TOELF - Tokyo Electron: Growth Should Recover But Shares Are Now Reasonably Valued (Downgrade)

2023-09-01 13:12:30 ET

Summary

- Tokyo Electron's revenue is influenced by the size of the wafer fabrication equipment market, which is expected to recover in the next two years.

- The company continues to invest aggressively in R&D, has a strong balance sheet, and its financial results are expected to start recovering soon.

- While we continue to like the company's long-term growth prospects, we see shares trading close to fair value and are therefore downgrading our rating to 'Hold'.

The last time we covered Tokyo Electron ( TOELF ) in November 2022 we remarked that despite the weak guidance the company was providing for the second half of FY2023, and shares remained cheap. Since then, shares have greatly outperformed the market, and we remain optimistic about the company and its long-term growth potential.

Seeking Alpha

As a major vendor of semiconductor fabrication tools, its revenue is significantly influenced by the size of the wafer fabrication equipment market (WFE). Its specialty is etch, deposition, and cleaning equipment, with its main customers being chipmakers such as Intel ( INTC ), Taiwan Semiconductor ( TSM ), Micron ( MU ), and Samsung ( SSNLF ). Estimates are that the WFE market size in 2023 will be about $70 billion to $75 billion, but that it should significantly recover in the next two years. The WFE market is expected to reach a total of around $200 billion when combining the years 2024 and 2025. According to the company, one of the main drivers of this recovery is the server market, which is expected to grow at an annual rate of ~8%. Tokyo Electron also expects the recovery to be more pronounced in 2025 compared to 2024.

Additional reasons to remain optimistic include growth in power semiconductors, especially for electric vehicles, and other semiconductors supporting the digital economy, including GPUs for AI applications. Tokyo Electron recently announced new etching technology for 400-layer level 3D NAND channel hole applications, and the company also shared that the adoption of wafer bonding technology has accelerated.

Q1 2024 Results

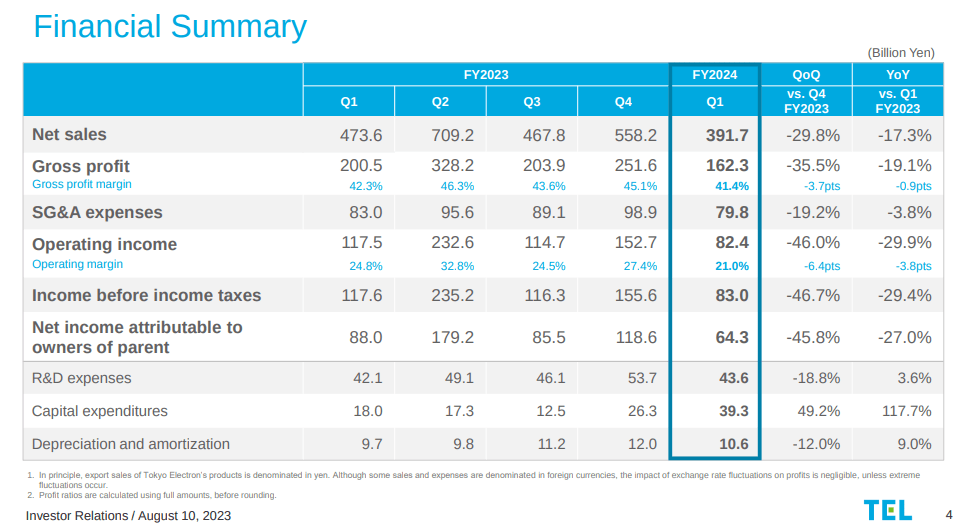

In the first quarter of 2024 , the company generated sales of ¥391.7 billion, which represented a 29.8% decline from the previous quarter. Gross profit was ¥162.3 billion, a 35.5% decrease from the previous quarter, and operating income was ¥82.4 billion, a 46% reduction from the previous quarter. Net income was ¥64.3 billion, a 45.8% decline from the previous quarter. Weakness in the WFE market is clearly impacting the company's revenue and profitability, but expectations are that the recovery should start soon.

Tokyo Electron Investor Presentation

{kind=link}

Financials

Despite lower earnings, the company continues to aggressively invest in maintaining a leading technological position. Tokyo Electron increased R&D spending in the quarter, as the company continues to bet that R&D investments will drive future growth.

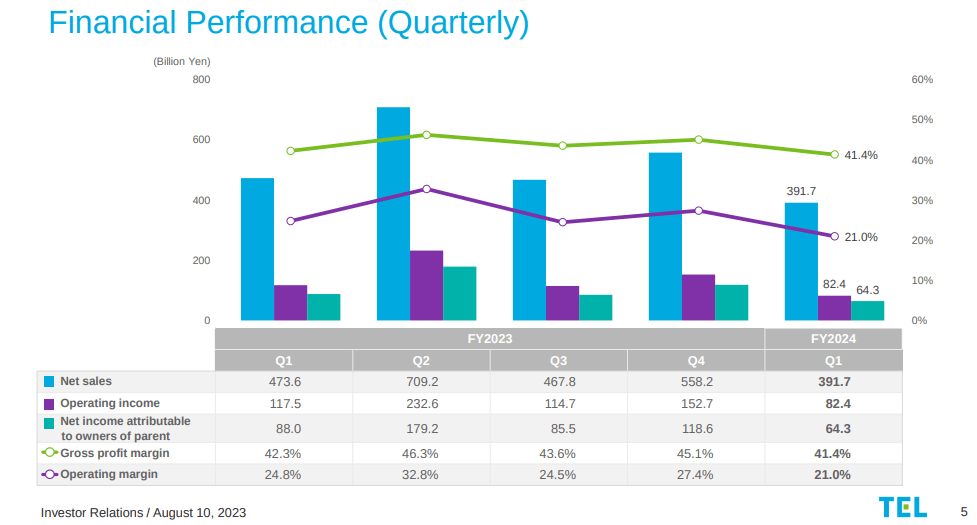

The company continues to have a very strong balance sheet, with cash and cash equivalents of ¥401 billion. This represented a reduction of ¥72.0 billion from the previous quarter due to the dividend payment, tax payments, and share repurchases. As can be seen in the slide below, this quarter's financial performance was the weakest in a long time. Still, we are impressed that, despite the tough operating environment, the company continues to deliver operating margins above 20%.

Tokyo Electron Investor Presentation

{kind=link}

Dividend

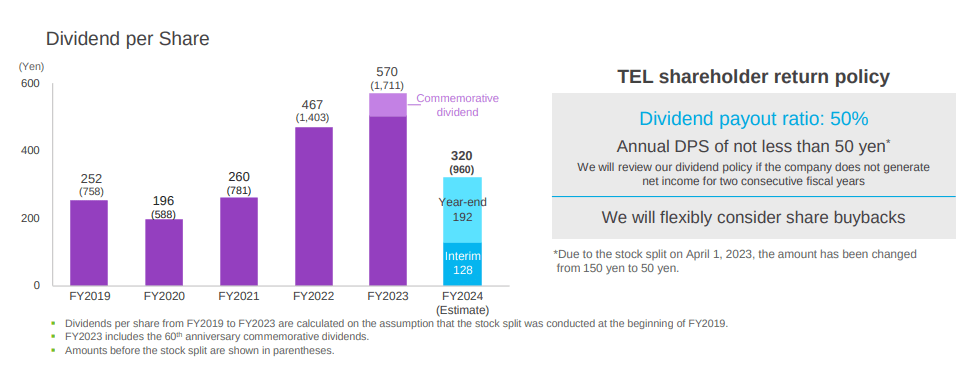

Tokyo Electron can be an interesting option for dividend investors, but they should take into consideration that the dividend varies very significantly depending on the company's recent financial results. The company targets a payout ratio of 50% of its earnings, which means the dividend tends to vary considerably from year to year.

Full year dividends are expected to be 320 yen per share, which at current prices means that the forward dividend yield is ~1.5%. The dividend will probably be significantly increased once the company's profitability returns to more normal levels. In addition to the dividend, the company has been returning capital to shareholders through share repurchases. The slide below shows the dividend per share for the last few years.

Tokyo Electron Investor Presentation

{kind=link}

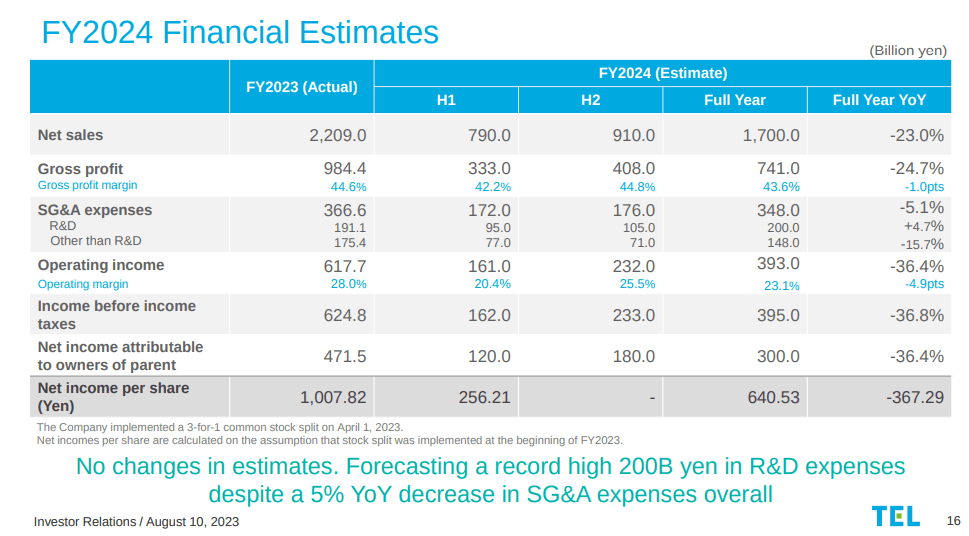

The good news is that it seems things are already improving for the company, with CEO Toshiki Kawai mentioning during the most recent earnings call that they see a gradual increase in net sales and gross profit margin.

So slightly product mix will be changed that's one thing. In the second half of this year; those positive factors will be increasing. Therefore you can see higher improvement of the gross profit margin along with the gradual increase of the gross net sales. Yes, we expect the increase of the net sales. Accordingly, we can see the increase of the gross profit margin as well. Thank you very much.

Growth

Tokyo Electron has an outstanding revenue growth track record, even if that growth has a cyclical component. The average quarterly year-over-year revenue growth for the last ten years is ~14%, which we find quite respectable. The company believes it can continue growing at a rapid pace and has previously said that it aims to reach more than 3 trillion yen in net sales by FY2027, which is ~$20 billion.

A key segment the company believes will keep the semiconductor industry growing is servers, which is estimated to grow with a CAGR of ~8% between 2023 and 2027. In particular, the number of servers dedicated to AI applications is forecasted to grow very significantly.

Tokyo Electron Investor Presentation

Valuation

The trailing twelve months GAAP P/E is ~22x, but the forward P/E is more than 30x due to the expected decline in profitability for FY2024. Still, this is normal in this industry and for Tokyo Electron in particular, and we believe earnings will return to more normal levels soon. We currently view shares as reasonably valued, and we are therefore updating our rating to 'Hold' from 'Buy' previously.

Tokyo Electron Investor Presentation

{kind=link}

Risks

There are several risks to consider with Tokyo Electron, including the fact that a significant percentage of its sales are to China. Sales to China rose to 39.3% due to significant WFE spending on matured nodes. Investors should also consider that the WFE market tends to be very cyclical. For example, the WFE market is expected to experience negative growth in calendar 2023, somewhere between -25% to -30% growth compared to calendar 2022. Fortunately, a recovery and positive growth are expected in 2024 and 2025.

There is also technological risk, with the company at risk of being disrupted by some of its competitors. This is mitigated by significant R&D spending by the company to remain on the cutting edge of technology.

Conclusion

Tokyo Electron delivered solid quarterly results given the current tough operating environment. Shares have appreciated significantly since our last article, and we now consider the company to be more reasonably valued. We continue to like the company and its long-term growth prospects but now find the valuation less attractive. The company has also become more reliant on sales to China. For these reasons, we are downgrading our rating to 'Hold' from 'Buy' previously.

For further details see:

Tokyo Electron: Growth Should Recover, But Shares Are Now Reasonably Valued (Downgrade)