UBT - TLT: Bullish Ahead Of September Payrolls And The CPI Update

2023-10-04 00:08:44 ET

Summary

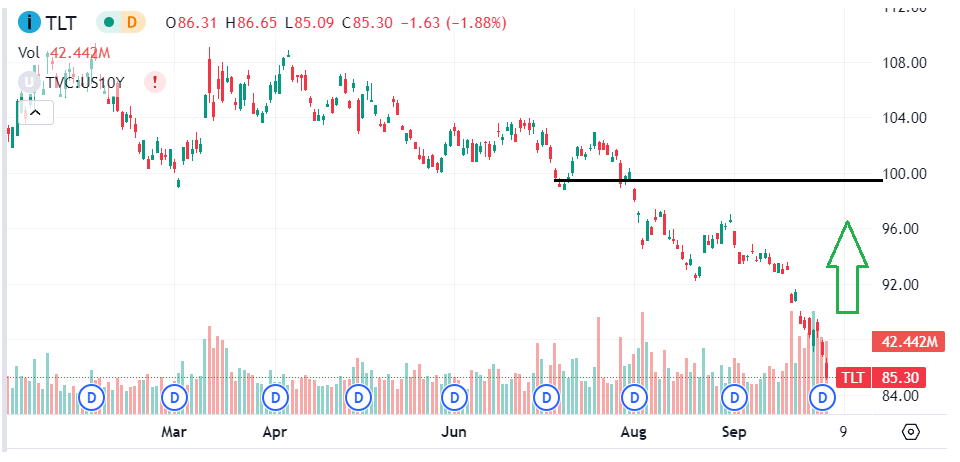

- Rising bond yields have caused the TLT to drop more than 50% from its high in 2021.

- We believe bonds are oversold and offer good value at the current level.

- The upcoming non-farm payrolls report and September CPI release could represent a catalyst as the market reprices interest rate expectations lower.

Rising bond yields have taken the market by storm with the 10-year and 30-year Treasury rate at the highest levels since 2007, approaching nearly 5%. The setup has been a disaster for the bond market, including the iShares 20+ Year Treasury Bond ETF ( TLT ), now down 50% from its high in 2021.

The fund technically tracks a basket of Treasury bonds with maturities greater than twenty years and represents a good bond benchmark as one of the most widely traded exchange-traded funds in the market. While the trading action has been poor, we see room to take the other side ahead of a rebound.

The potential for favorable indicators, between the September CPI as well as the payrolls report suggesting confidence that inflation will continue to trend lower could help build a consensus that the Fed is done with rate hikes. A pullback in bond yields from here would be bullish for TLT.

Why TLT is Down

The Fed's rate hiking policy in place since early last year, taking the Fed Funds rate from effectively zero to 5.5% at the short end of the curve explains much of the dynamic in rising yields at the long end of the curve.

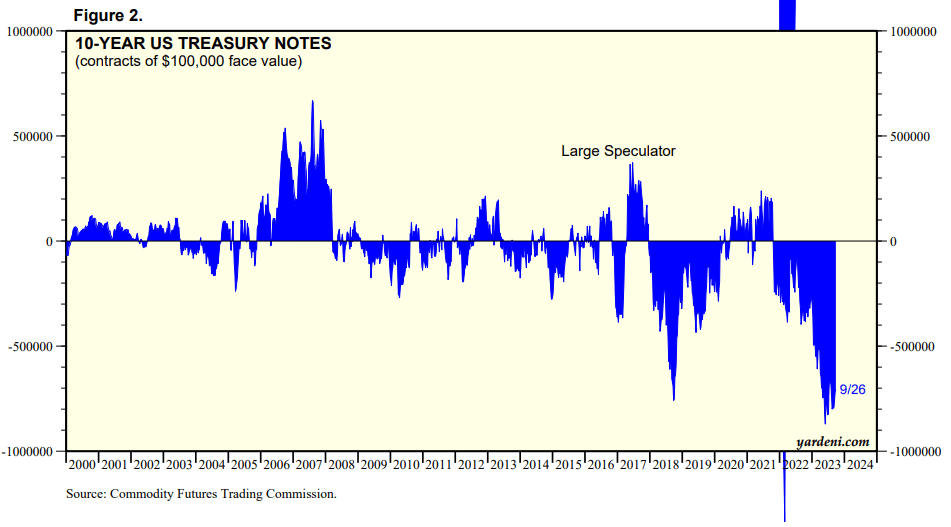

Still, what we're seeing now has evolved into more of a momentum-based selloff. Data shows that bond futures market positioning is at a record net short level , implying a bet on even higher yields going forward.

{kind=link}

As it relates to the macro backdrop, the interpretation is a view by some that "inflation remains a problem" and the Fed will need to keep hiking to bring the CPI down to the 2% target level.

This line of thinking received some fodder at the September Fed meeting with comments by Chairman Powell leaving the door open for another rate hike this year, noting the group remains data-dependent.

The "higher for longer" mantra was strengthened by the fabled dot plot forecast by Fed members revising the projection for the Fed Funds rates in 2024 to 5.1% compared to 4.6% from the June update.

All in all, it is fair to say bonds deserve to be higher compared to levels last year although we will argue that the move has been overextended.

source: Federal Reserve source: Fed

What Will The Fed Do Next?

The key point here is that there is some uncertainty regarding the actual direction of Fed policy even over the next few months. The difference between a continued "pause" or a rate hike over the next Fed meetings has significant implications for the broader bond market.

Importantly, that extra rate hike taking the Fed Fund Rates to 5.75% is far from certain with a case to be made that it won't happen. There is a deep divide in the market right now regarding where the Fed Funds rate will end this year.

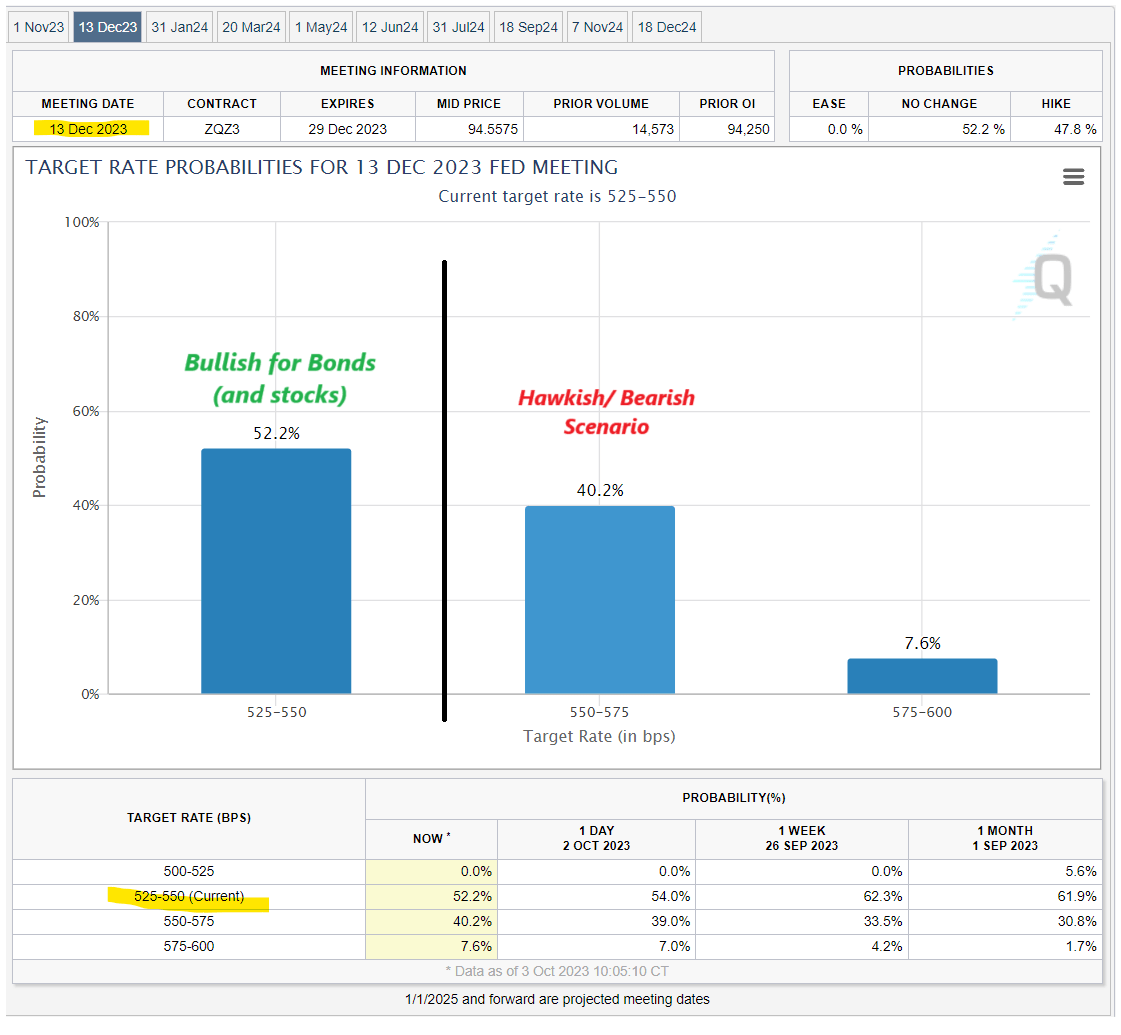

According to the CME FedWatch Tool , which extrapolates the probability for the Fed Funds rate move at each FOMC, there is currently a 52.2% chance the Fed ends the year at the December meeting with no change to the current 5.5% level, compared to a 47.8% odds for a hike.

The point here is to recognize that the interest rate expectations and the corresponding market probabilities are dynamic. Several factors can work to shift those probabilities.

A "good" or favorable data point suggesting lower-than-expected inflationary pressures between now and the next Fed meeting could be enough to keep the group on hold. If it becomes clear further rate hikes are unnecessary for the CPI to trend lower, this scenario would be particularly bullish for bonds and TLT with room for yields to correct lower.

This would be reflected in the December rate hike odds repricing lower and potentially even pulling forward the room for a rate cut earlier in 2024. This would also be a positive for stocks, although we'll leave that to a separate discussion.

On the other hand, bond bears are sort of hoping inflation surprises much higher with other macro data coming in exceptionally strong, forcing the Fed to turn even more hawkish. Here is the market-implied probability that a rate hike in December would become the consensus, as a further tailwind for bond yields to climb higher, and more downside in bond prices including the TLT ETF.

{kind=link}

Why Bonds Can Rally

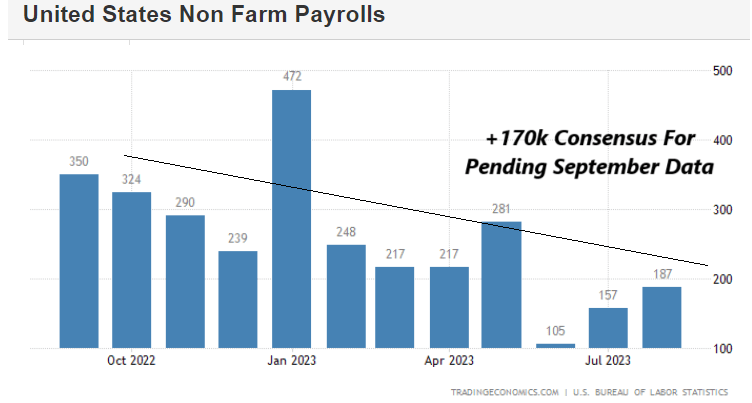

Two major indicators are coming out over the next few weeks that can help set the record straight. First up is the September non-farm payrolls report due out on Friday, October 6th. The current consensus is for 170k jobs added, representing a slight slowdown from 187k in August.

Our thinking here is that this otherwise "soft" figure confirms a gradual deceleration in the labor market as evidence monetary policy is working to cool demand-side consumer pricing pressures. For context, the average number of jobs added over the past year has been around 260k added per month meaning it's clear that the pace has slowed.

What might even be more encouraging is room for the unemployment rate to climb above 4%, based on a growing participation rate that was the theme in August.

This headline number returned to the highest level since 2021 indicating that the transmission of monetary policy to restrict economic activity within the credit cycle is working. We also expect wage growth to be subdued.

{kind=link}

In our view, it would take a "blowout" print higher implying the economy is exceptionally strong to raise an eyebrow at the Fed that the labor market trends are inflationary.

A miss to the downside on Friday with the payroll number a bit weaker than expected would be a very bullish backdrop for bonds because it pushes back on the need for the Fed to keep hiking and brushes aside concerns that inflation is accelerating.

If anything, bonds could react in a sort of "buy the news" dynamic, where any print is met with some market-wide short covering considering the recent weakness. We expect to see a rally in TLT here as part of a "short squeeze dynamic" against the excessive net short interest in the bond market.

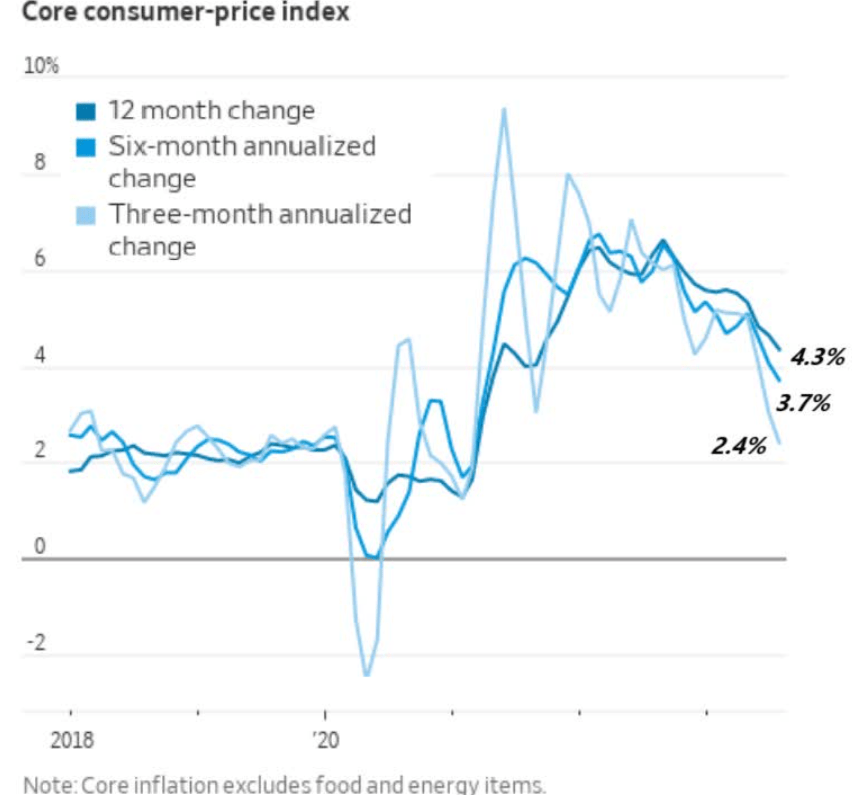

TLT bulls can also look forward to the September CPI report set to be released on October 12th. A lot of attention has been placed on the recent spike in oil prices, although the key here will be core trends. The September inflation update showed that the core CPI dropped to 4.3%, the lowest level in more than two years.

This is a very favorable development we expect to continue over the next few months because this side of the consumer price basket covers categories like housing, automobiles, and services that are more directly impacted by higher interest rates compared to energy prices.

{kind=link}

All indications are that core CPI which had been stubbornly elevated for much of the past year is finally turning. The Fed looks at three and six-month annualized levels which are well on their way to being at the target range. Again, the data has said they are data-dependent, and the cooling CPI is as important as it gets to confirm the trend is on track.

In terms of the headline rate, our call is that core can drag the broader index lower through 2024. Even as oil prices have climbed, we believe it would take oil significantly higher for it to begin driving a cost-pull inflationary wave. We can point to retail gasoline which remains under $4.00 a gallon as a national average as highlighted by the otherwise muted impact on the consumer price basket.

{kind=link}

TLT Price Forecast

Putting it all together, we see good value in bonds at the current level with room for TLT to rebound higher as interest rates stabilize and ultimately pull back.

Investors can pick up TLT with a compelling +4% dividend yield on a forward basis, with a good chance the fund will deliver a positive total return over the next year in our opinion. A scenario where the 30-year Treasury rate corrects to ~4.25% by year-end, implies TLT can reclaim the $100 as our initial target.

Into 2024, the possibility that the inflation converges toward the 2% target more quickly than currently expected, would provide the flexibility for the Fed to consider rate cuts based on anchored expectations. This could evolve irrespective of economic conditions within the soft landing scenario where the economy averts a recession.

A soft September payroll report and cool CPI can go a long way to reset the trajectory of Fed policy. TLT and bond market shorts covering within a broader repricing would kickstart a momentum trade to the upside.

In terms of risks, it would be more a concerning spike or re-accelerating of inflationary pressures that would be necessary to sustain a selloff in bonds. Factors such as the national debt, with supply and demand dynamics of Treasury bond issuances, also play a role in this market, but to a lesser extent.

The setup here is that bonds are oversold and the next move in prices is higher in our opinion. More aggressive traders can also consider the ProShares Ultra 20+ Year Treasury ETF ( UBT ) which is essentially a 2x leveraged version of TLT meaning double the risk as well as potentially double the upside return in percentage terms.

{kind=link}

For further details see:

TLT: Bullish Ahead Of September Payrolls And The CPI Update