BTI - Tobacco Stocks: Valuing Them Correctly Using Imperial Brands As A Case Study

2023-12-18 13:31:18 ET

Summary

- Valuing tobacco stocks using conventional methods (e.g. P/E, P/FCF, EV/EBITDA) can lead to overly optimistic expectations due to the known challenges of the cigarette industry.

- The article discusses an alternative, scenario-based valuation approach. Its main advantages are its simplicity and the comprehensibility of the conclusions that can be drawn from it.

- The method is illustrated using the example of Imperial Brands stock, a U.K. tobacco company known for its weak market position and lack of a meaningful smoke-free portfolio.

- Despite the company's weak position and the use of severely negative scenarios, IMMBY stock represents a solid investment opportunity.

Introduction

My regular readers know that I am a rather conservative investor who is wary of investing in companies that trade at very high multiples and have little or no short-term cash flow (i.e., growth stocks). Of course, this does not mean that I categorically exclude investments in growth stocks - quite the opposite - but I tend to stick to companies with long and ideally well explainable growth trajectories and strong current cash flows.

Tobacco companies are a different story due to their poor growth prospects. In many countries around the world, the number of smokers has been declining for decades and these companies rely on regular price increases to compensate for declining volumes. Despite this obvious warning signal, tobacco stocks are an important part of my portfolio. This is mainly due to their renowned profitability, generous returns for shareholders and their current unpopularity with many investors (e.g., sovereign wealth funds and major insurers , partly due to regulatory constraints ). Their unpopularity leads to weak share price performance, which in turn - quite counterintuitively - can lead to market-beating returns over long periods of time (e.g. as explained by Jeremy Siegel )

Therefore, in this article - as a sort of conclusion to my recent series of articles on tobacco companies - I will explain an alternative approach to valuing tobacco stocks using the example of U.K.-based Imperial Brands p.l.c. ( OTCQX:IMBBY , OTCQX:IMBBF ).

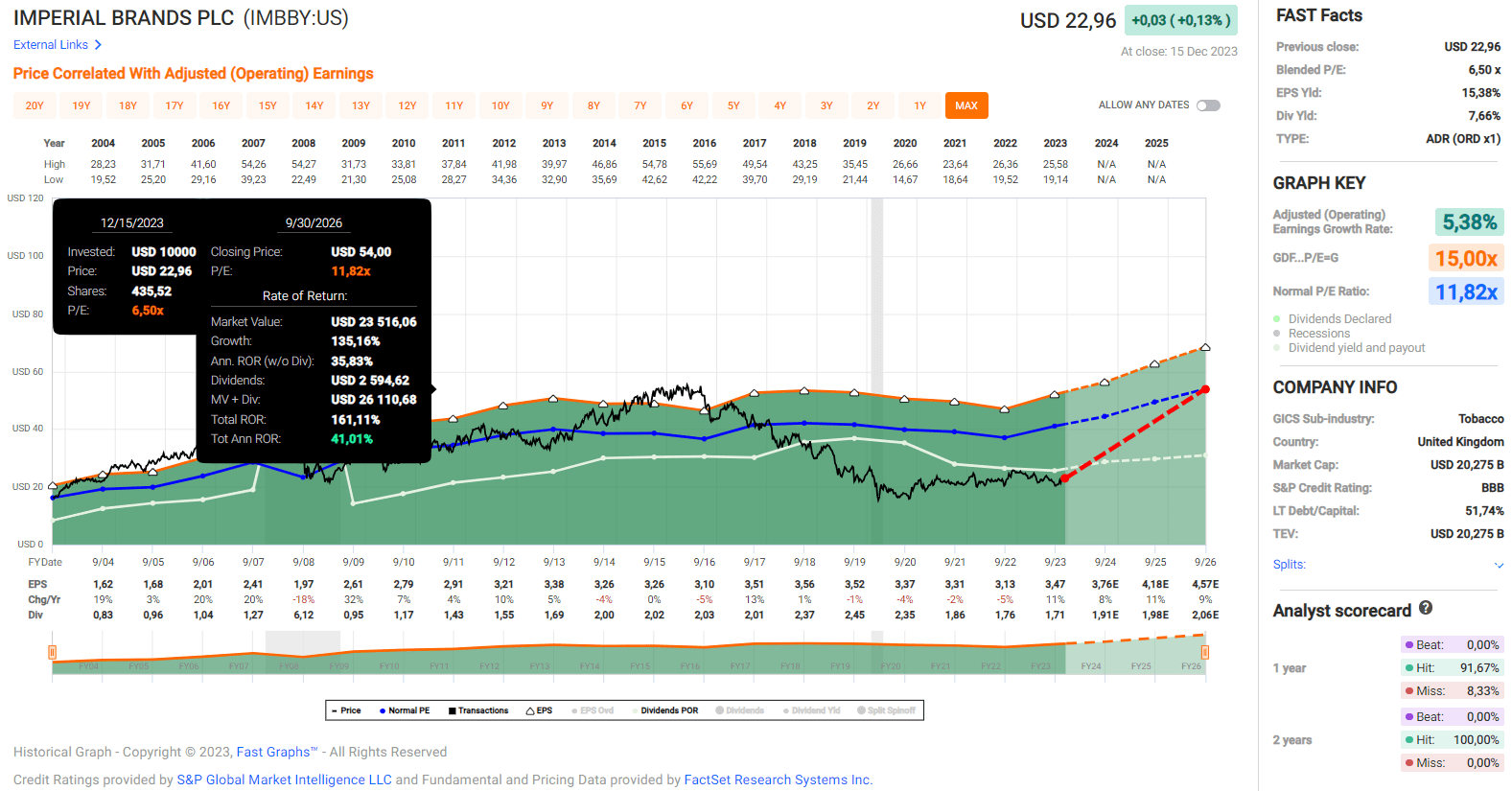

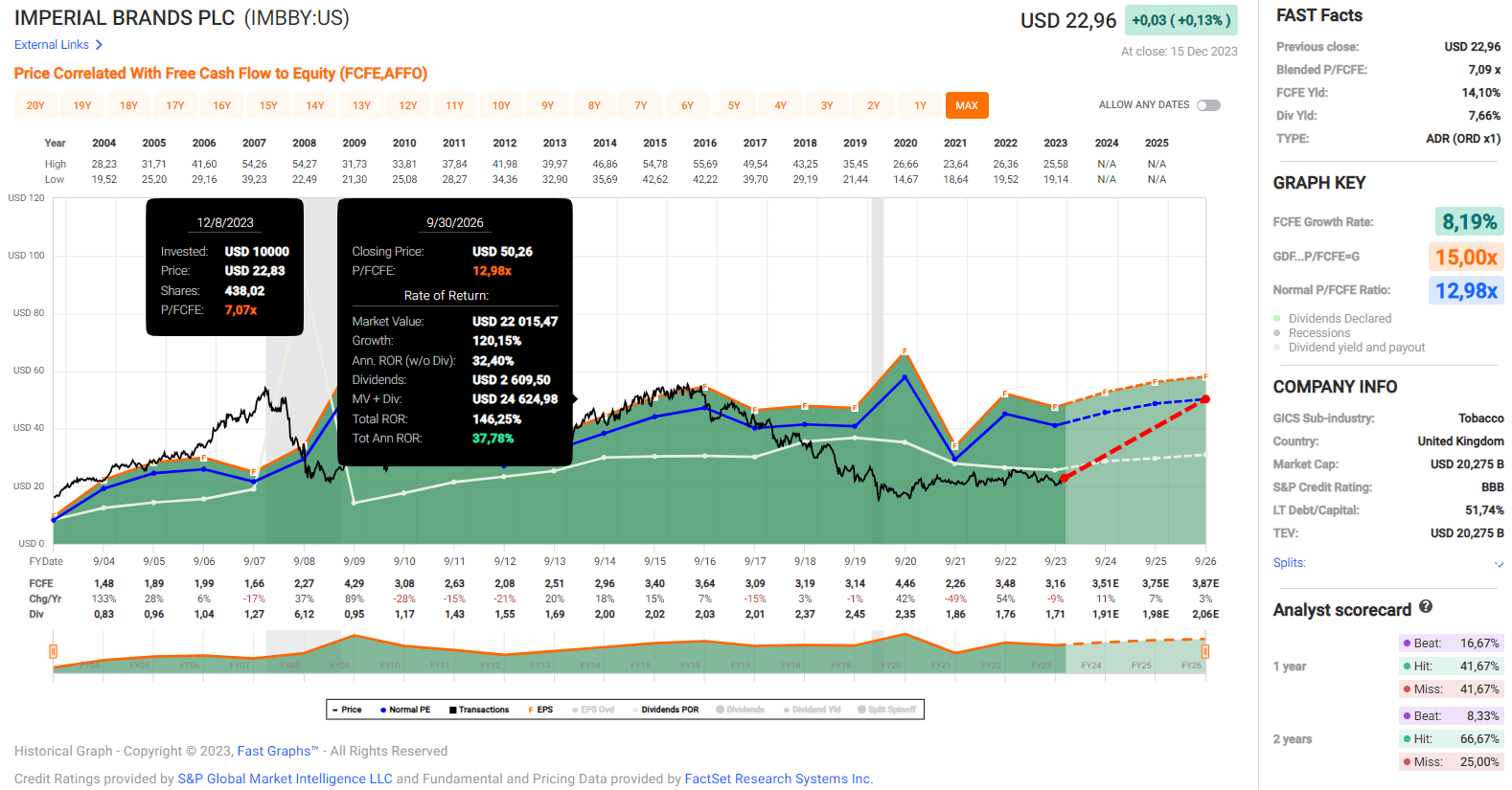

In my view, conventional valuation approaches, such as the price-to-earnings ratio (Figure 1) or the price-to-free cash flow ratio (Figure 2), can paint too rosy a picture and thus possibly lead to overly optimistic return expectations. However, there is a - fairly simple - solution to the problem in order to arrive at more realistic return expectations for tobacco stocks: inverse, or scenario-based valuation.

{kind=link}

Figure 1: FAST Graphs chart for Imperial Brands p.l.c. (IMBBY, IMBBF) stock, based on adjusted operating earnings (FAST Graphs)

{kind=link}

Figure 2: FAST Graphs chart for Imperial Brands p.l.c. (IMBBY, IMBBF) stock, based on free cash flow to equity (FAST Graphs)

What Is Inverse Valuation And Why Does It Make Sense For Tobacco Stocks?

The idea of inverse valuation came to me when I was working in risk management in the banking sector. Regulators mandate quite complex risk assessments, some of which, in a nutshell, are an estimate of the financial loss incurred with a given probability.

Such models essentially take into account market data from a specific period, apply statistical methods and arrive at a dollar (or other currency) estimate that can be related to a bank's tangible book value, for example. However, these methods rely on data from the past, which can be problematic. Take, for example, a value-at-risk ((VaR)) analysis of a bank's equity portfolio conducted in December 2019, which takes into account the daily volatility of asset prices over the last eight years (December 2011 to December 2019). What sounds like a reasonable time horizon would have led to a significant underestimation of what the global equity markets experienced in March 2020.

Although VaR approaches are still widely used, regulators are well aware of their shortcomings and their far from universal applicability and have therefore developed scenario-based - or inverse - stress tests, among others. The scenarios are oftentimes quite easy to understand, even from a layman's perspective. For example, the Federal Reserve's 2023 stress test included a scenario in which home prices fall by 38% over seven quarters (see, for example, my discussion of the latest stress test here ). These tests provide - in a very simplified way - an indication of whether a bank would collapse under these adverse stress scenarios.

At this point, you might ask what this has to do with the valuation of equities in general and tobacco stocks in particular?

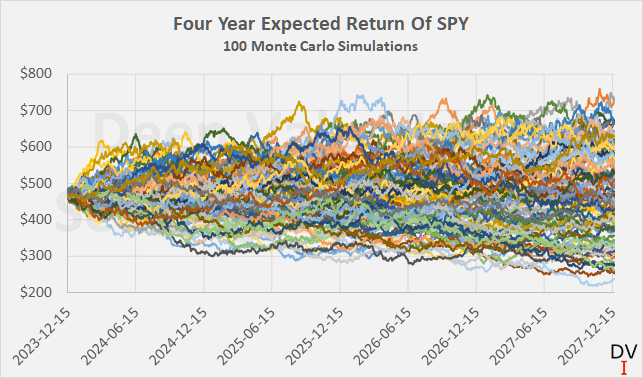

It's pretty simple. Conventional valuation approaches, such as the charts shown in the introduction, basically assume that the past is indicative of the future, which we all know is rarely the case. For example, consider Figure 3, which illustrates the increase in uncertainty of returns over time using 100 Monte Carlo simulations for the four year expected return of the SPDR® S&P 500 ETF Trust ( SPY ).

{kind=link}

Figure 3: Four year expected return of the SPDR® S&P 500 ETF Trust (SPY), 100 Monte Carlo simulations (own work, based on the daily closing prices of SPY over the last four years)

So instead of assuming that tobacco company stocks will return to their long-term average earnings and cash flow multiples, inverse valuations using scenario calculations can provide much more meaningful conclusions about whether the asset under study represents a good buying opportunity.

In this article, I will illustrate this valuation approach using the example of Imperial Brands p.l.c., a U.K.-based second-tier tobacco company that has suffered from significant management missteps, has no meaningful smoke-free portfolio and is likely to remain just that - a highly profitable cigarette company.

As an aside, simply ignoring the (potential) cash flow contribution of smoke-free products would definitely be too conservative an assumption for Philip Morris International Inc. ( PM ), which has the strongest portfolio of heated tobacco (IQOS franchise) and oral nicotine products (via Swedish Match ). British American Tobacco ( BTI , OTCPK:BTAFF ) expects its smoke-free portfolio to break even by the end of 2023, but it will likely take some time for the associated free cash flow to become meaningful. Altria Group, Inc. ( MO ) has a small oral nicotine franchise (e.g., on!), recently acquired NJOY Holdings (e-vapor), has begun development of its own heated tobacco device (SWIC, serving a small consumer niche ), and expects to commercialize heated tobacco products under the Ploom brand ( joint venture with Japan Tobacco). I recently compared the "Big 3" in a separate article .

Before I explain scenario-based valuation with the example of IMBBY stock, let's take a quick look at the company's current situation.

Imperial Brands p.l.c. – A Few Remarks

Imperial Brands shares are currently trading at approximately £18 on the London Stock Exchange, which equates to an ADR value of around $23 (ticker OTCQX:IMBBY ). As the company reports its earnings in pounds sterling, I will conduct my inverse valuation analysis in the reporting currency.

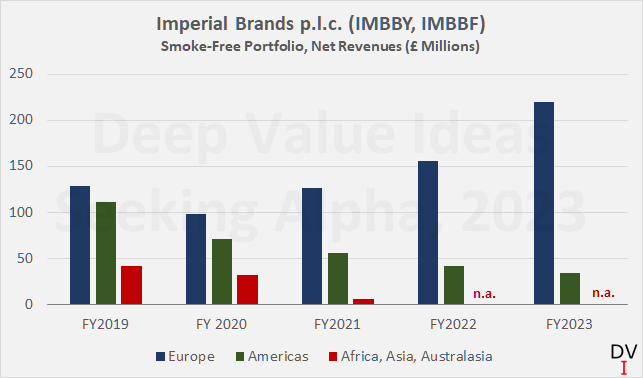

Imperial currently does not have a meaningful smoke-free portfolio and has even decided to discontinue its efforts in the Africa, Asia and Australasia segment last year (mainly Russia and Japan). Figure 4 clearly shows Imperial's poor performance in smoke-free products over the years, but at least the company is not wasting much money in this area. In fiscal 2023 (ended September 30), the company lost £156 million (4.0% of adjusted operating profit) on its smoke-free portfolio, and related sales accounted for 3.3% of total net sales (£265 million vs. £8.0 billion).

{kind=link}

Figure 4: Imperial Brands p.l.c. (IMBBY, IMBBF): Net revenues of the smoke-free portfolio (own work, based on company filings)

In fiscal 2023, Imperial generated free cash flow of around £2.6 billion, taking into account working capital movements, cash flows from derivatives, stock-based compensation, dividends paid to non-controlling interests and lease-related payments. With an average three-year free cash flow margin of around 31%, Imperial is slightly more profitable than its much larger rival British American Tobacco. In my view, £2.4 billion is a reasonable starting point for the ensuing scenario analyses, which is slightly less than the company's three-year average free cash flow.

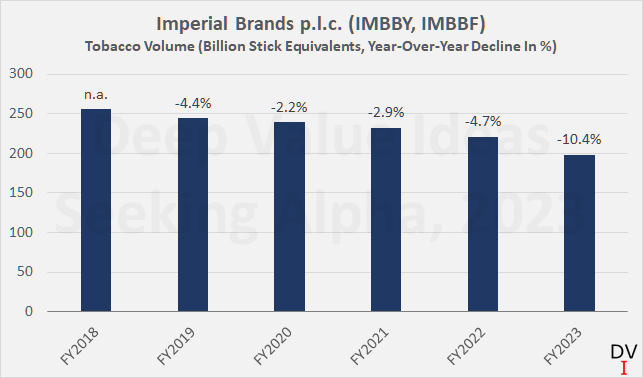

Like the three major tobacco companies, Imperial is also dependent on constant price increases in order to grow, or at least maintain its sales in view of the continuing decline in cigarette volumes (Figure 5). For the time being, Imperial's tobacco-related net revenue continues to grow (2.1% and 2.5% year-over-year in fiscal 2023 and 2022, respectively).

The recent accelerated decline in volumes is expected to slow somewhat due to inventory issues, the exit from Russia in April 2022 and inflation-related effects. However, I think it is important to recognize that smoke-free products are capturing more and more market share, creating an additional headwind for cigarette sales. For example, Altria management recently noted - for the first time - that cross category movement is a major driver of cigarette volume decline: 1.5 to 2.5 percentage points of the currently estimated overall U.S. industry decline of 8.5% (slide 16, Q3 earnings presentation ).

{kind=link}

Figure 5: Imperial Brands p.l.c. (IMBBY, IMBBF): Tobacco volume since 2018 (own work, based on company filings)

As the following scenario-based valuations are based on a discounted cash flow analysis, a value for the cost of equity needs to be determined. With long-term UK government bonds such as the 20-year gilt currently trading at 4.1% , a 5% equity risk premium seems a reasonable expectation. Of course, there are academic approaches to determine the cost of equity (currently 7.6% according to the Capital Asset Pricing Model ), but since return expectations are very personal and, in my opinion, depend on many factors other than the beta of the stock, I have resorted to my own hurdle rate of 9.1%.

What all of the following scenarios have in common is the expectation that Imperial Brands' management is not engaging in overly expensive transactions to build a smoke-free portfolio and is instead focusing on execution in its traditional cigarette business.

Let's now take a look at whether Imperial Brands' stock is a compelling investment opportunity based on several scenarios.

Is Imperial Brands Stock A Good Buy At $23?

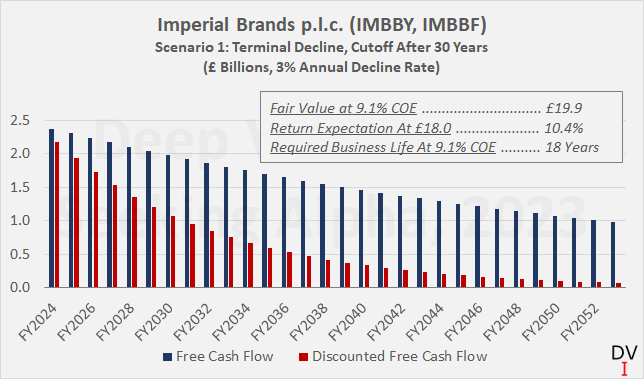

Scenario 1 – A Straightforward Terminal Decline, Imperial Goes Out Of Business After 30 Years (Or Faster)

Due to the recent accelerated decline in combustible volumes, it is becoming increasingly difficult for Imperial to grow its sales. At some point, sales and therefore free cash flow will peak and then fall.

Although the cigarette business is a notoriously profitable business that relies on few fixed assets and maintenance investments, fixed costs (below a certain level of sales) become an increasingly significant headwind that weighs on free cash flow. In this scenario, I expect the company to report a steadily declining free cash flow and to go out of business after 30 years. Of course, this might be unrealistic considering that a certain percentage of current smokers will keep their habit no matter what. However, considering that British American Tobacco recently reported a change in the economic life of its U.S. cigarette brands from an infinite period to a 30-year period (see my discussion here ), I still think this scenario is worth considering.

Figure 6 shows the profile of Imperial's annual free cash flow (blue bars) and the value of cash flows after discounting at 9.1% (red bars). The series is terminated after 30 years, but because the discounted cash flows far in the future are hardly significant, Imperial remaining in business after 2053 would not have a material impact on the present value of the investment.

{kind=link}

Figure 6: Imperial Brands p.l.c. (IMBBY, IMBBF): Discounted cash flow valuation using a 3% annual rate of decline and discontinuation of business after 30 years (own work)

The beauty of this scenario-based approach lies in its simplicity and the concreteness of the conclusions.

It is easy to see that if this scenario holds, Imperial shares are 10% undervalued today (fair value £19.9 or $25.2). Put another way, a 130 basis points higher cost of equity (10.4%) would be a realistic return expectation buying Imperial Brands stock today under this scenario - not bad for a company in decline.

But we can rephrase the conclusion further - if we assume Imperial goes out of business after just 18 years, the stock is still somewhat undervalued at the above cost of equity. In other words, Imperial's free cash flow could fall to zero as early as fiscal 2042 - how realistic is that?

Scenario 2: Accelerating Revenue Decline

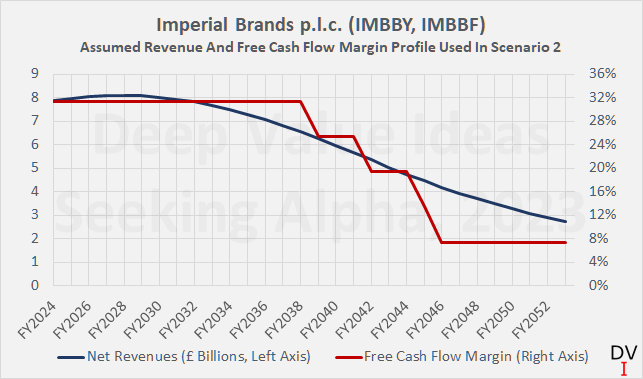

Admittedly, the first scenario might be too simplistic, even considering that Imperial's sales are still growing, albeit slowly. In the second scenario, I have modeled a decline in the revenue growth rate of 40 basis points per year, which means that net revenue will peak at £8.1 billion in fiscal 2028 and decline from there on. It should be noted that the actual decline in revenue accelerates as the 40 basis points are subtracted from the previous year's growth/decline rate. Admittedly, this might seem too conservative - especially given that the industry decline is likely to level off at some point. Therefore, I have set a floor of -6% as the lowest possible annual rate of decline, which in this scenario is reached in fiscal 2044.

Recognizing that Imperial may not be able to adequately downsize the business and fixed costs, I have factored in a 600 basis points decline in free cash flow margin following a revenue decline to £6.5 billion, and second, third and fourth declines by 600 basis points each at thresholds of £5.5 billion, £4.7 billion, and £4.2 billion, respectively. These assumptions result in the revenue and free cash flow margin profiles shown in Figure 7.

{kind=link}

Figure 7: Imperial Brands p.l.c. (IMBBY, IMBBF): Revenue and free cash flow margin profile used in scenario 2 (own work)

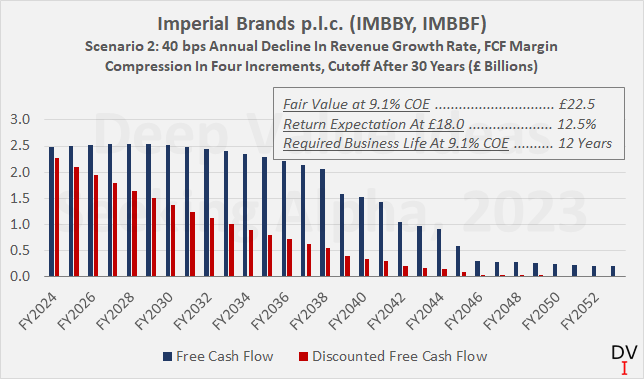

Using these data as inputs to a discounted cash flow model results in the cash flow profiles shown in Figure 8 and a fair price of £22.5 (approx. $28.50) for IMBBY stock, again assuming that the company ceases operations after 30 years.

Looking at this outcome from a different angle, free cash flow could fall from the fiscal 2035 level to zero next year, for the stock to be fairly valued today at a cost of equity of 9.1%. This means that as long as the free cash flow generated is returned to shareholders in the form of dividends or share buybacks, Imperial could close its doors after just 12 years. Or in this scenario, if Imperial stock is purchased at today's price, a cost of equity of 12.5% would be a reasonable expectation, assuming the company stays in business for another 30 years.

{kind=link}

Figure 8: Imperial Brands p.l.c. (IMBBY, IMBBF): Discounted cash flow valuation using the revenue and margin profile from Figure 7 (own work)

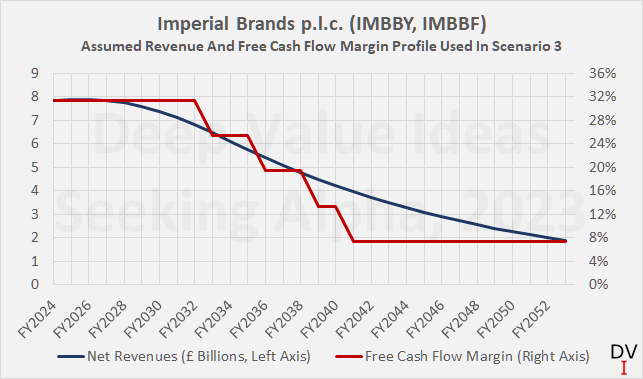

Scenario 3: How Fast Could Imperial's Revenues Fall For The Stock To Still Represent Good Value Today?

Finally, let's take a look at the extent of the revenue decline Imperial could experience before the stock could be considered a "value trap". Figure 9 shows the profile of revenue and free cash flow margin assuming a 70 basis point annual decline in the revenue growth rate. Again, this accelerating decline is applied until the floor of -6.0% is reached (in this example in fiscal 2035), as is the decline in margin at the revenue thresholds noted above.

{kind=link}

Figure 9: Imperial Brands p.l.c. (IMBBY, IMBBF): Revenue and free cash flow margin profile used in scenario 3 (own work)

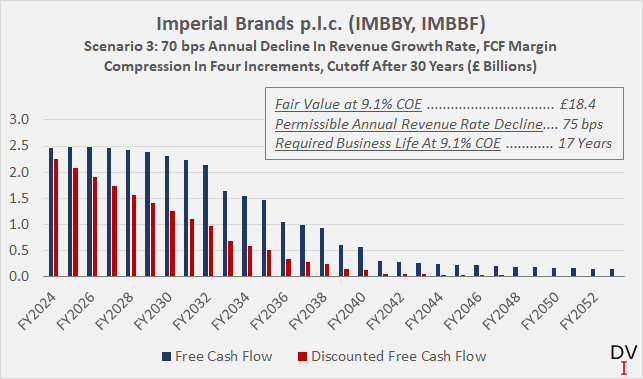

The resulting cash flow profiles are shown in Figure 10 and confirm that the stock is still slightly undervalued today, even under these pessimistic assumptions. Rephrasing the conclusion, Imperial's decline in sales could accelerate by 75 basis points each year until the terminal decline rate of -6.0% is reached in fiscal 2034, for the stock to be currently fairly valued at a cost of equity of 9.1%. Here, too, it is worth asking how realistic such a scenario is.

{kind=link}

Figure 10: Imperial Brands p.l.c. (IMBBY, IMBBF): Discounted cash flow valuation using the revenue and margin profile from Figure 9 (own work)

Conclusion

Conventional valuation methods, which generally assume that the past is an accurate reflection of the future, can lead to overly optimistic return expectations. This is particularly true for the shares of tobacco companies such as Altria Group, British American Tobacco and Imperial Brands, which derive most (or all) of their profits from the sale of conventional cigarettes. It is well known that the cigarette industry has been in decline for several decades. Therefore, and because the price elasticity of demand is increasing (which limits the scope for price increases), the growth prospects are rather poor.

In this article, I have presented an alternative, scenario-based approach to valuing tobacco stocks using Imperial Brands as an example. The beauty of this approach lies in its simplicity and the comprehensible conclusions that can be drawn from it. These models can be created in Microsoft Excel or similar spreadsheet programs by anyone with a basic knowledge of cash flow discounting (an overview can be found here ). Investors can easily formulate their own expectations to determine whether a stock represents good value in a given scenario. Realizing that a stock is cheap even under a significantly adverse scenario increases conviction in an investment, as in most cases things turn out far less negative than expected.

It has been shown that even in a very pessimistic scenario, Imperial Brands stock still represents good value at its current price of £18 ($23). In all the scenarios discussed in this article, it was assumed that Imperial would go out of business after 30 years. However, it was found that even with a much shorter remaining life (12 to 18 years), the stock still represents a solid investment opportunity. Conversely, if Imperial stays in business for another 30 years (or longer), the return prospects are really solid indeed (cost of equity of 10.4% or more) - despite the modeled steady decline in revenues.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Tobacco Stocks: Valuing Them Correctly Using Imperial Brands As A Case Study