TMRAY - Tomra: What Upside Is There At 110 NOK

2024-01-05 19:28:40 ET

Summary

- Tomra is worth a premium to its multiple, justified by its fundamentals, operations, and market position.

- The company has been discounted enough and is now trading at a significant discount to its recent-term valuation.

- Tomra is a world-leading recycler with potential for further revenue growth in sensor-based collection and other forms of recycling.

Dear readers/followers,

My last article on Tomra saw me improving my target and recommendation to a "BUY" from a "HOLD". While the company has been a very volatile investment for the past few months, I firmly believe in two things when it comes to Tomra.

First off, I believe that Tomra is worth a premium to its multiple. The degree of premium is subject to discussion, but a premium I believe is most certainly justified based on the company's fundamentals, its operations and its market position.

Secondly, I believe the company has been punished or discounted enough at this time. I went in too early when it came to my corporate account - but I kept averaging down at more and more appealing valuations until I was buying shares at below 90 NOK.

The company is now back to almost 115-116 NOK for the native ticker. That's still a significant discount to the recent-term valuation, but not as significant a discount as we've seen on a 20-year basis.

In this article, I'll update my thesis on Tomra, from my last article from September 20th back in the last year, which you by the way can find here.

My thesis for Tomra is that of a premiumized company moving back to a sort of premium, based on above-average growth rate on a forward basis. Because these latest negatives are based on non-recurring items such as cyberattack costs, I believe the market is severely underestimating Tomra at this, and at lower prices. This forms the core of my current thesis.

Let's look at what sort of returns and what sort of upside you can expect from Tomra this time around.

Tomra's upside after 3Q23 and a 115 NOK native share price

The company's problem, as it has always been, is its historical premium and the length that the company has been trading at that premium. The problem has never been Tomra's operations, its operational execution, its fundamentals, or its overall safety. Because all of these things are solid.

For the past few years, especially 2019-2022, this company has been trading way too high. But this is no longer the case.

This company is a world-leading recycler with operations in reverse collection, food, and general recycling. 4,600+ employees make this company a world leader, generating over $1B per year, and I believe this is only to be the beginning of this company's potential journey and overall revenue potential. Tomra's idea is to begin with a sensor-based collection of recyclables, and this has now moved into segments of both other forms of recycling as well as food sorting. Tomra is expanding - and it's expanding all into what are essentially not only future-proof but future-centric segments.

Tomra IR (Tomra IR)

Part of the reason why I believe you should allow this company some leeway in its valuation is the profitability this company has. When a company makes a substantial amount of profit on a per-dollar basis, you should pay attention. And for every dollar of revenue that Tomra makes, it makes over $0.58 in gross profit and almost $0.09 in net profit. That's market-leading for this sector, at least above 87.6% of all the other players in this sector, that sector being Waste management, containing 114 players globally for comparison, including Waste Management ( WM ), Republic Services, and others (Source: GuruFocus).

But it's where the company's profits from that I find a compelling investment argument. Because recycling, collecting, and food, are sectors that are going absolutely nowhere. And with the company's market-leading overall position, it would take something quite something large for the company to not continue to perform decently here because all of the company's sectors are set to grow in terms of volume over the next few years. (Source: Tomra IR forecast)

As I've said, 3Q23 is the latest set of Tomra results. You can find those here .

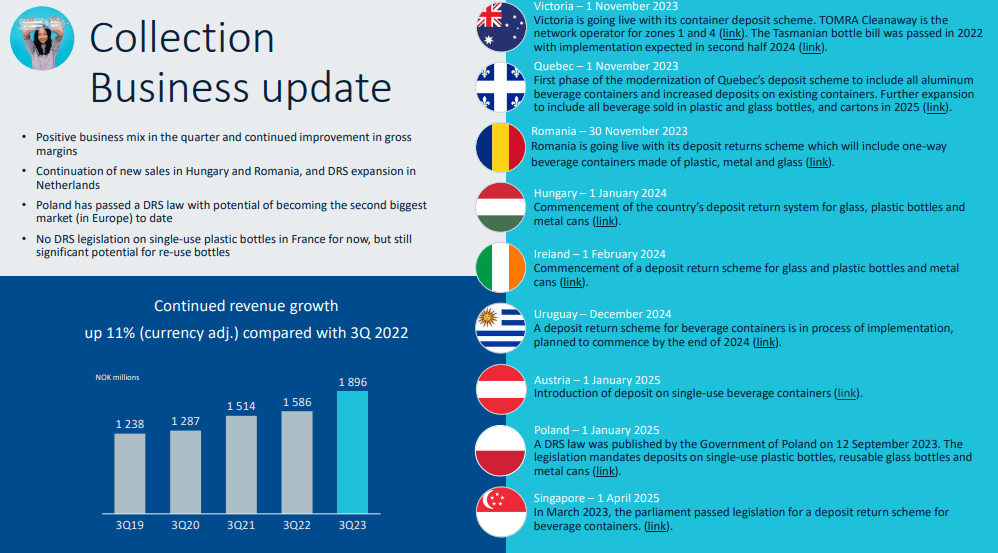

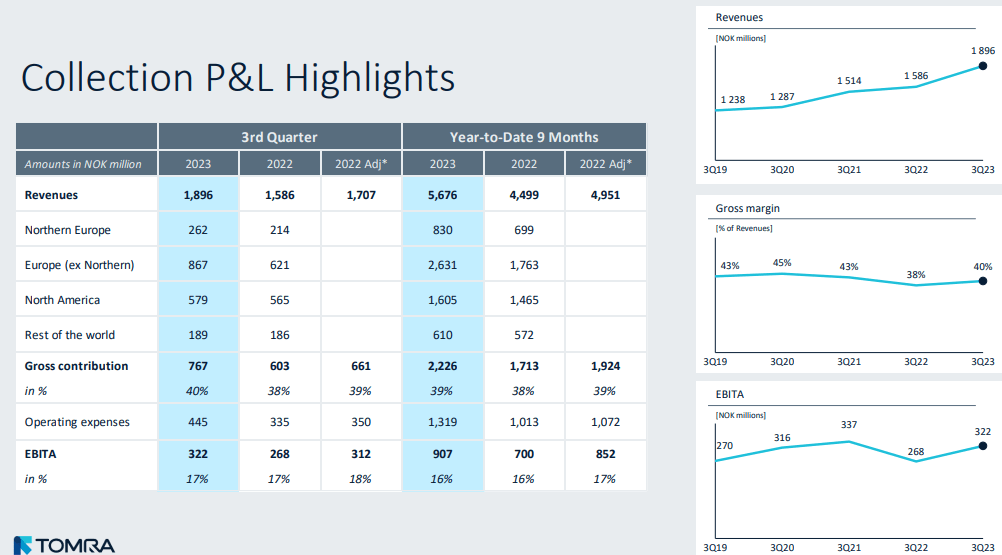

The company's total revenues were up for almost the entire group - double digits for Collection and recycling, but weighed down by food, which saw the total group revenues "only" go up 3%. However, gross margins were up to 43%, which is one of the highest numbers the company has ever had.

Some of the more challenging parts include an increase in operating expenses. This increased to over 1.2B NOK when adjusted for the cyberattack costs the company experienced during 2023, which was what sent the company's shares tumbling as much as they did in the first place. Without that though, the costs were still up significantly, and made it possible for the company to generate less in EBITDA for the quarter than for the YoY period, with cash flow going into the negatives. This cash flow negative though, was mostly due to delays in invoicing due to the aforementioned cyberattack.

Other than that, the P&L's for the 9M period are still impressive despite what's been going on this year. The company's revenues are up significantly, for the first time reaching over 10B NOK on a 9M basis, and over 5.5B NOK for collection alone. Because most of the issues the company faced were on the margin side, and most of them in the non-recurring category, I expect that finances will return to better growth going forward. None of the company's fundamental financial metrics have deteriorated as a result of this either. Recievables and inventories are up slightly, but once those recievables are turned around, the company will see an improvement here as well. The debt maturities for the company continue to be well-laddered, with the first debt above 550M NOK not coming due until 2025E. All this means the company retains what I would consider a very conservative financial position as of 9M23.

{kind=link}

Tomra IR (Tomra IR)

Tomra is essentially a play on the triple segments of collection, recycling and food, with over 105,000 installations in over 100 countries on the planet. The company's geographical diversification does mean it needs to treat every nation as a new market and work these individual markets to establish dominance for its recycling and reverse-collecting solutions.

{kind=link}

Tomra IR (Tomra IR)

Despite the lower results in Food, this is one of the segments the company expects to grow one of the most in the long term. It's also one of the segments where Tomra is not yet a market leader, even though it's among the market leaders, and it's not where Tomra made "its name".

Still, on the basis of population growth and the expansion of the middle class, the need for reduced waste and loss in food segments, shift to automation and digital. food safety regulations, all of these trends really go hand-in-hand with Tomra developing and selling its solutions. The company has also been working in this segment specifically, unlike others, to grow inorganically, with 4 large mergers in the past decade, beginning with Odenberg and ending with BBC Technologies back in 2018.

The group's P&Ls for the quarter and the current period mostly give indications of a mid-cycle current trend, impacted by the cyberattack. Without the cyberattack, it would be somewhat of a lower overall growth rate than the company might be used to, but in no way a bad result. more importantly, the collection segment with its P&L specifics still showing good trends, by which I mean that the revenue and profits are, sans cyberattack effects, growing at double-digit rates, with a top-line growth from ~4.5B NOK to 5.67B NOK in 2023 9M. This segment is, as is usually the case, far more resilient than other sectors.

{kind=link}

Tomra IR (Tomra IR)

The company is currently preparing for entry into new markets, and the next few quarters will be dependent on the timing of the new initiatives and market pushes. 2022 and 2023, in part, were years of really extraordinary growth. The company's expected growth is going to be less for the next few years, and the demand for recycled materials is going to continue to be high, leading to solid results in sorting that outweigh at least in part some of the challenging macro and backdrop, which currently is characterized by delayed customer investments.

Tomra is also expecting to see a good amount of savings from its cost reduction program, up to 350M NOK.

These facts and fundamentals mean that I expect the company to continue to grow, albeit at a slower pace than before.

Here are the current risks and upsides to Tomra, as I currently see them.

Risks & upside to Tomra

The upside to Tomra is easy - it's a continued recycling and collection upside with significant macro potential as the company expands into new countries and geographies. The company has margins and product expertise on its side already, and as long as it can manage to compete with new entrants, I don't see that market position or that upside changing materially.

The risk is premium - but we've already seen this premium moderate significantly over the past few months, first below 200 NOK, then under 175, and then finally under 150 NOK, below my last conservative PT. However, the company continued to fall even below that, until it was trading at 80 NOK - before it went up again.

Valuation remains the primary risk to this investment, and the best way to offset that risk is to make sure to not invest at any price that is too expensive. You could also, I suppose, make a case for why the company could go further south if the company's growth rates were to moderate below double digits. This would happen if the company's country expansion plans do not go according to plan. The premium we're paying for Tomra, even at this valuation, is based on growth rates. If you believe the company is unlikely to manage double digit growth, then the company is not worth even 110 NOK - it would be worth closer to 60 NOK, at around 16-18x P/E normalized. But I believe the company's growth estimates are likely.

That's why I'm happy I expanded significantly at 90 NOK, why I'm currently in the green, and why I'm giving you this valuation target and forecast for Tomra.

Valuation for Tomra

Tomra's valuation has moved from a high premium to a far more "moderate" premium. However, it's crucial to keep your eye on that multiple, because at a 5-year average, you're looking at an average premium of 66x. if you'd like to forecast the company on that basis, then feel free, and expect that several hundred percent RoR - but I don't consider it likely.

I consider this to be a justified normalization for where the company has gone in the last few years. A 25-30x P/E is far more likely for where this company might go, but that's as high as I would go for the company. With a current expected EPS growth of over 20-30% annually for the past few years, this gives us a 21% annualized upside to a 24x P/E, a valuation the company has not held for a very long time and only dipped briefly toward when it was as cheap as it was in a long time in September. That's a low valuation for this company.

A more normalized 30x P/E, which I consider to be the highest valuation possible here. And that 30x P/E, that's at a 30% annualized RoR - an excellent rate of return by any measure in a 3 year period, putting us at 122% RoR f it materializes.

Likely?

I do not consider it unlikely in the least. The company has an above 70% accuracy rating on its forecasts. S&P Global analysts following Tomra as a business do not consider it worth anything close to my own PT - but these are the same analysts that only a year ago most of them were over 180-200 NOK/share.

Now they're at a low of 82, with a high of 135 NOK. I believe analysts are significantly underestimating where Tomra might go here, and this is why I'm estimating the company at 150 NOK. I arrive at this target using premiumized and average P/S and P/E values. If you use DCF or Graham estimates, the company doesn't warrant anything higher than a 40-60 NOK. You need to accept a high amount of premiumization based on the company's historical annual growth records to reach that 150 here - because even on a 20-year basis, this company grows at above 10% EPS per year (Source: FactSet). For 2024E, this implies a 40x P/E, and for 2025E, it's a 30x P/E - which implies just how high the company's estimated growth is here - which again, I agree with. That's why I am investing here.

I considered changing my target here, despite holding my "BUY" rating, but in the end, I do not believe a lowering of the target is justified here.

Not if Tomra keeps performing as they have in the past few years, or the past 10.

Here is my thesis for the company as it currently stands.

Thesis

- Tomra is a market-leading, world-leading reverse vending machine and recycling business. At the right price, it becomes a "MUST-BUY", with a holding target that goes beyond the usual, for a superb business model with proven reach and scalability.

- However, anything above 45x P/E is a no-go for this business, and I want it cheaper. I don't believe sub-25x P/E is in the possibilities, but 25-35x is the most I will pay.

- This comes to a PT of around 150 NOK conservatively, and this makes the company a "BUY" here. I continue to view it as a "BUY" in early 2024.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.'

It's still not cheap, but I'm willing to call it a "BUY" here based on an attractive enough price target for the company.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Tomra: What Upside Is There At 110 NOK