ASTLW - Tis The Summer For Taking Profits

2023-07-19 02:19:59 ET

Summary

- The latest CPI numbers, moderate energy prices, low unemployment, and real wage gains could stimulate a stock market rally this summer.

- Despite the potential for a summer rally, counter-factors may slow and eventually halt the market, leading to a potential decline in early fall.

- I plan to take advantage of the higher market to make some profits, despite already having a significant cash position in the investment portfolio.

Investment thesis: The latest CPI numbers coupled with several other factors, including moderate energy prices, low unemployment, and continued gains in real wages as well as other factors are arguably adding up to a potentially potent stimulant for a stock market rally this summer. My view is that while the odds of a robust stock market rally are high this summer, perhaps extending into early fall, it will not last beyond that. Several counter-factors are likely to slow it down, then grind it to a halt, followed by a potentially spectacular stock market decline. Therefore, I intend to take advantage of a potential market rally to take some profits, despite my current cash position being already significant as a proportion of my overall investment portfolio.

The stock market is up in the last few sessions and it is likely to trend higher for the rest of the summer.

The DOW Jones Index reached its one-month low on July 10th going down to 33,600 points. It is up since then to over 34,900 as I write this. The S&P is up about 130 points for the same period, while the Nasdaq is up about 600 points. A lower-than-expected CPI number helped with this outcome and it is likely to continue being a catalyst for the market for the rest of the summer.

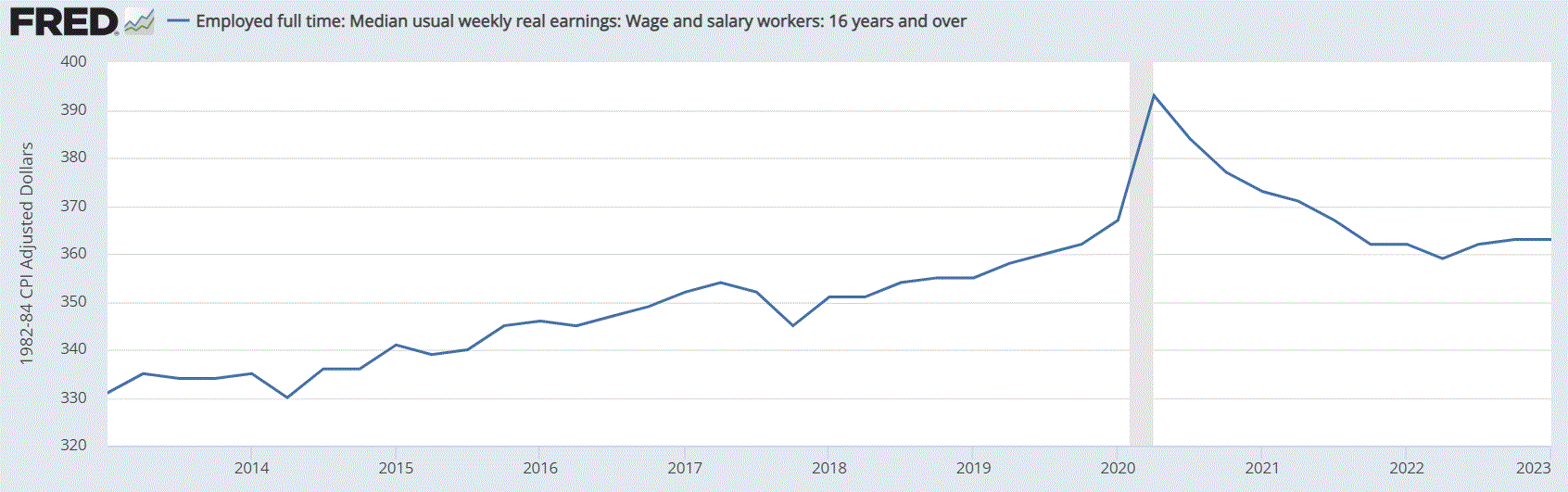

Other factors are also helping in creating a somewhat positive mood regarding the overall economy this summer. Low energy prices are providing some relief for consumers and helping businesses keep costs low. Real wage growth is also trending positive, with the latest numbers showing that after adjusting for inflation they were up .2% in June compared with May. What this means in real life, based on available data is that for the first time since the beginning of the decade, at least half the workers in the US feel that they are starting to take home slightly more in real earnings.

{kind=link}

Federal Reserve Bank of St. Louis

In line with the real income growth that we are seeing, real consumer spending growth adjusted for inflation is also advancing so far this year. This should be enough to potentially improve the mood of the market over the rest of the summer. Some decent earnings, combined with some more positive macro data points, if they materialize going into the current earnings season, make for a potentially robust stock market rally.

Fall is likely to see a gathering of economic storm clouds on the horizon, which will likely put an end to any further stock market gains for the year.

If the rest of the summer will go the way I expect it to, in other words, positive macro-metrics will boost overall confidence in the stock market, it will arguably set the stage for a severe energy price spike in the fall.

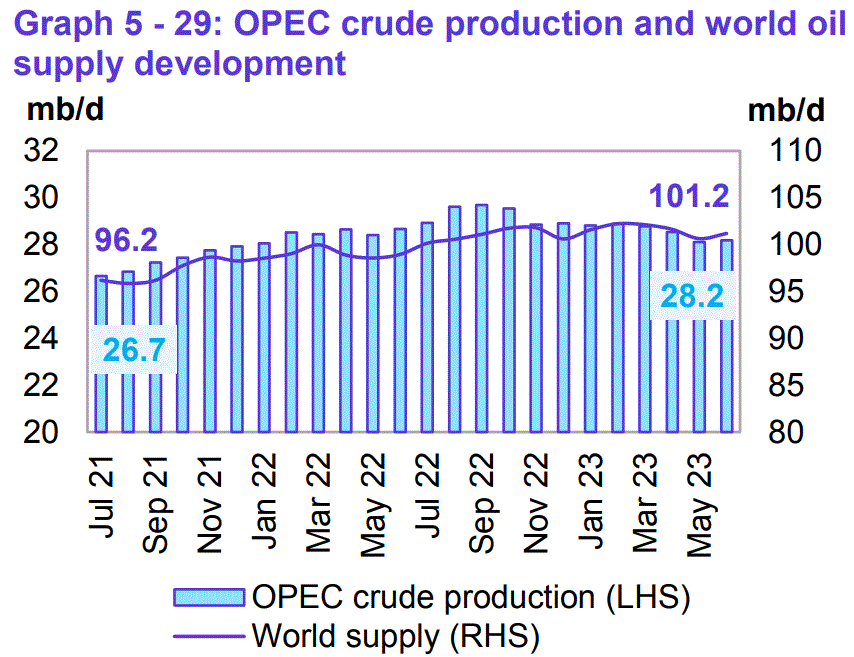

The latest OPEC monthly report still expects to see an increase in global liquid fuels production to 103.3 mb/d in the last quarter of this year.

{kind=link}

OPEC

As we can see, as of June, total global liquid fuels production averaged 101.2 mb/d, which means that between now and October we have to close a 2 mb/d gap to balance the market. In the meantime, the Saudis have cut production by 1 mb/d, while Russian production also seems to be declining. If those production cuts will persist in the fall and beyond, it is hard to see how the world can close that gap, which is more like 3.5 mb/d if the Saudi-Russian cuts will persist. On the demand side, if the economy holds up through the summer, it will also probably have some positive momentum going into fall & winter. If this is the case, inevitably we will have to see a demand destruction event happen at some point in the next six to twelve months, with oil and perhaps natural gas and other commodities and energy prices starting to rise within a few months.

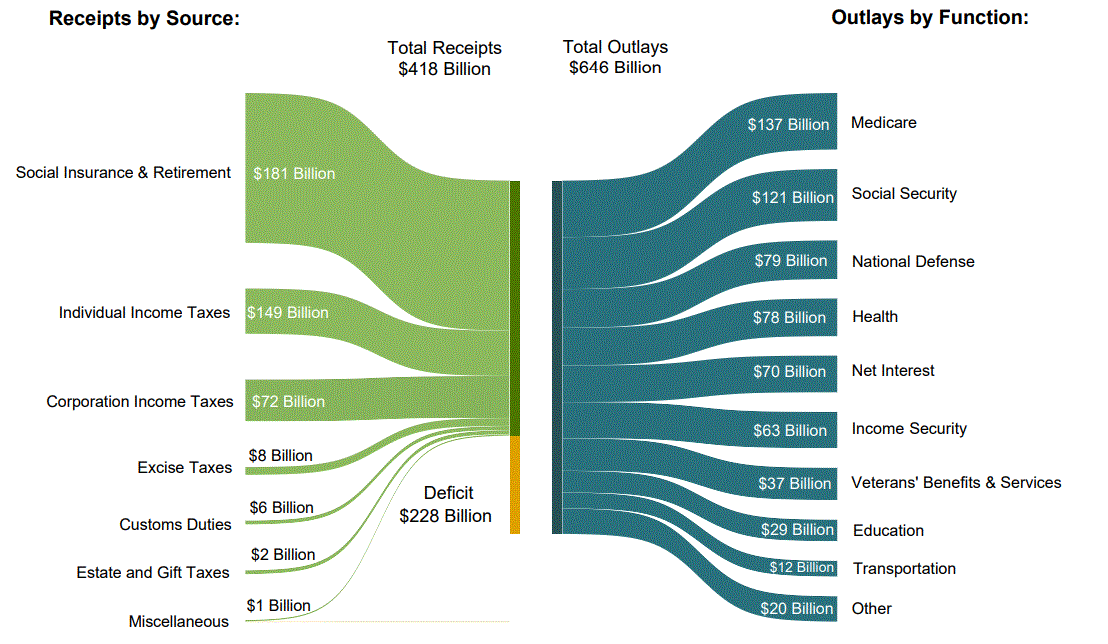

Several other factors may also exacerbate a global economic slowdown within the next year or so. It was recently reported that the US deficit as a percentage of GDP will be higher this year than last year, based on estimates such as the one made by the CBO. Going beyond the current fiscal year, it seems to be running out of control, with deficits constantly rising from 5.8% currently, to averaging over 8% two decades from now and 10% three decades from now. The Monthly Treasury Statement shows a wide deficit for June, of $228 billion.

{kind=link}

Monthly Treasury Statement

It is uncertain whether the widening shortfall is just a fluke or whether it is part of a sustained increase in deficit spending, but we should keep in mind that just two decades ago, the deficit we saw last month in nominal dollar terms was often seen as alarmingly high if such numbers were recorded for the full fiscal year. If this turns out to be a more fundamental problem, rather than just a fluke, a legislative reaction in the form of spending cuts or other measures may be needed to get ahead of the fiscal situation spiraling out of control. It is yet another situation that needs to be closely watched in my view.

Several other domestic as well as international factors may play a role in a worsening investment environment starting as soon as this fall. For instance, the economic confrontation with China seems to be intensifying. If this degeneration in relations will continue, it has the potential to greatly impact the world's supply chains, to the point where we could see severe economic damage, as well as operational damage inflicted on individual companies. Domestically, several companies seem to be caught in the middle of an emerging culture war that increasingly targets corporate entities that fail to align with one view or another, putting them in a no-win situation. The list of arguably worsening problems seems to be growing in length as well as in severity. This summer we seem to be in a period of relative calm, but that can easily change.

Investment implications:

If my thesis is correct and we will see decent upward momentum within the stock market this summer, followed by stagnation or even a reversal later in the year, then taking some profits might be a good idea. I am personally looking at selling some shares, mostly focused on my non-energy sector and non-precious metals positions.

Some examples where a complete exit from a position or at least a partial exit may be warranted, include my recent decision to sell my Greenbrier ( GBX ) stock. It had a significant stock price rally on the back of a decent Q1 report . I doubt that the outlook will improve much for GBX going forward if there is further pressure on the global economy from factors such as higher energy costs and so on. If anything, an opportunity to get back into this stock might emerge perhaps next year.

AMD ( AMD ) is a stock I am looking to reduce my position in, perhaps if we see a 10% to 20% rise in its current stock price. For a short review of my recent position in this stock, I first bought at $110/share, as it retreated from its all-time high of almost $170/share. I then bought some more at under $90/share and finally at under $70/share. I sold all my shares recently, except for the shares that I bought at under $70. If I do see a further increase in its share price, I will probably further reduce my position, but at this point, I intend to maintain a small position in the hope that AMD will reach new all-time highs within the next year or two.

I should note that there are some potential downside risks, aside from a slowing global economy. One of the risks that AMD faces is the prospect of a China surprise, where its efforts to domestically produce semiconductors without much Western input, due to the pressures we are putting on China's tech industry, might lead to a leap in Chinese capabilities in this regard. At that point, tech companies around the world might opt to hedge their options for semiconductor suppliers, by reducing exposure to Western companies, which they will see as always being at risk of being used as leverage or as a geopolitical pressure point. Such is the risk of weaponizing our current tech advantage.

Intel ( INTC ) is another stock position I am looking at reducing. I am currently modestly up on my position and at this point, I'd be satisfied with another 10% or so in terms of returns per share. Nokia ( NOK ) is a stock position I would like to completely exit from, as I pointed out in a recent article . I would like to ideally break even, but I am currently down about 18% on my position and at this point, a significant reduction in that potential loss will suffice. My Ford ( F ) stock position will probably be reduced if it sees a significant bump in its stock price from current levels. I am also looking to reduce or eliminate my positions in US Steel ( X ), Vale ( VALE ), Algoma Steel ( ASTL ), and Albemarle ( ALB ). These stocks should see a bump in their price if the market perception of the state of the US & global economies will improve, while an impending downturn will likely weigh heavily on these volatile mining & refining stocks.

I am keeping my positions in energy stocks, as well as precious metals miners. The latter I see as increasingly crucial in having in one's portfolio, given the increasingly unstable global geopolitical as well as economic situation, as I perceive it. In other words, I am not overly concerned with what gold & silver will do in the next few months. I want to keep constant exposure to physical as well as stock assets in case things go wrong with the global fiat system.

With my overall stock investment portfolio already leaning heavily toward my cash position, sitting at around 1/3 of my portfolio, I certainly do not want to cut too heavily into my existing stock exposure. If I happen to be very wrong and we will see continued upside momentum in the stock market beyond the summer, I will get caught out sitting on excessive cash, with few good opportunities to invest in advantageous positions. I'd have to wait until the next significant downturn before I can significantly reduce my cash position and be gainfully invested. While I do not intend to cut into my stock positions too deeply, if opportunities will rise this summer or early fall to take profits, I will do so, then wait for the next downturn to reinvest, reducing my already sizable cash position.

For further details see:

Tis The Summer For Taking Profits