STIP - TIPS: Why Inflation-Adjusted Treasuries Finally Look Attractive

2023-04-11 12:43:15 ET

Summary

- TIPS have struggled over the past year despite a high level of inflation.

- The chief cause of underperformance - a rise in real yields - is now a tailwind for the bonds and why we find them attractive.

- With current and trailing-twelve month yields of 5-7% and potential upside if inflation remains stickier than expected make the bonds appealing.

This article was first released to Systematic Income subscribers and free trials on Apr. 4.

Persistently high inflation has been one of the key market themes this year and last. It's not a surprise that many investors have turned to Treasury Inflation-Protected Securities or TIPS. However, as with any other traded asset, the entry point matters a great deal. Investors who bought TIPS as soon as inflation started rising quickly this cycle are likely sitting on sizable losses. In this article we take a fresh look at TIPS and discuss why they are now much more attractive assets than they were last year, despite some disinflation.

Within the broader TIPS investment universe we like shorter-dated bonds held via passive ETFs such as the iShares 0-5 Year TIPS Bond ETF ( STIP ) or the Vanguard Short-Term Inflation-Protected Securities ETF ( VTIP ), particularly for more risk-averse or defensive investors. Shorter-dated TIPS are trading at real yields of 1.1-1.5% which, on top of the latest relevant CPI index, gets us to forward yields of around 5-6%. Yes, CPI is more likely to fall over the next year or so but as we discuss below it's not falling very quickly and such a high rate is a nice place to start off. TIPS yields also compare favorably to 3-month Treasury Bill yields of sub-5% and brokered CD's that max out around 5%.

Why TIPS Look Attractive Now

There are many types of securities that are claimed as inflation-proof or as being inflation hedges, anything ranging from cash to loans to REITs and more. Many of these claims are exaggerated or incomplete. In this article we take a look at funds that allocate entirely or mostly to US government inflation-linked bonds. Much of the discussion revolves around Treasury Inflation-Protected Securities or TIPS but we also touch on the Series I Savings Bonds or, more plainly, I Bonds.

Many investors already know the mantra that TIPS can offer an inflation hedge. After all, "inflation" is in the name of the product. However many were disappointed by poor performance of TIPS over 2020 when they delivered a return of around -12% (better but still negative for short-dated TIPS) despite inflation rising more than 6% over the year.

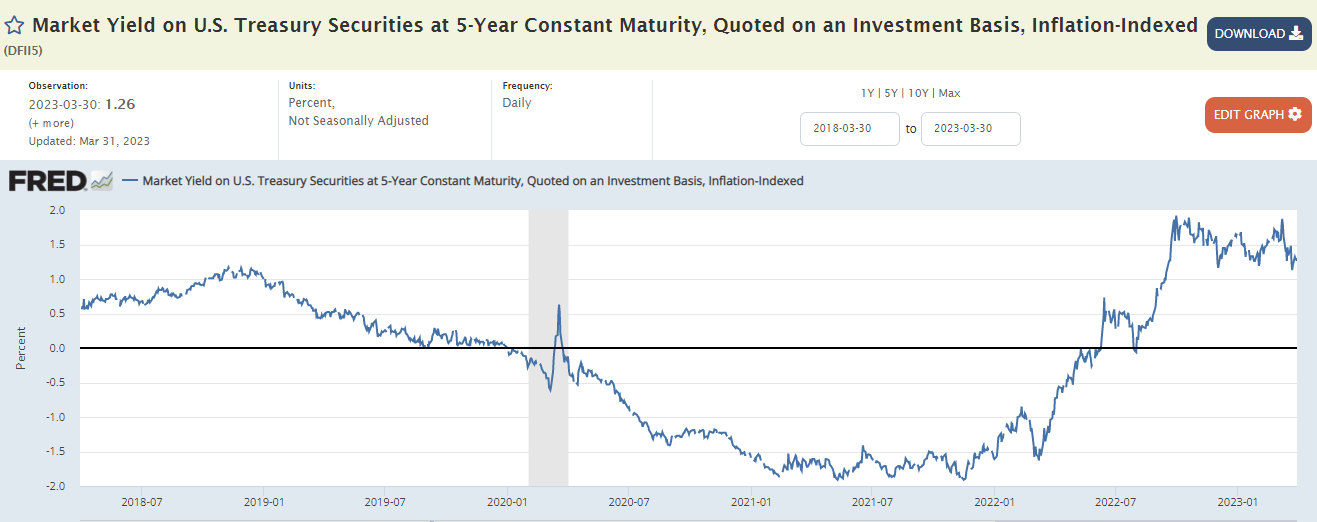

There are two important nuances for allocating to TIPS. One is the difference between income and return. Investors are indeed compensated for a rise in inflation through inflation adjustments to the principal of the bond. The return of TIPS, however, can be all over the place, much like all other traded securities. Specifically, real yields rose sharply over 2022, primarily because nominal yields rose and this caused TIPS prices to drop. Since TIPS are bonds, they are sensitive to prevailing yields. As we can see in the chart below, 5Y real yields moved from almost -1.5% at the end of 2021 to 1.7% by the end of 2022.

{kind=link}

FRED

This has two important implications for investors. One, it puts TIPS on a firmer footing as we are less likely to see a further 3% rise in real yields. This margin of safety should support TIPS prices and, possibly, lead to future capital gains. Second, it is an add-on for TIPS income. An easy way to think about TIPS yields in nominal terms is to add today's real yield to the inflation we are likely to see over a given period. Whether that inflation is 6% or 2%, the real yields of 1.1% to 1.5% (real yields have their own yield curve) top up whatever inflation we will see as an eventual return. This is a more attractive proposition than having 1.5% subtracted from the inflation return which is what we saw at the end of 2021.

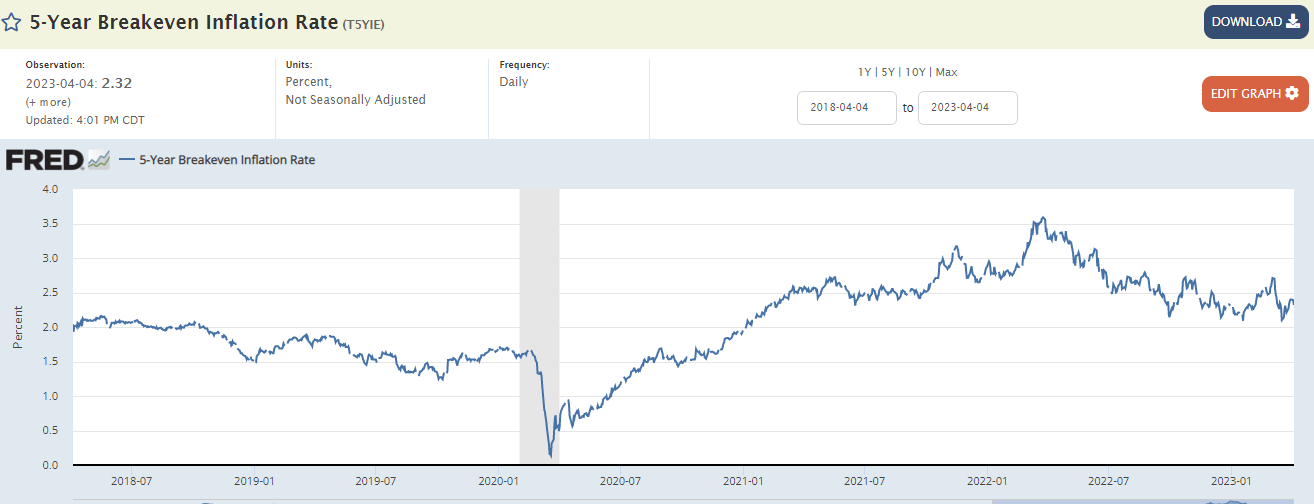

The other attractive feature of TIPS at the present moment is that breakevens are relatively low in absolute terms and have moved significantly lower in the past year as we can see below. The market thinks that inflation will be around 2.3% over the next five years. Current inflation readings have been well above that level. This sharp drop in inflation is certainly not impossible but it does offer an attractive entry point in our view in case inflation proves stickier than the market believes.

{kind=link}

FRED

Investment Options

Investors considering TIPS have a basic decision to make which is whether to allocate to individual bonds or to funds. The right choice for most investors is to go with funds, in our view. This has to do with greater ease of execution and tax reporting as well as the issue of phantom income.

Investors who hold individual TIPS don't receive the compensation for inflation adjustment until redemption or maturity but do have to pay taxes on it. Investors who hold TIPS funds will receive inflation adjustments in the form of actual dividends.

This is great because it allows investors to enjoy a higher level of income than they would otherwise. The reality is that TIPS pay out the lowest amount of cash to investors out of any asset outside of zero-coupon bonds (which are fairly common in the Muni sector).

For example, the largest, and fairly typical, TIPS fund iShares TIPS Bond ETF ( TIP ) has a weighted-average coupon of 0.61% which is roughly what it actually receives in cash and what it would have to pay out as its distribution rate if it couldn't treat the inflation adjustment as income.

However, since the majority of a TIPS return comes in the form of the inflation adjustment, it's a good thing investors can enjoy it without having to wait for the bonds to mature. It also provides an offset to the tax investors have to pay on the inflation adjustment which could otherwise make standalone TIPS bonds a negative income asset (until maturity).

Before looking at TIPS funds, investors should also be aware of I Bonds which are a different type of inflation-adjusted bond offered by the Treasury. This is a good primer on I Bonds for investors who have not heard of them.

I Bonds are unusual in that they can only be bought directly from the Treasury. The maximum investment is also limited to just $10k per person per calendar year (with an additional $5k in place of a federal tax refund).

I Bonds have a number of attractive features. One, earnings are free of state income taxes while federal taxes can be deferred until redemption or maturity. This is in contrast to TIPS which are free of state income taxes but are liable for federal taxes on phantom income. I Bonds are also not market instruments and so don't change in price, something which can provide a nice ballast to the portfolio, particularly in light of poor TIPS returns last year.

A technical point is that the I Bond "fixed rate", which is the add-on you get on top of the inflation adjustment and is akin to the real yield of TIPS, is quite low currently at 0.4%. This does not compare well with TIPS real yields which are all north of 1% across the yield curve. That said, the decision of buying now or waiting till May is not totally straightforward as inflation may continue to fall. This means that the all-in rate of May I Bonds may be lower despite a higher fixed rate. Over the longer term, however, the impact of a single inflation adjustment will be small so waiting till May to buy I Bonds is more worthwhile in our view.

Moving on to TIPS, the choices for investors are 1) passive ETFs, 2) active mutual funds, 3) leveraged CEFs e.g. WIA, WIW, 4) TIPS + derivatives actively managed ETF IVOL.

Taking a look across over 20 TIPS funds in our Funds Tool, the key factors for performance seem to be fee and low duration. The impact of the fee is obvious - the lower the fee the higher the return, all else equal. This also suggests that active management does not appear sufficient to overcome the impact of the fee. This is possible because an additional 0.5-1% in fees for actively managed funds is simply too high for the alpha that is available in the TIPS space.

The duration impact is also clear - because real yields have risen sharply, longer duration funds were hurt. This does not necessarily mean that investors should avoid longer-duration funds. It is simply an outcome of the recent rise in interest rates. Where investors choose to position on the duration spectrum is a function of their view on interest rates and their risk appetite.

There are arguments for allocating to both shorter-maturity and longer-maturity TIPS. Investors who are concerned that inflation may continue to move higher while the economy continues to grow may want to tilt to shorter-duration TIPS as real yields could reaccelerate higher. On the other hand, investors who are worried that we might have a stagflationary environment of a recession combined with inflation that is moving lower fairly slowly may want to tilt to longer-duration TIPS.

What is clear is that CEFs do not look like attractive options in the suite. A look at the 5-year total NAV performance shows that the two CEFs (blue bars) that allocate primarily to TIPS have significantly underperformed the sector.

{kind=link}

Systematic Income

What is also clear is that the actively-managed Quadratic Interest Rate Volatility and Inflation Hedge ETF ( IVOL ) which we panned in 2020 underperformed the space as well.

{kind=link}

Systematic Income

Although we see value in allocating to both shorter-duration and longer-duration TIPS, we decided to stick with a cheap modest-duration option - the iShares 0-5 Year TIPS Bond ETF ( STIP ) with a duration of 2.4 (about a third of the benchmark TIPS ETF TIP) in part because the allocation was made in our Defensive Income Portfolio which aims to keep portfolio volatility on the lower side. Shorter-dated TIPS also have a higher level of real yields - for example, STIP has a weighted-average real yield of 1.8% vs. 1.4% for its longer-duration counterpart TIP.

For further details see:

TIPS: Why Inflation-Adjusted Treasuries Finally Look Attractive