TR - Tootsie Roll: Solid Business But No See's Candy

2023-12-14 14:24:49 ET

Summary

- Tootsie Roll is one of the longest-operating confectionary manufacturers in the United States, having been listed since 1919.

- Although Tootsie Roll is a solid business in its own right, it is much more capital intensive than Berkshire Hathaway's See's Candy.

- Tootsie Roll is currently not attractively valued, and its dual-class structure means there's little in terms of catalysts for change.

The recent passing of the great investor Charlie Munger got me thinking about his wisdom and teachings, especially with regards to buying great businesses at fair prices.

This article compares Tootsie Roll Industries ( TR ), a Chicago-based confectionary maker, to one of Berkshire's 'dream companies', See's Candy. While I like TR's resilient business, it is much more capital intensive than See's. Furthermore, TR's valuation multiple is not attractive at the moment.

Company Overview

Tootsie Roll Industries is a candy maker dating back to 1896 when Leo Hirschfield invented the namesake Tootsie Roll candy, a mix between a caramel and a taffy. Tootsie Roll is one of the longest surviving listed companies in the United States, being first listed on the American Stock Exchange in 1919.

Through a series of acquisitions, Tootsie Roll actually owns a number of different candies and brands today, including Tootsie Roll, Andes Chocolate Mints, Dubble Bubble chewing gum, Dot's gum drops, Cella's, and Blow Pop, just to name a few (Figure 1).

Figure 1 - Major Tootsie Roll brands (TR annual report)

{kind=link}

Financially Stable For Decades

Historically, Tootsie Roll has delivered solid financial performance through thick and thin, with revenues hovering around $500 million and operating profits in the $60 to $90 million range (Figure 2).

Figure 2 - Tootsie Roll financials have been solid (roic.ai)

{kind=link}

If there were any complaints about Tootsie Roll's business, it was that growth was too low, with revenues barely budging from the $500 million level.

COVID And Recovery Has Been A Key Financial Catalyst

However, the COVID pandemic has been a key catalyst for Tootsie Roll's financial performance. In 2020, the pandemic caused an 11% decline in Tootsie's revenues as consumers refrained from purchasing and sharing occasions (i.e. Halloween).

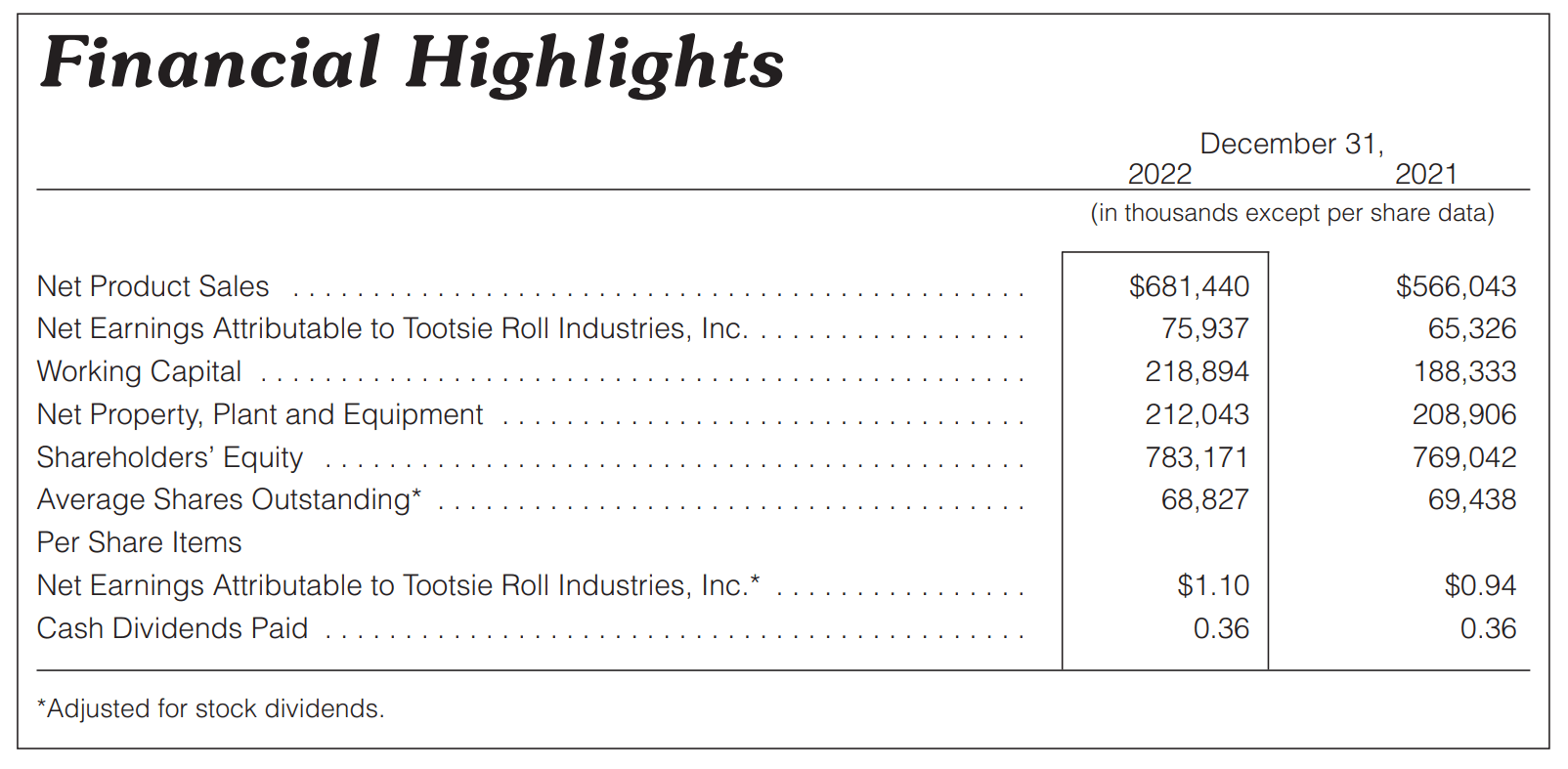

Tootsie rebounded strongly in 2021, with revenues of $566 million as COVID restrictions gradually lifted (Figure 3). Revenues were further boosted in 2022 to $681 million on the back of soaring inflation, as consumer staple manufacturers like Tootsie Roll took advantage of inflation to raise prices.

Figure 3 - TR financial highlights 2022 (TR 2022 annual report)

{kind=link}

Dil. EPS also reached all-time highs of $1.10 / share, as Tootsie Roll evidently did not see margin compression that affected other manufacturers.

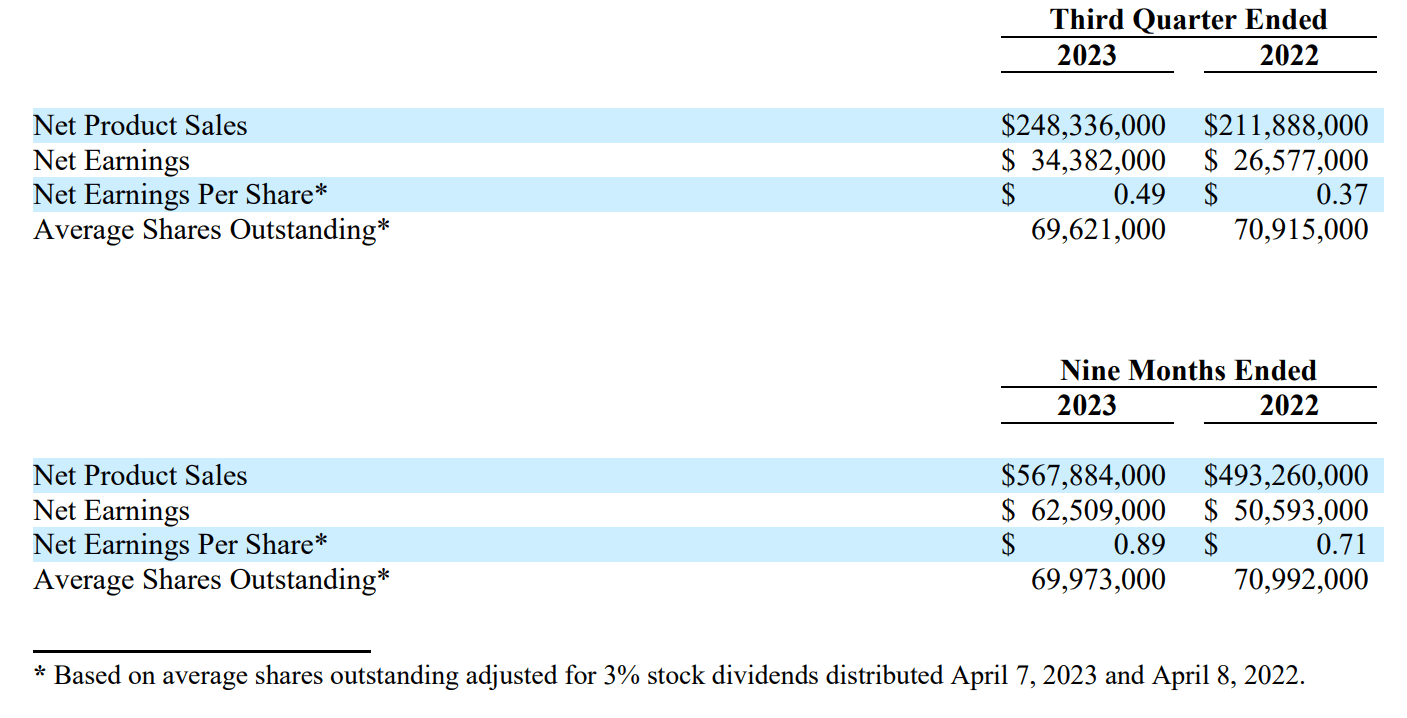

So far in 2023, Tootsie Roll has continued to see strong growth in revenues, as the company continued to push price. Revenues in the 9 months to September 30, 2023 reached $568 million, a 15.2% YoY increase, while dil. EPS reached $0.89, a 25.4% increase (Figure 4).

Figure 4 - TR continues to grow revenues in 2023 (TR Q3/2023 10Q report)

{kind=link}

See's Candy As A Model For A 'Dream Company'

According to Mr. Munger, in his early days, Warren Buffett was a strict disciple of Benjamin Graham and stuck to picking up 'cigar butts' for a few last puffs. However, as the two men got closer, Charlie's investment philosophies began to rub off onto Warren and Berkshire Hathaway's ( BRK.B ) investment strategy switched to buying great businesses at fair prices.

One such business was See's Candy. As described in Berkshire's 2007 annual letter , See's Candy was a dream business. When Berkshire acquired See's in 1972 for $25 million, the candymaker's annual sales was $30 million for 16 million pounds of candy and the business generated less than $5 million in pre-tax profits. However, the capital needed to operate the business was low, at only $8 million.

In 2006, See's sold 31 million pounds of candy (2% growth rate annually), but sales had risen to $383 million and pre-tax profit had reached $82 million. On a per-unit basis, See's sales increased from $1.88 / lb to $12.35 / lb, or a 5.7% CAGR over 34 years, or slightly better than CPI inflation of 4.8%. This showed See's candy had pricing power and was able to maintain margins through thick and thin. The capital required to operate the business had increased modestly to $40 million by 2006.

In total, from 1972 to 2006, See's Candy generated $1.35 billion in pre-tax profits for Berkshire to redeploy into new streams of cash, less the $32 million increase in capital. So Berkshire got a 23.7x return on its capital up to 2006 ($25 million initial purchase plus $32 million in additional capital).

Tootsie Is No See's

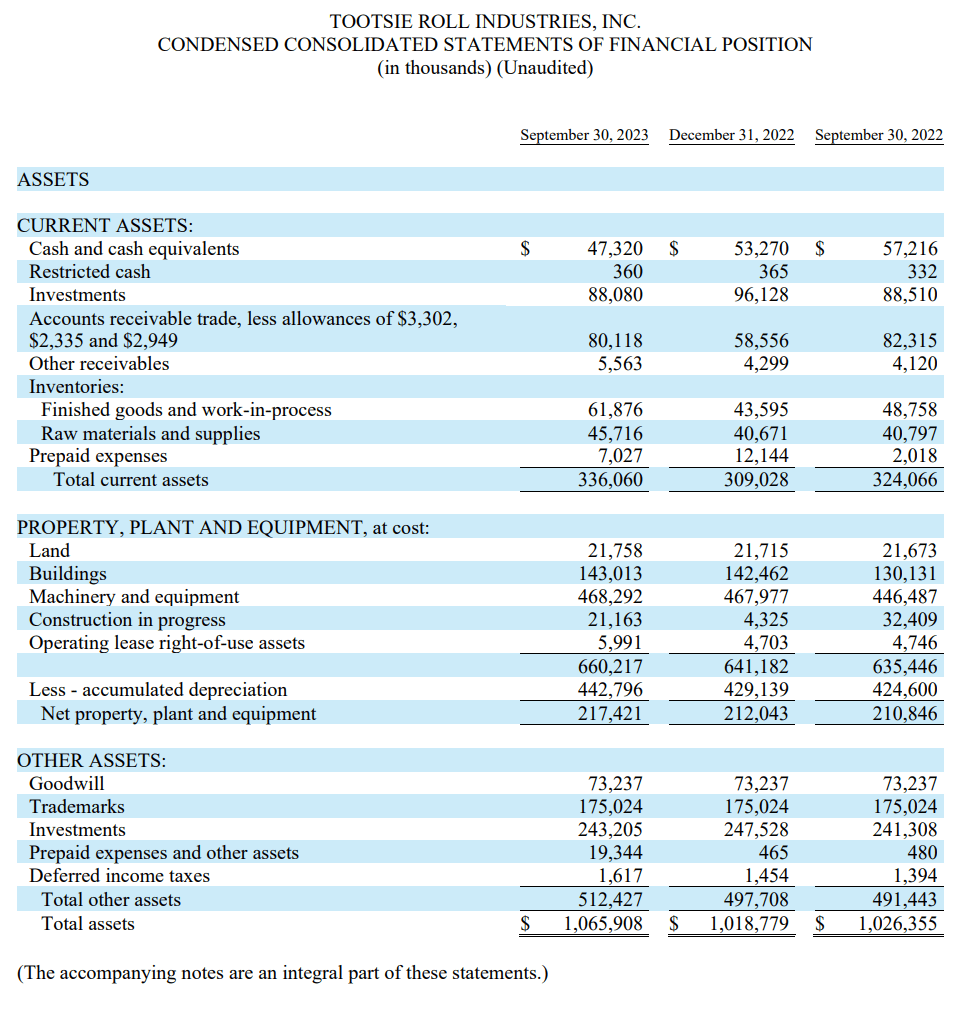

While both Tootsie Roll and See's have remarkably resilient businesses, Tootsie is definitely not See's, as the capital required to run the business is multiples of See's. For example, if we look at TR's latest balance sheet, we can see that the company had more than $600 million invested in PP&E (Figure 5, at cost). Furthermore, Tootsie Roll requires tens of million in working capital for receivables and inventories.

Figure 5 - TR balance sheet (TR Q3/2023 10Q report)

{kind=link}

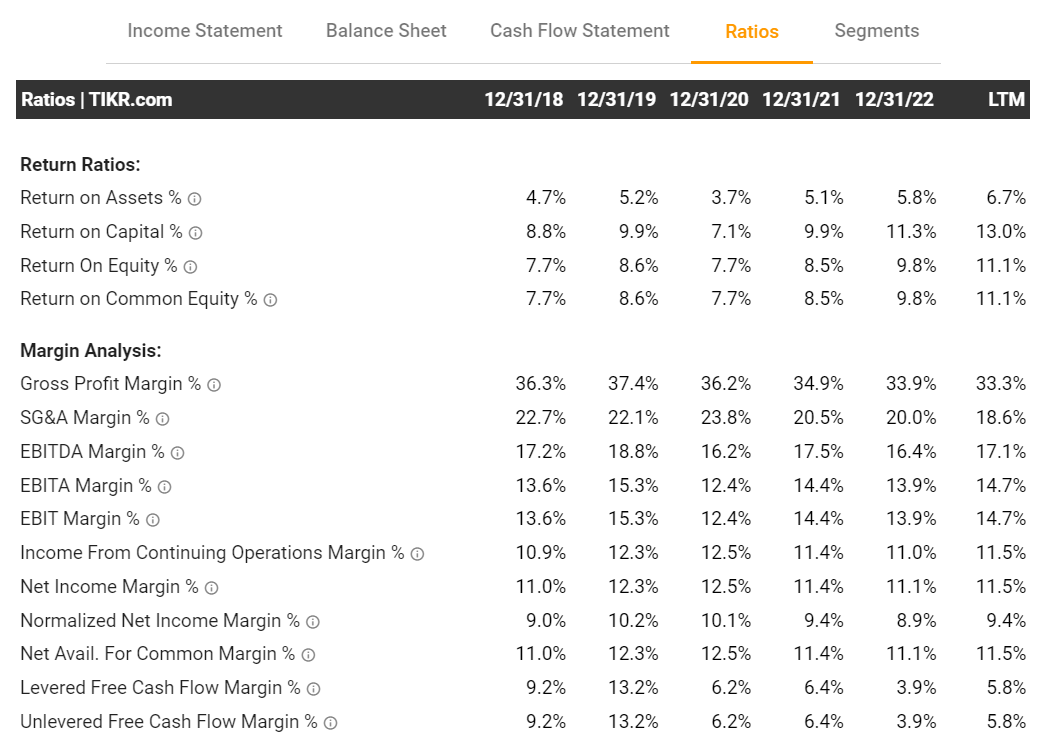

Overall, Tootsie Roll has decent net margins of 11-12% and generates ROIC's of ~10% (Figure 6). Good, solid metrics, but Tootsie Roll is definitely not See's Candy.

Figure 6 - TR financial ratios (tikr.com)

{kind=link}

Valuation Is Nothing To Write Home About

Granted, Tootsie Roll is not a 'dream business' like See's Candy, but if investors can buy it at a cheap enough price, they can still be handsomely rewarded. Unfortunately, I do not believe Tootsie Roll is attractively valued at the moment.

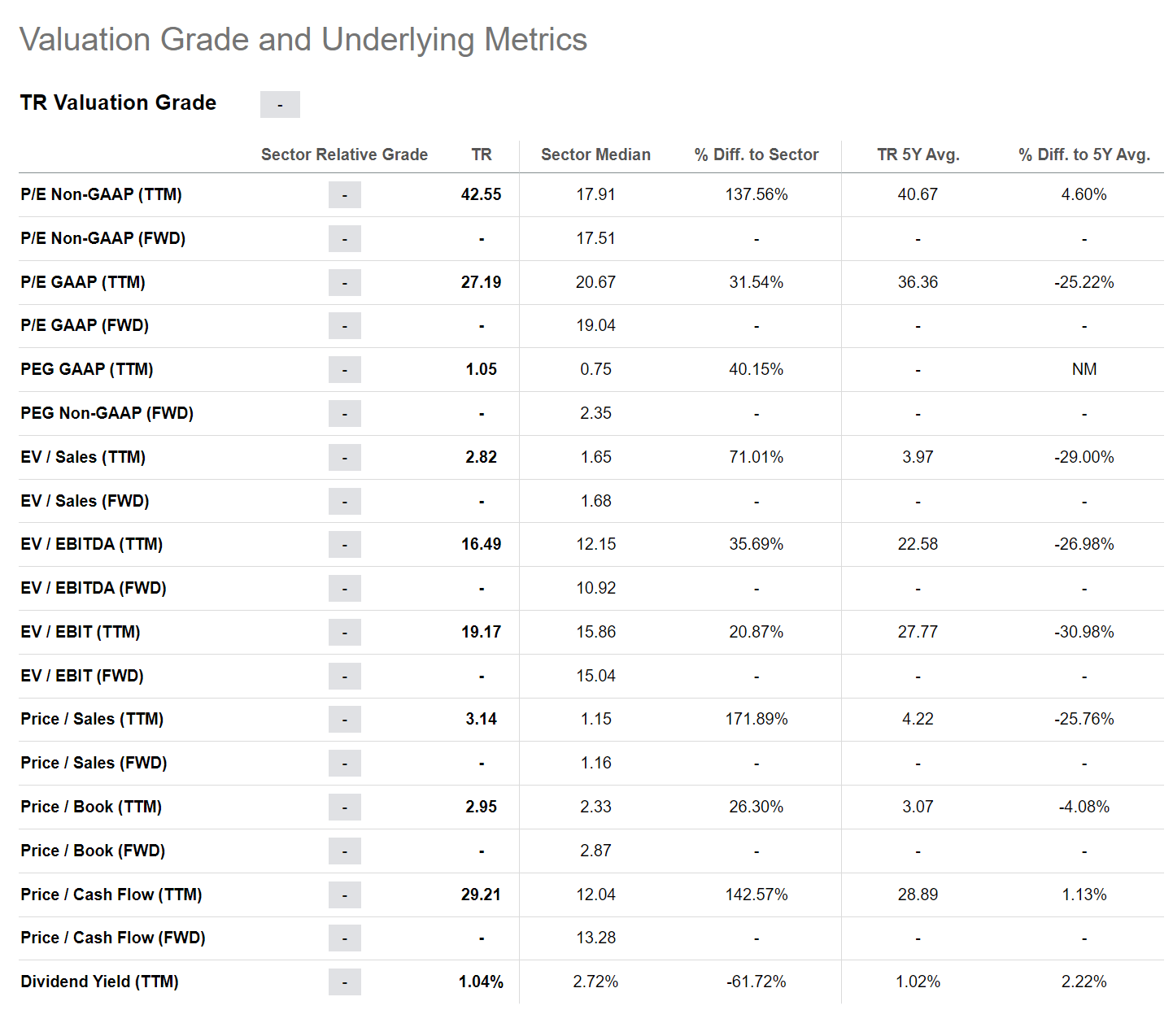

At $35 / share, Tootsie Roll is currently trading at a trailing P/E multiple of 27.2x, above the consumer staples sector median of 20.7x (Figure 7).

Figure 7 - TR is no bargain (Seeking Alpha)

{kind=link}

Furthermore, the company only pays a paltry 1.0% dividend yield.

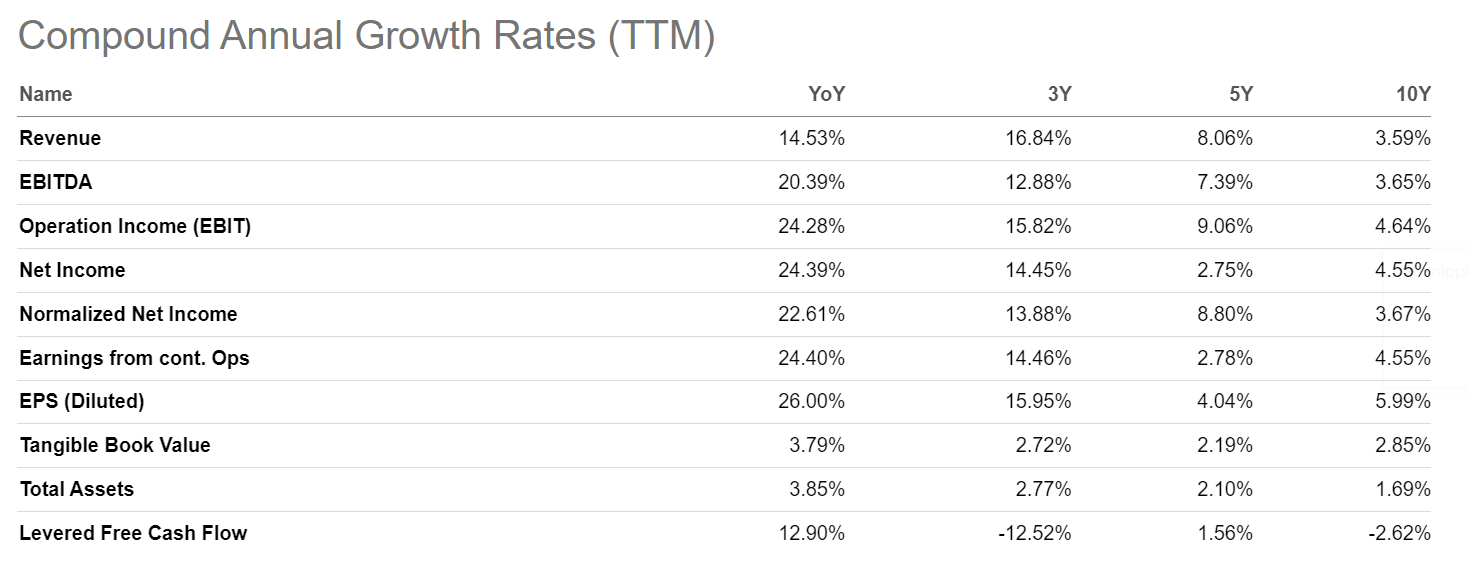

Given Tootsie Roll's low long-term (10 year) revenue and net income growth rates of 3.6% and 4.6% respectively (Figure 8), I believe Tootsie Roll should not trade at a premium to the sector multiple.

Figure 8 - Tootsie Roll has low long-term growth (Seeking Alpha)

{kind=link}

Using 20.7x TTM P/E on TR's $1.02 in EPS, I believe fair value for Tootsie Roll is closer to $21.

Dual Class Structure Means Insiders In Control

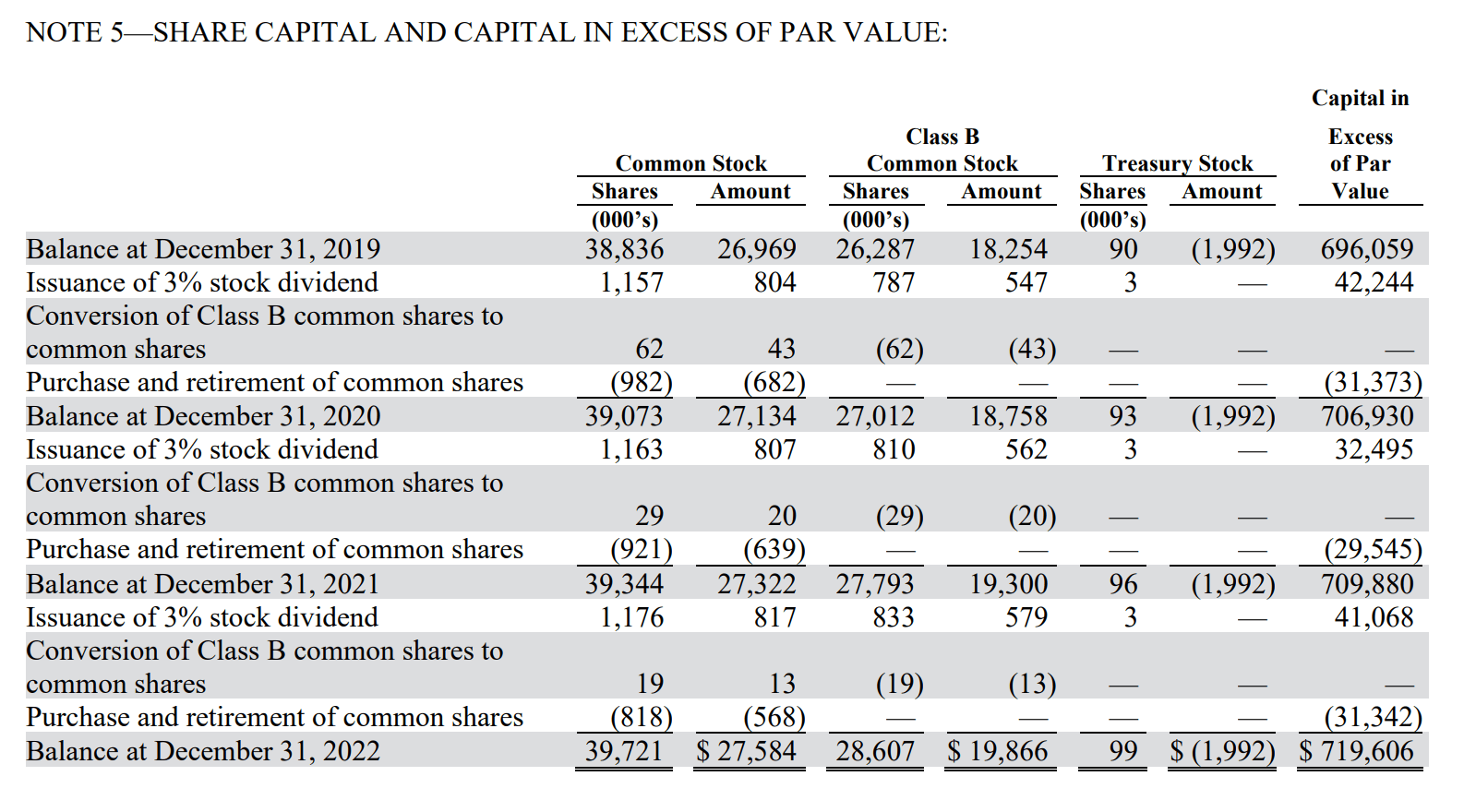

Another knock against Tootsie Roll is that the company has 2 class of shares: Common Shares and Class B shares that carry 10x the votes. The Class B shares are mostly held by company insiders and the Rubin/Gordon family (Figure 9).

{kind=link}

With their supervoting shares, insiders can essentially dictate what goes on with the company, and it appears they are content to keep churning out modest performance year-in and year-out.

Sleepy Stock With No Catalyst

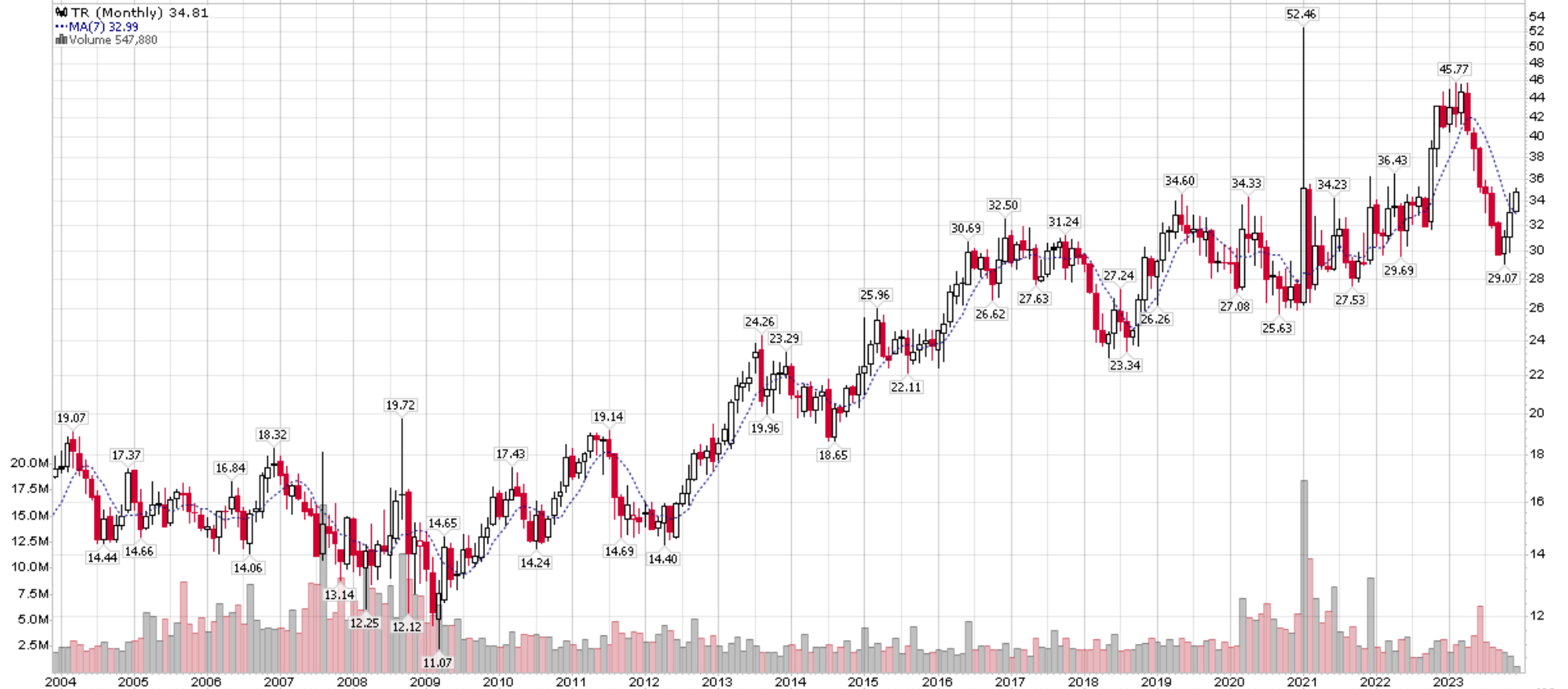

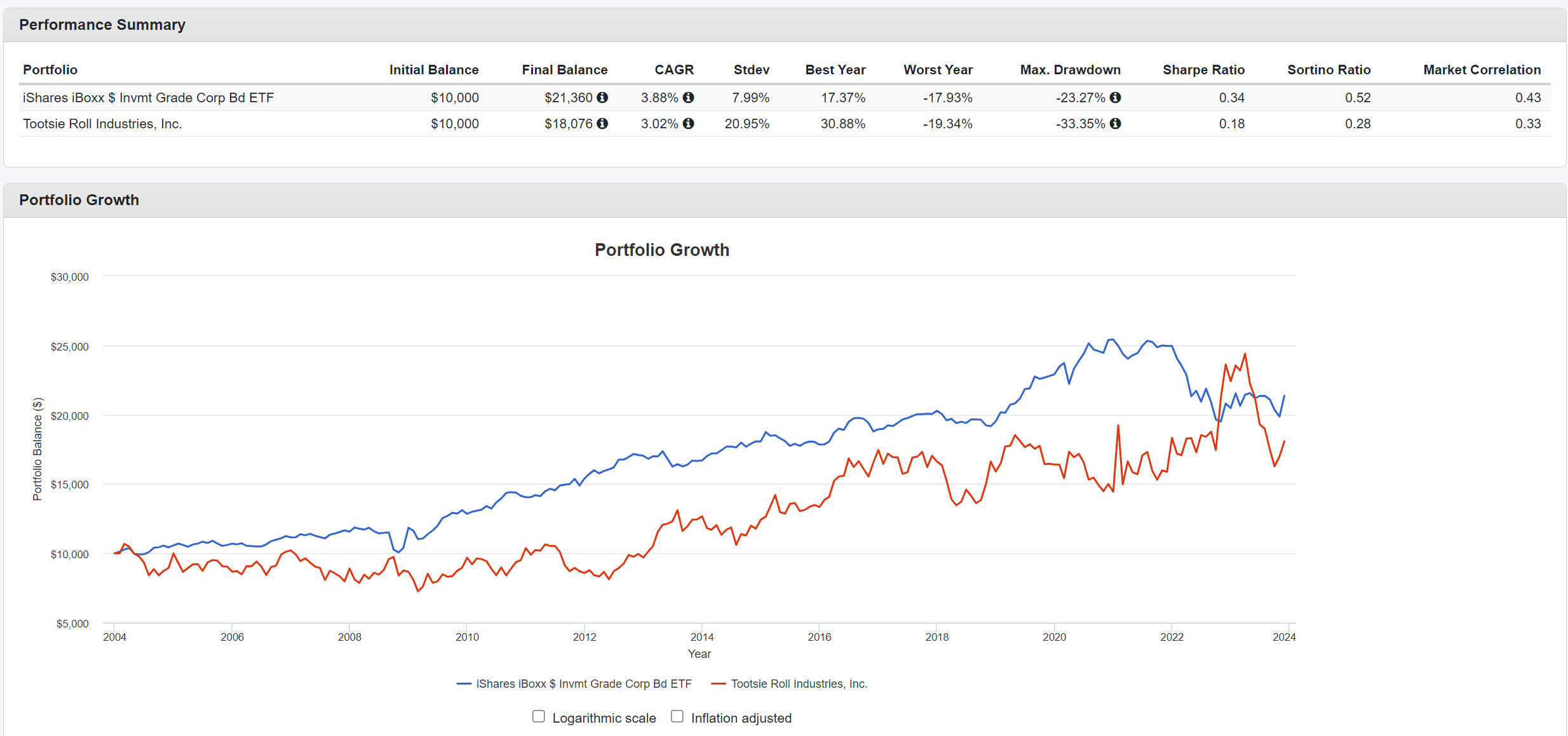

Technically, Tootsie Roll is one of the sleepiest stocks in the stock market, with the shares gaining a total of $15 / share or ~80% over 20 years, inclusive of dividends, or a CAGR of ~3% (Figure 10).

{kind=link}

Investors can probably get better returns elsewhere. For example, the iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ) would have delivered a 20 year CAGR of 3.9% compared to TR's 3.0%, with higher income (Figure 11).

Figure 11 - TR vs. LQD (Author created using Portfolio Visualizer)

{kind=link}

While Tootsie Roll is unlikely to go bankrupt, with no debts and almost $300 million in cash and investments, there are also catalysts on the horizon until/unless insiders decide to sell.

Conclusion

Thank you for reading my little homage to the late Charlie Munger. Charlie was truly a larger-than-life character, and I have learned a lot from reading about his and Warren Buffett's exploits and investments over the years.

This article really shows how remarkable some of the companies Berkshire Hathaway have been able to assemble in its portfolio. Comparing between Berkshire's See's Candy and Tootsie Roll, we can see that while Tootsie Roll is a solid business in its own right, it simply pales in comparison to See's remarkable returns on capital.

With regards to TR as an investment, I do not see any compelling reason to get involved in the stock. True, it has very resilient revenues and earnings, and inflation in the last few years have given the company cover to raise prices, but even at today's elevated earnings, Tootsie Roll is trading at 27x P/E.

I do not believe Tootsie Roll should be valued at a premium compared to its sector, given its historical low growth rates. If I apply the sector median P/E multiple to TR's trailing EPS, I derive a fair value of $21.

Furthermore, with insiders controlling the company via supervoting shares, common shareholders are at the whims of insiders and management.

I would personally avoid Tootsie Roll and rate its shares a hold .

For further details see:

Tootsie Roll: Solid Business But No See's Candy