JILL - Tilly's Failed To Live Up To Expectations

Summary

- Tilly's had a really difficult 2022, with results in the first nine months of the year showing material deterioration in sales and profits.

- This trend is expected to have been prevalent in the final quarter and the overall picture near term isn't great.

- The firm is not as valuable as I previously thought, at least not until it can get through this mess.

In an ideal world, every investment that you become bullish on would turn out to be a success. But sadly, that world does not exist. From time to time, even professionals can make a mistake when it comes to an investment opportunity. And over the past several months, It has become painstakingly clear that one of my mistakes has been Tilly’s ( TLYS ). This firm operates as a specialty retailer focused on casual apparel, footwear, accessories, and even hard goods. Even though I pointed out nearly a year ago that the company itself was mediocre, I felt as though shares were cheap enough to warrant some nice upside potential. Sadly, the market has had other plans in mind and the performance of the firm has been anything but great. Based on the most recent data available, I would even go so far as to say that it warrants a downgrade from the ‘buy’ I had it rated previously to a ‘hold’ today.

Tough times for this retailer

Back in the middle of February of 2022, I wrote a bullish article on Tilly’s. In that article, I acknowledged that the company was a mediocre firm. However, I found myself impressed by how rapid its growth was prior to the COVID-19 pandemic. The firm was showing promising signs even during the pandemic and near its end. And on top of this, its robust balance sheet and low share price made me think that it was worthy of a ‘buy’ rating. Unfortunately, shares have generated a loss for investors since the publication of that article totaling 28.7%. That's far worse than the 12.4% achieved by the S&P 500 over the same window of time.

{kind=link}

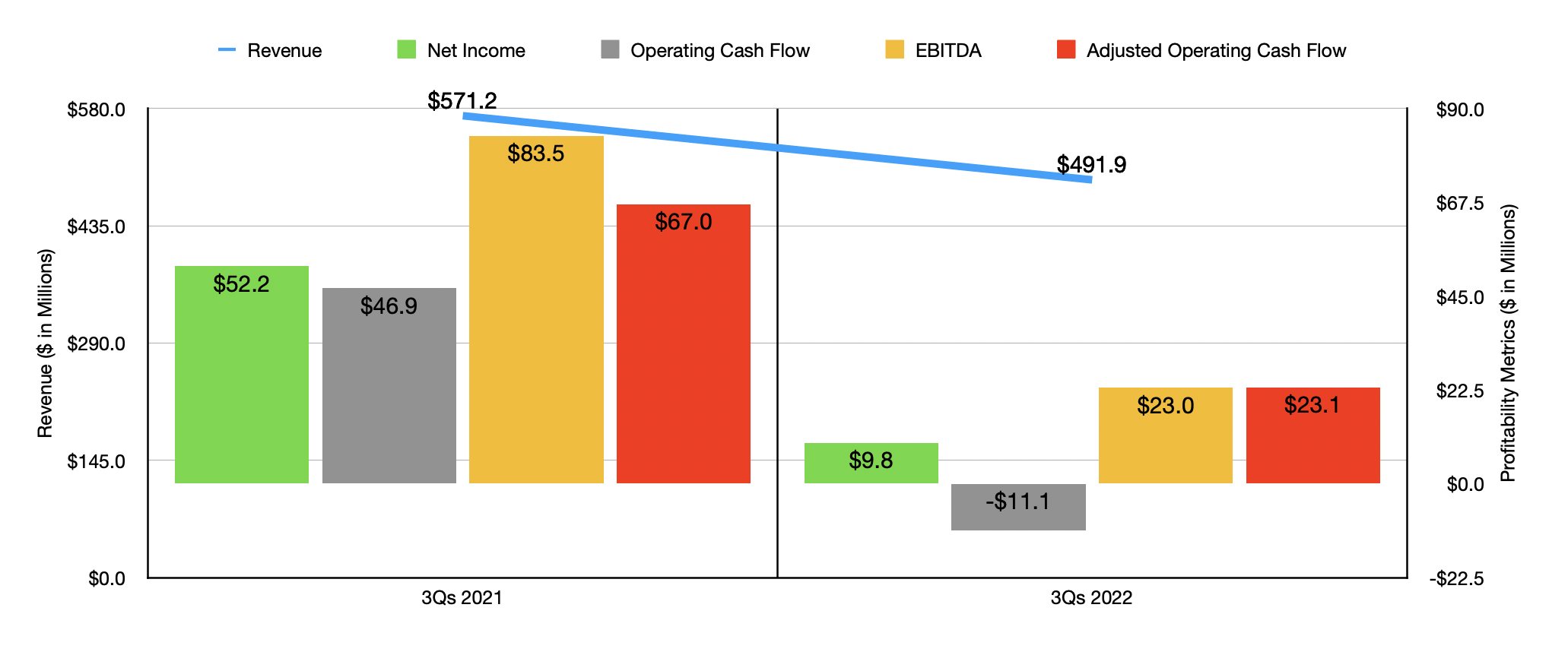

To understand why Tilly’s has underperformed so woefully, I would like to focus on financial results for the first nine months of its 2022 fiscal year . During this window of time, sales to the company came in at $491.9 million. That's 13.9% lower than the $571.2 million generated the same time one year earlier. The vast majority of this pain was driven by a 14.9% plunge in comparable store sales, with e-commerce net sales dropping 15.7%. Management attributed this weakness to the pent-up consumer demand and stimulus payments that existed in 2021 but that did not repeat themselves in 2022. The only positive was that the firm did see the number of stores it operated increase slightly from 243 to 247.

This drop in revenue brought with it a significant decline in profitability. The bad thing about retail is that even a small change in comparable store sales can lead to significant changes in the bottom line. Add on top of this inflationary pressures and supply chain challenges, and the company was due for a world of pain. In this case, net income plunged from $52.2 million to $9.8 million. Operating cash flow performed even worse than that, dropping from $46.9 million to negative $11.1 million. If we adjust for changes in working capital, the metrics still would have declined from $67 million to $23.1 million, while EBITDA plunged from $83.5 million to $23 million.

{kind=link}

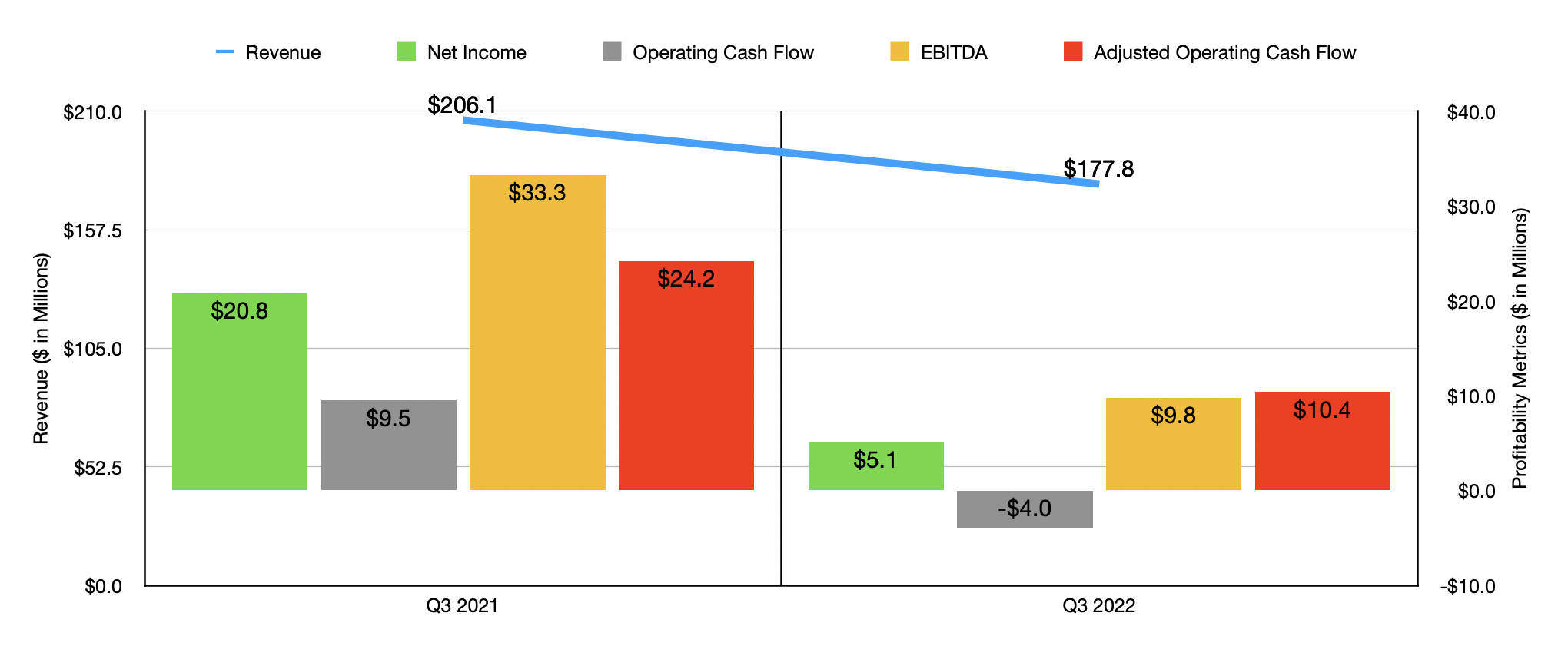

Performance has not shown any real signs of improvement heading toward the end of 2022. In the third quarter alone, sales came in at $177.8 million. That's down from the $206.1 million generated only one year earlier. Once again, the increase in the number of stores helped the firm. But comparable store sales were still down 14.9% year over year. Naturally, bottom line results also suffered. Net income dropped from $20.8 million to $5.1 million. Operating cash flow fell from $9.5 million to negative $4 million, while the adjusted figure for this dropped from $24.2 million to $10.4 million. And finally, EBITDA for the company dropped from $33.3 million to $9.8 million.

Management expects more of this pain to continue into the final quarter of 2022. Revenue should be between $183 million and $188 million. That's down from the $204.5 million reported the same quarter one year earlier. Even with that decline though, the firm is anticipating earnings per share of between $0.02 and $0.06, translating to net income, at the midpoint, of $1.20 million. For context, the profit per share in the final quarter of 2021 was $0.38. Based on all of these figures, the company should generate net profits of $11 million for 2022. Based on my own estimates, adjusted operating cash flow should be around $28.9 million, while EBITDA should come in at around $28.8 million.

{kind=link}

These figures imply a forward price to earnings multiple of 24.6, a forward price to adjusted operating cash flow multiple of 9.3, and a forward EV to EBITDA multiple of 5.7. The reason why the EV to EBITDA multiple is so much lower stems from the fact that the company has no debt on hand and has $105.8 million in cash and cash equivalents on its books. These numbers are all substantially higher though than if we were to use data from 2021. This much can be seen by looking at the chart above. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 3.6 to a high of 7.9. In this case, Tilly’s was the most expensive of the group. Using the price to operating cash flow approach, the range was from 3.4 to 11, with three of the five companies cheaper than our prospect. And finally, using the EV to EBITDA approach, the range was from 1.4 to 6.3. In this case, only one of the companies was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Tilly's |

| 24.6 |

| 9.3 |

| 5.7 |

| Citi Trends ( CTRN ) |

| 3.6 |

| 3.4 |

| 1.4 |

| Destination XL Group ( DXLG ) |

| 5.0 |

| 11.0 |

| 5.3 |

| Express ( EXPR ) |

| 6.0 |

| 7.7 |

| 6.3 |

| Chico's FAS ( CHS ) |

| 5.4 |

| 10.5 |

| 2.8 |

| J.Jill ( JILL ) |

| 7.9 |

| 4.0 |

| 3.5 |

Takeaway

Although some investors may gravitate toward the company's low valuation, I think that my mistake is that I didn't think that the firm would be hit so hard by current economic conditions. Perhaps it does offer some upside potential if the broader economy recovers. But that could take time and there has been no evidence from a fundamental perspective that the company's situation is getting any better. Given these concerns, I think it's only appropriate to downgrade the company from a ‘buy’ to a ‘hold’.

For further details see:

Tilly's Failed To Live Up To Expectations