TJX - TJX Companies Q3 Earnings: Remaining A Preferred Shopping Destination Ahead Of Holiday Season

2023-11-15 09:39:31 ET

Summary

- The TJX Companies just reported fiscal Q3 results.

- Heading into the release, shares were outperforming other retail peers, with the stock up more than 5% since my most recent coverage.

- Even though the stock continues to trade near the upper end of its 52-week range, I maintain a bullish view and see the momentum continuing through year-end.

- Shares remain viewed as a “buy” following the positive earnings release.

Off-price retailer TJX Companies ( TJX ), has gained more than 5% since my most recent coverage ahead of their Q2 print. At that time, I had called out the HomeGoods unit as a key variable in overall results, a callout that ultimately came to fruition.

With fresh quarterly results in hand, I remain bullish on the outlook for TJX. While investors may have been disappointed in the holiday quarter guidance immediately following the release, I view the post-release volatility in the share price as more of a profit taking and positioning move, following share price outperformance over the past year.

In my view, TJX clearly remains a preferred shopping destination ahead of the holiday season. And looking ahead, I remain confident on TJX’s prospects of reaching $100/share and continue to view the stock as an attractive “buy” for long-term investors.

TJX Key Stock Metrics

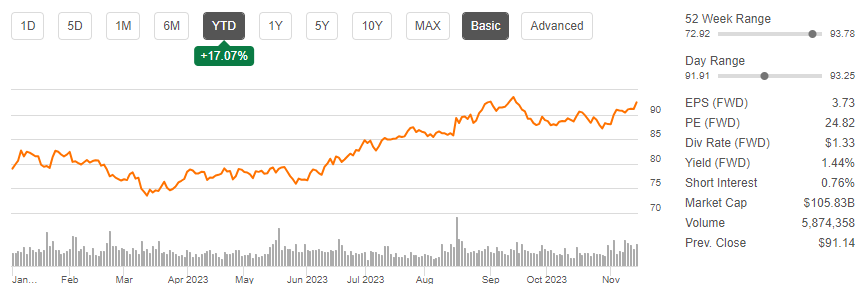

TJX is tracking ahead of the broader S&P ( SPY ) on a year-to-date basis. Shares have gained more than 17% during this period, ahead of the approximately 12.5% gain in the S&P over the same period.

{kind=link}

Seeking Alpha - Basic Trading Data Of TJX

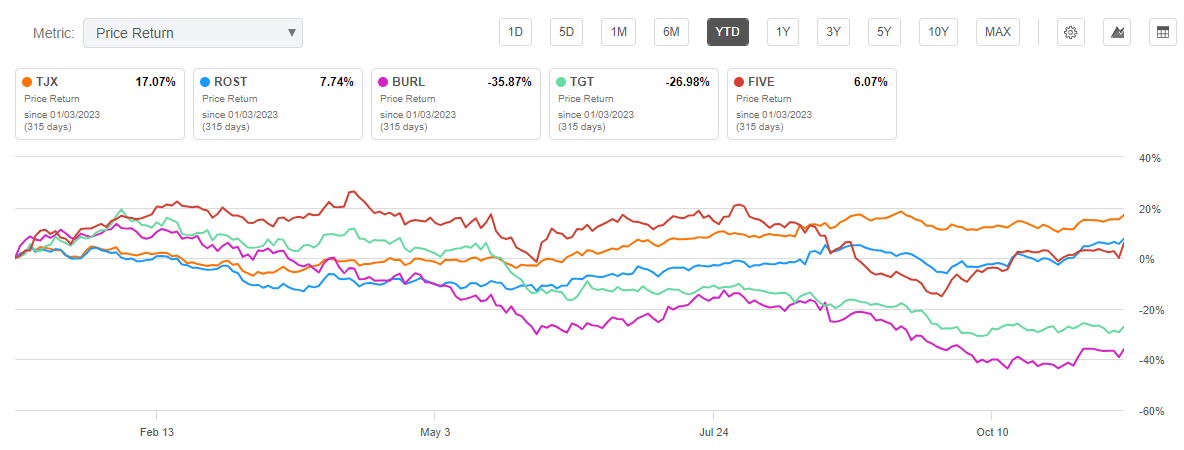

TJX also has outperformed over the last one year, with shares up more than 20% to the broader S&P’s 10.5%. In addition, the stock is outperforming their two other off-price retailers, Ross Stores (ROST) and Burlington Stores ( BURL ), as well as others within the broader retail space.

{kind=link}

Seeking Alpha - YTD Return Of TJX Compared To Peers

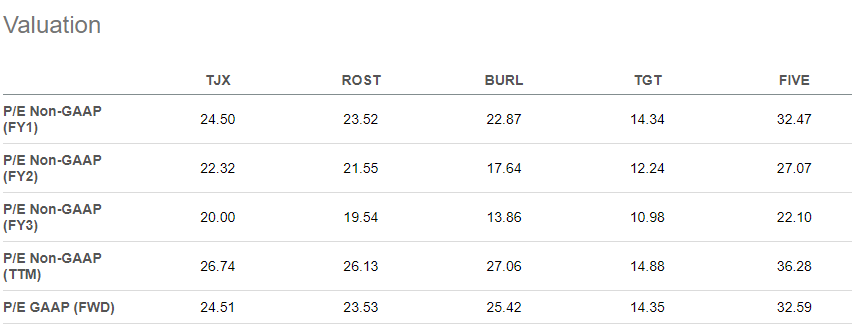

Currently, TJX is trading at the upper end of their 52-week range, with strong momentum during the past month. Based on the midpoint of TJX’s full-year diluted EPS target, shares currently command a forward multiple of about 24.7x, in-line with their off-price retail peers.

{kind=link}

Seeking Alpha - P/E Valuation Metrics Of TJX Compared To Peers

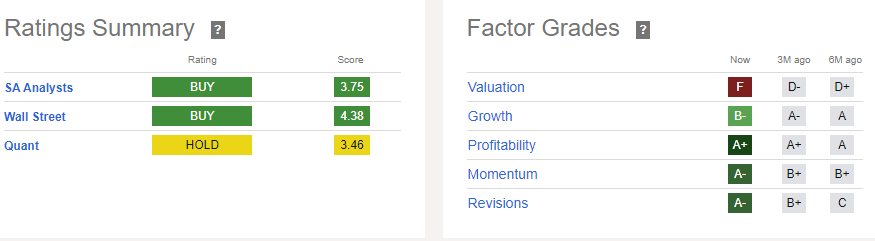

The higher trading multiple is the primary factor why the stock rates as a “hold” by Seeking Alpha’s (“SA”) quant factors. The stock is otherwise viewed bullishly by both the SA analyst community and by Wall Street, who currently see shares as fairly valued just shy of the $100/share mark.

{kind=link}

Seeking Alpha - Ratings Summary Of TJX

I have previously covered TJX several times in the past, all of which have been bullish calls. In my view, I see shares as fairly valued at $100/share and have cited the off-price appeal in the current inflationary environment as a prime supporting factor for my views.

{kind=link}

Seeking Alpha - Author Ratings History Of TJX

What Was TJX Expecting Heading Into The Q3 Earnings Release?

TJX turned in a large beat on their Q2 release , with both total revenues and earnings beating by +$310M and $0.07/share, respectively. The strong performance on the earnings front was consistent with Q1, where they also beat by $0.05/share.

The earnings strength during the first half of the year had been aided in part by the favorable freight environment, which provided a significant tailwind to pre-tax margins. In Q2, for example, pretax margins were up 120 basis points (“bps”) YOY to 10.4%, well above the company’s original expectations.

The impressive first half performance enabled an increase in the full-year outlook for comparable sales, pre-tax margins, and EPS. Heading into Q3, TJX was expecting comparable sales to be up 3.5% at the midpoint.

The midpoint of pre-tax margins also was bumped up to 10.75%, with a favorable assist expected in Q3, where the midpoint was seen landing at 11.4%. The revision marked a 35 basis point (“bps”) hike from the prior forecast. And it was also notable since it exceeded management’s 2025 target of 10.6%.

All considered, the sales and margin strength ultimately contributed to a new expected earnings midpoint of $3.59/share, a positive $0.15/share revision to the prior midpoint.

Recap of TJX Q3 Results

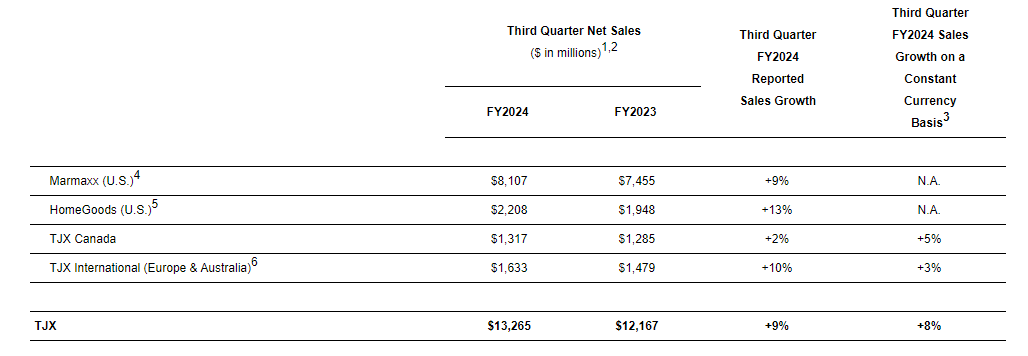

TJX turned in another strong quarter that came in above expectations. In Q3, total comparable store sales increased 6%, driven by customer traffic. The increase in comparable store sales stood in stark contrast to Target ( TGT ), who earlier reported a 4.9% decrease in the same metric. The sales strength supports the notion that TJX remains an attractive shopping destination ahead of the holiday season, perhaps at the expense of their more full-price peers.

{kind=link}

TJX Q3 Earnings Release - Summary Of Quarterly Sales

More to the bottom line, TJX reported pretax margins of 12%, well above the midpoint of 11.4% that the team had set out in their Q2 earnings commentary. Additionally, TJX reported a 200 basis point YOY increase in gross profit margins to 31.1%.

Driving the margin increase was a combination of sales strength and timing aspects pertaining to certain expenses, which are expected to reverse out in the fourth quarter. It’s also worth noting that the operating margin strength was despite a 140 basis point increase in SG&A costs.

On an overall basis, TJX reported total diluted EPS/share of $1.03, comfortably above expectations by $0.03/share. Looking ahead, TJX again increased their full-year guidance, with their sights on higher comparable store sales and diluted EPS.

While the management team continues to expect comparable sales to be up 3% to 4% in Q4, they now expect full year comparable store sales to be up 4.5% at the midpoint. Furthermore, pre-tax margins are seen at 10.8%, slightly above the prior midpoint of 10.75%, with a new diluted EPS midpoint of $3.73/share.

The Continued Recovery In The HomeGoods Division

In prior coverage, I called out the lagging performance of TJX’s HomeGoods division following a stellar fiscal 2022. But despite the underperformance, I expressed bullishness in the division due to positive store traffic trends in Q1 noted by CEO, Ernie Herrman.

As it would happen, TJX did receive a notable assist from HomeGoods in Q2. During the quarter, the unit saw comp store sales increase 4% due to an increase in customer traffic. More notably, the unit saw positive sequential upticks in every month of the quarter.

Returning to Q3, TJX closed its HomeGoods e-commerce business. In doing so, it created a negative and unexpected headwind to EPS of $0.03/share. Despite the shutting of the e-commerce unit, the division itself continued its recovery. In fact, it outperformed Marmaxx, with a comparable sales increase of 9% versus 7% for TJX’s mainstay.

In a sense, this should have been expected, given the positive second half comp environment for the division that TJX had guided for previously. Still, the turnaround is noteworthy given that the unit was down 7% to start the year.

Is TJX Stock A Buy, Sell, Or Hold?

The expectations were high for TJX following positive revisions to their second half guidance. The stock had also been pushed higher by investors who remained optimistic about the appeal of TJX’s off-price model in an era of persistently high pricing pressures.

In Q3, TJX not only delivered on expectations, but they surpassed on seemingly every metric. Most notable, in my view, was the outperformance in the HomeGoods division, which reported comparable sales growth of 9% during the quarter, above the 7% reported by Marmaxx, TJX’s more consistent and stronger unit.

While the closure of the HomeGoods e-commerce business added a notable $0.03/share headwind to overall earnings, TJX was still able to comfortably beat market expectations. In addition, they once again raised their full year outlook, given the strength reported thus far.

Looking ahead, I believe TJX can meet their full year targets by remaining a preferred shopping destination for consumers seeking a discount this holiday season.

Shares have gained since my last preview article, but the stock still trades modestly below my target price of $100/share. While the upside potential admittedly isn’t the most significant at current trading levels, I believe TJX is still an attractive “buy” for investors seeking positioning in the retail sector. Following earnings, TJX is riding high on positive momentum, momentum that I see continuing into year-end.

For further details see:

TJX Companies Q3 Earnings: Remaining A Preferred Shopping Destination Ahead Of Holiday Season