TJX - TJX Companies: Unraveling Retail Success Story

2023-11-12 00:06:41 ET

Summary

- The company's business model is highly attractive, with recurring customer visits, resilience against e-commerce, and the ability to maintain strong margins.

- With economic difficulty encouraging more to shop with TJX, scope for further store expansion, and brand diversification, we see growth continuing.

- Margins are also improving, although slowly due to inflationary pressures offsetting this.

- TJX outperforms its peers noticeably, with better growth and margins despite its larger size. This suggests the business model remains highly lucrative.

- TJX is currently expensive in our view, with limited scope for immediate upside.

Investment thesis

Our current investment thesis is:

- TJX is an impressive business, owing to its high-quality business model that allows the business to minimize costs while encouraging above-average customer store visits, the resilience of store demand despite the rise of e-commerce, and strong growth.

- Management has maximized the value of this model but expanding across other brands (all of which maintain good consumer interest), diversifying its revenue stream and capturing a bigger market.

- When compared to other retailers, the business performs incredibly well, with better growth, higher margins, less cyclicality, and a better growth runway.

- TJX is currently expensive in our view, with limited scope for immediate upside given the weakness in the macroeconomic environment. For this reason, we suggest investors remain patient until market conditions improve.

Company description

TJX Companies ( TJX ) is a leading off-price retailer based in the United States. It operates various retail chains, including T.J. Maxx, Marshalls, HomeGoods, and Sierra, offering a wide range of discounted apparel, home goods, and other merchandise.

Share price

TJX's share price has performed exceptionally well in the last decade, returning over 200% to shareholders and outperforming the wider market. This has been achieved through an impressive strategic execution, contributing to strong financial development.

Financial analysis

{kind=link}

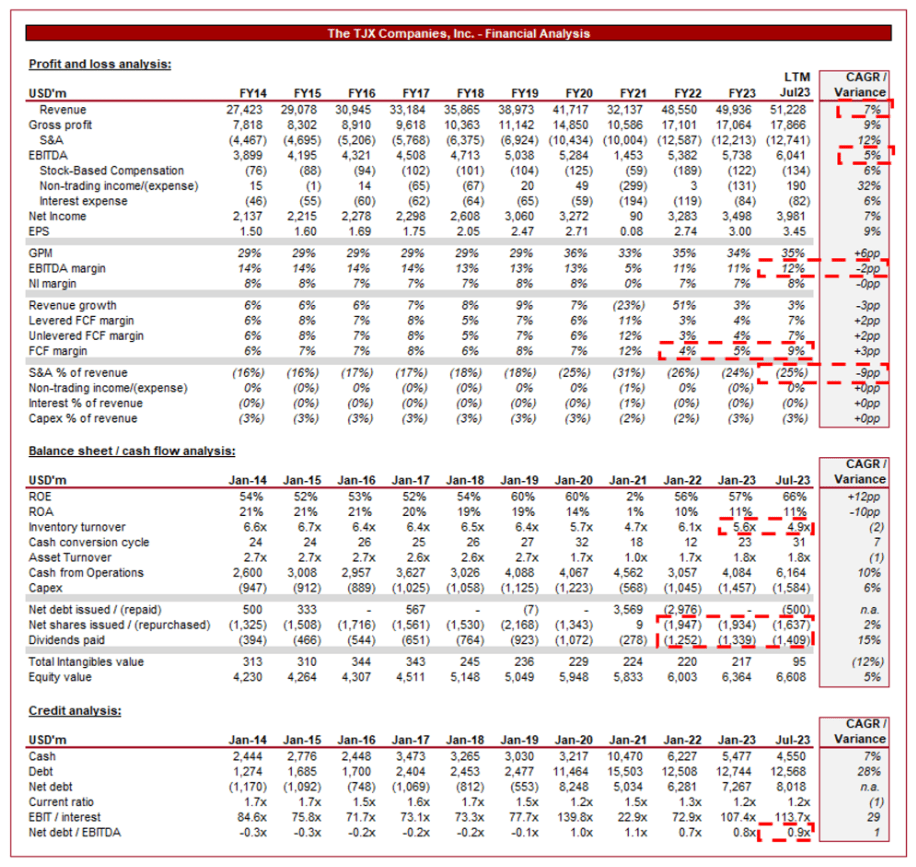

Presented above is TJX's financial performance in the last decade.

Revenue & Commercial Factors

TJX's revenue has grown at a respectable CAGR of 7% in the last 10 years, with incredibly consistent growth. Prior to the pandemic, growth sat between 6-9% in every fiscal year since FY14.

Business Model

TJX's primary business model is off-price retailing. It purchases brand-name and designer merchandise directly from manufacturers, department stores, and other retailers at substantial discounts due to a number of reasons (such as overstock, closeouts, canceled orders, etc.). This enables the company to offer these products at significant discounts to regular retail prices.

TJX's retail chains offer a wide and diverse range of products, including apparel, home goods, furniture, accessories, footwear, beauty products, and more. The constantly changing inventory is a uniquely fundamental characteristic of the business, creating a treasure-hunt shopping experience for customers, and encouraging frequent visits to the stores. Recurring customer visits is highly lucrative, and difficult to achieve, as it increases the likelihood of sales.

The company operates different store formats under different brand names, each catering to specific customer segments. T.J.Maxx and Marshalls focus on apparel and home goods, HomeGoods/HomeSense specializes in home decor and furnishings, and Sierra offers outdoor and active lifestyle products. This distinction allows the group to utilize its business model to expand across various retail industries, maximizing its returns. TJX has been incredibly successful with this strategy, developing a range of highly regarded brands, with the parallel benefit of diversifying its revenue.

TJX carefully selects store locations in high-traffic areas, including off-mall locations and other retail hubs, to attract a wide customer base. This strategy allows the company to reach a diverse demographic and maximize foot traffic.

The company's buying and merchandising teams possess extensive industry knowledge and expertise. They have a keen eye for identifying trends and popular products, as well as continuing to source high-selling goods. This is a critical success factor for the business and continues to be executed well, allowing its products to resonate continuously in an ever-changing retail industry.

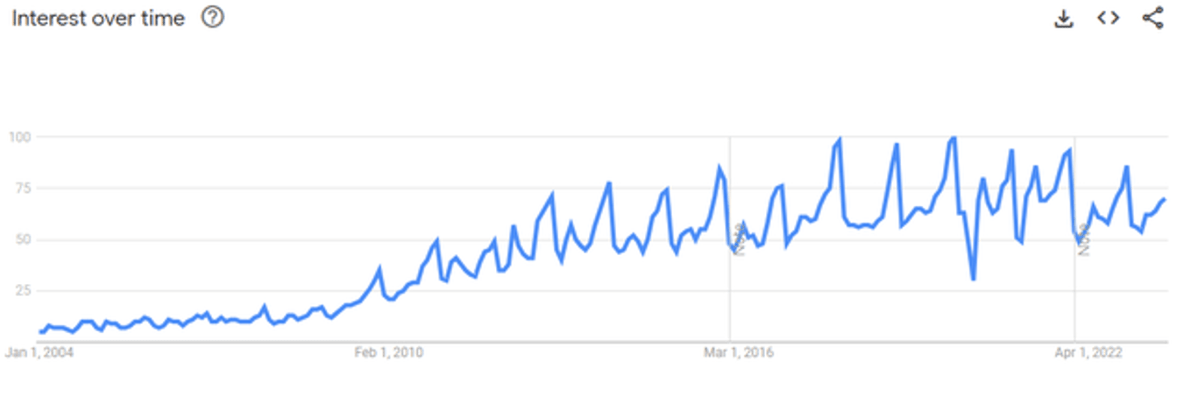

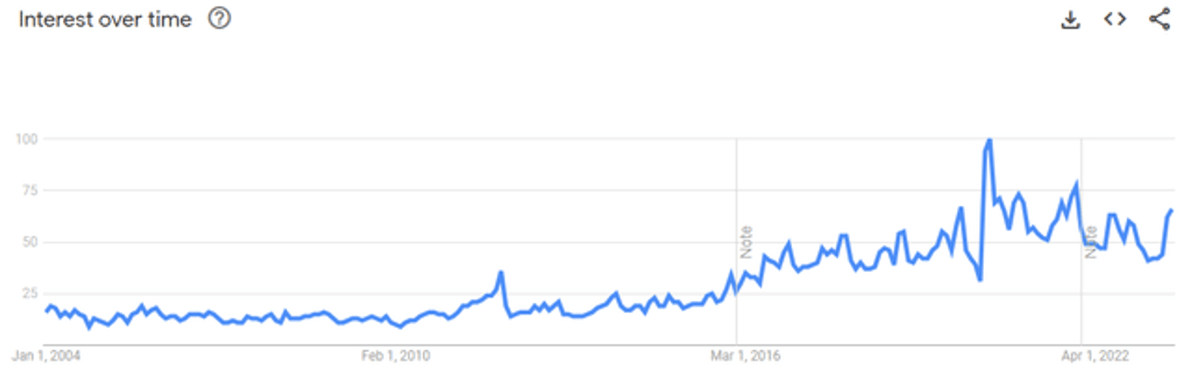

As the following illustrates, this business model has allowed the business to maintain and increase the interest in its brands over time. The key in our view is its ability to maintain its value proposition while continuing to expand nationally and internationally.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

TJX emphasizes rapid inventory turnover. Its off-price model encourages customers to make impulsive purchases due to the attractive discounts and limited availability of products. This approach maximizes cash generation and reduces the risk of stockpiling during downturns (a key downside of retailers).

Competitive Positioning

The retail industry has been incredibly hard hit by the rise of e-commerce. Consumers are in a position to shop around, benefit from convenience, and have the ability to compare. This has contributed to the "death of the department store / high street". TJX's growth trajectory reflects resilience against this. The reason is this "treasure hunting" experience. Although the business offers an e-commerce option, it is not the same (due to the nature of fast-moving products). For this reason, the company's store approach has continued to be lucrative and we see no reason why this would change, even as e-commerce continues to outperform.

TJX's core value proposition of offering brand-name merchandise at discounted prices has resonated well with consumers, especially during challenging economic times. A continued widening of the wealth gap, as well as changing economic conditions that worsen the finances of the working/middle classes will further attract consumers seeking bargains.

TJX's ability to succeed in the traditional brick-and-mortar segment is highly important to its competitive position, as it allows the business to market its offering through footfall while capturing an increased group as its related competitors reduce their store exposure.

Expanding store presence to new geographic regions (and continually in its core markets) will be a key growth driver going forward, in conjunction with organic growth. The strength of its brand in the UK and Europe should allow a smooth transition into new markets, while its key capabilities in global product sourcing should be a compelling offering on day one.

TJX competes with various retailers in different segments, including Ross Stores ( ROST ), Burlington Stores ( BURL ) Nordstrom Rack (part of Nordstrom Inc.) ( JWN ), and many other off-price divisions of department stores. Relative to these businesses, we believe TJX performs well, particularly due to its ability to continue store growth.

Economic & External Consideration

Current economic conditions represent potential headwinds, as high inflation and elevated interest rates dissuade discretionary purchases, particularly as finances are currently being squeezed.

What is slightly different from past years of comparable conditions is that unemployment remains low and wage inflation is respectable, reducing the risk of a recession.

In the long term, we believe these conditions could be beneficial for the business. As mentioned previously, this will contribute to financial hardship for many, which will take years to recover from. This will encourage increased bargain/discount spending, particularly for those looking to maintain a certain lifestyle.

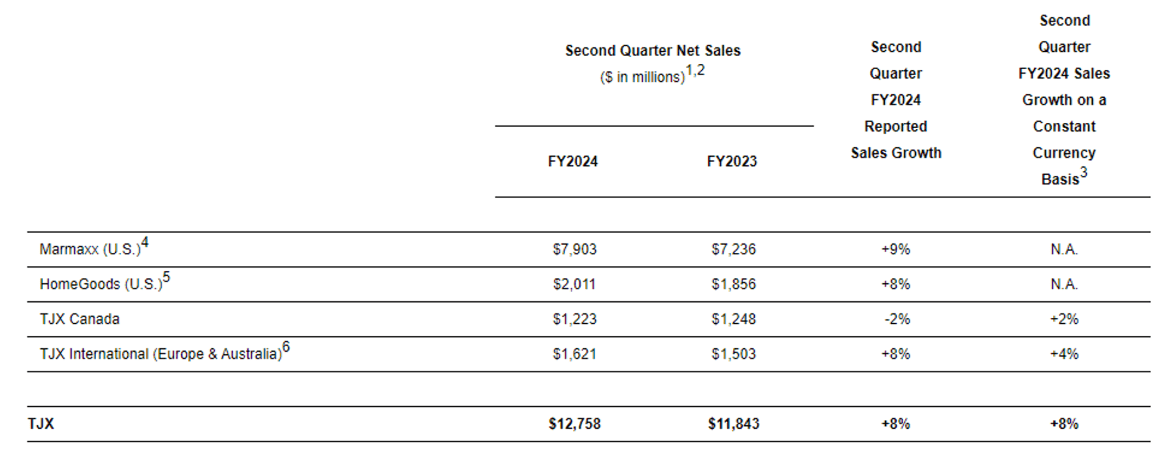

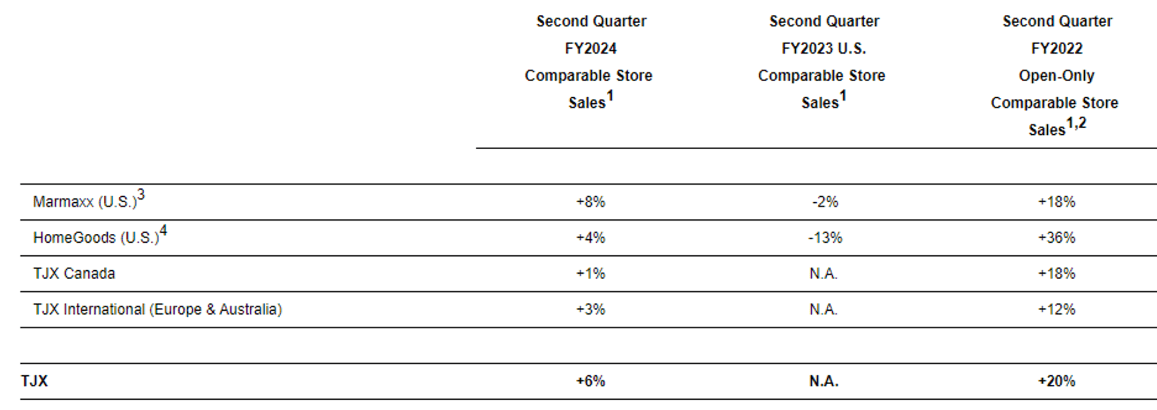

In the most recent quarter, TJX has experienced a 8% top-line growth rate (6% comparable), led by a strong performance in the US and a modest performance in Europe, offset by weakness in Canada. This is unsurprising considering the US has progressed the furthest with bringing inflation under control.

{kind=link}

Drilling into this further, comparable growth looks marginally better, with a specific weakness in HomeGoods over a longer period. This is not surprising given home sales are declining rapidly and generally represent larger purchases, which are not going to be made with elevated mortgage rates.

{kind=link}

Our expectation for the coming quarters is MSD/LSD growth as demand softens, with improvements once expansionary policy can return. On a relative basis, this is extremely good, as many peers are seeing inventory build-up and growth turn negative.

Margins

TJX's margins during the historical period were strong, with little variability. Following the pandemic, the business experienced some erosion, primarily due to its reliance on footfall.

Margins have been on an upward following FY22, as the business continues to ramp post-pandemic. Given the high level of competition in the industry and the offsetting inflationary headwinds, this improvement is gradual. Our expectation is that it will take the business another 24-36 months to return to an EBITDA-M of 14%.

Balance sheet & Cash Flows

TJX's inventory turnover remains below its pre-pandemic level and has slightly declined from Jan23. This implies growth is slowing, likely reflecting the weakness in home goods. This does imply an upside in FCF once Management can bring this level up, which we believe is possible.

TJX is conservatively financed, with a ND/EBITDA ratio of 0.9x. This has allowed the business to heavily distribute to shareholders through dividends and buybacks, boosting its ROE from 54% to 66%.

Industry analysis

{kind=link}

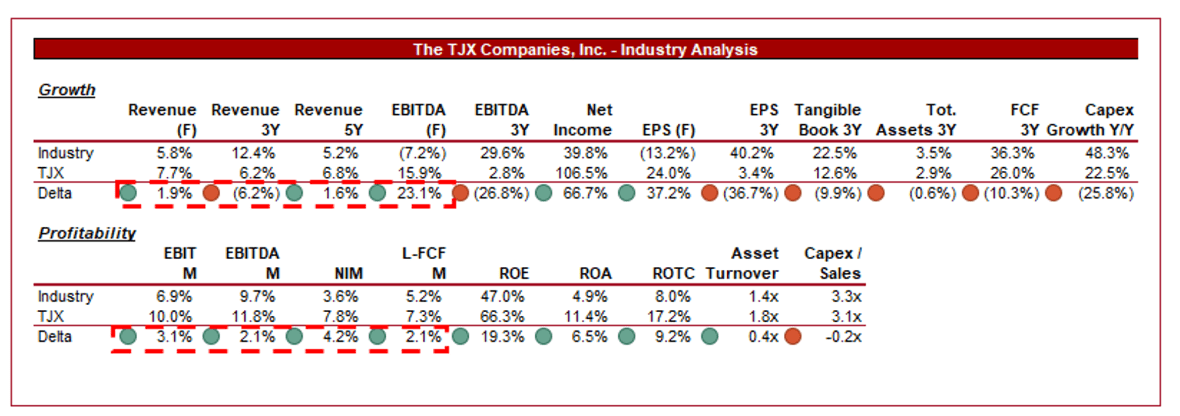

Presented above is a comparison of TJX's growth and profitability to the average of its industry, as defined by Seeking Alpha (25 companies).

TJX performs incredibly well compared to its peers. TJX has achieved strong revenue and profitability growth relative to the cohort, with the expectation for this to continue. This is highly impressive given the group includes businesses that are smaller and focused on growth. This is driven by a continued slowdown by its peers while TJX is still positioned well to benefit from footfall.

Further, the business has noticeably higher margins, despite the post-pandemic contraction. This is not only a reflection of its scale but the success of its business model.

Based on this analysis, we believe TJX should trade at a premium to the industry average on a financial basis. Compounding this is its commercial resilience (retail is highly cyclical while TJX has shown itself to be less so) and ability to continually expand footfall. When also considering this, we believe the premium should be large.

Valuation

{kind=link}

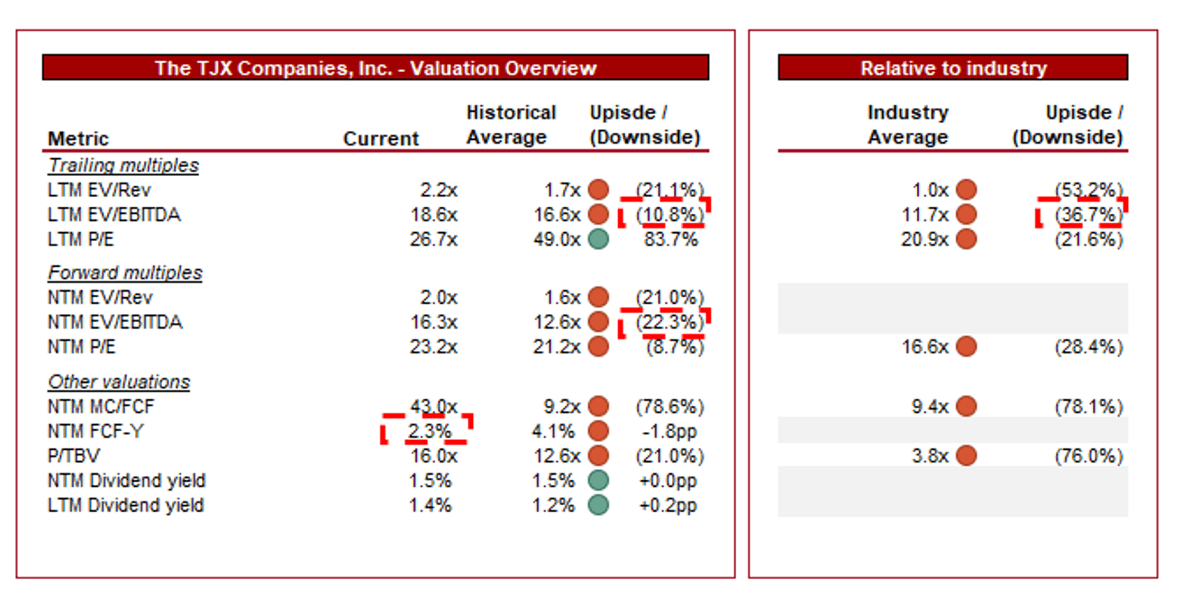

TJX is currently trading at 19x LTM EBITDA and 16x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is warranted in our view, primarily due to the resilience it has shown in the last decade, the growth in distributions that are sustainable, the development of a range of brands, and continued expansion. The current premium of ~23% (NTM basis) looks expensive. Compounding this is its FCF yield, which has currently declined to 2.3% (although is short-term depressed).

As previously discussed, a premium to its peer group is also warranted. On an LTM basis, this premium looks fairly substantial, but this shrinks when considering it on a NTM P/E basis. The existing level appears reasonable, although does not suggest upside beyond this.

It is likely that the immediate upside is somewhat limited based on the current share price of TJX, however, its strong business model and continuation of its growth trajectory despite some weakness implies the business has scope for growth long term.

Key risks with our thesis

The risks to our current thesis are:

- QoQ results. The evidence is clear that with housing market weakness, the business is feeling the strain on that part of the business. There is a risk that growth slows further, likely to be due to a further decline in home goods.

- Continued margin improvement. Our thesis implies EBITDA-M can at least return to its pre-pandemic level of 14%. Given the time period required to achieve this, there is a clear execution risk.

Final thoughts

TJX is an incredibly attractive business. The company has grown consistently despite industry disruptions, maintaining leading margins. Further, its business model is innovative and continues to allow the business to outperform, allowing Management to "copy/paste" it into other retail segments. With brand interest remaining strong and economic conditions encouraging new consumers to try TJX in the medium term, we suspect this trajectory will continue.

TJX currently appears expensive. We would usually disregard this as the company shows sufficient long-term potential that timing is not overly important. This said, with near-term demand concerns, and limited catalysts, we suggest a hold until macroeconomic conditions improve.

For further details see:

TJX Companies: Unraveling Retail Success Story