TWI - Titan International: Shares Have Gotten Cheap Enough At Last

2023-06-11 08:09:29 ET

Summary

- Titan International, a producer and seller of wheel, tire, and undercarriage industrial equipment, has become an attractive investment opportunity due to improved financial performance and a decline in the company's share price.

- The company's bottom line performance has continued to improve, with net income expanding from $23.9 million to $31.8 million, and operating cash flow going from negative $18.5 million to positive $24.1 million.

- Despite a lack of estimates for the year, if current results are annualized, Titan International's shares appear to be cheap, with a forward price to earnings multiple of only 3, making it a soft 'buy' for investors.

One of the great things about investing is that a company that did not make sense to invest in previously can become an attractive opportunity. This can be because of improved financial performance, a decline in the company's share price, some combination of these two, or something else entirely like a catalyst. One firm that I have recently become a bit bullish on happens to be Titan International ( TWI ), a producer and seller of wheel, tire, and undercarriage industrial equipment for companies in the agricultural space, mining, the military, and more. Last year, I was actually very bearish about the firm. By December, I had become neutral. But since then, shares of the company have declined while bottom line performance has only continued to improve. Add on top of this how cheap shares are at this moment, and I believe that the company now makes for a reasonable prospect for investors to consider at this time.

Shares are cheap enough at last

The last article that I published about Titan International came out in early December of last year. In that article, I talked about how shares of the company had taken a beating, dropping 21.8% compared to the 1.9% decline seen by the S&P 500. That drop, combined with continued attractive performance, led me to change the company from a ‘sell’ prospect to a ‘hold’. This kind of rating indicates a scenario where I think that shares should generate returns that would more or less match the broader market for the foreseeable future. But unfortunately, things have not been quite that simple. Since the publication of that article, shares have dropped 22.4% at a time when the S&P 500 has spiked 8.8%.

Given this massive return disparity, you could be forgiven for thinking that the fundamental condition of the company was worsening at a rapid pace. But the fact of the matter is that things are going quite well. Not everything is perfect, mind you. For instance, during the first quarter of the 2023 fiscal year, management reported revenue of $548.6 million. That's 1.3% lower than the $556 million the business reported one year earlier. This drop, according to management, was the result of weakness across all of the company's operating segments. But when you dig deeper, you realize that the picture is not quite that bad. For instance, the company was hit to the tune of 1.5% by foreign currency fluctuations. The company also saw a 1.8% hit associated with the sale of its Australian wheel business that occurred in the first quarter of last year. These were largely offset by higher product pricing and higher shipping volume. In fact, had it not been for these one-time items, sales would have actually increased 2% year over year.

Despite the tumult on the top line, the company's bottom line actually improved. Net income, for instance, expanded from $23.9 million to $31.8 million. Part of this was because of a rise in the company's gross profit margin from 15.6% to 17.4%. This, according to management, was mostly because of productivity initiatives centered around the company’s production facilities, as well as cost-cutting initiatives and lower input costs such as freight. Selling, general, and administrative costs, also improved, dropping from 6.5% of sales to 6.3%. This was related to the aforementioned asset sale in Australia.

{kind=link}

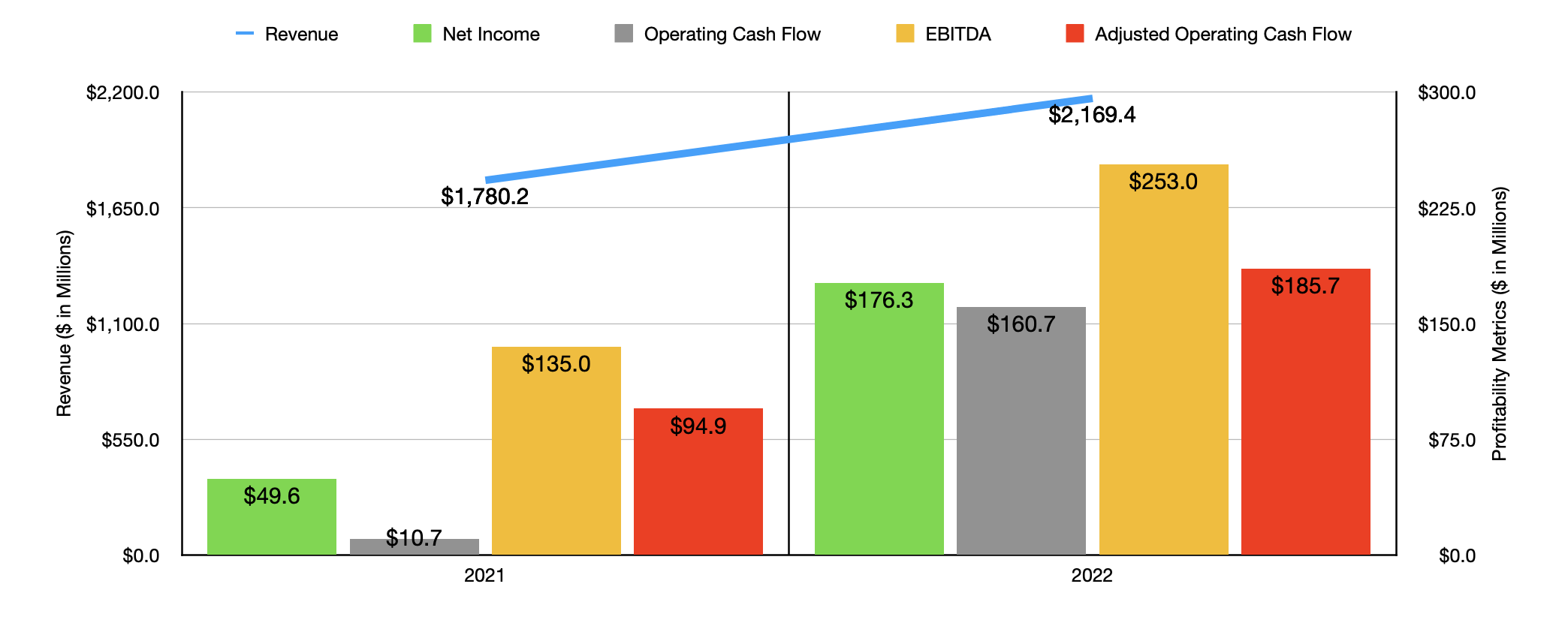

As you can imagine, other profitability metrics for the company also improved during this time. Operating cash flow went from negative $18.5 million to positive $24.1 million. If we adjust for changes in working capital, we would have seen this metric climb from $43.1 million to $49.2 million. Meanwhile, EBITDA for the firm expanded from $56.8 million to $67.6 million. In the chart above, you can see that the first quarter was not a one-off event. Results in 2022 were significantly better than what the company experienced in 2021. In my initial bearish assessment of the firm, I maintained that the strong market conditions that existed at that time were unlikely to persist. But so far, they have done just that. In the company's latest quarterly release, management said that underlying market conditions in the agricultural space imply healthy demand for the firm's products moving forward. The earth moving and construction market is also expected to remain stable throughout this year. But management has been a bit more noncommittal in assessing the consumer market. But with this accounting for only 8% of the company's revenue, even a decline would be unlikely to affect the business materially.

{kind=link}

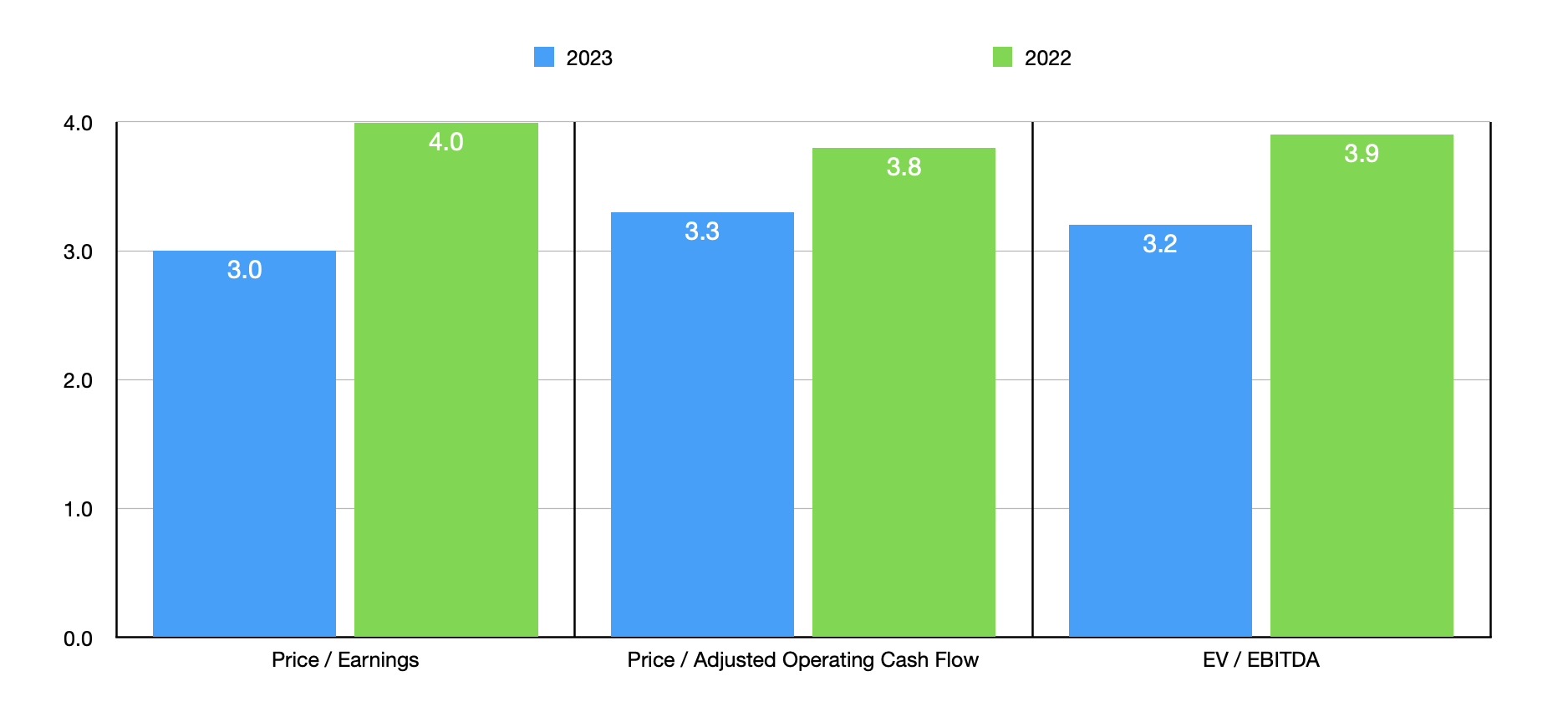

Despite management's thinking regarding market conditions, we don't actually have any estimates for the year. If we simply annualize the results that we've experienced so far, we would expect net income of $234.6 million. Adjusted operating cash flow would be a bit lower at $212 million, while EBITDA would come in at about $301.1 million. If we assume that these numbers turn out to be accurate, then shares of the company look quite cheap at this time. The forward price to earnings multiple of the business is only 3, while the price to adjusted operating cash flow multiple should be 3.3. The EV to EBITDA multiple, meanwhile, should be about 3.2. As you can see in the chart above, even a return to the kind of results experienced in 2022 would indicate that shares look cheap on an absolute basis. As part of my analysis, one thing I did was compare the company to five similar firms. The results can be seen in the table below. In all three cases, Titan International ended up being cheaper than all five of its peers.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Titan International |

| 4.0 |

| 3.8 |

| 3.9 |

| Lindsay Corp ( LNN ) |

| 17.5 |

| 29.8 |

| 10.6 |

| AGCO Corp ( AGCO ) |

| 9.5 |

| 10.7 |

| 6.8 |

| CNH Industrial ( CNHI ) |

| 8.7 |

| 25.4 |

| 9.2 |

| The Toro Co ( TTC ) |

| 21.3 |

| 32.2 |

| 15.7 |

| Deere & Co ( DE ) |

| 12.8 |

| 18.1 |

| 11.0 |

Takeaway

Operationally speaking, Titan International is doing far better than I thought it would be doing at this point. The markets in which it operates have remained strong. Of course, I still maintain that this picture will change at some point. But in all likelihood, the rest of this year will probably be fairly positive for the firm. Even if we assume that conditions deteriorate enough such that the trading multiples of the business double from what they were in 2022, the stock would still look attractively priced on an absolute basis and would still be trading at or near the low end of the scale compared to other prospects. For these reasons, I feel comfortable upgrading the company slightly from a ‘hold’ to a soft ‘buy’.

For further details see:

Titan International: Shares Have Gotten Cheap Enough At Last