TWI - Titan International: Additional Upside Is On The Table

2023-09-12 05:57:04 ET

Summary

- Titan International's fundamental performance has weakened, but its shares have continued to outperform the broader market.

- The company's cheap valuation and potential for future growth make it an attractive investment.

- Despite a drop in revenue and profitability, management remains optimistic about the long-term prospects of the company.

When it comes to investing, strong fundamental performance is often viewed as being correlated with shares rising. Normally, this is the case. But it's not always the case. The beautiful thing about value investing is that you don't always need the fundamental picture for the company that you buy into to come in strong in order for shareholders to benefit. One really good example I could point to, where fundamental performance has weakened as of late but where shares have continued to outperform the broader market, would be Titan International ( TWI ). For those who don't know, Titan International operates as a producer and seller of wheel, tire, and undercarriage industrial equipment, as well as other offerings. Sales, profits, and cash flows have all weakened year over year and, on a forward basis, the stock has gotten more expensive. But with shares of the company looking cheap, both on an absolute basis and relative to similar firms, the market has rewarded shareholders handsomely. And, quite frankly, I don't see why investors shouldn't expect this trend to continue for some time.

When cheap trumps performance

When I last wrote a bullish article on Titan International back in early June of this year, I found myself impressed with continued improvements on the company's bottom line. Because of broader economic conditions, management opted not to provide guidance for the entirety of the 2023 fiscal year. Normally, that would be a red flag for me. But because of how cheap shares were, both on an absolute basis and relative to similar firms, I ended up keeping the company rated a soft 'buy' to reflect my view at the time that shares would be likely to outperform the broader market for the foreseeable future. Since then, one additional quarter worth of data has come out and, in response, shares have spiked. As of this writing, they are up 11.1% since I last wrote about the company. That dwarfs the 4.4% increase seen by the S&P 500 over the same window of time.

It is worth noting that I have not always been bullish on Titan International. In fact, when I first wrote about the company in May 2022, I ended up assigning it a 'sell' rating. This was based on inflationary pressures at the time, the role that said inflation played in the company's revenue growth, and other factors. From that date through today, the stock is actually down 33.7% at a time when the S&P 500 has jumped 8.4%. It was only after the substantial drop in share price that my attitude gradually changed.

{kind=link}

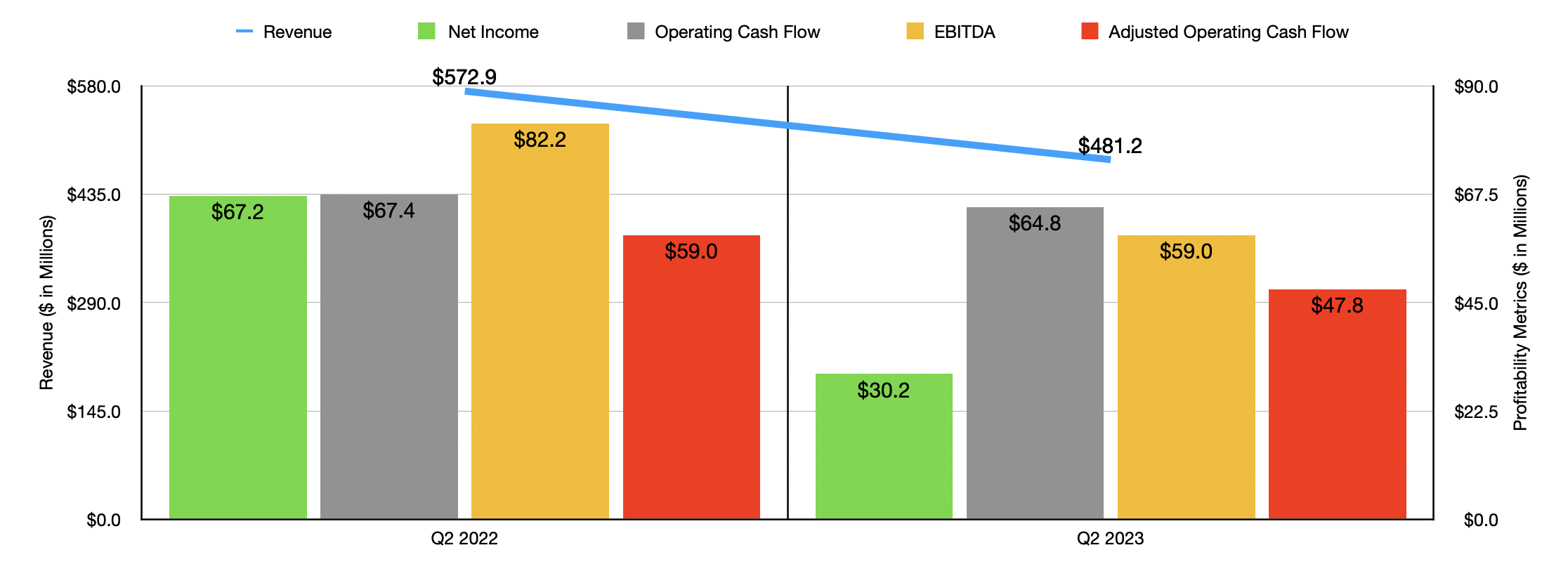

Fast-forward to today, and we do have an interesting picture to ponder. During the second quarter of the 2023 fiscal year , the most recent quarter for which new data is available, Titan International generated revenue of $481.2 million. That is 16% lower than the $572.9 million in sales generated the same time last year. According to management, this drop in sales was caused by lower sales volumes across all of the companies operating segments as customers that IT services deal with elevated inventory levels. This is especially true of OEM customers throughout the Americas. And it's worth noting that the decline in revenue came even as prices that the company charges for its products dropped as well.

Management has been very open about what they believe of current market conditions. In the near term, elevated inventory levels are likely to continue impacting sales negatively. But the longer-term picture looks positive. For instance, in the agricultural market, management said that commodity prices have remained high enough to make sure that farmer income is at or near historically high levels. In addition to this, there is a real need to replace aging large equipment that comprises a good portion of the agricultural market's fleet. When it comes to the earth moving and construction market, the picture is far more complicated. There has been a slowdown in demand associated with OEMs, most notably throughout the Americas. And as was the case with the agricultural market, elevated inventory levels have proven to be a key driver of this pain. In the long run, however, management believes that high mineral commodity prices will drive growth.

It should not be surprising to see a drop in revenue result in a drop in profitability as well. After all, this is an asset-intensive industry and even a small decline in sales can lead to a lot of pain when it comes to margins. Net income in the most recent quarter, for instance, came in at $30.2 million. That's less than half the $67.2 million in revenue generated one year earlier. Other profitability metrics held up better. Operating cash flow declined from $67.4 million last year to $64.8 million this year. If we adjust for changes in working capital, we get a decline from $59 million to $47.8 million. Meanwhile, EBITDA for the business shrank from $82.2 million to $59 million.

{kind=link}

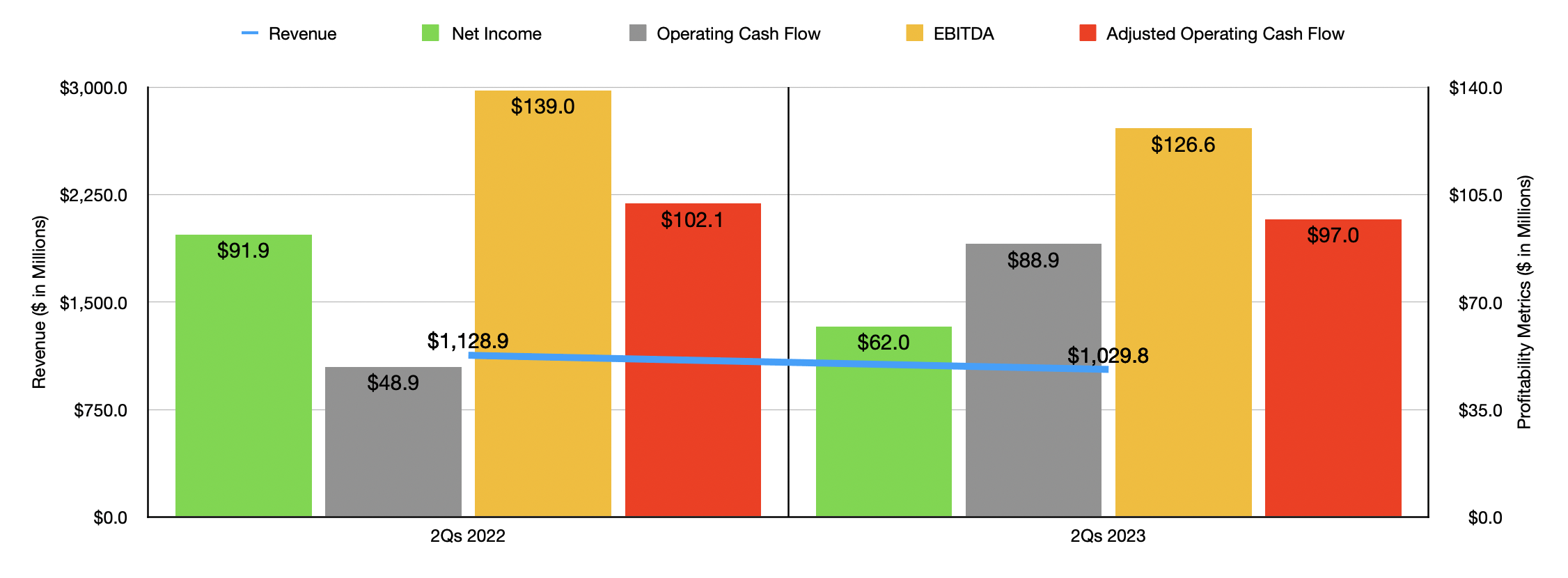

To provide proper context, I also, in the chart above, provided results for the first half of this year relative to the same time last year. As you can probably tell, most of the pain that the company has faced so far this year has been because of poor results in the second quarter. The good news, however, is that management still remains optimistic. For 2023 and its entirety, they are forecasting revenue of between $1.85 billion and $1.90 billion. That would represent a decline from the $2.17 billion the company generated in 2022. Although this is disappointing, profits and cash flows are likely to remain at respectable levels. For instance, EBITDA has been forecasted to be between $200 million and $210 million. Operating cash flow should be somewhere between $165 million and $180 million, while net profits should be around $118.9 million based on my own estimates.

{kind=link}

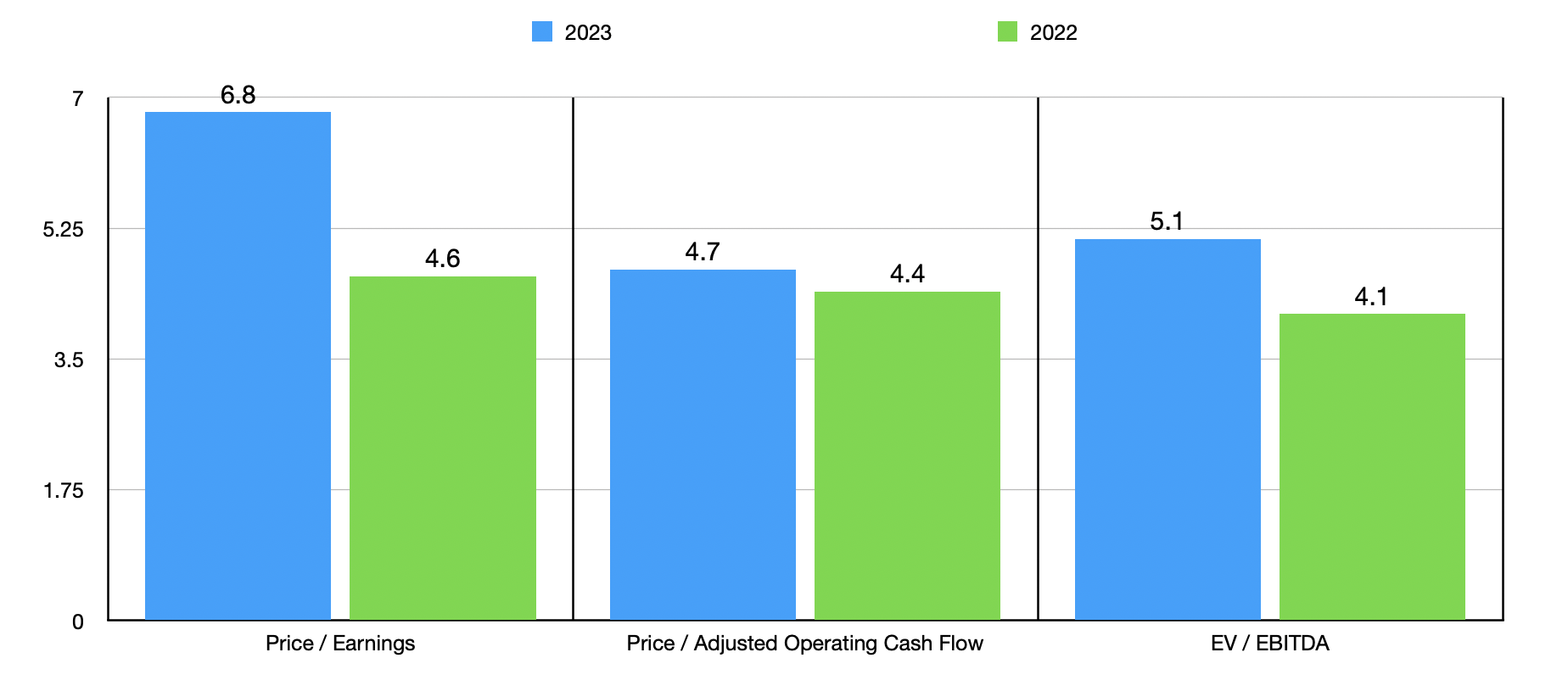

With these figures, I created the chart above. In it, you can see how shares are priced using the forward estimates for 2023. You can also see how they are priced relative to the data provided for 2022. Even though the stock does look more expensive on a forward basis, these multiples are still low enough, in my view, to make the company fundamentally attractive on an absolute basis. But what makes the picture even better is that shares are still cheap relative to similar enterprises. In the table below, you can see how, even using the more conservative 2023 estimates, Titan International is the cheapest of its peers using any of the three valuation metrics that the table illustrates.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Titan International |

| 6.8 |

| 4.7 |

| 5.1 |

| Lindsay Corp. ( LNN ) |

| 19.7 |

| 16.1 |

| 11.2 |

| AGCO Corp. ( AGCO ) |

| 8.9 |

| 9.6 |

| 7.0 |

| CNH Industrial ( CNHI ) |

| 8.1 |

| 21.5 |

| 9.0 |

| The Toro Co. ( TTC ) |

| 21.1 |

| 34.6 |

| 14.5 |

| Deere & Co. ( DE ) |

| 12.4 |

| 17.4 |

| 10.4 |

Takeaway

Investing can be complicated. When the fundamental performance of a firm starts to deteriorate, it can be tempting to run. But this is not always the proper decision to make. If a company is cheap enough and if the deterioration is not overwhelmingly bad, some nice upside can be captured. Don't get me wrong. Investors should continue to monitor this situation very closely. However, I would make the case that some additional upside likely exists. Because of this, I have decided to keep the company rated a soft 'buy' at this time.

For further details see:

Titan International: Additional Upside Is On The Table