the strength of the brands Tilly's stocks. This period has been incredibly difficult for many retailers and so consider this growth rate to be a good achievement.

The primary disruption has been the rise of e-commerce, which has materially changed the industry dynamics. Consumers are increasingly shifting toward online shopping, valuing convenience, the ease of comparing options, and a wider product selection. Tilly's has faced increased competition as a result, contributing to slowing demand. E-commerce retailers are able to price lower than their peers / spend more on marketing due to reduced overhead costs. This is the primary reason why despite many of the traditional retailers developing an e-commerce offering, they have been unable to easily catch up. Tilly's has done well to increase online sales yet continues to trail behind the likes of Zalando, in part because it lacks the breadth of options the e-commerce businesses can stock.

Brick-and-mortar is not dead, however. The segment has shown resilience, especially post-Covid, illustrating the value consumers place on the offering. The important factor is that the offering expected has changed. Omni-channel retailing has become an essential strategy for retailers. Consumers expect a seamless shopping experience across various channels, creating a new form of convenience. Tilly's offers services like buy online, pick up in-store (BOPIS), which has the added benefit of avoiding returns.

Consumer preferences for the products they purchase are also changing. The younger audience, Tilly's target market, is increasingly influenced by fashion trends, seeking to wear such products but not at the price charged by the trend-setters. This gave rise to the Fast fashion trend, whereby similarly designed products to high fashion would be produced quickly and at a far lower price. This has been a major challenge for traditional brands as they have faced reduced demand due to an inability to innovate at the same level (while maintaining their design philosophy). For this reason, Tilly's has been subject to this underperformance as the majority of the fast fashion brands are usually retailers themselves, keeping their brands in-house.

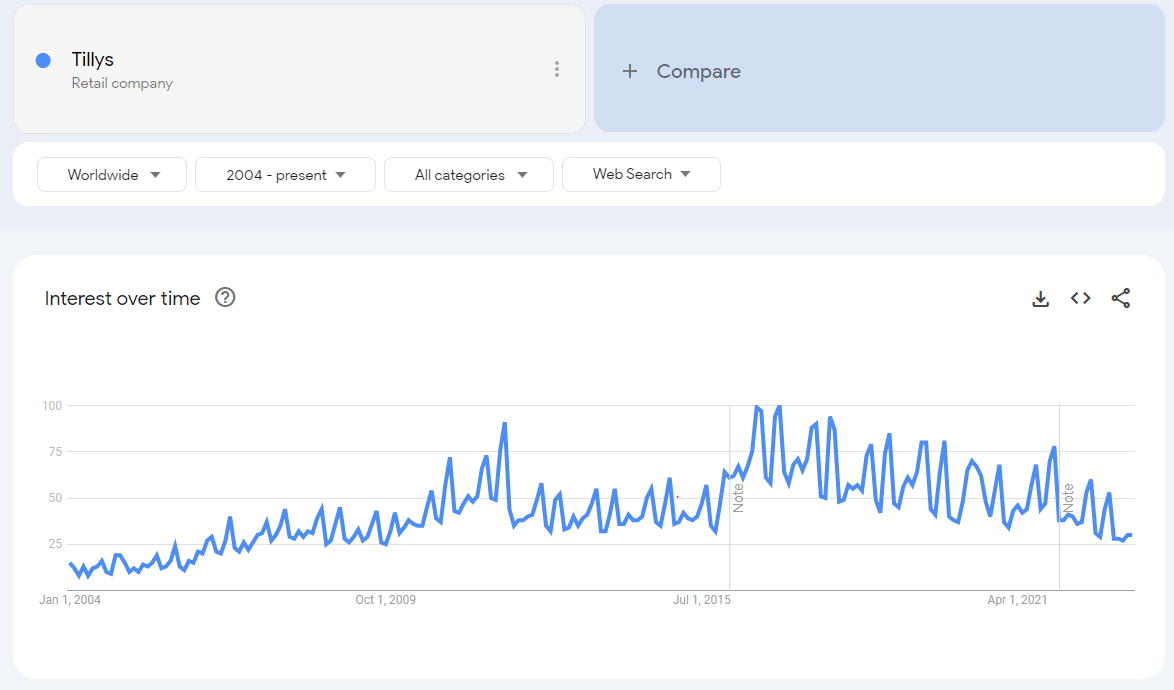

The power of Social media platforms should not be understated. They have become an influential channel for retailers to engage with a large share of the retail-buying public. Although this favors those with the largest marketing budgets, we have also seen success with alternative / creative marketing, which seems to be well executed by start-up brands. Like so many of its peers, Tilly's has seen a consistent decline in relevancy over the last decade.

{kind=link}

Tilly's (Google Trends)

The rise of Direct-to-consumer ( DTC ) is a by-product of the power of social media and is a major issue for retailers. With brands increasingly engaging directly with potential customers, they are increasingly driving traffic to their own outlets. Historically, most brands lacked the power to do this and so needed retailers to advertise their products in stores. This has completely changed and resulted in more and more leading brands reducing their retailer allocation. This makes us very concerned as Tilly's does not have the retail might of Kohl's, Nordstrom, etc. and so could be one of the first to see the quality of brands it is able to stock decline over time.

Economic considerations

Current economic conditions represent a short-term headwind. With high inflation and elevated rates, consumers are reducing consumption where possible as a means of protecting finances. The retail industry is generally negatively impacted during such times as apparel spending is easily foregone. This is likely the primary reason for Tilly's 13% decline in sales in FY23.

Our expectation is for rates to begin declining in early 2024, with inflation declining consistently throughout the year. This will likely mean continued struggles in FY24. Although we lack sufficient forward guidance, we estimate a 3-8% decline is likely.

Margin

Tilly's historical margins reflect a retailer with little bargaining power and one facing a high level of competition. This said, the consistency is commendable. The decline in FY23, however, is highly concerning. With an EBITDA-M of 4%, the company is completely unattractive in our view. This decline looks to have occurred post-Covid, although Tilly's did experience a bump in line with the industry as a whole.

The reason for this in part is likely inflationary pressures, as well as discounting which Tilly's may not be able to unwind without materially reducing demand. 3 of the top 5 "related topics" according to Google Trends are discount related, suggesting this is the primary reason for consumer searches.

Balance sheet

Inventory turnover has declined by 0.9x in FY23, which suggests Management anticipated greater demand. This is not an issue from a liquidity perspective as the ratio remains above FY21 levels.

Tilly's has a ND/EBITDA ratio of 1.2x, which suggests the company is reasonably financed in our view. This mainly relates to a change in accounting standards resulting in leases being taken on balance sheet. This is a key positive for us as an overleveraged balance sheet would leave Tilly's in a serious predicament.

Outlook

Outlook (Tikr Terminal)

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a (3)% decline in sales during FY24, which we believe to be on the bullish side. Further, margin improvement is not expected in the coming 2 years but instead further deterioration. This could be the reason for the soft decline forecast, as analysts believe aggressive discounting will continue to maintain sales.

Valuation

Tilly's is trading at 14x LTM EBITDA and 64x NTM, given the substantial decline forecast.

Our view is that the valuation does not appropriately reflect the financial position of the company. FY24 will be difficult and looking long term, we struggle to see what the value driver will be for Tilly's. There are many struggling retailers trading in the single digits who are a far better bet on retail.

Final thoughts

Tilly's is a run-of-the-mill retailer. We see very little to suggest this business will outperform the industry as a whole or has anything of unique value. Further, retail continues to be an incredibly competitive environment that is seemingly a race to the bottom on prices while brands continually flee as stock is allocated to their retail operations.

We see no value opportunity and given that retailers such as Kohl's and Nordstrom are cheaper, we rate this stock a sell.

For further details see:

Tilly's: Another Struggling Retailer With Little Hope