VTIP - TIPS Funds Vs. A Ladder

Summary

- TIPS performance could rival that of the S&P 500 over the next decade.

- TIPS can serve as a low-cost, do it yourself annuity for those near or in retirement.

- There are important differences between buying TIPS via a fund/ETF or a bond ladder.

- The ladder has several key advantages, especially for those seeking higher certainty of income and cashflow.

- Current rates are near 14-year highs but might get even better.

This is a follow-up to my last article, TIPS Performance Could Rival That of the S&P 500 Over the Next Decade . There I outlined the case for TIPS, which could return about 5-6% per year in the coming ten years. Here I discuss how investors might buy TIPS, comparing mutual funds/ETFs versus a ladder of individual bonds. There are differences, but for many investors, especially those at or near retirement the nod will go to the ladder. Each investor is unique, so the approach will depend on their goals, situation and preferences.

TIPS Can Serve As A Low Cost, Do It Yourself Annuity Income Stream

For investors at or near retirement, a TIPS ladder is an effective means of generating reliable, predictable income. For more details, I highly recommend Playing Inflation Russian Roulette in Retirement , by William Bernstein. He also references a useful article by Alan Roth. Here are some key takeaways:

- TIPS are as close as it gets to risk-free assets. Rather than pay an insurance company for an annuity and bear inflation risk and the risk they may fail (witness AIG which required a bail out in 2008), TIPS effectively serve as a safe, DIY annuity product.

- TIPS are most effective and reliable if held to maturity . This argues in favor of buying individual bonds via a ladder, not a mutual fund or ETF. More on this below.

- You can build an effective TIPS ladder that is relatively simple, with a manageable number of holdings via a mix of auction buys and via the secondary market.

As someone who is also skeptical of insurance products, I offer Roth’s thoughts: “Actuaries are very smart people, and if they aren’t willing to take the inflation risk, I don’t recommend my clients take it either.”

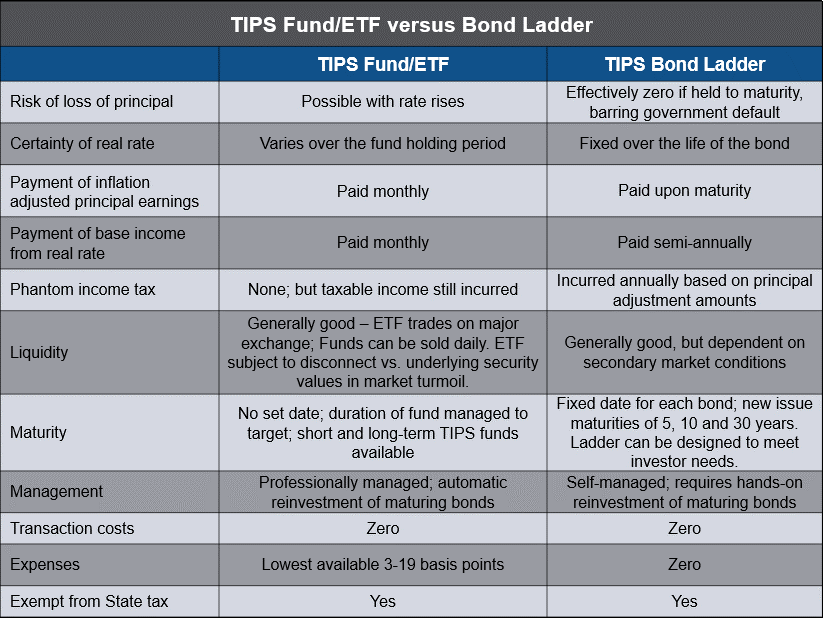

Differences Between a TIPS Bond Fund Versus a Ladder

There are two basic ways to buy TIPS – via a mutual fund/ETF or direct bond purchases. I believe the best way to invest depends on the investor. That’s why there is a market for both. The table below summarizes the differences.

{kind=link}

The Effect of Rate Movements on Investment Principal is a Prime Consideration for TIPS

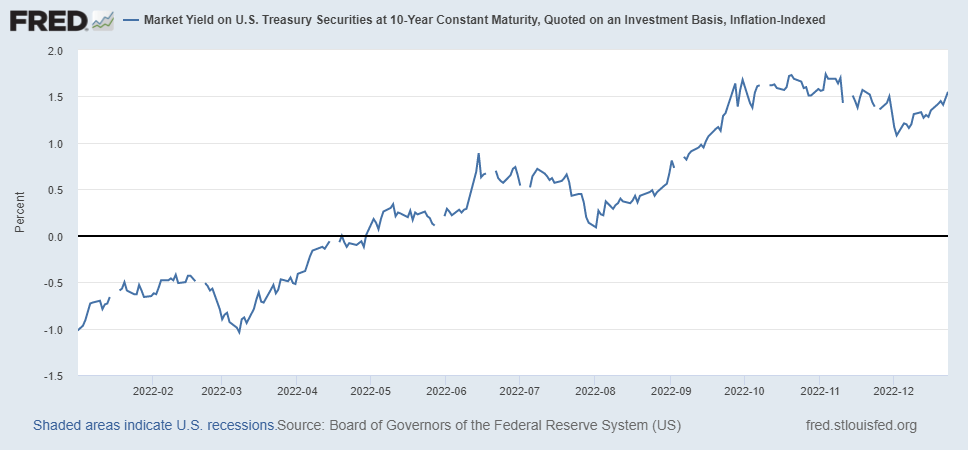

This was painfully evident this year. Fund investors have been punished as the 10 year real TIPS rate went from -1% to the current 1.6%. As a result, the TIP ETF is down YTD 12.2%. Since its duration is 6.94, for each 1% point rise in rates, TIP would decline by about 7%. Some of that loss was offset by the real interest earned and the inflation principal adjustments.

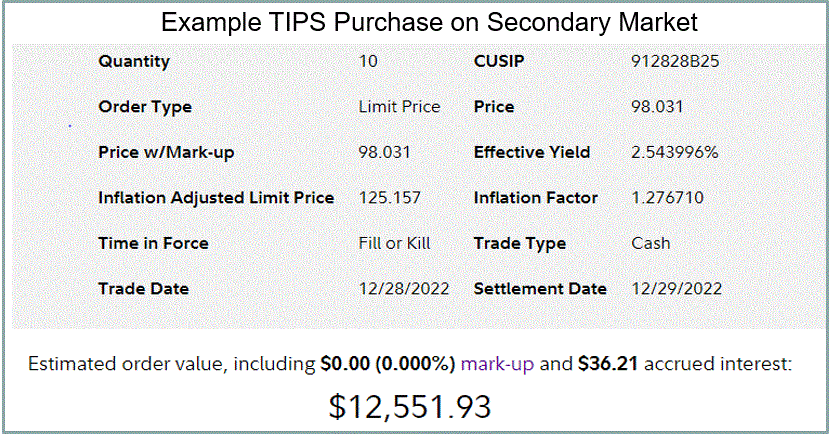

However, individual TIPS bonds held to maturity protect against principal loss in the event of rising real rates. To demonstrate, let’s look at an example. Today you could buy a TIP bond on the secondary market maturing in January 2024. The screen shot below shows the numbers for a live transaction via Fidelity’s brokerage platform.

{kind=link}

The ask yield to maturity, or real rate, is 2.54%. You could buy 10 bonds ($1000 face value each) for an investment outlay of $12,552. You’d earn two coupon payments at a rate of 0.625%: $40 in January and $41 in July. Let’s say real rates rise by one percentage point and inflation runs at 4% from now until the maturity date. At maturity, you’d receive an estimated adjusted principal payment of $13,278. Your total estimated earnings would be the gain from adjusted principal plus the coupons, or $812, for a total return of 6.5%.

Now let’s compare that to buying the TIP ETF. During the holding period your principal (market price) would decline by approximately 7 (duration) x 1% (rate increase) = 7%. Fortunately, that would be offset by the inflation principal adjustment of 4% plus the ongoing TIP ETF coupon yield. The coupon and principal adjustment payouts of the ETF will fluctuate throughout the year as the market real rate changes, the fund’s existing bonds mature and new positions are added. For sake of example, let’s say the real yield during the year averaged halfway between the current 1.8% and 2.8% in January 2024. That would generate 2.3% in coupon yield, leaving you with a total return on the TIP ETF of approximately -7% + 4% + 2.3% = -0.7%. That compares much less favorably to the more predictable individual bond return of 6.5%. These numbers aren’t exact but demonstrate an important difference between buying an individual bond versus a fund or ETF.

In my opinion, this is the most important advantage of buying individual bonds in a ladder versus a fund. This is especially important for retirement investors who want predictable income and cash flow.

Of course, if you want to bet on declining rates, you can buy a fund, which will appreciate if rates drop. In that event, your individual bond’s secondary market price would also go up, but if you held to maturity, you would not reap the benefit.

A TIPS Ladder Has Certainty of Real Returns

With the individual bonds, you also have certainty of your real yield over the entire holding period, unlike a fund where rates fluctuate. A fund reinvests maturing bond proceeds on a continuous basis for you. On the plus side, any price drop in the fund due to rising rates would be offset over time with higher interest rates. With the ladder, you would be manually reinvesting at the maturity dates.

There is No Need for a TIPS fund for diversification

From a bond diversification standpoint there isn’t a need to buy a fund. Unlike corporate or muni bonds where you want to diversify default risk across issuers, TIPS are effectively riskless assets backed by the full faith and credit of the US government. I know the latter phrase may evoke disdain among some readers. To be sure, TIPS have risks and shortcomings as I described in my last article .

TIPS Maturities Can Be Customized with a Ladder, But Require Effort

As far as maturities, ETFs and funds have continual turnover as TIPS mature and are reinvested. You can buy short-term TIPS funds like VTIP with an average weighted maturity of 2.5 years or the TIP ETF with a maturity of 7 years. A TIPS ladder can be designed exactly to your needs, but you will have to buy bonds on the secondary market given TIPS are issued at auction only in 5, 10 and 30 year maturities. Also, there is a “hole” in TIPS maturity target dates, with none that mature between July 2032 and February 2040.

The Treasury auction and secondary markets for TIPS require a learning curve

If you want to go the TIPS ladder route, you’ll need to understand the basics of any purchase. That includes the par value, inflation index, market price, and accrued interest. Fortunately, David Enna’s excellent website covers all this and more. If you want to buy TIPS at auction, check out the Treasury Department’s auction schedule .

My Approach – TIPS Bond Ladder

In my case, as an experienced investor in semi-retirement with a holding period of 15-25 years, I prefer a ladder. Given my cash flow and retirement plans, I am implementing a ladder with an average weighted maturity of about 18 years. Real rates now are 1.7% on secondary market TIPS maturing in February 2040. This nicely complements my all-weather portfolio with inflation protection and a nearly risk-free return that approaches my overall portfolio real return goal of 2%.

The ladder approach is also viable for me since I don’t need immediate access to a fund's extra monthly income from principal adjustments. I am also very comfortable with setting up and managing a bond ladder. Finally, I like low cost. A bond ladder via a brokerage account like Fidelity or Vanguard costs nothing. There are no transaction costs and no annual expenses – which is even better than the best funds and ETFs that charge 3-20 basis points.

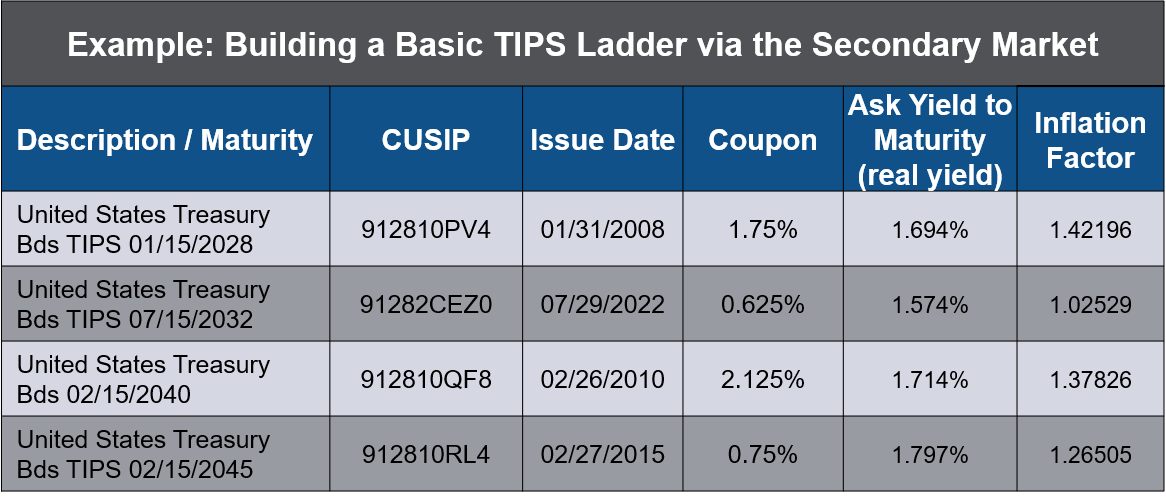

The table below shows an example of a basic TIPS ladder that could be constructed via secondary market purchases. It has an average maturity of about 13 years with real yields ranging from 1.57% to 1.79%. Since secondary market TIPS have inflation accruals which could decline in a deflationary scenario, it’s also favorable to buy at Treasury auction, which occur on a regular schedule.

{kind=link}

I carry my TIPS in both Traditional and Roth IRA accounts to shelter the income from taxes. Conventional wisdom says to put TIPS in tax deferred accounts like IRAs and 401ks and put stocks in a Roth given their expected higher returns than bonds. However, as I demonstrated in my last article, TIPS returns could equal or even exceed those of equities over the next 10 years, so I carry some of my holdings in a Roth.

Why Use a TIPS Fund

Although I believe the ladder is better for me, there is a role for funds. For example, those with limited account options may prefer - or even require a fund. Some investors may not have substantial funds available in a Traditional IRA or Roth IRA brokerage account. They might have most of their retirement portfolio in a 401K or SIMPLE IRA. In that case, they probably won’t be able to use a brokerage account to access the primary or secondary TIPS markets. Also, investors who don’t want to lock up funds in individual bonds for a long time, or those who don’t want to set up and manage a TIPS ladder might prefer a fund. Finally, those who want access to the more regular and larger income payouts might prefer a fund.

A short-term TIPS fund can also be very useful. A Vanguard paper, The Long and Short of TIPS , indicated that short-term TIPS have much higher correlation with inflation than long-term TIPS: 0.48 versus 0.17. Short-term TIPS funds can also fill gaps in a bond ladder. And their shorter duration protects investors’ capital in the event of real rate increases. For example, TIP (duration 6.77) declined 12.2% YTD versus VTIP (duration 2.5) down only 2.9%.

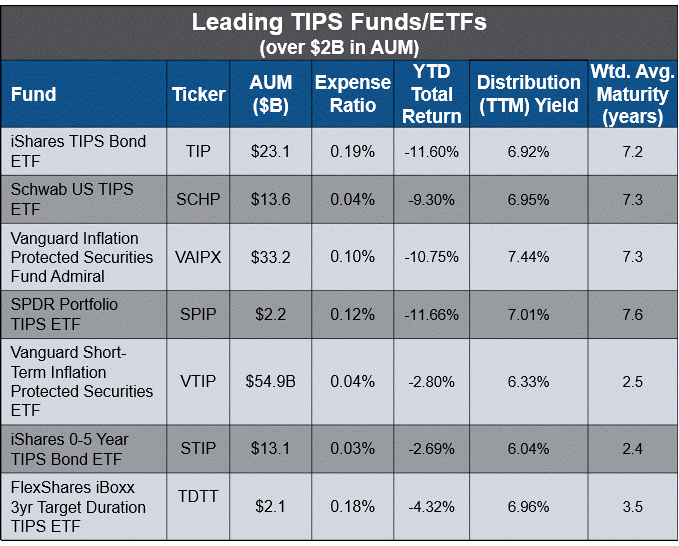

Suffice it to say, each investor is different and should carefully consider their own situation, goals and needs. The table below shows sample TIPS funds to consider.

Blackrock, Vanguard, State Street, Flexshares, Schwab, Morningstar

{kind=link}

I believe the most important factors in selecting a TIPS fund are low expenses, high liquidity (which correlates with AUM – bigger is better), and weighted average maturity. Yield is certainly important, but will tend to be competitive across funds and will primarily be a function of expenses.

Entry Points and Timing

I discussed my views on inflation and the Fed in my last article so won’t repeat those here. First, a disclaimer: those who follow me know I am skeptical of anyone being able to time markets – or rates - consistently . Investors who attempt that do so at their own peril. Having said that, there is evidence of the effectiveness of Elliott Wave analysis. One analyst that I follow has a primary Elliott Wave count for the 10-year Treasury bond rate bottoming in a wave 4 pattern, expecting a wave 5 reversal that may carry rates above their recent peak.

Treasury debt presents another interesting dynamic that could weigh on Treasury and TIPS rates. Last week prescient analyst Felix Zuluaf said that due to debt ceiling limitations, the Treasury Department is $300B behind on debt issuance to fund operations. Congress has approved, and Biden is expected to pass a $1.7 trillion spending package soon. This will add more financing demands. The debt ceiling issue remains unresolved but may be settled early next year. Once that happens, a massive Treasury supply dump could put upward pressure on rates.

{kind=link}

Yet, one should not look a gift horse in the mouth, with real rates close to a 14-year peak. Rates have already risen dramatically this year and could be ready to reverse. Even if Elliott Wave or debt supply dynamics prove correct, real rates could behave differently. I am in process of completing the construction of my TIPS ladder. I’ve been a buyer since real rates approached 1% and am looking near-term for slightly higher real rates before buying more. I will continue to dollar-cost average in with TIPS rates over 1.5%, while I would be enthusiastically all-in at 2%.

Conclusion

A TIPS ladder is an effective way to invest, especially for those in or near retirement who are comfortable creating their own do-it-yourself annuity. The ladder is currently generating one of the highest yields in the past 14 years with higher certainty of returns, and better principal protection than a mutual fund or ETF. TIPS funds and ETFs also provide a good vehicle for many investors. I am a buyer at these yields and am looking for a slightly higher yield in the near-future.

I wish all of you a happy and healthy holiday season and all the best for a prosperous 2023. Thanks for reading my articles! I look forward to sharing more ideas in 2023.

I look forward to your comments.

For further details see:

TIPS Funds Vs. A Ladder