BIL - TLT: A High-Yielding Hedge

2023-07-17 11:11:35 ET

Summary

- Inflation and the subsequent rise of long-term interest rates to ~4% have resulted in long-term treasuries having a superior risk-reward profile to stocks and many other types of bonds.

- The Federal Reserve has institutional mandates to lower inflation and reduce unemployment, and these increase the probability of treasuries acting like a hedge during an economic downturn.

- The iShares 20+ Year Bond ETF is a compelling vehicle for capturing this opportunity within a tax-advantaged account.

- Depending on individual circumstances, it may make more sense to hold other investments that both have high yields and will hedge against an economic downturn.

Thesis

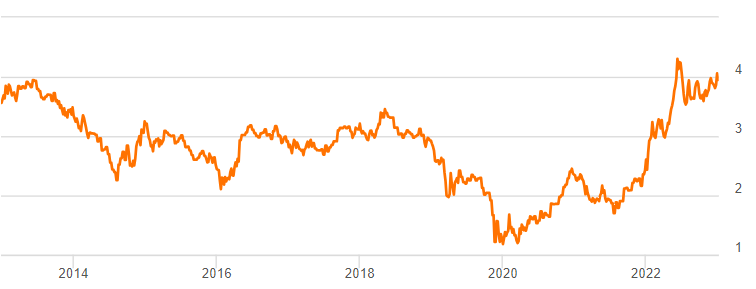

This year marks the first time in about a decade that the 30-year treasury bond has yielded more than 4%. Although US headline inflation ((CPI)) has declined in June to 3% from 9% last year, core inflation (PCE and CPI) remains close to 5%. The Federal Reserve targets core PCE inflation of 2%. As a result, it continues to increase the fed funds rate and roll off mortgages and treasuries from its balance sheet. Although it is impossible to know exactly when monetary tightening will end, all trends indicate the Fed will accomplish its inflation goal within the next couple of years. Looking ahead, the ~4% yield of the iShares 20+ Year Treasury Bond ETF ( TLT ) combined with 2% inflation is compelling. The high yield combined with the institutional imperative to lower future inflation makes long-term treasuries attractive.

US 30-year treasury bond yield over the past 10 years (Seeking Alpha)

{kind=link}

Unless risk is a primary concern, investing in treasuries may seem counterintuitive. Financial theory indicates higher return options should exist. Until the most recent debt ceiling crisis, treasuries were typically considered risk-free assets. Ideally, risky assets such as stocks should compensate investors with additional reward for assuming more risk. However, the popularity of investment themes in the past few years such as meme stocks, blank check companies, crypto, ESG, AI, and so on should be cause for some skepticism regarding rational pricing.

To compare the risk-adjusted return of treasuries and stocks, an estimate of the expected return of stocks is required. As a simplistic rule of thumb, I take the earnings yield of the S&P 500 as a starting point. Currently, trailing and forward price-to-earnings for the S&P 500 are ~20 . Inverting this ratio leads to a 5% earnings yield and expected return. Next, arguments can be made for positive or negative adjustments. On the positive side, earnings yield does not consider future growth. On the negative side, earnings are an accrual accounting metric and can easily be inflated by management assumptions and estimates. Free cash flow is more difficult to manipulate than earnings and can be more representative of actual performance. It also tends to be much lower than earnings for most companies. Also on the negative side, business conditions were exceptionally favorable for many US companies over the past twelve months. For example, the war in Ukraine has disproportionately benefited US oil and gas producers and defense companies. Perhaps more importantly, there continues to be subtle lagging effects from stimulus. Although consumer spending on goods has moderated, spending on services such as international travel has not. There are signs the spillover from government spending will continue to diminish. As research from the Federal Reserve indicates , excess savings accumulated over the pandemic are close to being exhausted. Certain federal subsidies for Medicaid expansion expired in March. Also, the Supreme Court ruling against student loan forgiveness will result in interest accruing starting in September and payments due in October. In addition, the cost of credit for mortgages, auto loans, personal loans, and small and medium business loans has soared. Accordingly, certain credit metrics have deteriorated over the past 12 months and are likely to worsen with the further removal of stimulus. Examples include credit card debt , auto loans , and commercial mortgage-backed securities .

The depletion of savings, restrictive monetary policy, and removal of fiscal expansion underlie my view that a 5% expected return for the S&P 500 is generous. Even if 5% were accurate, an additional 1% of expected return does not seem like adequate compensation for the added risk above treasuries. These same considerations hold for investments in other types of equity or equity-like investments such as real estate and high yield bonds . Treasuries have a distinct advantage over stocks and other risky assets. If the US experiences stagnating growth, a mild recession, or a severe economic downturn, stocks are likely to perform poorly; whereas, inflation is likely to be mild at worst. The Federal Reserve has a mandate to achieve maximum sustainable employment. In the past, the Fed accomplished this by decreasing interest rates and purchasing long-term treasuries and other securities. During the pandemic, the Fed added $4T to its balance sheet and accounted for a significant share of treasury market volume. The employment imperative implies that the Fed would likely drive-up treasury prices again during a downturn and causes treasuries to act like a hedge. Other investors also expect the Fed to stabilize markets, and this amplifies the effect.

Investment Alternatives

Treasuries are not the only assets that benefit from high yields and potential hedging effects. For example, both high quality corporate and municipal bonds exhibit the same characteristics to varying degrees. High quality corporate bonds yield more but are unlikely to hedge as well during a downturn. For example, the Vanguard Long-Term Corporate Bond ETF ( VCLT ) has a yield to maturity of 5.5% vs. ~4% for TLT. Some bonds are likely to get downgraded and the spread between corporate bonds and treasuries is likely to widen during a severe downturn. Another factor of concern for corporate bond funds, particularly index funds, is they track market-weighted benchmarks. If a particular corporation issues more debt, then this company will represent a larger share of the index. This compounds the risk of downgrades and spread-widening. Lastly, covenants and features such as call options on corporate bonds become increasingly favorable to the issuer during economic expansion. An active fund might mitigate some of these issues; although, additional fees can also wipe out any benefits. Despite these issues, a long-term corporate bond fund might make sense as part of a tax-advantaged account if the US only experiences a mild recession or none. In a taxable account, high-grade municipal bonds may be a better alternative than both treasuries and corporates. For investors in the top income tax bracket who live in states and municipalities with high income taxes, such as New York City, holding high-quality, long-term, triple-tax-free bonds in a taxable account should result in a higher effective yield and retain many of the hedging benefits. In this case, purchasing non-callable, individual bonds near the par amount and holding to maturity may make the most sense to avoid both capital gains tax and transaction fees.

Thus far, the focus has been on long-term bonds; however, intermediate-duration treasury bonds, such as those in the iShares 7-10 Year Treasury Bond ETF ( IEF ) currently have higher yields and should experience some of the hedging benefits. Many 401k plans only have an option for investing in medium-term bonds. Although the interest rate sensitivity is lower and potential hedging upside more limited, considerations such as accessibility may dictate that these are the best choice. Lastly, short-term duration bonds and bills currently have the highest yields and would fare the best during protracted inflation and sustained high rates. For those living in high income tax states and municipalities, holding high-yielding, short-term ETFs, such as SPDR Bloomberg 1-3 Month T-Bill ETF ( BIL ), iShares Short Treasury Bond ETF ( SHV ), or Schwab Short-Term U.S. Treasury ETF ( SCHO ) in a taxable account should provide some tax benefits and rollover holdings automatically.

One last option for benefitting from high yields and hedging benefits are international government bonds. During the pandemic, many other governments and central banks around the world engaged in fiscal and monetary expansion. As a result of this and the war in Ukraine, many other countries are currently experiencing inflation and rising interest rates. International bonds have the potential advantage of currency diversification but face several drawbacks in practice. First, Canada and the US were among the first countries to start rising rates, and therefore, yields are higher in both than many other countries that started later. Not only does this limit how much other international bonds currently yield but also detracts from the potential upside from falling rates. Second, many of those with higher yields have structural problems, such as the UK, that may limit their ability to fight inflation and lower rates. Third, the US dollar usually appreciates versus most other currencies during economic downturns, and this offsets the possible diversification benefits. Lastly and like corporate bonds, foreign bond funds such as Vanguard Total International Bond ETF ( BNDX ) are indexed based on float, or availability. As a result, the countries that have issued large amounts of debt are likely to have higher weights in the index. Currently, Japan floats the most bonds in the international market and accounts for 15% of the index. Japan is one of the few developed countries that has avoided raising rates to lower inflation and has extremely low yields. For all these reasons, I think there are better opportunities available than international bonds.

In summary, the ~4% yield and Federal Reserve dual mandates make TLT an attractive asset to hold in a tax-advantaged account. Depending on individual circumstances, it may make sense to hold other investments that both have high yields and will hedge against an economic downturn in addition to or instead of TLT.

For further details see:

TLT: A High-Yielding Hedge