TR - Tootsie Roll Industries: Strong Revenue Growth But Margin Pressure Remains

2023-09-08 09:51:56 ET

Summary

- The company's revenue increased by 11.6% YoY, while operating margin reached 9.2%.

- The ability to pass on higher inflation rates to the end consumer and effective cost control supported both revenue growth and profitability.

- I would like to change my recommendation to HOLD after the decline in shares and relatively strong financial results.

Introduction

Shares of Tootsie Roll Industries ( TR ) have fallen 25% YTD. Since the publication of my article , where I recommended selling the company's shares, quotes have decreased by 27%, while the S&P 500 index has shown an increase of 12%. In my article, I would like to analyze current business trends and update my view of the company.

Investment thesis

First, despite pressure from macro headwinds, the company continues to both successfully pass on increased inflation to end consumers and demonstrate stable sales volumes. Secondly, the company's management continues to effectively control operating expenses in the face of rising prices for labour, packaging and ingredients. In addition, the company's shares have dropped significantly, so at the moment the stock quotes are below the fair level ($37), in accordance with my DCF model, which I wrote about in my previous article .

Company overview

Tootsie Roll Industries manufactures and sells confectionary products. The main market for the company is the USA (91% of revenue). The main brands are: Tootsie Roll, Charms, Junior Mints etc.

2Q 2023 Earnings Review and expectations

The company's revenue increased by 11.6% YoY due to increased prices for the company's products, increased sales volumes and an effective marketing campaign. Gross profit margin decreased from 33.2% in the 2nd quarter of 2022 to 32.9% in the 2nd quarter of 2023 due to increased costs for freight, packaging, labor and supplies.

Gross profit margin (Company's information)

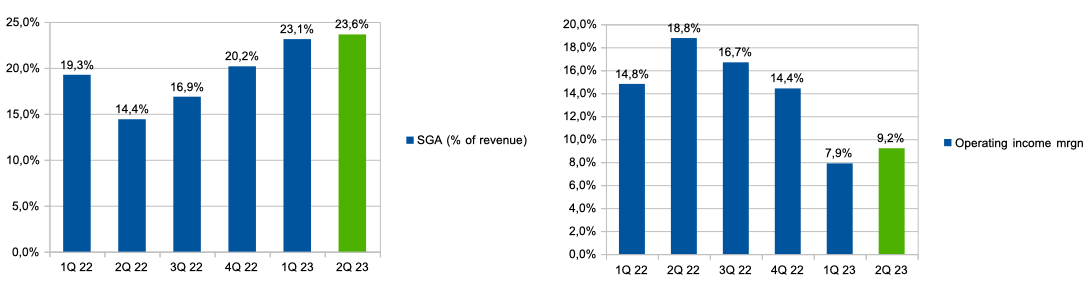

SGA expenses (% of revenue) increased from 14.4% in 2Q 2022 to 23.6% in 2Q 2023 due to one-time expenses such as certain deferred compensation in the amount of $4.7 million. Thus, adjusted SGA (% of revenue) decreased from 22.8% in the 2nd quarter of 2022 to 20.9% in the 2nd quarter of 2023.

Therefore, operating margin decreased from 18.8% in Q2 2022 to 9.2% in Q2 2023. Adjusted operating margin increased from 10.1% in Q2 2022 to 12.4% in Q2 2023.

{kind=link}

SGA (% of revenue) & operating margin (Company's information)

On the one hand, I like the fact that the company increased product prices, as a result we saw a recovery in gross profit margin compared to the previous quarter, however, on the other hand, I do not think that we can see a rapid recovery in operating margins in the next few quarters.

First, inflation continues to be relatively high, so I expect margin pressure from input costs to continue. This is confirmed by management's comments in the financial results for the 2nd quarter.

As we look into 2024, we believe that our costs for ingredients will be even higher in 2024 than in 2023.

In addition, in the 1st quarter of 2023, the company successfully increased product prices, which provided significant support to financial results, however, it is necessary to understand that the potential for price increases is not unlimited. I believe that rising prices for the company's products next year may help maintain current levels of profitability, but I do not expect that we will see a continuation of the trend towards profitability recovery.

Risks

Margin: an increase in prices for input costs (labor costs, freight, packaging, services, manufacturing) due to the relatively high level of inflation may have a negative impact on the level of operating profitability of the business in the following quarters.

Competition: increased competition may lead to increased marketing costs and investment in prices, which may also have a negative impact on the profitability of the business in the future.

Supply chain: disruptions in the supply chain, labor shortages, or increased competition for labor can lead to a decrease in product supply volumes and, consequently, a decrease in revenue growth.

Valuation

According to the P/E ((TTM)) and P/S ((TTM)) multiples, the company is trading at 39x and 3x, respectively, which implies a premium to the sector median of about 116% and 168%, respectively.

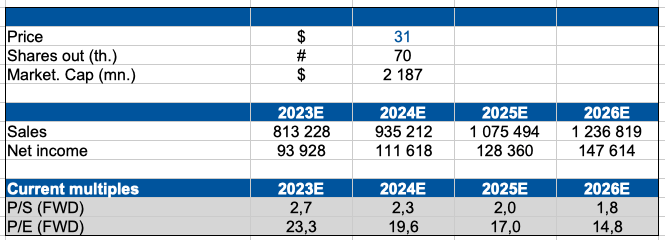

I think investors need to pay attention to forward multiples, as forward multiples take into account the improvement/deterioration of future financial performance. Since we do not have forecasts from sell-side analysts, I will rely on my own forecasts, which I wrote about i n my previous article . So, according to my calculations, the current P/E and P/S multiples for 2023 are about 23x and 2.7x, respectively. Thus, I can conclude that the company is still not cheaply valued, but the current premium, in my personal opinion, is fair due to stable cash flow, dividends and a long historical record.

{kind=link}

Conclusion

In my personal opinion, the company's reporting confirms the fact that management is able to act effectively under pressure from macro factors. The company continues to demonstrate both revenue growth and margin expansion despite continued rising inflation, so I would change my recommendation to HOLD. I would like to add that I like the company's business model and its positioning in the market, so I would happily change my recommendation to BUY in the future if I see signs of a slowdown in inflation and opportunities for operating margins to return to historical levels.

For further details see:

Tootsie Roll Industries: Strong Revenue Growth But Margin Pressure Remains