TMRAY - Tomra: An Update On Recycling Still A Hold

2023-07-05 03:11:29 ET

Summary

- Tomra, a world leader in reverse vending and recycling, has seen significant top-line growth of almost 30% YoY in Q1 2023, despite being 7% more expensive than three months ago.

- The company is expected to continue its revenue growth at around 15%, with EBITA margins expected to improve due to new contracts and record-high backlogs in various segments.

- Despite trading at a premium, Tomra is considered an attractive investment due to its market dominance and potential growth in the recycling industry, a sector considered to be in its infancy.

Dear readers/followers,

I provide periodic updates on companies even if their valuation for the past few months hasn't really shifted much. It's been almost 3 months since my last article on Tomra ( TMRAY ). While this company has valuation-related issues, meaning it's chronically expensive and unlike to drop significantly in the near term.

The question becomes if the company isn't attractive at these levels, around 160-178 NOK/share, and whether it's time to start loading up on a world leader here.

There are reasons why you could make very decent returns here, even if you elect to "go in" at what is a relatively high valuation. Let's look at what we have going for us with the company, despite that it's 7% more expensive now than when I last wrote about the business.

Tomra - Appeal from reverse vending

Q1 2023 is the latest report we have for Tomra, and trends here were positive. The company saw significant top-line growth of almost 30% during the first quarter YoY. On a constant FX, the company's various segments saw growth of over 15%, with 17% on a group-wide basis.

This also came without any sort of significant margin decline. Gross margins remain at around 40%, with collection margins and recycling/food margins going up as well - although we saw a corresponding increase in operating expenses as well. These expense increases weren't, for the most part, driven by unfavorable costs or lack of cost control, but by significant business expansion.

EBITA was up 17%, EPS was slightly down, and cash flow was at around 500 MNOK. The company retains a very appealing backlog in all segments, and order intakes were very strong. While we shouldn't expect wonders in the margin or revenue side, we can at least expect a continuation of the positive margins and trends - which should keep the company going upward. Here are the specifics for Q1 2023.

{kind=link}

The company's business fundamentals and "basics" remain attractive here. The company continues to target revenue growth at around 15%, and I expect this to be maintained.

{kind=link}

The one metric that is far from its target is the EBITA margin - though with new contracts now being handled for the next few years, the margins will improve, and overall backlogs for the various segments are at record-high levels. Also, in key segments like collection and recycling, which are the company's core segments, margins are already at 17-18%.

The company's growth vectors are what is interesting to me long-term, beyond the obvious appeal of its legacy dominance. The Food segment in particular is one I expect great things from - and margins here are still at a negative level, with other portions of the financials improving.

The company's fundamentals are a non-issue. With a debt maturity profile with no significant maturities until 2024-2025, and even then easily coverable by credit and cash, Tomra can expand and plan as it needs to.

The outlook for the company's various markets is positive. In collection and recycling, positive momentum is assumed to continue - albeit normalizing from the high 2022 levels. However, it's important to remember that there is a "natural" move to recycled materials and tech, and this push is unlikely to do anything except grow. The company is also preparing to enter entirely new markets in the collection.

The need for automation in the food segment is creating opportunities in the medium to long term - in processed food products, demand is good and Tomra expects good trends from here.

On a high level, inflation isn't going anywhere - and cost inflation is the key factor that we want to keep an eye on with regard to Tomra. Like any company, the business is raising prices and executing measures to make sure that margins are not lost - but in the end, I consider it likely to see some pressure on a forward basis. On an overall basis and generalizing in broad strokes, Tomra is a net beneficiary of the weak Scandinavian FX, including the weak NOK - because portions of its cost base are NOK-based. This means EUR/USD advantages.

However, in the end, Tomra is one of the most qualitative businesses that I review. The company makes close to a double-digit net margin from recycling and is profitable to an almost chronic degree despite the increased overall cost of capital.

{kind=link}

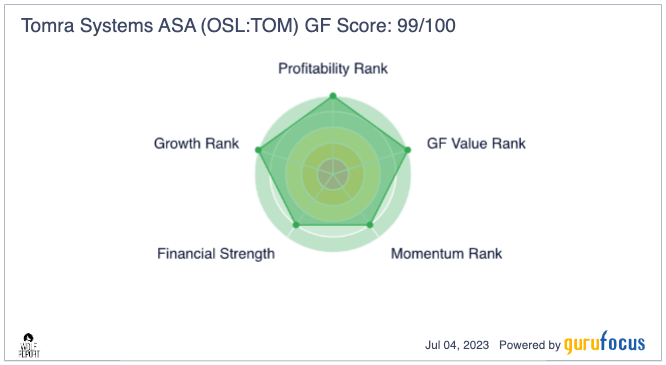

In my work, I use GuruFocus as one of the sources for data and tables. The service collects a company's appeal in a "GF Score", combining finances, profit, growth, Value, and momentum in a single score out of 100.

{kind=link}

An almost-perfect score here is nothing to completely ignore because it does imply certain characteristics and considerations you may want to know about. The company has superb fundamental scores, managing an expanding operating/EBIT margin during a rising inflation. Its PB is actually low, and it manages consistent revenue growth per share no matter the environment.

The company is a very clear leader in the global reverse vending machine market. Any competitor is significantly smaller in terms of what markets they're in, and the company has the significant, worldwide business expertise to bring to the table in any of the projects they work in.

Most of all, the company is an attractive play on a trend that's really only beginning and can be argued to be in its infancy. Recycling is what I would call a "megatrend". The company has already more than tripled its revenues since the early 2000s, and I believe this to be continuing, based on the four global trends:

- Climate Change/Resource Scarcity

- The ongoing demographic and social change

- Changes in technology

- Global urbanization isn't declining.

All of these point in turn to Tomra and companies like it to be attractive investments and continue to grow here - and Tomra is the better choice out of potential entrants or competitors because the company comes to the table with a half-century worth of expertise and experience in exactly this market. It already has a market-dominating position in many nations, and expanding this is something they've been working with for the past decade.

Things to keep an eye on with Tomra is mostly its margin development and revenue trajectory. Cost inflation will likely continue to be a pressure point. The important points include making sure that Tomra continues to win attractive tenders and offers here - which the company currently does. Australia is a good example of this. The company recently won a large tender in Victoria, and there's one running in Tasmania as well - so keeping an eye on new markets where the company is entering is key as well.

I also wouldn't expect all that much in the way of operating leverage even as the company grows. There are some - but the fact is, the company is operating installation- and service-heavy machinery which requires physical presence, even though some digital options are being pushed at this time. If there is operating leverage here, I consider it as being somewhat limited compared to other companies.

The company has set profitability targets company-wide for 2027 that reflect the current profitability for Recycling and Collection. If the company does manage this, I believe its valuation metrics might be justified, in conjunction with the growth that the company is offering here. So that is the main factor that I am watching with Tomra.

Tomra's valuation - is somewhat attractive despite a premium

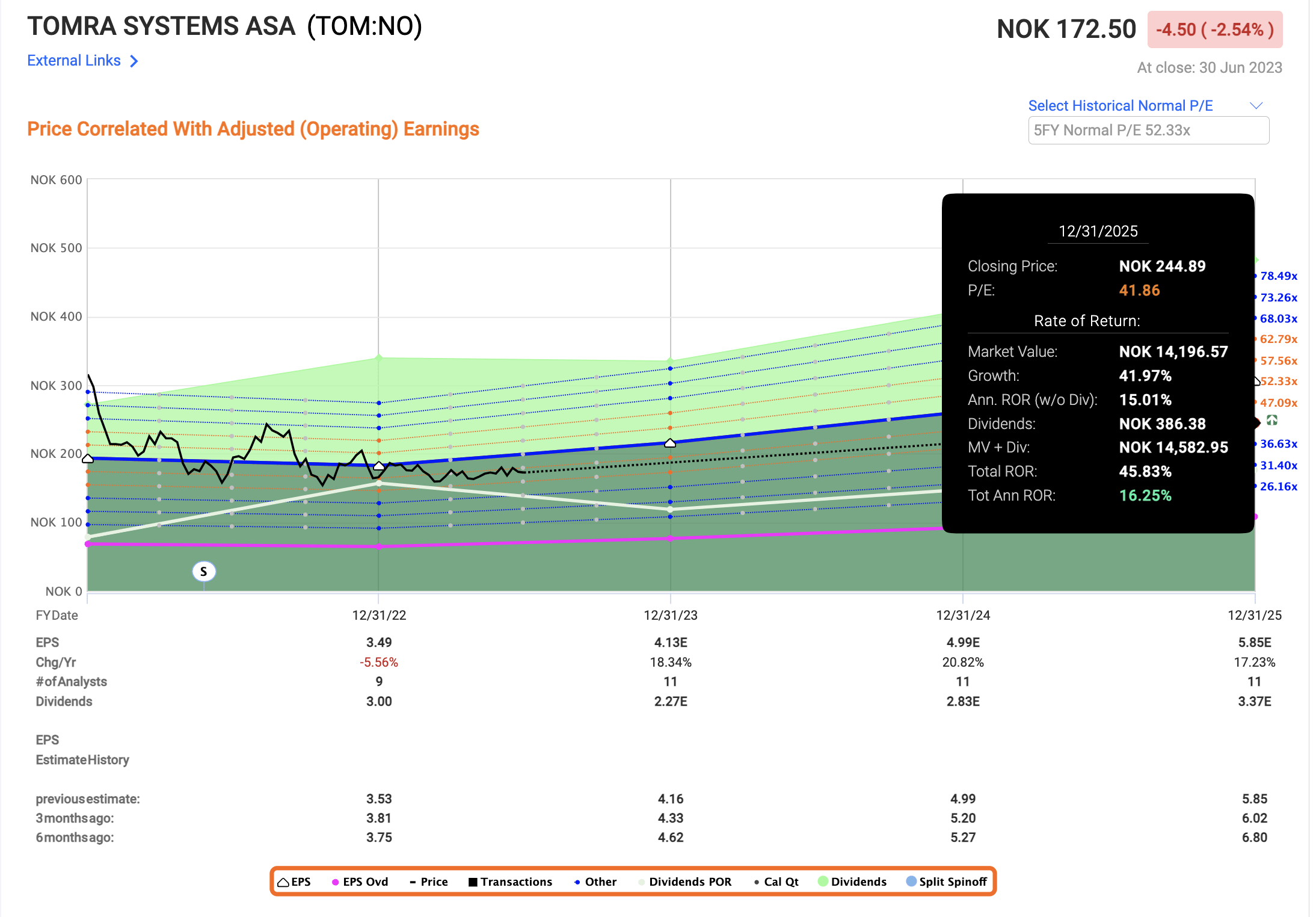

Tomra is an attractive company despite the overall premium we have going for us here. In my last article, I argued that the company, despite it trading at 35-40x P/E, can be attractive if you forecast it at the right and fair level. I also raised my share price target to 166 NOK at the time. This still put the company at a "HOLD", but it was close to a "BUY".

Tomra, as of this morning, trades at 176, having gone up somewhat. From a perspective of significant growth and premium, the company could be viewed as a "BUY" here, but you would need to value it at over 40x P/E. While the company over the past 15 years has traded as high as 85x P/E and has not been below 30x P/E since 2017, I'm still always leery about such a premiumization for any company - unless that company is something like LVMH (LVMUY). Even then, I think twice before going in.

The reason is the degree of growth that must happen in order for that valuation to be even close to fairly considered.

Tomra is currently expecting double-digit forward growth. That's 18-25% for 2023, 2024 and 2025E. If that happens, there is an argument to be made for the valuation. You could forecast at around 40-41x, and you'd come away with good profit.

{kind=link}

This takes into account all the market leadership the company does have, but such a foundation is a shaky one to build a "bridge" upon - or an investment thesis. If the company had better accuracy ratings, then I would consider it more seriously. But with a 30-40% negative miss ratio on a 1-2 year basis with a 10-20% MoE, coupled with current cost inflation, labor challenges, and macro, that's what in the end tips the scale for me.

I'm not increasing my PT further on Tomra. I'm not buying more at over 170. I own a position in Tomra that I expanded last time the company fell below 165 NOK, and I will buy more if we see such a dip again - but you have to put a stop somewhere - and this is where I put my stop.

S&P Global averages for this company come to around 161 NOK per share. That means that for once, my target is actually above the average. 8 analysts follow the native share of Tomra Systems ASA, and those are at a range of between 140 NOK to 205 NOK.

In addition to my position in the common shares, I also have cash-secured puts running at a strike of 142.5 NOK that expire in 3 weeks which would essentially triple my position if going ITM - I hope for it, but I doubt it'll happen because Tomra usually doesn't move that "fast".

However, this is how I play Tomra as an investment. You need to be quick when the company is attractive - and you need to have the guts to stay passive when it isn't - and really go for the single cents and stick to your price target.

My price target is 166 NOK. My rating, therefore, is "HOLD", and here is my thesis.

Thesis

- Tomra is a market-leading, world-leading reverse vending machine and recycling business. At the right price, it becomes a "MUST-BUY", with a holding target that goes beyond the usual, for a superb business model with proven reach and scalability.

- However, anything above 45x P/E is a no-go for this business, and I want it cheaper. I don't believe 30x P/E is in the possibilities, but 35-40x is the most I will pay.

- This comes to a PT of around 166 NOK/share normalized, which is still a "HOLD", but the company has been a "BUY" a few times the past few weeks.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.'

Tomra is a 4 out of 5, if you accept the premium. Keep your eye on the ball here, because it might go attractive in less than 48 hours. For now, it's a "HOLD", and this is my update in June 2023.

For further details see:

Tomra: An Update On Recycling, Still A Hold