TR - Tootsie Roll Industries: Don't Chew On This Stock Right Now

2023-05-24 05:31:13 ET

Summary

- Tootsie Roll Industries is as stable and predictable as you might imagine.

- This is virtually a no-growth business, with no M&A along with the secular shift away from sugar.

- Share prices recently hit an all-time high, but does this mean the stock is overvalued?

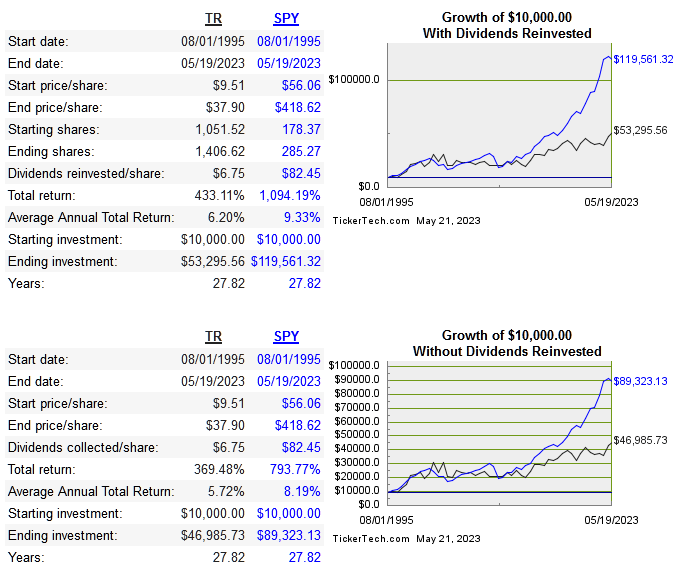

Tootsie Roll Industries ( TR ) is an American producer and distributor of many different confection brands. The company is over 100 years old, and unlike many other smaller packaged food brands, TR was never taken out by one of the big players. Below is the long term performance of the shares:

{kind=link}

| Company |

| Revenue 10-Year CAGR |

| Median 10-Year ROE |

| Median 10-Year ROIC |

| EPS 10-year CAGR |

| FCF/Share 10-Year CAGR |

| TR |

| 2.3% |

| 9.2% |

| 9.1% |

| 5.2% |

| -11.4% |

| -1.1% |

| 12.4% |

| 7.5% |

| 1.3% |

| -2.2% |

| 4.6% |

| 62.9% |

| 19.8% |

| 10.7% |

| 7.8% |

| 6.3% |

| 11.6% |

| 9% |

| 8.2% |

| 7.9% |

| 5.2% |

| 12% |

| 12% |

| -1.5% |

| n/a |

| 4.7% |

| -1.8% |

| 0.8% |

| n/a |

| n/a |

While most companies in this space tend to acquire and sell off brands as if they were trading cards, TR has been relatively stable as far as acquiring and divesting.

Capital Allocation

Below is a look at cash flows and how they were allocated in USD millions:

| Year |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| EBIT |

| 72 |

| 84 |

| 91 |

| 92 |

| 71 |

| 70 |

| 69 |

| 58 |

| 67 |

| 111 |

| FCF |

| 94 |

| 78 |

| 76 |

| 82 |

| 26 |

| 73 |

| 80 |

| 57 |

| 54 |

| 49 |

| Dividends |

| 14 |

| 19 |

| 21 |

| 22 |

| 23 |

| 23 |

| 23 |

| 24 |

| 24 |

| 25 |

| Debt Repayment |

| 3 |

| 2 |

| 3 |

| 3 |

| 4 |

| 4 |

| Repurchases |

| 23 |

| 25 |

| 33 |

| 29 |

| 34 |

| 19 |

| 34 |

| 32 |

| 30 |

| 31 |

They haven't made a meaningful acquisition in many years, and this won't be a driver of growth going forward. They usually pay out around half of earnings in dividends, and haven't reduced share count by any meaningful amount in spite of the repurchases that took place.

Long term debt is only at $4 million, so since the balance sheet is in great shape, I wouldn't mind them using a little debt to acquire something that embraces the move away from sugar and traditional candies. In addition I think this is yet another stock that would benefit from a "cannibal" strategy instead of regular dividends. The stability of the business does result in stability of the dividends, but with such underperformance over the long run, an aggressive reduction in share count would have increased shareholder return more than with the current policy.

Risk

The biggest risk here is paying for much for what is essentially a no-growth business. The CEO is 90-years-old, so I won't expect any major changes whatsoever. As far as ownership, she is part of the controlling family, so any activism is basically off the table. The plan is for the next generation to keep running the business, so betting on any kind of turnaround or major change would be pointless.

In spite of the commendable stability of the company, it is facing a long term secular risk as consumers continue to eschew sugar. I don't see this causing any serious decline in the company, the brand power is real and will always have a place. However, top line growth will always be minimal, and I don't expect the top or bottom line to ever grow aggressively again.

As I mentioned with capital allocation, I would actually like to see them take on a little risk by using debt to acquire some newer brands that reflect what consumers will go for in the future.

Valuation

Shares hit an all time high in April of this year, but does this mean the stock is overvalued?

Below is the multiples comp:

| Company |

| EV/Sales |

| EV/EBITDA |

| EV/FCF |

| P/B |

| Div Yield |

| TR |

| 3.8 |

| 25.8 |

| 70.4 |

| 3.6 |

| 0.9% |

| MDLZ |

| 3.6 |

| 23 |

| 39.3 |

| 3.7 |

| 2% |

| HSY |

| 5.3 |

| 20.7 |

| 30.2 |

| 15.5 |

| 1.5% |

| LDSVF |

| 5.4 |

| 26.5 |

| 50.7 |

| 6 |

| 1.1% |

| JJSF |

| 2.1 |

| 24.9 |

| -246.4 |

| 3.5 |

| 1.8% |

| THS |

| 1.2 |

| 22.4 |

| -17.7 |

| 1.6 |

| n/a |

There isn't any under-pricing judging from these comps, the stock trades as multiples in line with its peers, so let's look at the dcf model next:

moneychimp

I feel I'm being overly kind with my EPS projections, but even so the shares are definitely overvalued at these levels. Fundamentally I think the stability of this company will continue, and the secular decline will take a long time to play out. For that reason I consider the stock a hold, not a sell.

Conclusion

TR has many iconic brands under its umbrella, and these brands have stood the test of time, as the company is over 100 years old. Although it is in a very low/no growth phase, cash flows are very stable and predictable. The balance sheet is very strong, and there is no risk at all coming from debt or dilution.

With the stability comes no chance of change. This is a family controlled business, and there won't be any activism to force change, so don't make that part of your investment thesis. The status quo is in charge and there won't be any major changes for a long time.

The problem is that the market has gotten far too optimistic about this company. The multiples aren't exactly low, and intrinsically I think this is way too much to pay for a business that barely grows, and pays out around half of its earnings in dividends. This is a hold for me, but I still wouldn't hold my breath for a much needed rerating of this stock.

For further details see:

Tootsie Roll Industries: Don't Chew On This Stock Right Now