TR - Tootsie Roll Industries: Don't Expect Rocket-Like Growth Hold It For The Dividend

2023-06-29 12:57:52 ET

Summary

- Tootsie Roll Industries is a slow-growth company with a high earnings multiple, but it offers a regular cash and stock dividend.

- Despite operating in a mature industry with larger competitors, Tootsie Roll has a competitive advantage due to the brand strength of its primary offering and its niche market position.

- Tootsie Roll's strengths make it a potential long-term buy, but at the current price, it is a hold.

At a time when investors are seeking rapidly growing companies, Tootsie Roll Industries ( TR ) passes only a few screens. It is not a company with tremendous growth potential. It operates in a mature industry with a penchant for slow organic growth. Also, the stock trades at a high earnings multiple, scaring investors away.

But the company is one of the few paying a regular cash and stock dividend, making it attractive for those seeking a reliable passive income stream. The combination of the dividend types pays a 4% yield. Moreover, the fortress balance sheet and decades of dividend growth make it more appealing. If you own the stock, hold it, and buy on the dips.

Overview of Tootsie Roll

Tootsie Roll Industries, Inc. traces its history back to 1896, but the iconic candy was not created until 1907. Today, the company sells various candy and gum products, mainly in the United States, Canada, and Mexico. Other well-known brands include DOTS, Junior Mints, Andes, Charms, Blow Pops, Sugar Daddy, Razzles, Sugar Babies, Charleston Chew, Dubble Bubble, etc.

Tootsie Roll has a dual-class share structure. According to the proxy, the Chairwoman and CEO, Ellen R. Gordon, owns or controls approximately 57.1% of the common stock and 82.8% of the Class B shares. Because the Class B shares have ten votes, Ms. Gordon has control of the company. Her ownership stake has been rising because of share buybacks.

Total revenue was $687 million in 2022 and $708.4 million in the last twelve months.

Tootsie Roll Will Not Grow Fast

Tootsie Roll will not grow fast. So, investors expecting rapid growth and thus share price appreciation, like Nvidia ( NVDA ) and other trillion-dollar stocks, will surely be disappointed. Instead, Tootsie Roll grows incrementally each year with rising volumes and sales. Most of this growth will occur from minor product innovations, price increases, and seasonal products.

In the confectionery market, Tootsie Roll's competitors are much larger. Companies like Hershey ( HSY ), Mondelez ( MDLZ ), and privately-held Mars control the segments. However, Tootsie Roll’s competitive advantage is the brand strength of its primary offering, the Tootsie Roll. It lacks direct competition because of its unique flavor and texture. Some of the company's other brands are also well-known. Brand strength and family control have allowed the firm to operate successfully as a niche player.

The firm’s sales are concentrated around the holidays typically associated with candy and giving, like Halloween, Valentine’s Day, Easter, Christmas, etc. In fact, the third quarter is usually the most important for sales and earnings because of Halloween.

The firm seemingly avoids acquisitions. As a result, we do not view it as a likely avenue for growth.

Inflationary Risks Are High

Although top-line growth will likely be slow, the company's earnings per share are rising. The firm has lowered its share count by over 10% in the past decade. In addition, in order to counter high inflation and increasing input costs, the firm focused on operational efficiencies. Despite higher packaging, freight, commodity, services, and labor costs, Tootsie Roll has grown earnings per share and is attempting to restore margins to historical levels through price increases and realization.

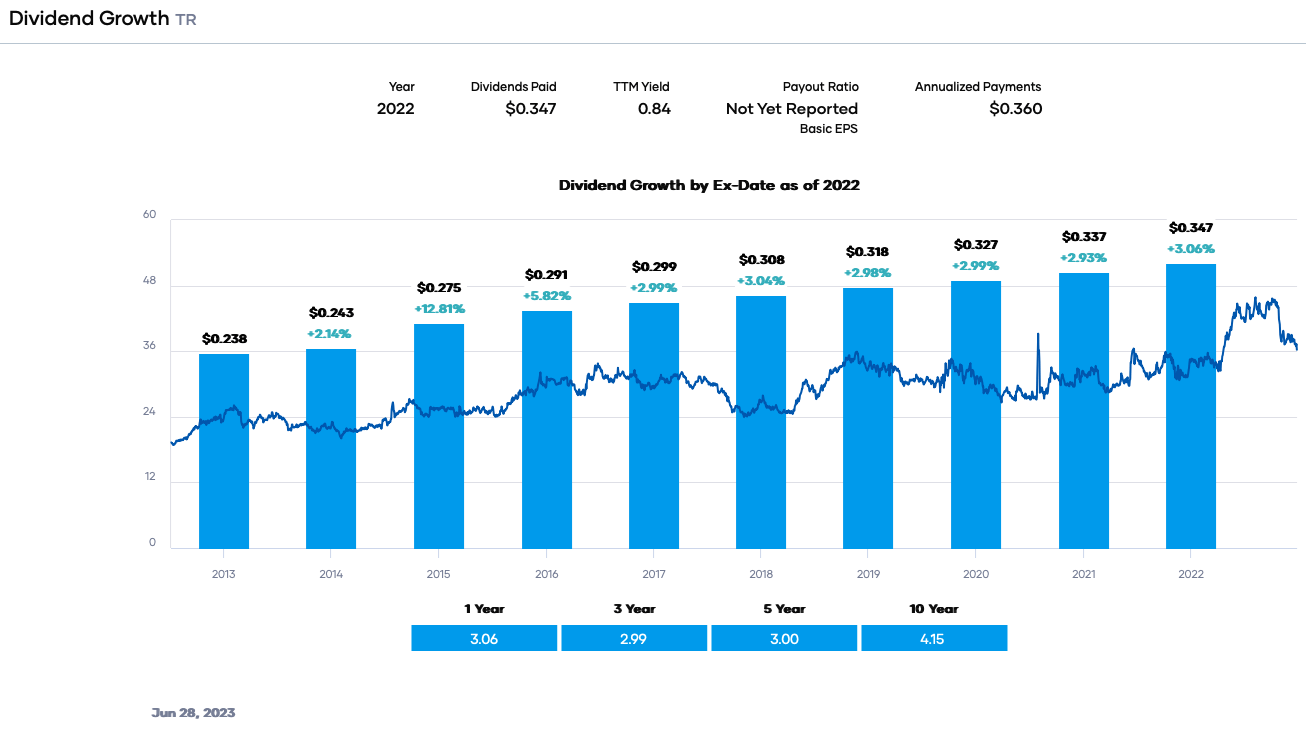

Dividend Analysis

Tootsie Roll’s dividend yield is usually about 1% and does not fluctuate much based on a rate of $0.36 per share. Besides the regular cash dividend, the candy company pays an annual 3% stock dividend, treated as a 103-to-100 stock split. Investors can either retain or sell the extra stock annually, giving a 4% yield.

The regular cash dividend was last increased in 2016 and is due for raise. The moderate trailing twelve months [TTM] payout ratio of around 33% provides room for a slight increase. However, Tootsie Roll focuses on stock repurchases and maintaining a net cash position on its balance sheet. But because of the stock dividend, owners of shares see higher dividend cash flow annually. Consequently, Tootsie Roll is on the list of 2023 Dividend Kings with 57 years of increases. The 5-year growth rate is 3% CAGR.

{kind=link}

Tootsie Roll has solid dividend safety based on earnings per share, free cash flow ((FCF)), and its balance sheet.

Our earnings estimates for the calendar year 2023 are $1.13 per share, and the dividend rate is $0.36 per share. These numbers give a payout ratio of roughly 32%. This value is well below our target of 65%. We do not expect this ratio to fluctuate much year-to-year. During the COVID-19 pandemic, the company showed that earnings per share were only modestly impacted during a Black Swan event, allowing the dividend to be paid.

Tootsie Roll produced almost $49 million in FCF in 2022. The dividend required ~$24.6 million, giving a dividend-to-FCF ratio of ~50%. This value is less than our desired percentage of 70% or less. However, FCF before the pandemic was about $75 million. If the company's FCF returns to the higher value, the dividend safety is obviously much more robust.

The firm has a fortress balance sheet with a net cash position. Tootsie Roll has $123.9 million in total cash and short-term investments and no short-term debt. The only long-term debt has been an industrial revenue bond of $7.5 million. Hence, interest coverage is excellent, ad debt is not an issue for dividend safety, considering the cash on hand covers the payout several times.

Valuation

Tootsie Roll’s share price has fallen ~13.3% year-to-date but is still up nearly 5% in the past 1-year. Despite the share price decline, the forward price-to-earnings ratio is still elevated at roughly 32X. The value seems high but is actually below the 5-year and 10-year averages, suggesting an elevated value is characteristic of this stock. We ascribe this to the limited float, share buybacks, and investors' tendency to buy and hold the shares.

We estimate earnings per share of $1.13 in 2023. We will use 30X as the fair value multiple accounting for brand strength, company control by the Gordon family, and changing tastes to healthier options. Thus, our fair value estimate is $33.99. The current stock price is ~$36.24, suggesting Tootsie Roll is slightly overvalued.

Applying a sensitivity calculation using P/E ratios between 29X and 31X, we obtain a fair value range from $32.86 to $35.12. Hence, the stock price is approximately 106% to 113% of the fair value estimate.

Estimated Current Valuation Based On P/E Ratio

| P/E Ratio |

| 29 |

| 30 |

| 31 |

| Estimated Value |

| $32.86 |

| $33.99 |

| $35.12 |

| % of Estimated Value at Current Stock Price |

| 113% |

| 110% |

| 106% |

Source: Author's Calculations

How does this calculation compare to other valuation models? Portfolio Insight’s blended fair value model gives a result of $33.68 per share. This model is based on the relationship between stock price and P/E ratio and dividend yield in the trailing 5-years and 10-years. Fair value estimates based on the two metrics are created and averaged together, giving a blended fair value based on P/E ratio and dividend yield. An EV/EBITDA model on finbox provides a fair value of $43.87.

The three-model average is ~$37.18, indicating Tootsie Roll is near fair value at the current price.

Final Thoughts

Tootsie Roll is often an overlooked stock in the dividend growth community because of its elevated earnings multiple, family control, and slow growth. But the company has many strengths, including a solid dividend yield, decades of dividend increases via a stock dividend, and outstanding dividend safety. The company will probably grow slowly but steadily. Also, when faced with recessionary challenges like the pandemic, Tootsie Roll’s excellent financial positions allowed it to emerge relatively unscathed. Hence, we view Tootsie Roll as a long-term buy, but at the current price, it is a hold.

For further details see:

Tootsie Roll Industries: Don't Expect Rocket-Like Growth, Hold It For The Dividend