AFRAF - Time To Buy Air France-KLM

Summary

- Air France-KLM had its fair share of problems even before the pandemic.

- The company seems to be coming out of the pandemic more unified and focused.

- Debt is manageable and dilution risk seems low.

I haven't been a big fan of Air France-KLM (AFRAF) in recent years and that's not so much of the company's product. In fact, before the pandemic in late 2019, I flew with KLM and it was a very enjoyable experience. It was the last airline I would fly with before the pandemic would unfold and it also was the first airline I would fly when air travel was made easier again. Unfortunately, my one-hour flight on KLM was not long enough to assess their food and beverages but I guess even if the flight was longer at that time there was no product offering and even if there was my guess is that I did not miss much. I flew with Lufthansa some months after and the service was underwhelming as they merely offered food and a chocolate bar. Nevertheless, the cabin product that KLM offered me on a brand new Embraer E195-E2 was superior to the cabin product Lufthansa offered on their CRJ-900s.

Why I Disliked Air France-KLM Stock

So, I do enjoy the product that Air France-KLM and KLM in particularly offered. Yet, for a long time I wouldn't touch its stock with a 10-foot pole. The reason was quite simple and that was that KLM was actually performing quite well financially as its crew made sacrifices while the French side was mostly resisting necessary cuts supported by the French State which was a shareholder. The result was hostility where profitable growth was not placed with Transavia and French pilots saw KLM as the company that was growing at their expense. From business perspective, the objections the French had against growing KLM with modern aircraft instead of Air France made no sense. If you spend tens of millions of dollars and often over $100 million on a plane, then it only makes business sense to put that aircraft in service with the airline that generates most value with that aircraft. Somehow, that simple thing was lost on the French side and unions being more fragmented in France also led to a weaker negotiations position for unions compared to the Dutch counterpart often leading to strikes which cost the airline group and at some point in 2015 also erupted in violence.

{kind=link}

Pieter Elbers, CEO of KLM at the time, has always protected the interests of KLM and that was also the case when on group level the company wanted KLM to stream up its cash position basically losing cash control and that cash could potentially be used to fill the gaps at Air France. With this in mind, when Benjamin Smith became CEO of Air France-KLM in 2018, Elbers resisted the control that the new CEO was looking for by demanding a board seat at KLM. Eventually it made Elbers' position shaky and only after a petition from KLM employees and intervention from the Dutch government, his tenure as CEO was extended. Not long after, to back Elbers who protected the interests of the Dutch Arm, the Dutch government took a stake in the airline group which subsequently angered the French State and another chapter of the never ending book of hostility between the French and the Dutch was written.

The continued quarrel and the non-performance of Air France was why I have not been a shareholder for years, but things might be getting better.

Dutch States Shows Itself A Bad Investor

{kind=link}

The Dutch State quietly purchased stock of Air France-KLM to match the stake of the French State in 2019. The timing of that obviously couldn't be worse with the pandemic hitting airlines a year later, putting the investment under water. That's where the misery for the Dutch State started. The Dutch Government provided a €3.4 billion aid package consisting of a direct loan and guarantees. The French State also provided a relatively high interest loan and when Air France-KLM was looking for recapitalization in 2021. The Dutch State did not participate while the French State simply converted €3 billion into shares plus €1 billion in fresh capital bringing the stake in the airline group to roughly 30%. In 2022, Air France-KLM prepared to issues shares and this time the Dutch State did participate to maintain its diluted share while the proceeds would be used to pay off the high interest loans that the French Government provided. An interesting action, because essentially the Dutch State was participating in paying French Government loans with taxpayers' money while not seeing its share in the airline group improve.

Why I'm Liking Air France-KLM Better Now

One reason why I'm liking Air France-KLM better today is because despite the hostility between the Dutch and French State regarding the participation in the airline group, within the business there are less quarrels. KLM and Elbers decided not to renew his mandate for a third term. A reason for his departures is not known, but I would expect that this has to do with his resistance against a unified business approach on group level and with that we see that the stake the Dutch took being close to meaningless in terms of achieving their goals. Elbers now leads Indian airline Indigo and he has been replaced by Marjan Rintel.

Rintel worked 15 years for KLM before heading to the Schiphol Group, which owns KLM's hub, and eventually she headed the Nederlandse Spoorwegen or Dutch Railways. I have yet to see Marjan Rintel doing something meaningful at KLM and looking at the state of the Dutch Railways, I don't have high hopes of her mandate but maybe this all fits in the strategy of Air France-KLM with more control on group level than on airline level. Nevertheless, the airline is finally functioning and performing more as a group than as a set of individual airlines each with their own bosses and interests and we see that back in various elements.

Unified fleet

{kind=link}

One thing that Benjamin Smith wanted is making fleet decisions on a group level while Elbers was a proponent of making fleet decisions on airline level. By December 2021, Air France-KLM announced it had selected the Airbus A320neo family on group level and one month later it was decided Elbers would leave KLM. It's hard to see no connection between both events. Either way, operating a unified fleet has big advantages which should render the airline group more cost efficient.

Cabin Improvements

{kind=link}

In May 2022, Air France-KLM announced it would be introducing a new cabin product which has been finished recently with 48 seats in Business Class, 48 Premium Economy seats and 273 Economy seats on the Air France Boeing 777-300ERs with availability of USB sockets, chargers, Bluetooth connectivity and WIFI. Also KLM's Boeing 777s and the Dreamliner fleet would be updated. While a new cabin product might not seem like a big thing, it's a major improvement bringing connectivity options as well as a premium economy product to the customer fitting a demand trend we have seen in the industry for a while.

Better Performance

Q3 2022 Air France-KLM (Air France-KLM)

{kind=link}

The most recent performance also shows improvement and with improvement I don't mean the year-over-year change because that was already expected. What I mean is improved margins with Air France and KLM showing similar margins. In Q3 2019, Air France had an 8.2% margin while KLM had a 16.2% margin. That's a significant gap. By Q3 2022, Air France margin grew to 11% while KLM had a 14% margin pressured by capacity constraints at Schiphol. The group as a whole saw margins improve from 11.7% to 13% and I would say that this should be the start of more unified performance within the group.

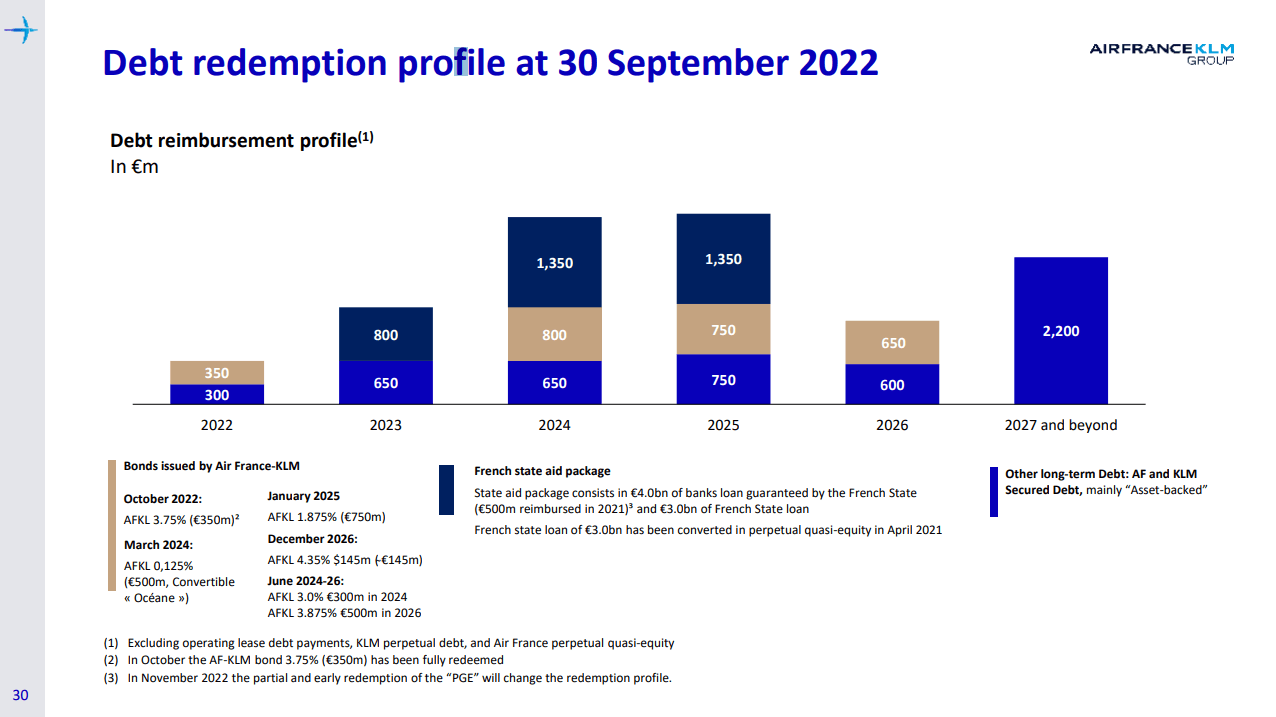

Debt Profile Improving

Debt maturity Air France-KLM (Air France-KLM)

{kind=link}

Ideally, I would like to see companies having a debt free runway of a year or two ahead, but for airlines that is simply not realistic at this point. With €12.3 billion in cash at hand, the company can fully cover its financial liabilities for the coming years. This excludes lease liabilities, but its net debt has already improved from €8.2 billion at the start of the year to less than €6 billion and I think with the current demand environment we can expect that reduction in net debt to continue with its net debt to EBITDA now at 1.6x compared to 11x in 2021.

Conclusion: Air France-KLM Could Be A Buy

Given the strong liquidity, improved business focus and manageable debt and low-risk of further dilution, I do believe that there's a compelling entry point for shares of Air France-KLM. The company currently trades at over 16 times earnings, which doesn't sound attractive but it has a history of trading at elevated PE ratios partially due to the non-performance at Air France. With Air France performance also improving and a better business and product strategy, I would think Air France-KLM should be able to improve results allowing shares to trade at higher levels but not at the exorbitant high price-to-earnings levels previously seen.

For further details see:

Time To Buy Air France-KLM