TSBK - Timberland Bancorp: Interesting Thanks To A 5% Dividend Hike And Increasing Book Value

Summary

- Timberland Bancorp is a small local bank focusing on Washington State.

- The bank has an impressive history of asset quality, which helps to keep the loan loss provisions low.

- TSBK stock is still not expensive after a recent rally as the stock is trading at less than 10 times earnings.

- Although the dividend was increased, the bank still retains the majority of its earnings on its balance sheet, which will boost the TBVPS.

Introduction

Timberland Bancorp ( TSBK ) is a local bank in Washington State. I have been keeping an eye on this bank for more than two years now, and since November 2020, the total return (share price appreciation and dividends) comes in at almost 90% , which is a pretty nice outperformance compared to the performance of the S&P 500 ( SPY ) during the same time frame.

Seeking Alpha

In a follow-up article published in the first half of 2022 I explained how Timberland should be able to benefit from the increasing interest rates: The bank was guiding for a $0.50 EPS increase for every 100 bp increase of the interest rates.

The bank recently reported its Q1 results (the financial year ends in September, so Q4 2022 is Q1 FY 2023 for this bank) and as widely expected, the results were good and shareholders were rewarded with a 5% dividend hike to $0.23 per quarter.

FY 2023 has just started, and Timberland is doing well

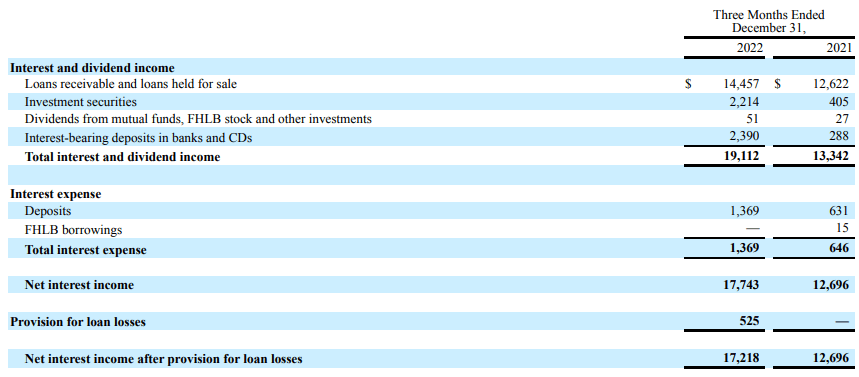

Timberland Bancorp is definitely taking advantage of the increasing interest rates as the bank’s net interest income has increased by almost 50% compared to a year ago. As you can see below, the total interest and dividend income increased from $13.3M to $19.1M while the total amount of interest expenses increased by just $0.7M.

{kind=link}

Of course, the interest expenses will continue to increase but so will the interest income as existing loans still have to "reset" to a new, higher interest rate and this is only happening gradually. The total net interest income increased to $17.7M and even after taking the loan loss provisions into account (there were no provisions required in Q1 FY 2022 but the bank had to allocated just over $0.5M in Q1 FY 2023), the net interest income after provisions for loan losses jumped by almost 40% to $17.2M.

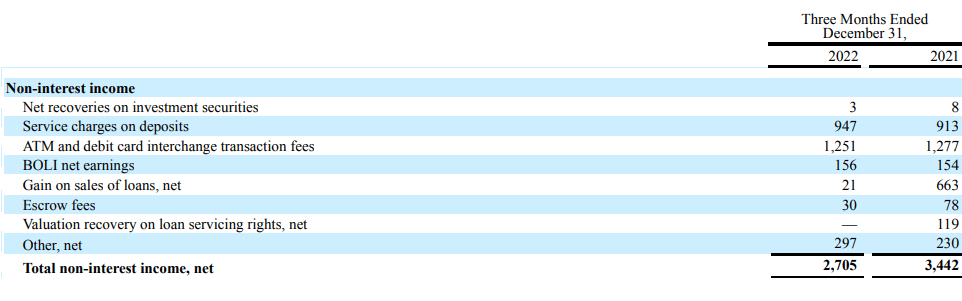

The net interest performance is important for Timberland Bancorp as its non-interest income is pretty low. That clearly shows in the image below where the total non-interest income fell to $2.7M on the back of a lower realized gain on the sale of loans.

{kind=link}

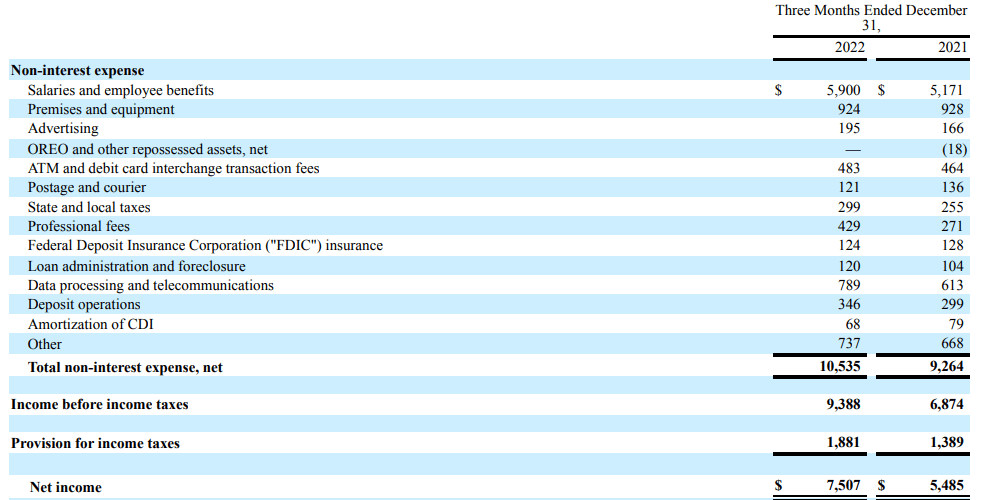

Meanwhile, the total amount of non-interest expenses increased to $10.5M and this resulted in a pre-tax income of $9.4M and a net income of $7.5M That still is almost 40% higher than the net income realized in the first quarter of last year. The EPS in the first quarter came in at $0.91 based on an average share count of 8.23 million shares.

{kind=link}

Timberland increased its quarterly dividend to $0.23 per share , a 5% hike. This means the payout ratio is still less than 30% which indicates the dividend should be pretty safe. As the bank’s share price has increased by 75% since my article in November 2020 , Timberland is no longer very attractive as a dividend stock as the dividend yield as the yield has decreased to roughly 2.7%, but it still is in "value" territory: the stock is trading at less than 10 times earnings and in an article published in Q2 2022, I explained how Timberland will see its EPS increase by $0.50 per year for every 100 bp increase in the interest rates. Of course this doesn’t happen overnight, but as the interest rates have increased by a multiple of 100 basis points, Timberland’s net interest income will likely continue to increase over the next few quarters and even years, notwithstanding the bank will have to pay more on the deposits.

Another important element here is that Timberland doesn’t have a lot of securities available for sale on its balance sheet. That explains why the unrealized loss on those securities was just a few thousand dollars in the first quarter of the current financial year.

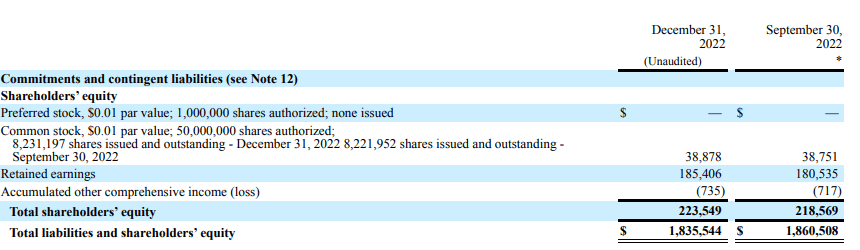

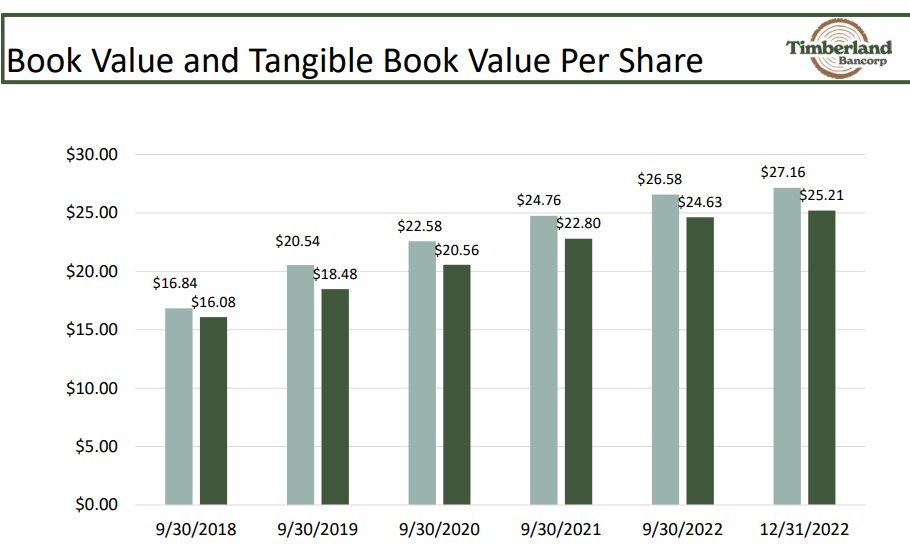

As of the end of December, the value of the equity portion was $223.5M (see below). And considering there are 8.23M shares outstanding, the book value per share was approximately $27.15 (rounded).

{kind=link}

The balance sheet does contain about $15.1M in goodwill which means the tangible book value per share is about $1.85 lower, and about $1.95 lower if you also include the $0.9M in other intangibles. As of the end of December, the tangible book value came in at $25.21 per share .

Investment thesis

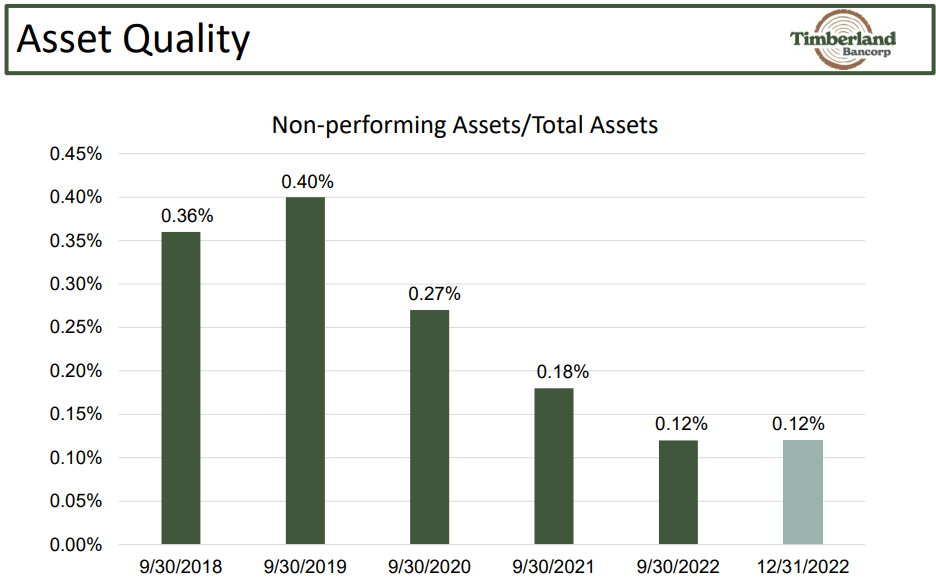

While I prefer to buy banks at a price closer to their tangible book value, I have no issue paying the current 30%-35% premium to the tangible book value. First of all, Timberland has an excellent history of maintaining a quality loan book. Default rates are low and loan loss provisions do not have a major impact on the earnings profile. The asset quality is an important metric, and Timberland scores well on this metric.

{kind=link}

Additionally, the bank has a history of increasing its book value and tangible book value.

{kind=link}

Indeed, based on Q1 results, Timberland is retaining almost $0.70 per quarter in earnings due to the low payout ratio. As the net income may increase thanks to the anticipated higher net interest income, I wouldn’t be surprised to see Timberland being able to retain about $3 per share per year in earnings which means the TBVPS increase will accelerate. Even if the bank can retain "just" $2.75 per share per year, the TBVPS will increase to almost $31 by the end of calendar year 2024.

I have a small long position in TSBK, and in hindsight, I wish I had bought more. That being said, the stock still isn’t expensive as it’s trading at a single-digit earnings multiple and a relatively small premium to the tangible book value. And that premium is decreasing fast.

For further details see:

Timberland Bancorp: Interesting Thanks To A 5% Dividend Hike And Increasing Book Value