TJX - TJX Companies: Valuation No Longer Attractive

2023-10-11 05:59:46 ET

Summary

- TJX Companies has massively outperformed the retail sector year-to-date and raised its FY2024 guidance on comp sales, margins & earnings after an exceptional quarter.

- The company's solid results in Q2 were broad-based with an additional benefit from Gen-Z shoppers, it's confident it's taking market share and is benefiting from strong buying opportunities.

- TJX is no longer cheap & is trading at a premium valuation after a 70% rally over the past 18 months, making it difficult to justify chasing it above $89.00.

It's been a rough few months for the Retail Sector ( XRT ) with relatively low beta large-cap names like Dollar General ( DG ) being cut in half, and several smaller-cap names struggling to find durable bottoms in their share prices. However, one name that has performed exceptionally well and shrugged off the sector-wide weakness is off-price retailer TJX Companies ( TJX ), which has trounced XRT's negative year-to-date performance and has even outperformed the S&P 500 ( SPY ). This can be attributed to another exceptional quarter from the company, which prompted it to raise FY2024 guidance. In this update, we'll look at how the stock is set up heading into its Q3 and FY2024 results, its valuation after two years of significant outperformance, and whether the stock is worthy of buying after its recent correction:

Marshalls Stores - Company Presentation

{kind=link}

Introduction & Recent Results

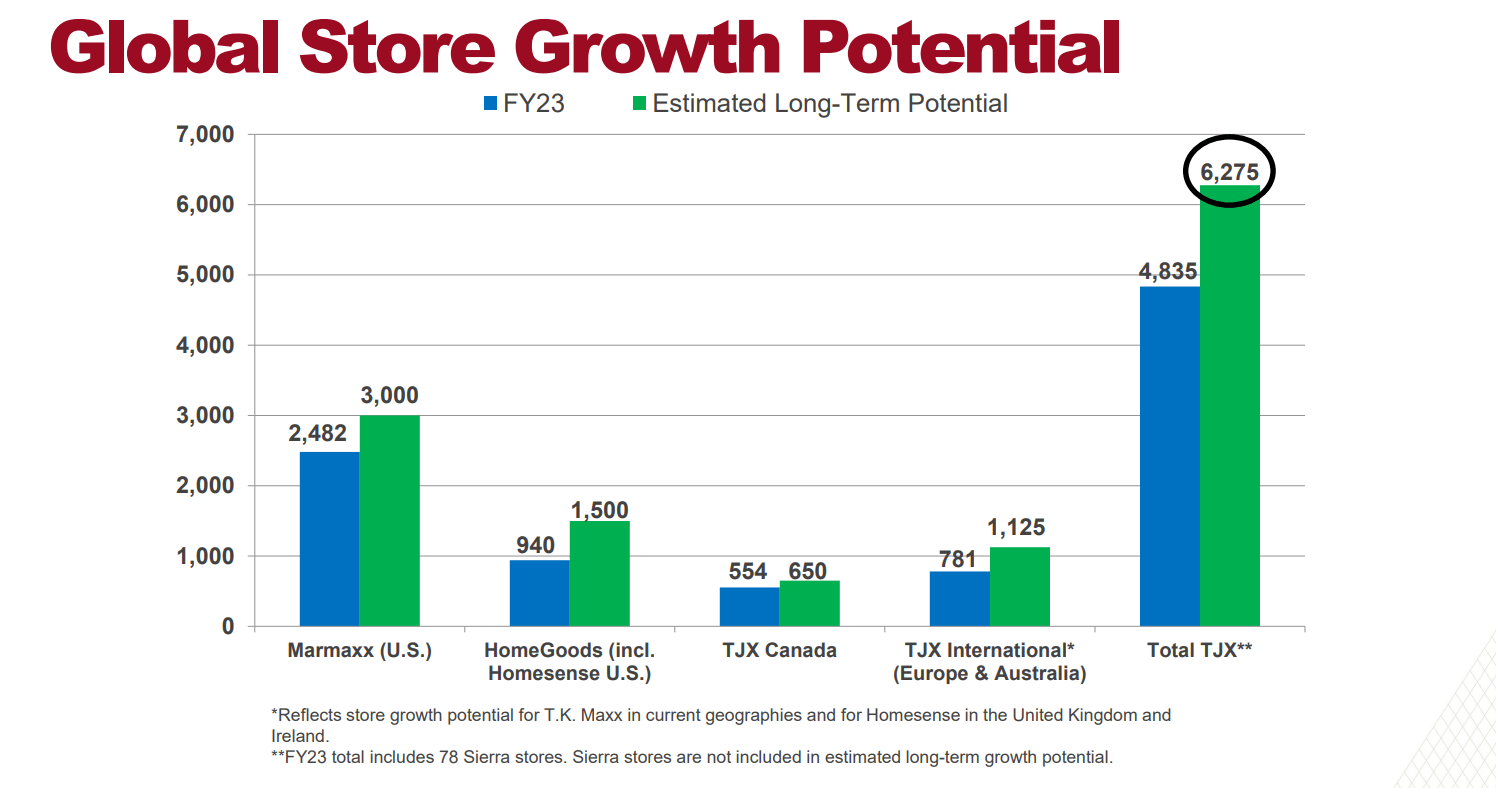

TJX Companies ("TJX") is one of the largest retailers globally, offering a treasure hunt experience in the off-price category with a fleet that is nearly half that of Walmart ( WMT ) with over 4,800 stores globally, but still a respectable unit growth rate of ~3%. The company was founded in 1976; its brands include TJ Maxx, TK Maxx, HomeSense, Winners, Marshalls, Sierra and HomeGoods, and the company has more than doubled its store count since 2006. Also impressive is that the company has executed extremely well against its strategy and outside of a misstep with AJ Wright (now closed), the company has trounced its previous outlook of a long-term potential for 3,000+ stores across its concepts. In fact, the company's new outlook is for ~6,300 stores across its current geographies, over double its previous outlook provided two decades ago, and with the potential to gain market share at existing stores that overlap following the closure of Bed Bath and Beyond.

TJX Store Count & Long Term Growth Potential - Company Presentation

{kind=link}

Digging into the company's fiscal Q2 2024 results, they were nothing short of exceptional, with revenue up 8% to ~$12.8 billion, quarterly earnings per share soaring 23% to $0.85 (Q2 2022: $0.69), and comp sales coming in up 6%, above the company's expectations for the period. Just as impressively, MarMaxx (TJ Maxx and Marshalls) was up 8% for the period driven by higher transactions, with the company calling out strength in apparel and accessories. Meanwhile, it also reported that home sales returned to positive comp sales growth and that traffic was higher at every division. Finally, the company noted that while its average ticket was down, this was offset by a larger basket size, and it shared that comp sales and transactions at its MarMaxx division accelerated throughout the second quarter with the momentum continuing into fiscal Q3.

TJX - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

This is certainly encouraging commentary against a backdrop of more cautious commentary sector-wide, with many companies citing the weaker macro outlook as a reason to retract or revise their full-year guidance lower. And while it certainly helps to be a trade-down beneficiary vs. full-priced retailer with TJX offering a treasure hunt like experience with constantly refreshed offerings at a strong value proposition, it was also positive to hear that it's seeing consistent performance across all income categories. And digging into development, the company is expecting ~3% unit growth for the year with 125 net new stores, leaving the company just shy of 4,500 stores to finish the year across its concepts. This unit growth provided a further boost to sales, with 19 stores added in the quarter, with six new HomeGoods stores and a relatively even split across its other concepts.

Moving over to margins and inventory, TJX also outperformed its expectations, delivering a 10.4% pre-tax margin, up from 9.2% in the year-ago period. The company noted that this was driven by lower freight costs and sales leverage, and its gross margins were up 260 basis points in the period on higher merchandise margin from lower freight costs. These margins are up sharply from pre-COVID-19 levels despite a consistent trend of above-average wage inflation in the sector with rising minimum wage and several larger brands investing in wages to improve retention and ensure they have the team members to deliver on their growth. Finally, consolidated inventory on a per store basis was down 6% excluding in-transit and e-commerce, and total inventory was down from $7.1 billion to $6.6 billion year-over-year.

H2 2024 Outlook & Company Commentary

In terms of the macro outlook, it's certainly one that makes it difficult to justify owning retail and restaurant stocks, with risk-free rates continuing to march higher and most retail names warning about a choppy environment. This is certainly clear in the restaurant industry where traffic fell off a cliff in August and September, even among trade-down categories like quick-service. However, while some lower-priced retailers are struggling given, the backdrop of a weaker average consumer (with increased softness for less affluent consumers), TJX is favorably positioned with a core customer that is a 25-55-year-old female in the mid to high income categories. And it doesn't hurt that the company is getting visits from Gen-Z customers, with some of this potentially attributed to RushTok which has been trending on TikTok, with many of those participating highlighting apparel they've picked up at TJ Maxx, with the company stating on its Q2 Call:

Just generally looking at the transaction increases that we have, we believe that we are attracting more new customers to our brands. And when you look at how we're attracting those customers. They tend to be more younger customers, the more Gen Z customers that we're attracting, which we're really excited about because that speaks to the longevity that we see."

- TJX, Fiscal Q2-24 Conference Call

As for general commentary, shrink and any headwinds, TJX noted that its shrink indicators are pointing to shrink being flat this year but that it will not know the full impact of its shrink initiatives until its full inventory count is complete at year-end. As for pricing, the company noted that it sees room to take price in certain areas and that it's confident that it's seeing some market share growth evidenced by categories it carries, and there's room for growth from Bed Bath and Beyond and online home retailers that may not have executed as well, in addition to the benefit of potential attractive sites opening up following the Bed Bath & Beyond closures. Finally, the one negative is that wages continue to be a headwind and the company noted that it plans to continue to invest here to stay competitive. On a positive, attrition rates are either in line or improving vs. last year which should at least provide some benefit on the hiring/training side if the company can see better retention.

Personal Savings Rate - FRED, BLS

{kind=link}

To summarize, while personal savings rates have continued to trend lower, there's a further impact from student loan payments restarting and traffic overall in the Retail Sector has softened, TJX is finding a way to drive sales and seems to have a bonus tailwind from a non-core customer in Gen Z with occasional free promotion of items available at its stores, and a benefit on the home category from the closure of Bed Bath & Beyond. Meanwhile, the company benefits from being the only major off-price retailer in Canada at HomeSense and Marshalls with a loyal base of shoppers that continue to hunt for deals at its stores in a tougher economy. And with the company highlighting "strong buying opportunities in the marketplace" and growing market share, investors can be confident in a strong fiscal Q3 (mid-November) and finish to the year for this mega-cap retailer.

Valuation & Technical Picture

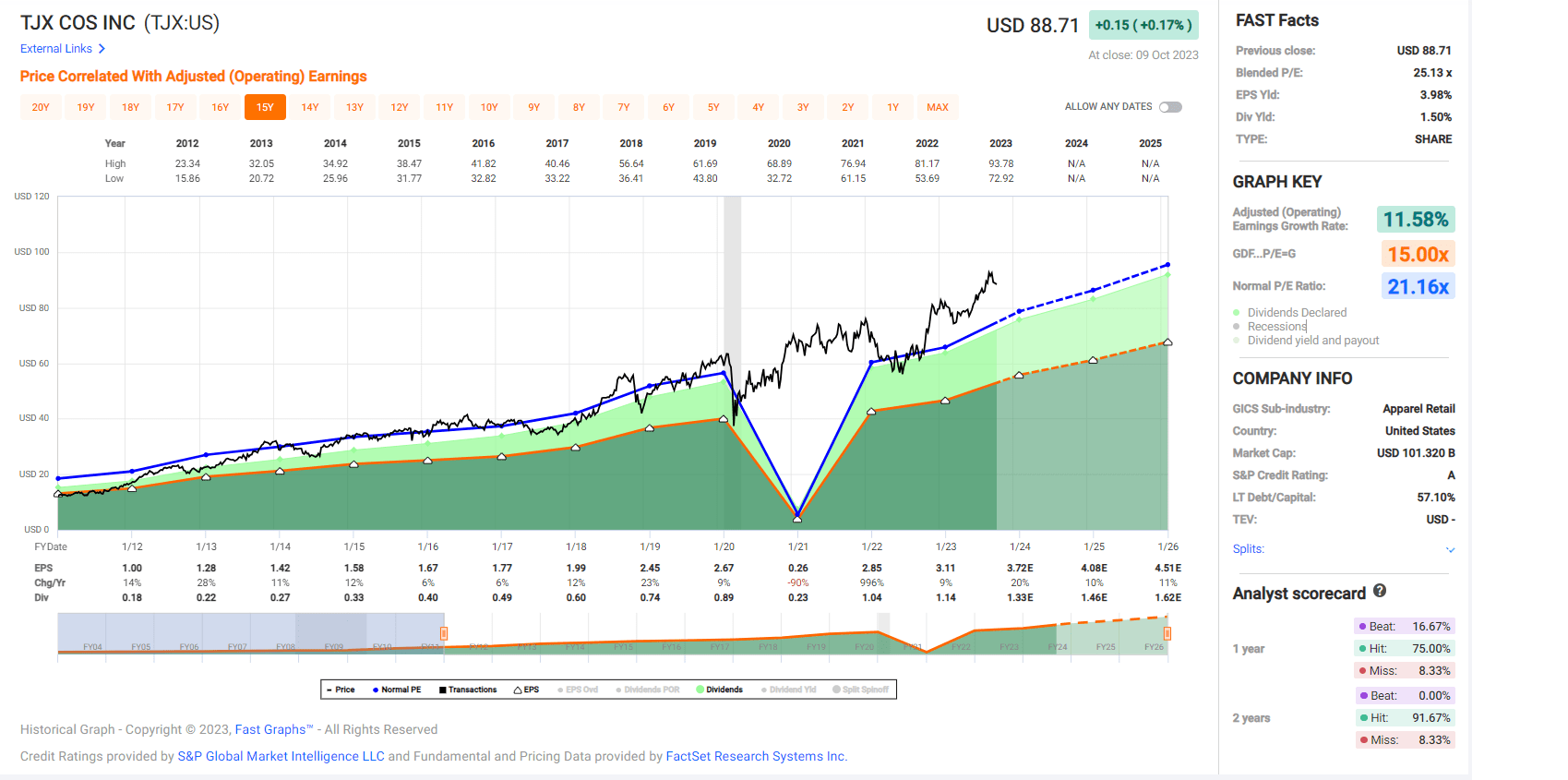

Based on ~1.16 billion shares and a share price of $89.50, TJX trades at a market cap of ~$104 billion, making it one of the highest capitalization names in the Retail Sector ( XRT ), just behind other behemoths like Walmart and Costco ( COST ). However, while the stock has outperformed the S&P 500 ( SPY ) by ~4000 basis points since its 2015 lows and is deserving of its premium multiple for its strong execution, the stock is no longer cheap, especially after its considerable outperformance this year (+13% year-to-date) vs. XRT. In fact, TJX currently trades at ~24x FY2024 earnings estimates, a premium to its 15-year average multiple of ~21.2 and in line with the PE ratio it traded at earlier this year before it suffered a ~13% correction. This doesn't mean that TJX can't head higher, and it's certainly possible that its outperformance could persist. However, with it trading at ~30x EV/FCF on FY2024 and at an earnings multiple where it's been more susceptible to 10-15% corrections, I think it's tough to justify chasing this relief rally.

TJX - Historical Earnings Multiple - FASTGraphs.com

{kind=link}

Some investors might argue that the stock has significantly more upside to fair value, with the potential to trade up to ~30x earnings like it did in late 2021. However, hoping for similar multiple expansion in the current environment might be a stretch, especially when risk-free rates are sitting near their highest levels in two decades, which should prompt investors to look for a higher hurdle rate or margin of safety for new potential investments. Using what I believe to be a more conservative earnings multiple of 22.0x earnings and FY2025 earnings estimates of $4.10, I see a fair value for TJX of $90.20, pointing to just a 3% upside from current levels. However, I prefer a minimum 20% discount to fair value to justify buying $100+ billion market cap names to ensure a margin of safety. And if we apply this discount, TJX's ideal buy zone comes in at $72.20.

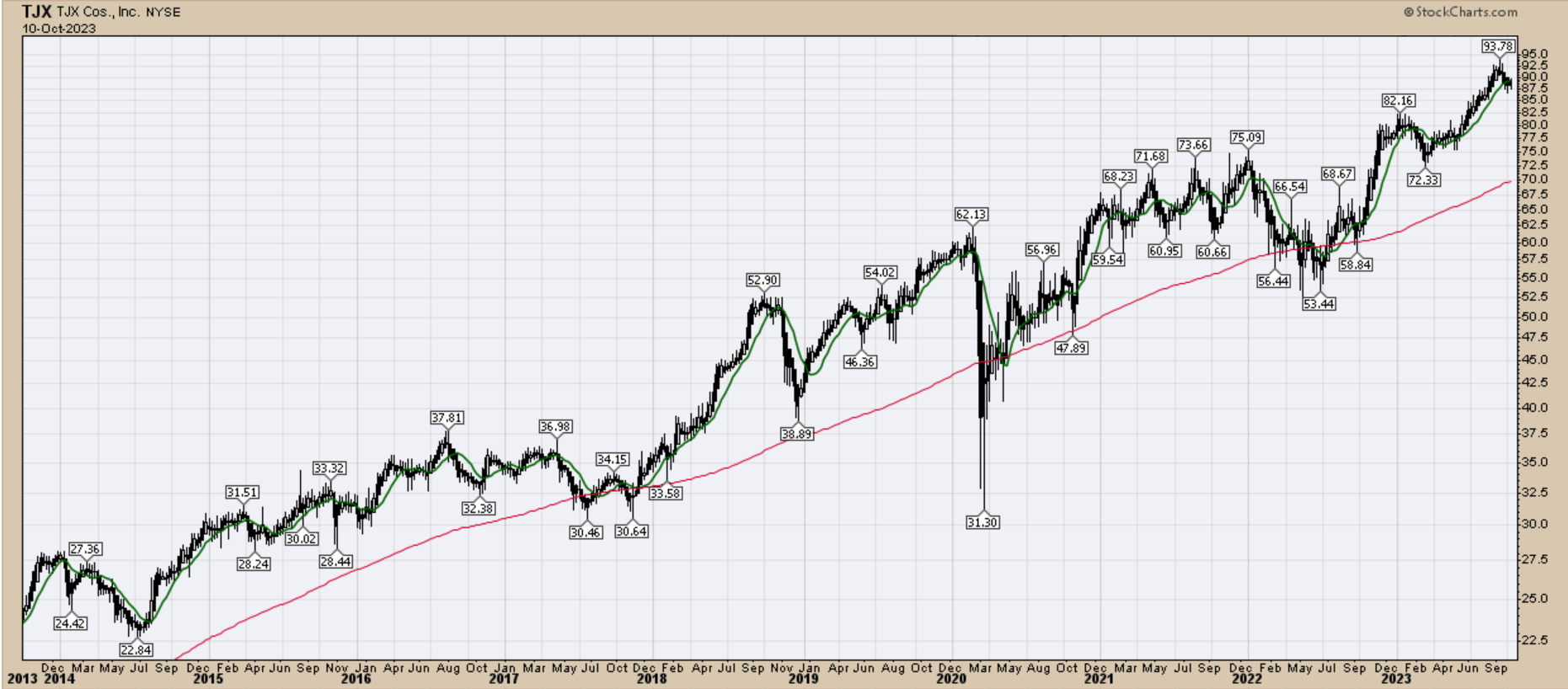

TJX Weekly Chart - StockCharts.com

{kind=link}

So, with TJX well above this buy zone, I don't see any reason to pay up for the stock here, and I think there are far more attractive places to direct one's capital if one is looking for deals. In addition, if TJX were to hit new highs above $97.00 on the back of a strong Q3 report before year-end, I would view this as an opportunity to book some profits into strength. Finally, if we look at the technical picture above, we can see that TJX has historically visited its 150-day moving average (red line) every couple of years, and it's now the most stretched above this moving average it's been since Q4 2018. So, if I were looking to start a position or add to the stock, I would wait for a pullback below $75.00 at a bare minimum, where this moving average might catch the stock as it has in the past.

Summary

TJX just came off another impressive quarter and is one of the few retailers firing on all cylinders and one of only a handful to raise its full-year guidance on comp sales, margins, and earnings. That said, I prefer to buy stocks when they're hated and trading at deep discounts to fair value, and while there was an excellent opportunity to scoop up off-price retail last year with Ross Stores ( ROST ) under $70.00 as I highlighted in my May 2022 update , the same deals aren't available today and TJX is arguably getting closer to fully valued as it heads into its fiscal Q3 results next month. So, while I think this is easily a top-10 name in the Retail Sector, I don't see this as the time to rush into the stock, and I would view any rallies above $97.00 before year-end as an opportunity to book some profits.

For further details see:

TJX Companies: Valuation No Longer Attractive