JBSAY - Time To 'BUY' JBS The World's Biggest Butcher? I Say Not Yet

2023-11-22 09:45:58 ET

Summary

- JBS S.A. is the world-leading company in several types of consumer meats and packaged foods. The company has a long history and is likely to be a continued market leader.

- The company is currently in a declining trend, making it an attractive prospect for long-term investment, as long as the fundamentals hold up.

- I give you my view on JBS S.A., which at this time is a positive view with upside, and a "BUY" rating.

Dear readers/followers,

I make a point out of investing in attractive consumer staples. Butcher and meat businesses such as JBS S.A. (JBSAY) are pretty rare on the market - a few peers exist in the meat market, but this is not the most common type of company.

In addition to this, we're talking about a Brazilian company. I have a few investments in this market and in South America or with SA exposure overall - and the common denominators for these investments are relatively high volatility - but also, typically, a relatively high yield. JBS S.A. is certainly no different from its peers in this regard.

In this article, I'll take a look at this global butcher and see if you, as an investor from a profitability standpoint and valuation perspective, should consider taking a stake in this company either for the long or short term.

This article represents my foray into more international sorts of businesses - because attractive businesses exist all over, not just in Europe or North America, which are my main markets.

Let's see what we have going for us here. This is my first and initiating article on the company.

JBS S.A. - The world's biggest butcher, potentially on sale.

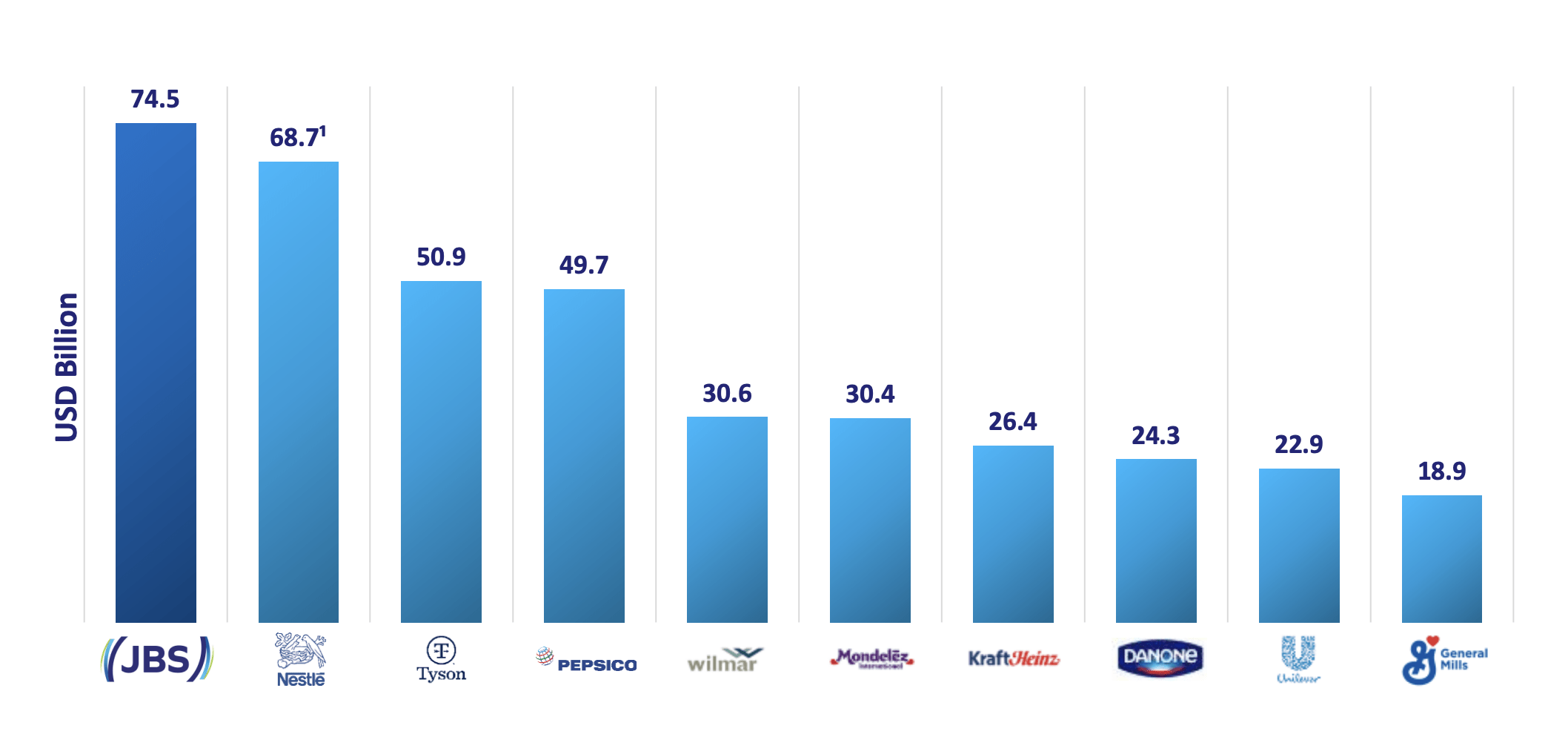

JBS is the biggest in a lot of things. The company is the largest beef and the largest poultry producer in the entire world. It's also the second-largest producer of pork on the planet, with a leading position in lamb as well. In short, the company is one of the most significant producers of meat out there, with the following well-known brands under its belt (though this is only a small selection of them). (Source: JBS )

{kind=link}

It's by far the largest producer of foods in terms of billions of dollars in revenue and makes even established companies look small in comparison - or at least, smaller.

{kind=link}

Aside from the segments I mentioned, the company has also moved into, and is already one of the leading players in Salmon, with #2nd place in Australia, and is also a leading player in VAP products, such as prepared foods where it has a #2nd place in Brazil, #1 in the UK, New Zealand and Australia.

Surprisingly perhaps for a traditional meat producer, the company has moved into plant-based and alternative proteins as well, holding the leadership position in Brazil, and the #3rd position in Europe in terms of plant-based proteins. When it comes to investing in these segments, I would rather invest in these companies that already have a market-leading position than I would invest in other companies that need to grow their customer base and whose only appeal is this, such as Beyond Meat (BYND).

The company's history is a successful one of growth that goes back almost 20 years, if we look at the company's international diversification and expansion. If we look at the company's current 2023E mix, we see that the company is mostly a NA/Brazilian-based protein business , because over 60% of net sales come from these geographies alone. If we include Asia, specifically China and Japan, we're looking at almost 75% of the total sales coming from these, with currently only 9% from Europe, 3% from Africa, and 3% from NZ and Australia. That leaves the company open for significant expansion. (Source: JBS SA )

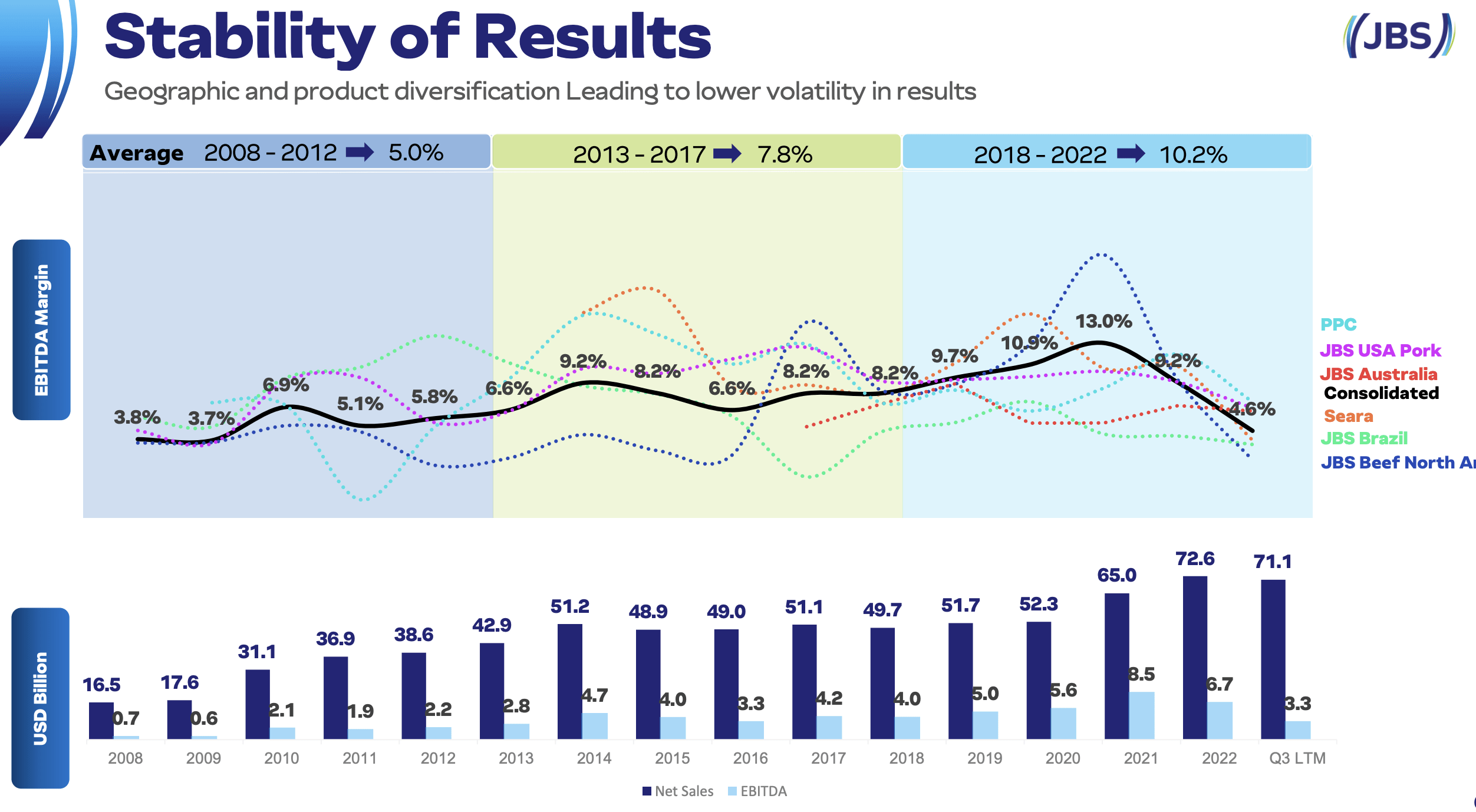

What's more, despite being a Brazilian company, which are typically somewhat volatile due to several factors including FX, this business has managed a through-cyclic attractive earnings trends, with EBITDA not dipping into the negative for going on 15 years at this point.

{kind=link}

The company employs 270,000 people around the world, the majority of which (the vast majority with 152,000) are employed in the company's home nation of Brazil.

JBS is a play on demographic macro. We're talking about being over 2,8B more people in 2050, we're talking urbanization and new moves to wealth, with the income growth supporting a trend to growing protein consumption - regardless of how this protein is consumed and in what form. The company's growth in supermarkets and online sales, as well as its plant protein segments, are part of this overall shift. Sales are made to 330,000 clients around the world in 180 countries, and the company manages 500+ offices spread around 20 nations. (Source: JBS )

The company can be characterized as well managed, with plenty of independent oversight, with 78% of board members completely independent.

3Q23 was a good quarter for the company as well, on an operational basis. The industrial complex which was started by the company in Rolandia was inaugurated, a new breaded chicken/hot dog plant, the largest in these categories in all of Latin America. These also represent the most modern and automated plants in these segments in the entire world.

The company has also been aggressive with its debt - in October, the company issued certificates and with the proceeds of these paid down short-term debt and increased its average debt to around 12 years. The company also issued senior notes, at a coupon of 6.75% with maturities in 2035, and yet another with a coupon of 7.25% and maturity in 2053. The company, as such, is among the businesses that can issue 30-year notes at a contextually relatively appealing interest rate, implying a conservative and safe outlook for the company.

This likely has to do with the company's business model, which is very solid. The company trades under the native Brazilian ticker JBSS3. Some of the fundamental KPIs aren't as good as you might expect from the world-leading meat producer. The company has decent cash on the books, but a debt to equity of 2.8x, which is high for the sector, and a sub-1x interest coverage ratio as of this time, with a debt to EBITDA of above 6.5x, due to the company's lower EBITDA this year. The company's dividend yield of 9.24% is one of the highest in the entire sector, though this dividend is hardly sustainable in the long term given current earnings. (Source: JBS SA )

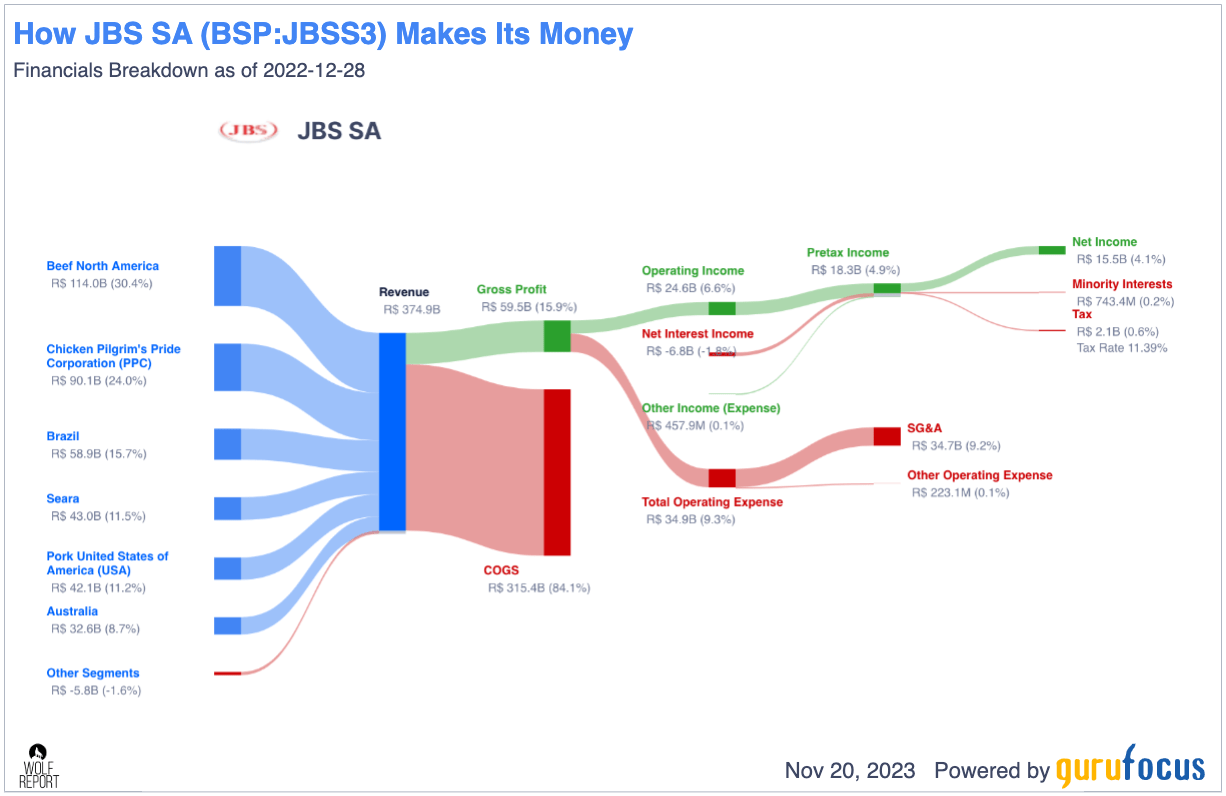

The combination of new debt issuances coupled with the current high dividend, the somewhat declining margins, and the business model specifics - which for 2022 looks like this, confirms that we're looking at a company that despite some stability, is still what we expect out of a Brazilian producer and company.

{kind=link}

The extremely high COGS is a product of this industry. Peers that are global or regional, such as Tyson Foods (TSN) are showing similar, even worse trends in terms of COGS. A good net margin for this industry is somewhere in the neighborhood of 5-6%, with JBS managing a high over the past 10 years. The last few months were, despite the company's work, impacted by both inflation and geopolitical factors.

Revenue was down as sales increases were unable to make up for a reduction in demand, and EBITDA was down materially, down to a margin for 3Q23 YoY to 5.9% in margin from 9.6%, and a reduction of over $700M. This naturally impacted the company's net result, which was down to $117M from $765M from the last year.

It doesn't need to be mentioned that the company is unable to keep up the near-double-digit dividend yield we saw last year here. However, it's fair to characterize this downturn as momentary over the longer term, and for this company to potentially be attractive here in terms of valuation.

At least, most valuation models show there to be a non-trivial upside to this stock here. We're clearly in a dip, but just as clearly based on trends, that's moving up again in 2024-2025.

JBS SA - The valuation implies this being a trough, with eventual upside in 2024-2025.

When it comes to evaluating JBS S.A. I go for fairly simple models. The company currently trades well outside of what I would consider its standard price range of between BR$ 28-40.

The company's unfortunately volatile EPS trends make earnings-based forecasts very difficult. Instead, we can focus on Median sales values, projected free cash flow, and book values. Forecasts tend to be inaccurate here, as is the case with many businesses I've reviewed from Brazil. The company, despite a storied history, manages only a 40-50% accuracy, essentially the overall forecast accuracy of a coin toss.

Street targets for this company have declined for the past year and more. A year ago, during the height of the EPS, the company was forecasted to be worth between BR$34 to BR$77/share, with an average of BR$50.75. We're now down to an average of BR$28, from an average of BR$22 to BR$38, which represents essentially a halving of all targets here. 10 out of 14 analysts are at a "BUY" here, showing a relatively high conviction.

Even a conservative sales multiple in a peer context gives the company a valuation of BR$ 35/share or above here. (Source: TIKr.com)

Based on how this company works in terms of fundamentals what it manages, and how massive it is, I would view any sort of fundamental deterioration of this company's long-term fortunes as an extremely unlikely prospect. While the company is currently in an earnings slump, both the history of the company's earnings as well as the underlying demographic and macro trends speak in favor of companies like this in the long term. I expect margin recovery and earnings recovery in 2024E, followed by more in 2025E, and just as I have been with previous companies out of Brazil, I am happy going "in" here and giving this company a "BUY" rating at this time.

To be clear, I'm not going in "deep" here. I'm always sizing my stakes in accordance with risk, and the risk here is not "small" as such, at least in terms of investment volatility and how much money I can expect out of this company in the short- to medium-term.

However, I'm a long-term investor - and JBS is a company I'd be comfortable holding for several years if nothing changes.

I give you my thesis here.

Thesis

- JBS SA is the world's largest butcher. It's also a company that's currently trading at a very high normalized P/E, but this is only due to the sheer decline in 2023 results, where the earnings have declined and are expected to come in at a level no higher than BR$0.09 - though normalize towards higher single digit EPS in 2024-2025.

- In the case of normalization, this company currently trades at a very cheap level. Despite what I would view as sub-par leverage at 66.77% LT/cap, and a credit rating of BBB-, I would say that with the right expectations, this company is certainly a "BUY" here.

- I would say JBS is worth at least BR$25/share even in the most conservative of forecasts and fundamentals, which makes this company a "BUY" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversions.

The company's dividend can't be called well-covered, and the company can't be called cheap in the context of its current earnings, but I do see an upside here that to me justifies going in with a "BUY".

For further details see:

Time To 'BUY' JBS, The World's Biggest Butcher? I Say Not Yet