AR - Time To Get Paid: 2 Stocks With Yields Up To 14%

2023-04-13 07:00:00 ET

Summary

- In this article, I make a case for investing in high-yield stocks and the risks investors should consider before buying stocks in that category.

- I present two stocks related to the energy sector that come with juicy yields and strong parent companies that provide strong product flows.

- Both stocks have healthy balance sheets and the ability to generate satisfying long-term total returns, despite their high yields.

Introduction

I'm usually not an investor in high-yield stocks - at least not the kind of yields we're about to discuss in this article. Because of my focus on dividend growth, I often ignore the biggest cash cows in the room, as I am not yet in a stage where I want to prioritize dividend income over capital gains.

That said, there are many reasons why investors might want to buy high-yielding stocks. I also own some high-yield stocks to boost the average yield of my portfolio - for tax reasons.

In this article, I will give you two high-yielding cash cows with different yet similar business models, yields, and risks.

- One stock is an agriculture/energy high-yield cash cow with a small market cap and a very high yield.

- The second stock is an energy midstream company with room to grow its dividend and a strong long-term demand outlook.

So, without further ado, let's dive in!

Buying High-Yield

What's a high yield?

Using the Vanguard High Dividend Yield Index Fund ( VYM ) as a benchmark, a high yield starts at 3.1%. I use this ETF as a benchmark to assess whether something is a high yield or not. I also have to say that most high-yield stocks in my portfolio have yields between 3.0% and 5.5%.

While I would argue that 3.1% is not a high yield in the current interest rate environment, I am still sticking to these definitions.

In this article, we're going a step further.

However, before I present my picks, it's important to discuss a few things.

First of all, too many people mess up when it comes to high-yield stocks. I have seen so many people focus on dividends only. These people buy everything with a high yield. For example, mortgage REITs, high-risk REITs like Medical Properties Trust ( MPW ), and high-risk plays like ZIM Integrated Shipping Services ( ZIM ).

The other day, someone showed me his portfolio. Half of his holdings were down more than 50%, offsetting any benefits from high dividends. Moreover, a significant number of stocks had cut their payout in the past 12 months.

Even worse, this person is 45 and enjoying a steady job, which means there is no need to prioritize income over long-term total returns.

Furthermore, I'm not cherry-picking here. I could write a book about all of my discussions with people who make similar mistakes.

That said, buying high-yield makes sense in some cases. I do it for tax reasons. Others do it as it allows them to retire from cashflows. And in some cases, it makes sense to switch from growth to value due to macroeconomic reasons.

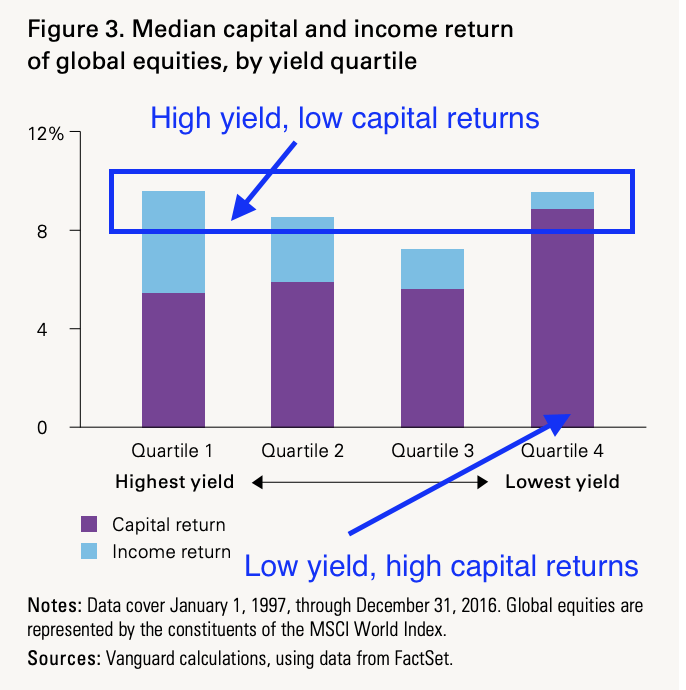

When buying high-yield, people need to be aware of the balance between capital returns and income returns. Essentially, the total return on the stock market is a combination of capital gains and income.

As the overview below shows, low-yielding stocks tend to have mainly capital returns. High-yielding stocks have higher income returns.

{kind=link}

Needless to say, this only holds when low-yielding stocks are able to grow rapidly and if high-yielding stocks are able to also provide some capital gains. Or, to put it differently, it only works when buying high-quality stocks.

There are countless low-yielding stocks with low or negative capital returns and plenty of high-yielding investments that have unsustainable dividends and deeply negative capital returns.

Now, let's focus on my picks. Please note that I will write more articles like this one. This article includes two stocks related to the energy industry. The next one might be very different. So, please let me know in the comments what you're looking for in the high-yield space, so I can incorporate these suggestions.

Agriculture High-Yield With Green Plains Partners ( GPP ) - 14% Yield

Earlier this month, I wrote an in-depth article covering this stock. I decided to put the stock in my high-yield model portfolio, as I like the value this somewhat unusual stock brings to the table.

Headquartered in Omaha, Nebraska, GPP is a midstream company. In other words, it manages the flow of energy (and related) commodities. Please be aware that this company comes with a K-1!

This business, with a market cap of $300 million, operates as a publicly traded master limited partnership ("MLP"), adhering to the regulations set forth by the Internal Revenue Service ("IRS") in the United States. MLPs, as per the IRS guidelines, are typically exempt from federal and state income taxes. Instead, each partner is responsible for reporting their portion of taxable income, gains, deductions, or losses on their respective individual income tax returns.

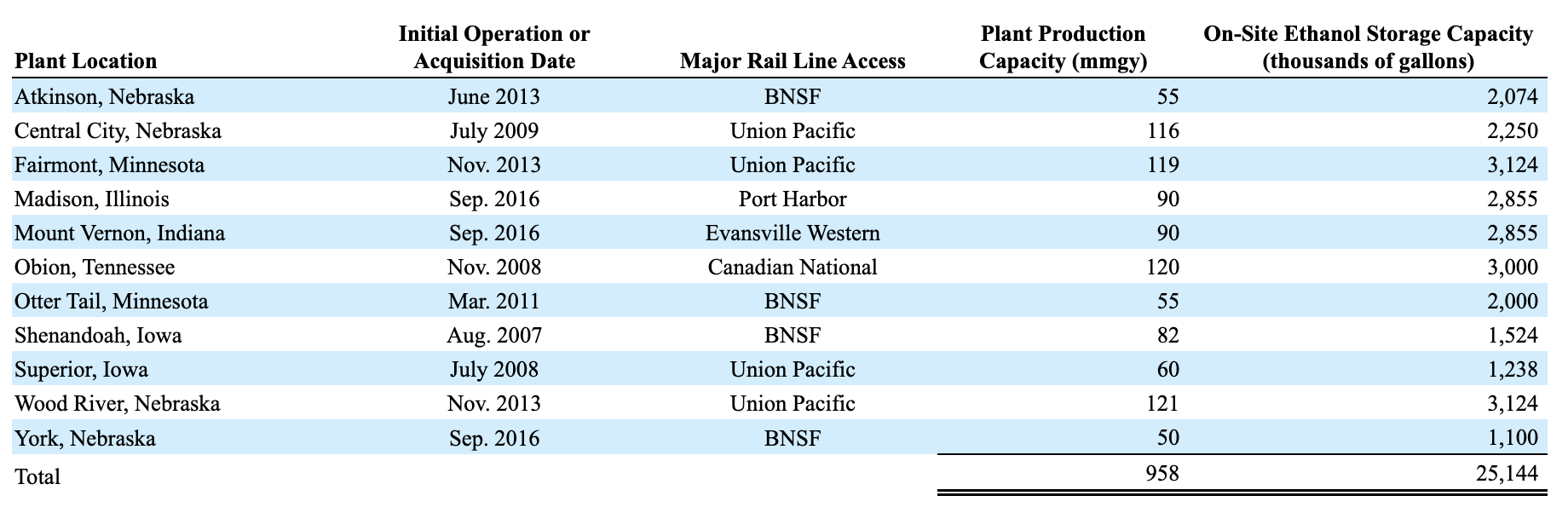

That said, GPP owns the fuel storage and transportation assets of its parent Green Plains ( GPRE ). Green Plains is a major ethanol producer in the United States. It owns 100% ownership interest in GPP's General Partner and 48.8% of limited partner interest.

This eliminates competition risks for GPP, as it is tied to GPRE. GPRE has the ability to produce roughly 960 million gallons of ethanol per year and various byproducts. I discussed GPRE in this article .

{kind=link}

GPP makes money on the storage and transportation of these products. Hence, it's a play to benefit from ethanol without being subject to its volatile margins. GPP makes money on throughput, while its parent GPRE is dependent on margins on ethanol sales. After all, it buys corn, which it turns into ethanol. That's not impacting GPP's income.

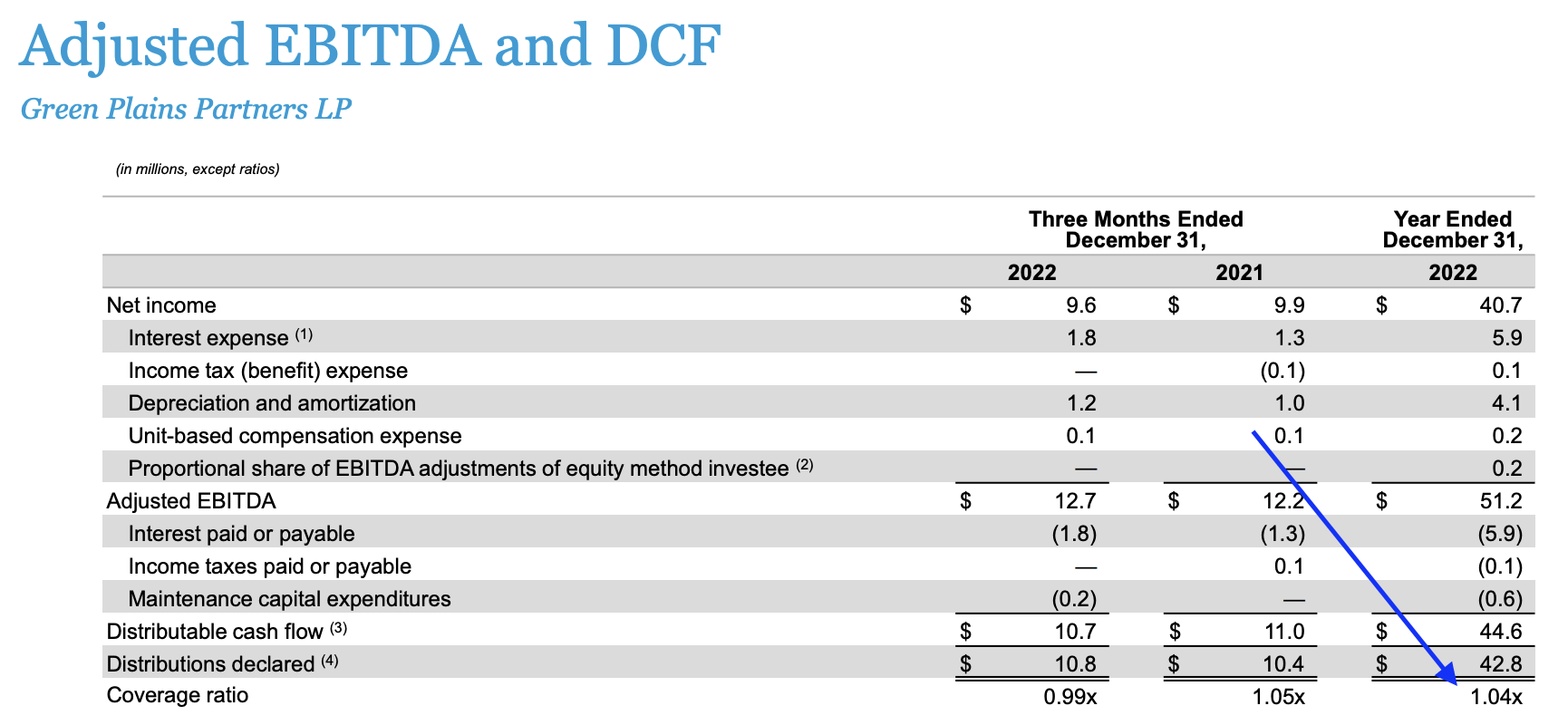

In 4Q22, the company had total storage volumes of 226.2 million gallons. Its terminal services saw flows of 50.7 million gallons. During this quarter, its parent GPRE lost $32 million due to low ethanol margins.

GPP made money as it is not subject to these margins. The company generated $9.6 million in net income. On a full-year basis, the company generated $40.7 million in net income. Distributable cash flow during this period was $44.6 million, thanks to extremely low capital requirements. After all, the company has everything taken care of. It has the assets it needs and no major growth plans in need of cash.

{kind=link}

In 2022, the company paid $42.8 million in dividends. This means that its 14% yield was fully protected by distributable cash flow.

That said, the payout ratio in 2022 was 96%. When adding that the company doesn't have a lot of room to grow, we're dealing with a cash cow. There's not a lot of growth in this stock. But that's OK, as GPP is a yield play that comes with small long-term capital gains (according to my expectations).

The balance sheet is healthy. Net debt is just 0.8x EBITDA, and the company has no debt maturities until 2026.

When looking at its dividend, we see that the company cut its dividend by 75% in 2020. Back then, the pandemic reduced ethanol demand. After all, ethanol is tied to the energy industry. When fuel demand goes down, ethanol demand falls as well. However, because of its balance sheet, the company did not run into trouble. When demand came back, the dividend was hiked again.

So, even if the dividend is cut in the future, I expect that the dividend will continue to be tied to ethanol volumes, which leads me to believe that GPP will remain a cash cow for many years - if not decades.

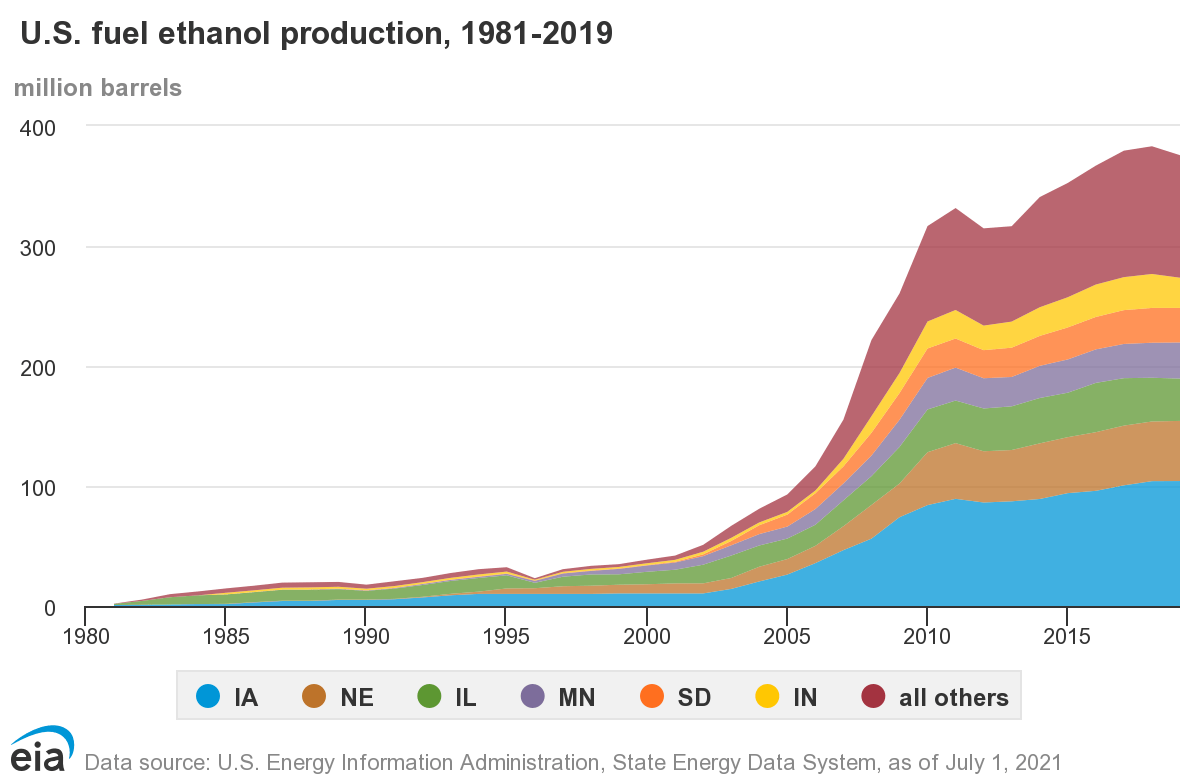

In the early 2000s (and prior to that), ethanol wasn't a big deal. However, because of government regulation, it became a huge tailwind for farmers. 40% of all corn crop in the US is turned into ethanol. Annual production is now close to 400 million barrels. That's fuel ethanol only. Iowa alone produces more than 100 million barrels of ethanol per year.

Energy Information Administration

{kind=link}

Since 2013, roughly 10% of the gasoline consumed consists of ethanol. This explains why ethanol and corn have become energy commodities.

Energy Information Administration

While this means that investing in GPP relies on the government to stick to its support for ethanol, there is no reason to believe this will change. After all, neither political party is willing to address this issue. It would have such a massive impact on the Corn Belt that it would make winning any major election impossible.

Moreover, as I wrote in my GPP-focused article, politicians in the Corn Belt are pushing for a 15% ethanol blend. Even if this would only apply to Corn Belt states, it would have a major impact on demand.

On top of that, ethanol is environmentally friendly and a great tool for decarbonizing road traffic. Moreover, if energy prices remain high, it becomes attractive to increase the ethanol mix in gasoline for cost reasons.

So, to summarize, GPP:

- GPP has a very high yield, which is covered by steady ethanol flows.

- The company has low CapEx requirements and a healthy balance sheet.

- While it depends on politics, the long-term ethanol bull case is strong.

- Its dividend is likely to be cut during recessions that impact energy demand.

- However, the company will quickly boost the dividend when demand rebounds.

I expect little in long-term capital gains, but the mix of its high yield and healthy business make it a suitable play for income-oriented investors. However, due to cyclical risks, I would not go overweight GPP.

The stock is a holding of my high-yield model portfolio, as I expect that long-term total returns will be satisfactory.

High Natural Gas Income With The Antero Midstream Corporation ( AM ) - 8.6% Yield

Just like Green Plains Partners is connected to Green Plains, Antero Midstream is connected to Antero Resources ( AR ), one of the biggest natural gas producers in the United States. I recently wrote an in-depth article on Antero Resources. I highly recommend readers take a look at that article, as it includes my view on natural gas and liquid natural gas.

That said, Antero Midstream is not a Master Limited Partnership. In other words, it does not issue a K-1. It's a normal C-Corp and available to almost every investor, both domestic and international. This is somewhat rare in this industry, which is one of the reasons why AM is included in this article.

With a market cap of $5.1 billion, Antero Midstream owns, operates, and develops midstream energy assets that primarily serve Antero Resources' production and completion activity in the Appalachian Basin in West Virginia and Ohio. Its assets include gathering systems, compression facilities, water handling, and blending facilities, and interests in processing and fractionation plants.

The company conducts its operations and owns its operating assets through Antero Midstream Partners and its subsidiaries, which are wholly owned.

Antero Resources holds 29.1% of Antero Resources. Because of this relationship, Antero Midstream does not have any competition, as it is responsible for AR's operations. Unless a miracle happens, this won't change.

Just like GPP is an ethanol play without the margin risks its parent faces, one can think of AM as a natural gas play without the pricing risks that come with it. However, there's also less upside in case natural gas prices explode.

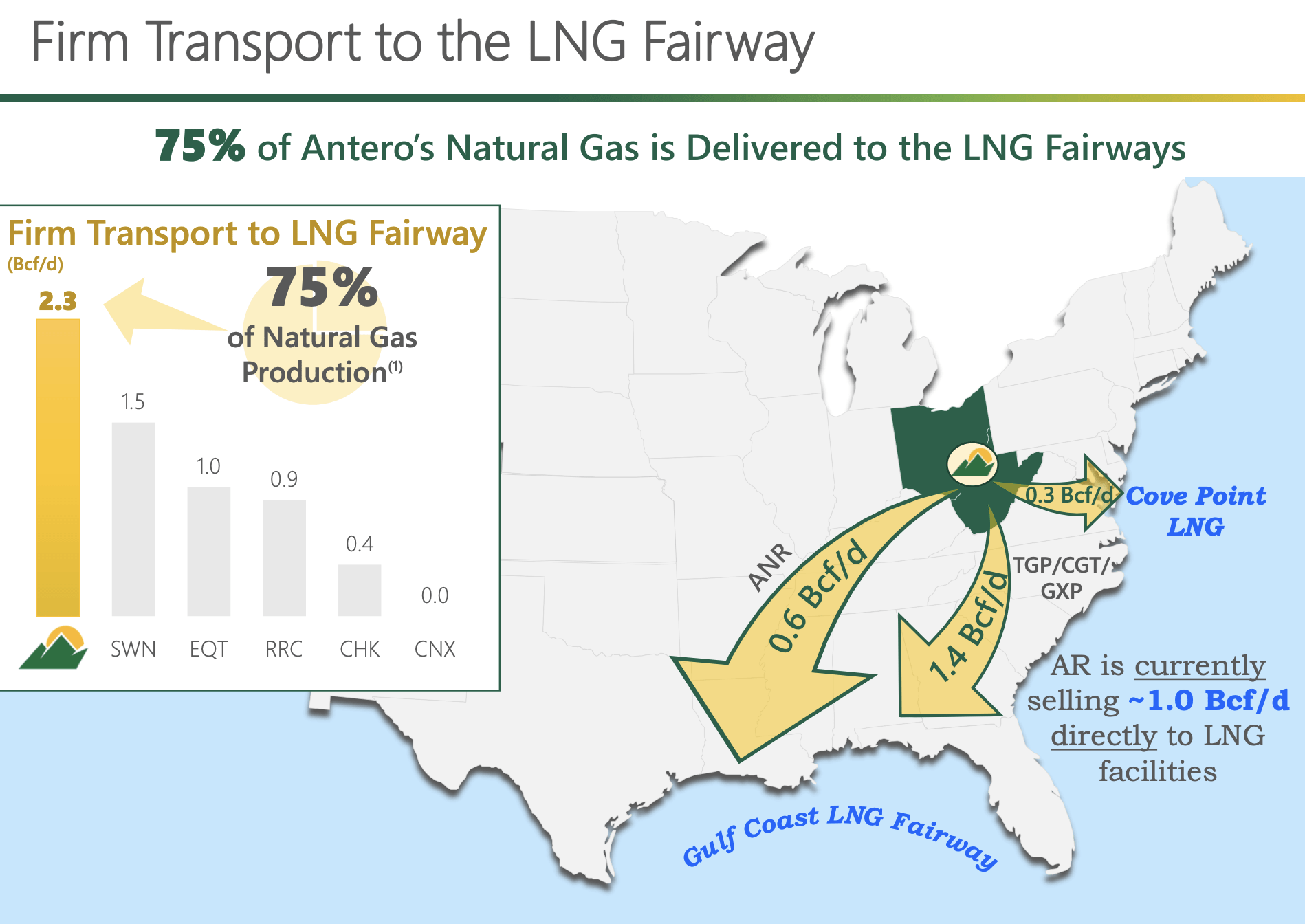

As I wrote in the aforementioned article, Antero Resources and Antero Midstream are highly tied to one of the biggest bull cases for natural gas: liquid natural gas ("LNG"). 75% (2.3 billion cubic feet per day) of its production is led through the LNG Fairway, and 1.0 billion cubic feet per day is directly sent to LNG facilities, which comes with great pricing benefits for Antero Resources and safety for Antero Midstream, as these energy flows are desperately needed for the global LNG market.

{kind=link}

At the end of this year, the US will be able to export 14.9 billion cubic feet per day. Next year, that number could be 18.3 bcf, followed by a steady surge to 34.0 bcf in early 2027. These numbers are based on planned export projects, so we can assume that the actual outcome will be very close to this number (maybe higher!).

While this benefits AR way more than AM, it does almost guarantee that volumes through its pipelines will be high.

Not only that, but Antero Resources is sitting on at least 20 years' worth of high-quality inventories, which means a sudden inventory depletion won't be a risk to natural gas flows. Many smaller natural gas companies are struggling with these issues.

Note that after 20 years, the company won't go out of business. AR is steadily finding new resources.

Moreover, AR has more than ten years' worth of inventory at breakeven prices below $2.0/Mcf, which is roughly $2.07/MMBtu. So, even distressed natural gas prices would not cause natural gas flows to stop because AR stops unprofitable production.

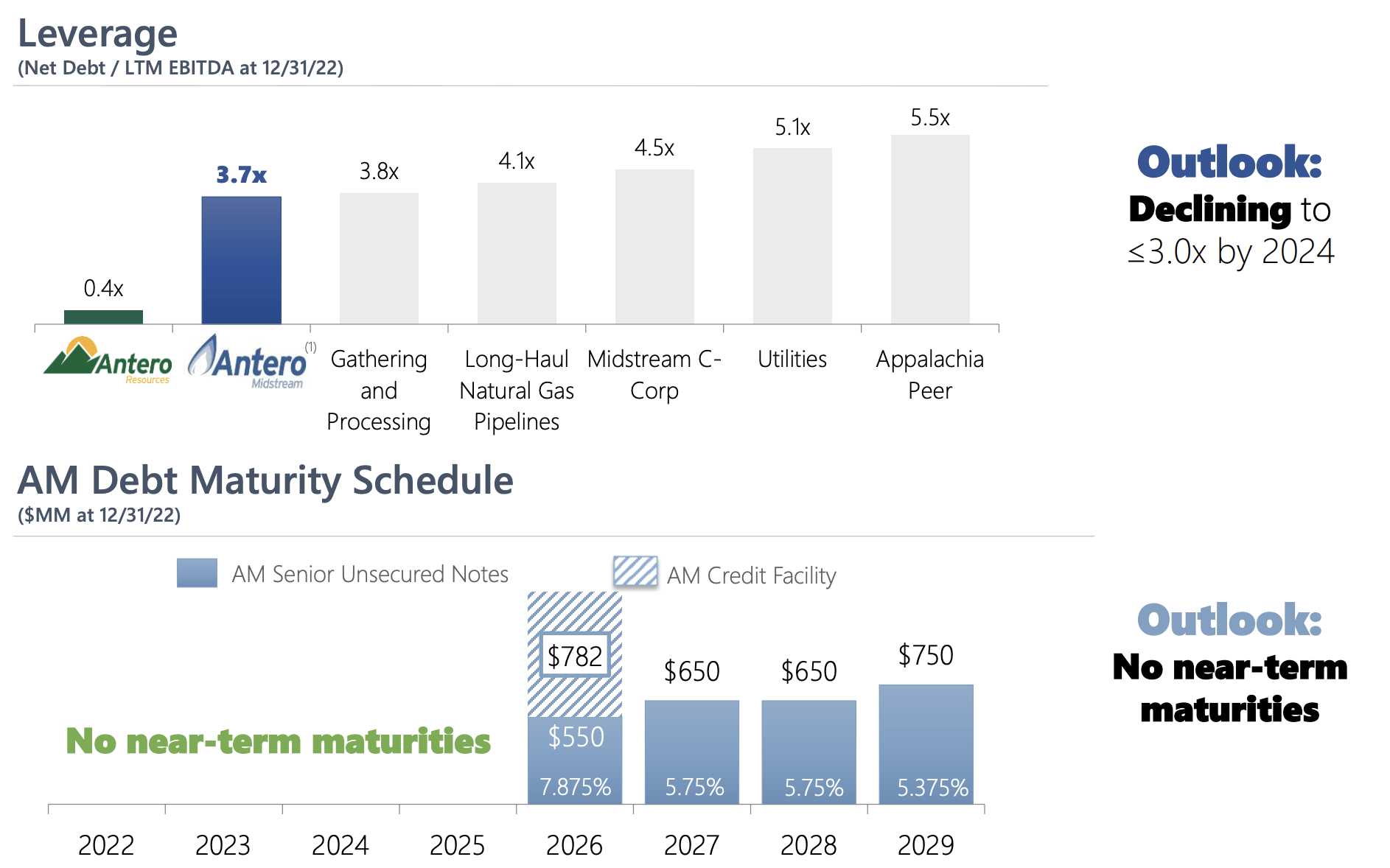

Furthermore, Antero Midstream has a healthy balance sheet with a net debt ratio of less than 4x EBITDA. By the end of next year, that ratio is expected to be below 3.0x EBITDA. Also, as visible in the slide below, the company has no debt maturities until 2026, which is especially great given the current high-rate environment.

{kind=link}

With that said, because AM is tied to AR, its growth CapEx is limited. Most operations are in place, and only incremental production growth calls for growth investments in infrastructure.

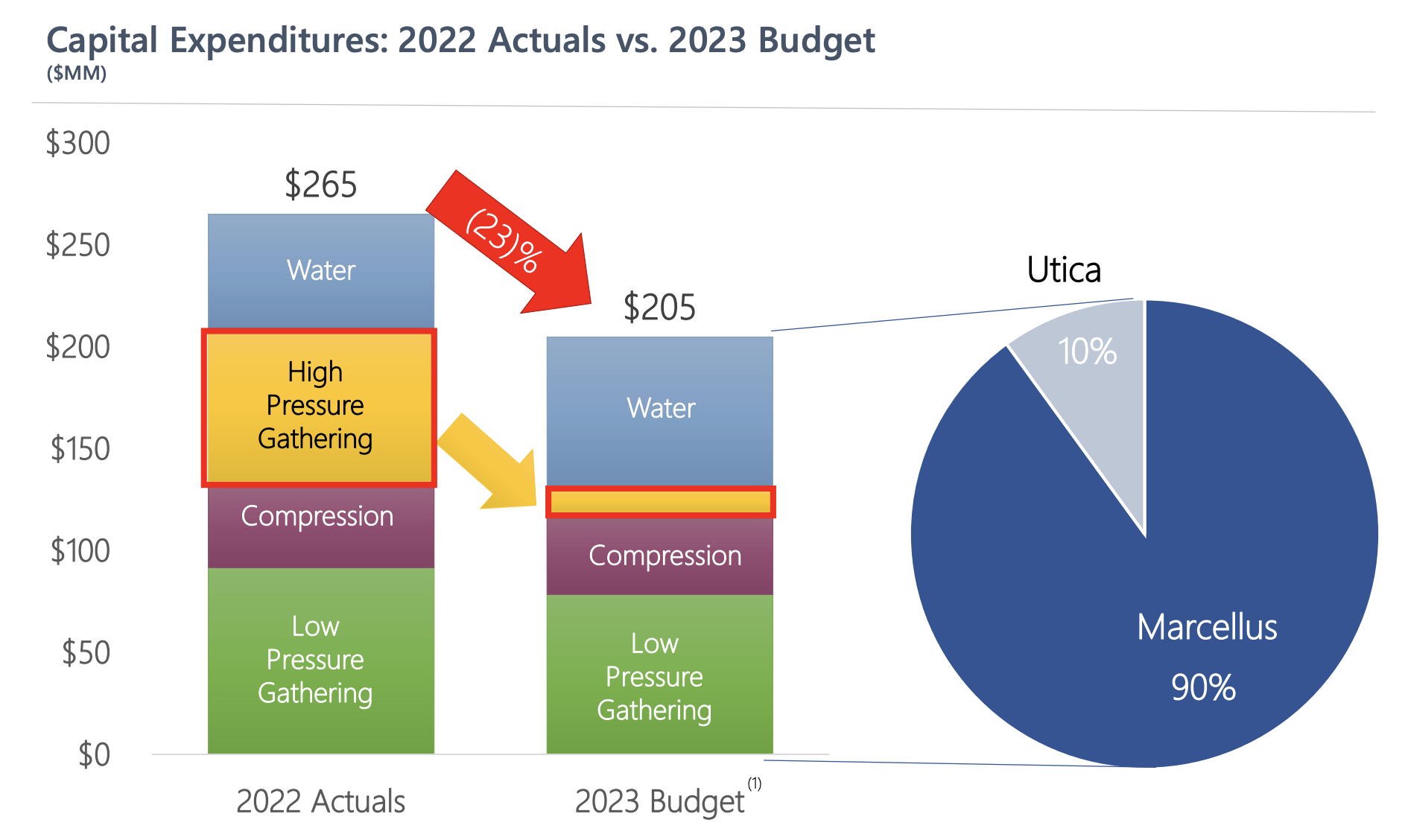

Hence, the company had a CapEx of just $265 million in 2022. In 2019, that number was close to $650 million. This year, the company has budgeted between $195 and $215 million for CapEx, another big step down versus 2022. This number is expected to decline further through 2027.

{kind=link}

EBITDA is expected to grow by 7%.

Even better, through 2027, the company is expected to consistently grow EBITDA by 2% to 4% per year.

With regard to the dividend, the company is expected to generate $540 million in free cash flow this year. This translates to a 10.6% free cash flow yield. Next year, that number could be $640 million, or 12.5%. This indicates that the dividend is safe and able to grow further.

While this may be the case now, the dividend wasn't safe in the past. In 2021, the company cut its dividend. The current dividend is $0.225 per share per quarter or $0.90 per year.

That said, the future is likely looking better.

Over the five-year period from 2023 to 2027, Antero Midstream targets a substantial amount of free cash flow before dividends, with the assumption of a flat $0.90 dividend on an annual basis. This expected free cash flow after dividends will be utilized for ongoing debt reduction and, once the leverage target of less than 3x net debt is achieved, an increased return of capital to shareholders. Hence, it's likely that investors will see a dividend hike at the end of 2024 or early 2025. While that is a long time, the current dividend yield of 8.6% is a good deal - in my opinion.

So, while AM is far from risk-free, I like it as a high-yield energy play, and I put it in my high-yield model portfolio and on my watchlist, as I am considering buying it to improve my average portfolio yield.

Takeaway

In this article, we discussed two stocks with very juicy yields. While both come with cyclical demand risks, I like the risk/reward of both. Green Plains Partners has the benefit of a very strong long-term demand case for ethanol and the fact that its parent is a highly efficient ethanol producer. Its balance sheet is very healthy, and low CapEx needs allow for a 14% dividend yield.

Antero Midstream is a C-Corp, which operates the midstream assets of its parent company Antero Resources. The company benefits from a strong long-term natural gas demand outlook, access to the LNG Fairway, a healthy balance sheet, and the substantial premium resources of its parent company.

Moreover, while it does have a history of cutting its dividend, the current 8.6% yield looks safe. Moreover, once the company achieves its leverage targets (likely at the end of 2024), management is in a good spot to boost the dividend quite significantly.

Again, while both stocks come with risks, I like them as income plays without giving up on potential capital gains.

Going forward, we'll discuss more high-yield trades, so please don't hesitate to give me your views, requests, and opinions.

For further details see:

Time To Get Paid: 2 Stocks With Yields Up To 14%