TKOMF - Tokio Marine: Volatile Profitability But Continued Upside Potential

2023-04-09 03:48:33 ET

Summary

- The oldest insurance company in Japan continues to perform.

- At present, there are more tailwinds than headwinds for the industry.

- A buy for income investors looking for broad global exposure in insurance, the stock still has room to go higher.

Tokio Marine’s vision is "to be a good company", and that it has been for a century and a half now. But not just good, the group is a true blue blood in Japanese insurance. Japan’s first non-life insurer, it was underwriting in London, Paris and New York only a year after its founding, though earnest expansion into Europe and the US started in more modern times about 15 years ago . By that time, its specialty insurance business in emerging markets was already going strong. Today, Tokio Marine earns more than half of its profit from international subsidiaries which manage risk largely uncorrelated with domestic insurance.

Despite the uncertainty in the world economic outlook, the high interest rate environment — and the improved investment and underwriting returns as a result — augur a positive year ahead for the insurance industry. Tokio Marine should be able to improve profitability in the near future and, as it always has till now, should continue rewarding its shareholders handsomely.

Financial performance

The latest 3Q FY2022 results were solid: on the back of price hikes in foreign markets, net premiums increased by 9.6% and life insurance premiums by 3.6%, excluding foreign exchange gains. For reference, global premiums have been forecast to grow 6.1% in 2022 on the back of ongoing hardening, or tightening of underwriting practices by risk-conscious institutions, in non-life lines.

{kind=link}

Tokio Marine

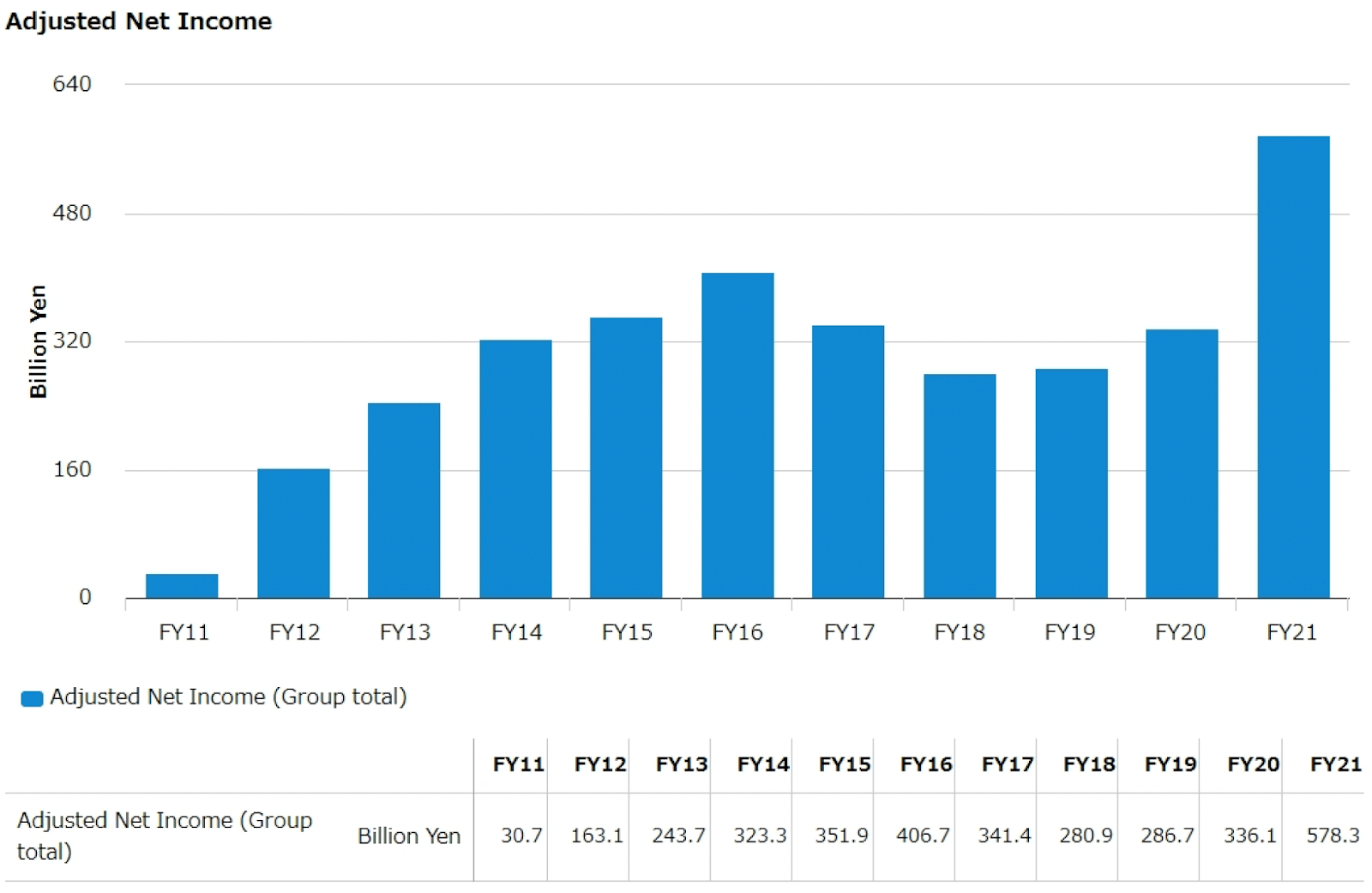

Group-level adjusted net income came in line with expectations, and no revision was made to the full-year projection of ¥400b (ROE 12.5%). That will be a downgrade from FY2021's record ¥578b (ROE 14.4%), but it would also be more fitting with the overall track record of the past decade. The medium to long-term target is to keep profit permanently above ¥500b (ROE 12%) through organic growth in earnings of over 5%.

{kind=link}

Tokio Marine

Achieving sustainable profitability hinges not only on high-growth emerging markets but also reforming stale products including the loss-making fire insurance in Japan, although the current inflation in claims costs makes it difficult. Fortunately, the group’s financial health allows for such challenges to be pursued at a comfortable pace. The total debt is exceeded by cash and amply covered by operating cash flow. Investment grade ratings — A+ from S&P and Aa3 from Moody’s — strengthen the case.

Market

For an industry that is as old as society itself, insurance is still growing and is about to surpass a major milestone of $7t in global premiums . More than 50% of the latter comes from the top three markets, and while Tokio Marine has significant operations in two — the US and Japan — it is apparently outcompeted in China , the largest emerging market.

Operating network: Japan and 46 other countries

Based on non-life insurance premiums as of March 2022 (Tokio Marine)

The performance is stable in Japan, the homebase, but the group is much more animated about growth prospects in the US and Europe. Still, it is in the emerging markets where most of the growth is happening for both Tokio Marine and the industry as a whole. India , for example, where the group sits just outside the top ten insurers, is expected to become the fastest growing market over the next decade.

Strategy

Tokio Marine may be old but it is not old-fashioned. And this is evident not only in the way it focuses on emerging markets and high growth sectors, but also in the way it approaches management practices. Unlike a traditional Japanese organization, it eschews the strict hierarchy of uniformly Japanese directors. The globally minded management structure leverages local talent and is more responsive to local needs.

Mid-Term Business Plan 2023 (Tokio Marine)

In another effort to remain relevant, the group has been adopting the latest technological innovations to measure and predict risk. By feeding proprietary data to machine learning algorithms , it produces risk detection and mitigation solutions for domains such as mobility, disaster management and healthcare.

Tokio Marine is also opportunistically tapping into other research spearheaded by specialist firms or startups . Acquiring GCube has made it capable of underwriting renewable energy projects; its latest investment in Axelspace will enable it to develop new products for the space market.

Valuation

After a sprightly debut on the Tokyo Stock Exchange in 2002 (TSE:8766), Tokio Marine fell into an extended lull in the aftermath of the financial crisis and re-started its upward trajectory only in 2012 gaining more than 300% since then. On February 13, the price hit its highest point ever of ¥2.90k.

A good portion of total returns have been contributed consistently by dividends — which have been growing every year since listing. An increase of 18% is expected in FY2022 which will result in a dividend of ¥300 per share (before last October’s stock split ). The trailing yield is 3.9% which puts Tokio Marine in the top quartile of Japanese dividend payers. Dividends aside, the group also buys back its shares regularly — every year since FY2016; up to ¥100b was approved for FY2022.

{kind=link}

Tokio Marine

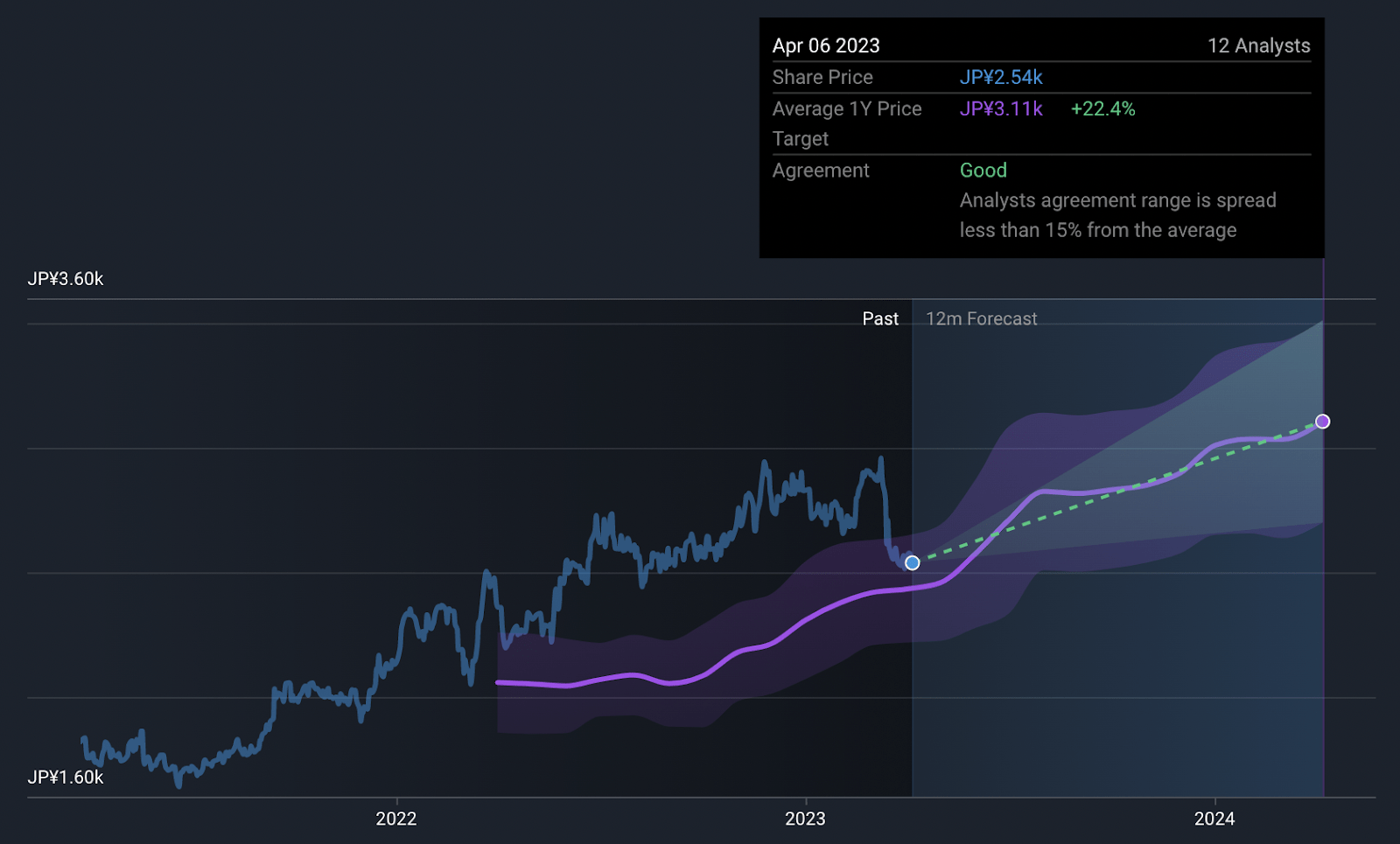

Valuation wise, Tokio Marine looks slightly expensive relative to both the Japanese insurance peers and competitors elsewhere. OTC-traded TKOMY is currently selling at a trailing P/E of 16.04 versus the Financials sector median of 9.44. Allianz ( OTCPK:ALIZY ) and Chubb ( CB ) — among other stocks that Tokio Marine often likes to compare itself against — are also marginally cheaper at 13.36 and 15.62 respectively. Analysts, however, expect the share price to rise about 22.4% in a year’s time to about ¥3.11k.

{kind=link}

Simply Wall Street

Risks

Tokio Marine believes that being geographically diversified is a natural hedge against systematic risk. However, global expansion brings about a lot of additional exposure too. Like all others, Tokio Marine has inflation to worry about, its persistence and lingering effects. The present forecasts of economic growth look especially inauspicious for the developed markets which the group has been pouring resources into. The short and medium-term impact of the war in Ukraine might affect earnings from niche specialty insurance.

Conclusion

Tokio Marine ticks many boxes as a high-quality stock with a good dividend that is growing continually. To be sure, lowering volatility in profitability is a work in progress. Higher interest rates will help boost returns in the immediate future. More importantly, the company is working toward more sustainable solutions. In addition to AI optimized operations, new sources of revenue may be on the horizon as the group expands to cover businesses such as renewable energy and space.

For further details see:

Tokio Marine: Volatile Profitability But Continued Upside Potential