TJX - TJX Companies: Raising Price Target As Momentum Continues

2023-09-06 04:16:08 ET

Summary

- The recovery in TJX Companies' home segment bodes well for the stock.

- TJX remains in an ideal environment for off-price retailers.

- I'm rasing my price target as its strong operating momentum continues.

With The TJX Companies ( TJX ) up over 25% since my initial write-up in March and closing in on my original $100 price target let’s take a close look at the name. I originally placed a “Buy” rating on the stock, saying that while it was not cheap, that the company was riding the perfect wave and that it should be a nice beneficiary of industry de-stocking issues.

Company Profile

As a quick reminder, TJX is an off-price retailer that operates the T.J. Maxx, Marshalls, HomeGoods, HomeSense, and Sierra concepts in the U.S. Internationally its concepts include Marshalls, HomeSense, and Winners in Canada and T.K. Maxx, HomeSense, and similar chains internationally.

Marmaxx, which consists of its T.J. Maxx and Marshalls brands, is its largest segment, and the two concepts focus on apparel, footwear and accessories, as well as home furnishings and home decor. Its HomeGoods and HomeSense brands, which sell items such as furniture and other home items, make up its second largest segment it calls HomeGoods.

Q2 Results and Home Decor Recovery

Part of my ongoing thesis with TJX was that the company was in a great situation in the apparel space. This was due to the company getting better inventory at attractive prices as a result of retailers over-ordering due to prior supply chain issues leading to retailers and brands needing to offload excess inventory, as well as shoppers looking for bargains as the inflation hit consumers buying power. This dynamic once again showed up in Q2.

For Q2, TJX’s Marmaxx segment once again led the way, with sales up 9% to $7.9 billion in the U.S. Same store sales climbed 8%. The segment’s profit margin was 13.7%, up 80 basis point. The same-store gains were entirely driven by increased traffic, and both apparel and the home category saw high single digit comp increases. Same-store sales were also strong across regions and customer income levels.

HomeGoods, meanwhile, saw a nice recovery, with revenue rising 8% to $2.0 billion. The segment’s comparable-store sales rose 4%. Segment profit margin was 8.7%, up 600 basis points, helped by lower freight costs. The company saw comps and traffic accelerate each month in the quarter

TJX International sales, meanwhile, climbed 8% to $1.62 billion on a 3% increase in same-store sales. TJX Canada saw revenue slip -2% to $1.22 billion, as comparable store sales rose 1%.

Overall sales jumped 8% to $12.76 billion, topping the $12.45 billion analyst consensus. Overall comparable store sales rose 6%.

EPS of 85 cents, meanwhile, beat analyst expectations by 7 cents. Gross margins came in at 30.2%, up 260 basis points.

Inventory at quarter end was $6.6 billion, down from $7.1 billion a year ago. On a per store basis, inventories are down -6% year over year.

The company ended the quarter with 4,884 stores compared to 4,736 a year ago.

This was a terrific quarter from TJX. While apparel continues to lead the way, the bigger story was the recovery in the home segment at both Marmaxx and HomeGoods. The home furnishings industry as a whole has struggled this year, both at TJX and other retailers, so to see a bounce back is a great sign. The company should have plenty of attractive buying opportunities in the space given the struggles of full-price retailers, so this could certainly turn into an area of strength moving forward.

Outlook

Looking ahead, TJX forecast fiscal Q3 EPS to be between 95-98 cents. Overall sales are projected to jump 6-7% to $12.9-13.1 billion. It is looking for same store sales to rise between 3-4%

For fiscal Q4, it guided for EPS to be between $1.10-1.13. It is looking for same store sales to increase between 3-4%. Q4 will have an extra week compared to last year. It is projecting adjusted gross margins to be between 29.4%-29.5%, a 180-190 basis point increase versus last year, helped by lower fright costs.

For the full year, the company is projecting EPS to be between $3.66. $3.72. It is looking for comparable sales to rise between 3-4%.

On its Q2 earnings call , CEO Ernie Herrman said:

“We are very pleased with the continued momentum of our business and the excellent execution of our teams across the company. They have been laser-focused on driving sales and traffic and improving profitability. The third quarter is off to a very strong start, and we feel great about our plans for the remainder of the year. The marketplace is loaded with outstanding buying opportunities and we are confident that we will continue to offer a terrific mix of brands and an outstanding assortment of gifts to our shoppers during the fall and holiday selling seasons. We are convinced that our differentiated treasure hunt shopping experience and excellent values will continue to serve us well and allow us to capture additional market share across our geographies for many years to come.”

TJX’s momentum appears to have continued into the early part of Q3, with no signs of slowing down. Importantly, the company said it is still seeing good buying opportunities. At the same time, the company has said it is attracting new customers, particularly Gen Z and millennials, which should bode well for continued future growth.

Valuation

TJX stock currently trades at 17.2x the FY 2024 (ending January) consensus EBITDA of $6.63 billion. Based on FY25 analyst estimates of $7.18 billion, its trades at ~15.9x.

On an EBITDAR basis, it trades at 13.2x FY24 estimates and about 12.4x FY25 estimates.

It trades at a forward PE of 24.9x the FY24 consensus of $3.72, and 22.8x FY25 estimates of $4.07.

The company is projected to grow revenue 7.7% in FY24 to $53.1 billion and 4.8% in FY25.

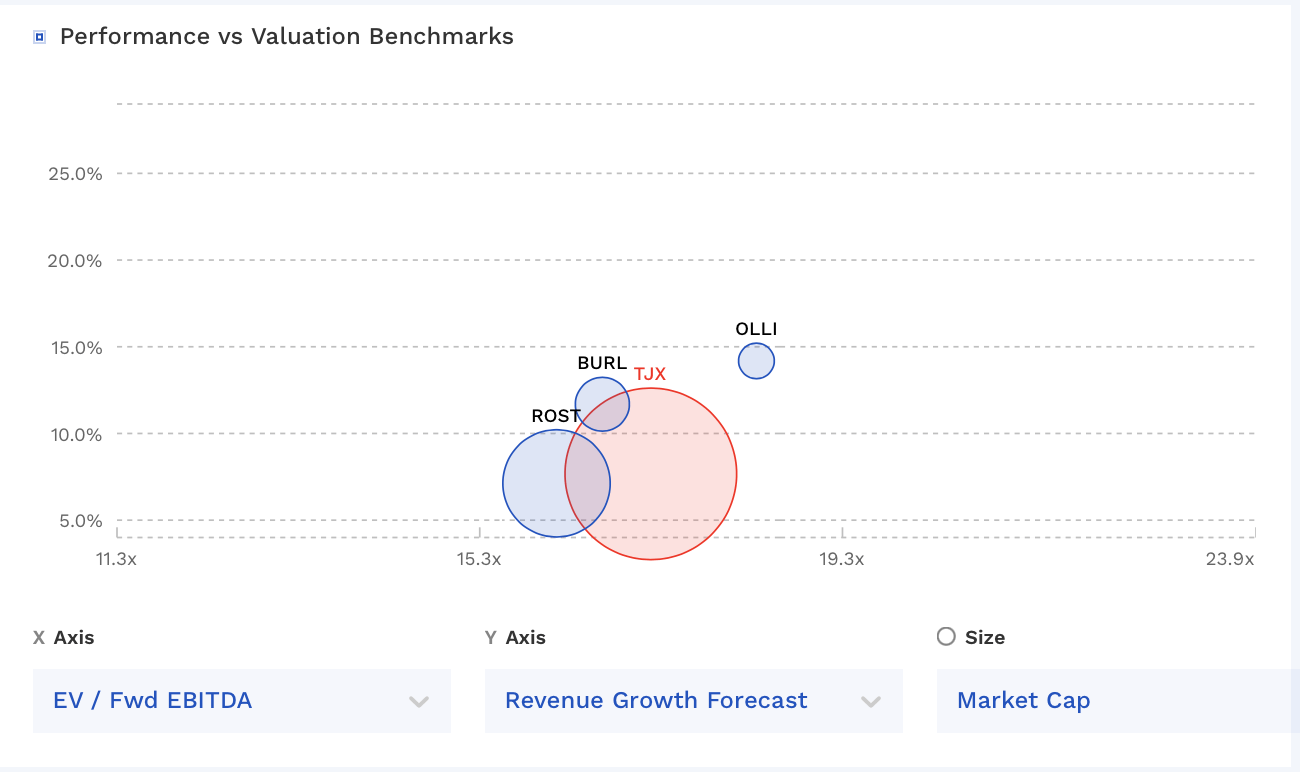

TJX trades at a similar multiple to its off-price peers.

{kind=link}

Conclusion

With both apparel and home goods now both working and freight costs coming down, TJX appears to be firing on all cylinders. This momentum should continue as consumers look for areas to cut back on without reducing overall spending. The company remains in a strong place in a great environment for off-price retail.

With the momentum continuing, I’m going to increase by price target from $100 to $120. That equates to around a 20x EBITDA multiple on FY25 estimates and under 16x on a EBITDAR basis. My ‘Buy” rating remains. While its valuation continues to creep up, as long as TJX's sales and margin momentum continue, the stock should be able to support a higher valuation.

For further details see:

TJX Companies: Raising Price Target As Momentum Continues