HLIT - Top 10 Tech Stocks For 2023

Summary

- The beaten-down tech sector ended 2022 with six consecutive quarters of declines, but 2023 could offer upside when the market recovers.

- In anticipation of a 2023 recession, a contrarian position of buying stocks in the beaten-down tech sector may be just the risk-reward you need to start the new year.

- We'll look at 10 Strong Buy tech stocks that have performed well during the 2022 downturn. The stocks have excellent fundamentals, and their bullish momentum indicates they could perform well.

- My 10 Top Tech Stocks possess forward EPS growth rates ranging from 20% to 118%, and eight have forward P/E ratios below 18x. All have solid profitability and excellent factor grades.

- Not one of our Strong Buy recommendations is a Mega Tech stock or FAANG. Our Quant Rating System provides powerful signals that separate the weak from the strong and can help investors minimize risk and maximize returns.

Tech Options

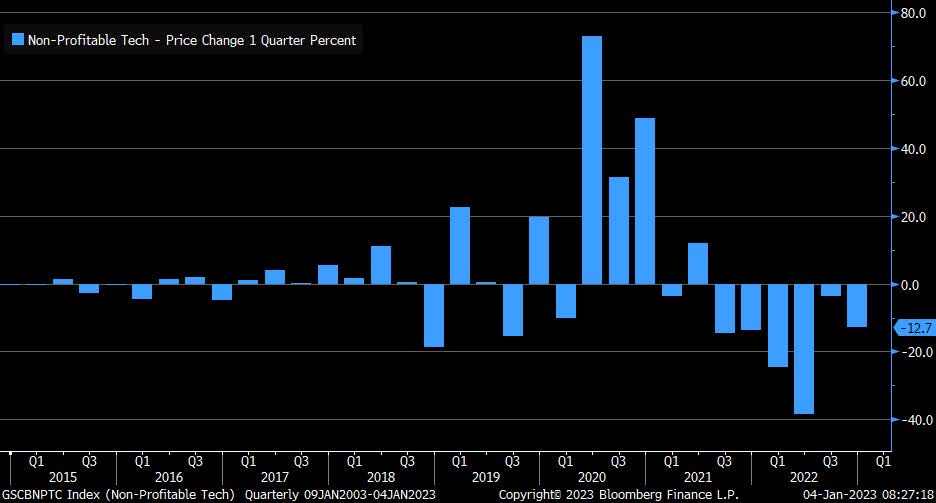

It’s not new news that the 2022 markets took investors and their portfolios on a rollercoaster ride. Technology was one of the worst-performing sectors ( XLK ) -24%, ending 2022 with six consecutive quarters of declines, as showcased in the below chart. And after poorer than expected earnings, slowing revenues, deteriorating profit margins, and slashing more than 154,000 jobs in 2022, many tech companies continue their plight.

Six Consecutive Quarters of Tech Declines

{kind=link}

Six Quarters of Tech Declines (Bloomberg Finance)

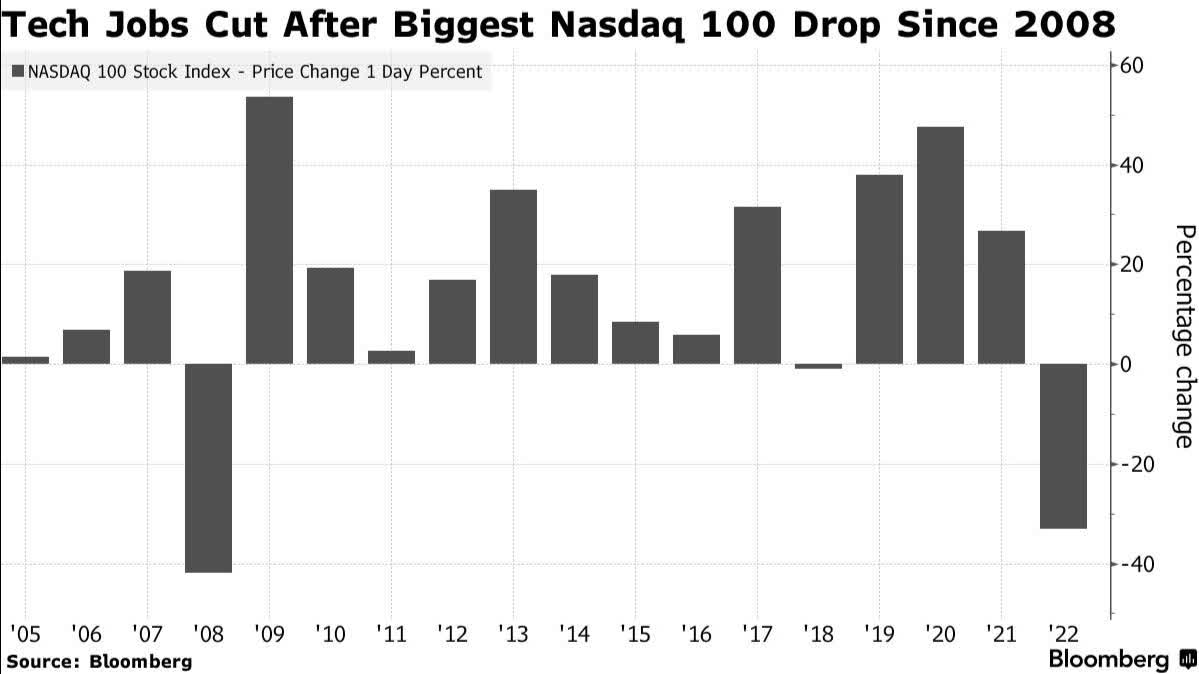

Uncertainty is looming in the first part of 2023 as an economic downturn seems likely, and companies take steps to reduce costs in anticipation of revenue declines. After the 33% decline in the Nasdaq 100, its worst showing since 2008, “Analysts have already slashed revenue growth estimates for tech companies to 2.4% for 2023, versus a consensus projection of 5.4% just three months ago,” according to Bloomberg Intelligence .

{kind=link}

Tech Sector Job Cuts Chart (Bloomberg)

And although projections for 2023 earnings are expected to fall 2.2% versus the growth projection of 4.3%, as investors and the economy battle 40-year high inflation, consumers – and companies – will likely feel the pain.

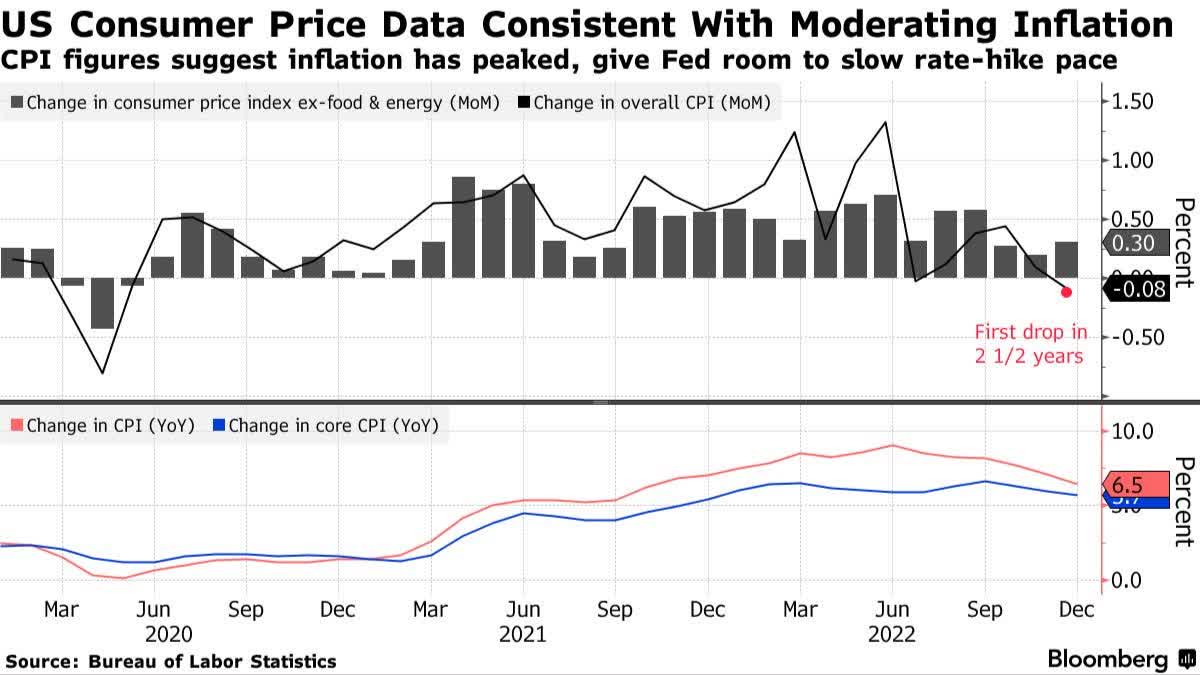

But then there’s the latest ‘Goldilocks’ CPI reading that shows consumer prices rose 6.5% over the last 12 months, one of the slowest inflation rates in a year. Core inflation increased to 5.7%, and while it would appear that the Fed may downshift rate hikes, the outlook hasn’t changed meaningfully from what it was one week ago. Inflation is trending down in line with expectations, which is neither good news nor bad news for tech stocks. This reading may be ‘just right,’ giving the Fed a runway to downshift the rate of increase by an additional 25 basis points from the December 50-basis point hike in their upcoming meeting.

{kind=link}

CPI May Suggest 'Goldilocks' Economy (Bloomberg, Bureau of Labor Statistics)

I’ll reiterate, as I have in the past, “Don’t fight the Fed,” which is why it’s crucial to consider tools when investing that offer powerful cues when markets rotate from exuberance to confusion, limiting risk while maximizing returns.

Seeking Alpha’s Quant Ratings and Factor Grades System showcases stocks with shared traits of value, growth, profitability, rising earnings revisions, and momentum that are best equipped to withstand volatility. It is a data-driven process that relies on the statistical measurement of a stock’s financial metrics and scoring how it compares to the sector. I have selected ten tech stocks that have performed well in 2022, possess excellent factor scores, and maintain bullish momentum. While past performance is no guarantee of future results, check out our top ten tech stocks for 2023.

10 Tech Stocks to Buy Despite Inflation And Potential Recession: Semiconductor And a Mix

Seven out of my top 10 stocks are semiconductors. Why? Because they are found in nearly every piece of technology used today. The semiconductor industry is on an uptick and has proven resilient when most of the tech sector was pummeled in 2022.

Because a crucial piece of investing involves diversification, especially amid market volatility, and when selecting growth or tech stocks in a rising rate environment, my picks are unique. Not all are the largest in their respective industries, offering something different for each investor. Let’s dive into my first semiconductor stock and my #1 pick overall for 2023.

1. Super Micro ( SMCI )

-

Market Capitalization: $4.47B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 3 out of 659

-

Quant Industry Ranking (as of 1/12/23): 2 out of 29

Offering SuperStorage, SuperServers, advanced cloud, and Big Data solutions, Super Micro Computer, Inc. ( SMCI ) and its subsidiaries offer a broad range of products and services in the IT space. With a strong network of semiconductor manufacturing relationships, SMCI is becoming a global tech leader that offers diverse systems, designing the newest tech innovations to optimize products. In addition to its vast portfolio, SMCI is making strides for the environment through its “ green computing ,” which offers customers cost-friendly, more energy-efficient, and environmentally-friendly solutions while trading at an extreme discount.

SMCI Stock Valuation & Momentum

SMCI has been a resilient and top-performing stock in a beaten-down sector. Not only is it my top tech stock, I included SMCI in my Top 10 Stocks for 2023 , and it was one of November’s two Alpha Picks .

Continuing to outperform the S&P 500 and Nasdaq, SMCI offers one of the best valuation frameworks in the IT sector. SMCI showcases a forward P/E ratio of 8.87x, a more than 62% difference to the sector, and a forward PEG of 0.28x, a -82.05% difference to its peers.

SMCI Valuation Grade (Seeking Alpha Premium)

In addition to its undervaluation on several metrics, Super Micro’s bullish momentum in 2022 has continued into the new year. Quarterly momentum grades of A+ highlight the stock’s significant price performance relative to the sector median, showing its strength, as evidenced by consecutive earnings beats.

Super Micro Growth & Profitability

Following record revenue for the first quarter of FY2023, SMCI beat analyst expectations. With EPS of $3.42, which beat by $0.60, and revenue of $1.85B, which beat by $129.67M, sales surged 79% year-over-year.

With goals of expanding its product portfolio by 25%, SMCI is focused on cost-cutting measures and maintaining a strong balance sheet to deliver year-over-year triple-digit percentage growth, superior to its competitors. SMCI’s plug-and-play Rack-Scale Total IT solutions are a significant growth driver. Additionally, client strength, demand capacity, and its broad server and storage portfolio is helping drive results.

SMCI vs Industry Growth Rate (SMCI Q123 Investor Presentation)

Focused on Total IT Solutions, SMCI, and saving the planet, one server at a time and homes to become a $20B revenue company amid its addition to the S&P midcap 400 Index.

2. Taiwan Semiconductor ( TSM )

-

Market Capitalization: $409.42B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 6 out of 659

-

Quant Industry Ranking (as of 1/12/23): 1 out of 66

Despite a one-year decline of 35% and geopolitical risks, Taiwan Semiconductor ( TSM ) is a chip stock that managed to withstand the substantial drawdowns that hurt other tech stocks in 2022. As the world’s largest chip maker, having manufactured more than 12,300 products that include smartphones, automotive, and digital consumer electronics, although the semiconductor industry and fabrication can be very cyclical, TSM’s bullish momentum continues to allow this stock to outperform. Taiwan Semiconductor has managed to maintain its pricing power in a popular industry while continuing to trade at a discount, all while garnering the interest of Warren Buffett, whose Berkshire Hathaway disclosed its $4.1B stake in November.

TSM Stock Valuation & Momentum

Momentum for TSM is bullish, showcasing a B- momentum grade and outperforming its sector peers quarterly. With a forward P/E ratio of 12.70x compared to the sector median of 24.11x and a forward PEG of 0.58x, Taiwan Semiconductor is undervalued substantially relative to its peers.

TSM Valuation Grade (Seeking Alpha Premium)

With plans to ramp up production , TSM’s growth and revenue projections look tremendous. Its YTD revenue of $53B is 105 times greater than its competitor Intel ( INTC ), and TSM’s advantage over popular electronics rival Samsung looks promising. As fellow Seeking Alpha author Robert Castellano writes:

“TSMC's share of the foundry sector increased from 53.4% to 56.1%, while Samsung's share decreased from 16.4% to 15.5%. Intel's share increased from 0.36% to 0.46%, according to The Information Network's report entitled "Hot ICs: A Market Analysis of Artificial Intelligence ("AI"), 5G, Automotive, and Memory Chips." While TSMC is #1 and Samsung #2 in the foundry market, Intel's acquisition of Tower in 2023 will move INTC to #7 just behind Huahong.”

TSM Stock Profitability Grade (Seeking Alpha Premium)

With consecutive top-and-bottom-line earnings beats, TSM’s reported solid earnings for Q4. Despite revenue of $20.55B missing, EPS of $1.82 beat by $0.07, the markets seemed to be unfazed by the revenue figures, as the stock rose nearly 6% after the market open. With more than $47B in cash and A+ profitability, TSM is a stock worth considering for portfolios in 2023.

3. Amkor Technology ( AMKR )

-

Market Capitalization: $7.18B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 6 out of 659

-

Quant Industry Ranking (as of 1/12/23): 3 out of 29

Another quant rated strong buy rated IT company involved with semiconductors is Amkor Technology ( AMKR ). AMKR is a leader in integrating memory and storage for computing and automotive products, offering flip-chip solutions, including turnkey packaging for smartphones, tablets, and other mobile devices. On an uptrend following stellar Q3 earnings, the stock is trading near its 52-week high but still offers upside potential given the demand for Big Data and chips, which is why I’ve selected it as one of my top 10 tech stocks.

AMKR Stock Valuation & Momentum

AMKR is trading at a premium, given its D+ overall Valuation grade. But, the majority of its underlying metrics come at an extreme discount. Showcasing a forward P/E ratio of 9.32x, a -61.34% difference to the sector, and a trailing PEG of 0.19x versus the sector 0.65x, a -71% difference, AMKR offers some value as well as bullish momentum.

AMKR Valuation Grade (Seeking Alpha Premium)

As evidenced in its performance over the last year, +22.84%, AMKR is strongly bullish. Its quarterly price performance significantly outperforms its sector peers, so much that many analysts call the stock overbought as investors continue to actively purchase shares, driving its price higher. With a Q3 2022 EPS of $1.24 that beat by $0.31 and revenue of $2.08B that beat nearly 24% year-over-year despite macroeconomic headwinds, AMKR continues to grow. Its advanced packaging technology made up nearly 80% of its Q3 business. As its CEO, Giel Rutten, stated , “Amkor continues executing on its strategy to leverage a leadership position in advanced packaging and its broad geographical footprint to capitalize on the industry megatrends of 5G, IoT, automotive, and high-performance computing.”

4. ON Semiconductor Corporations ( ON )

-

Market Capitalization: $27.79B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 16 out of 659

-

Quant Industry Ranking (as of 1/12/23): 4 out of 29

Headquartered in Phoenix, Arizona, this semiconductor stock has been one of my favorites for a while. Offering premier intelligent technology for automotive, industrial, and 5G cloud power, ON Semiconductor is paving the way for global lighter and longer-range systems. With tremendous earnings growth, EPS, and fundamentals, consider this stock for a portfolio, especially as it trades at a discount.

ON Semiconductor Stock Valuation & Momentum

Despite geopolitical and supply pressures within the semiconductor industry, and a downgrade by investment firm William Blair to start the new year, ON continues to advance. With a current B- Valuation Grade, Onsemi is more attractive than its sector by more than 36%, at a forward P/E of 15.29x. Its A+ forward PEG 0.67x indicates its great value.

ON Valuation Grade (Seeking Alpha Premium)

On a longer-term uptrend, ON shares are trading above the 200-day moving average, with investors paying higher prices for shares. Showcasing a quarterly price performance for six- and nine-months substantially better than its sector peers, it's no surprise given the tremendous growth and profitability the company has displayed.

ON Growth & Profitability

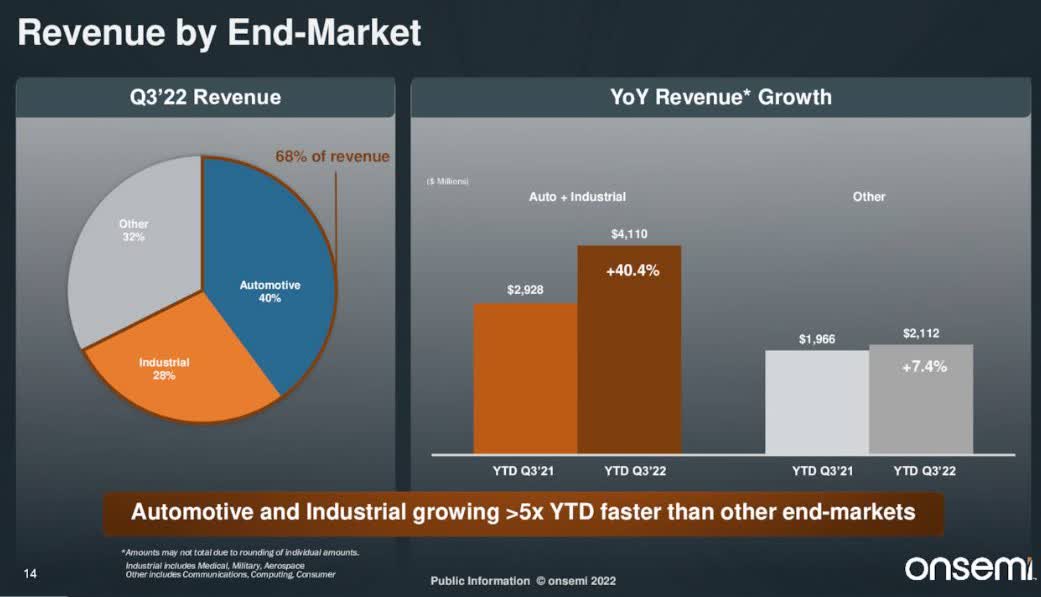

ON’s increases in revenue can be attributed to its tremendous growth on the heels of high demand in the core end markets of auto and industrial.

{kind=link}

ON Revenue by End-Market Illustration (Onsemi Q3 2022 Investor Presentation)

The two markets collectively made up 68% of revenue, up 40.4% in Q3 2022 compared to the same period in 2021. In addition to an EPS of $1.45 that beat by $0.14 and record revenue of $2.19B, ON’s strategy continues to drive its long-term growth plans while reducing the volatility in its business, all while expanding market share.

5. Axcelis Technologies, Inc. ( ACLS )

-

Market Capitalization: $3.14B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 6 out of 659

-

Quant Industry Ranking (as of 1/12/23): 3 out of 29

Capitalizing on semiconductor innovation, Axcelis Technologies, Inc. ( ACLS ) designs, manufactures, and services ion implantation in the fabrication of chips around the world. Currency and geopolitical risks have affected the industry in general. Still, ACLS has gained amid high demand and outperformed the overall semiconductor industry and S&P 500 over the last year, as evidenced in the chart below, while managing to trade at a discount.

ACLS Significantly outperformed SPY & SMH (1-year price performance)

{kind=link}

ACLS Significantly outperformed SPY & SMH (1-year price performance) (TradingView, SA Premium)

ACLS Stock Valuation & Momentum

Despite trading near its 52-week high of $97.43 per share, ACLS is undervalued. Forward P/E of 18.34x is a -24.98% difference to the sector 24.45x, and its forward PEG of 0.92x is more than -40%. With bullish momentum showcasing substantial quarterly price-performance beats, analysts call the stock overbought as shares are actively being purchased and the 200-day moving average is upward sloping. In anticipation of Q4 revenues exceeding $250M, above its previous guidance of approximately $232M to $240M, Axcelis raises Q4 guidance , indicating solid growth and profitability anticipated.

ACLS Growth & Profitability

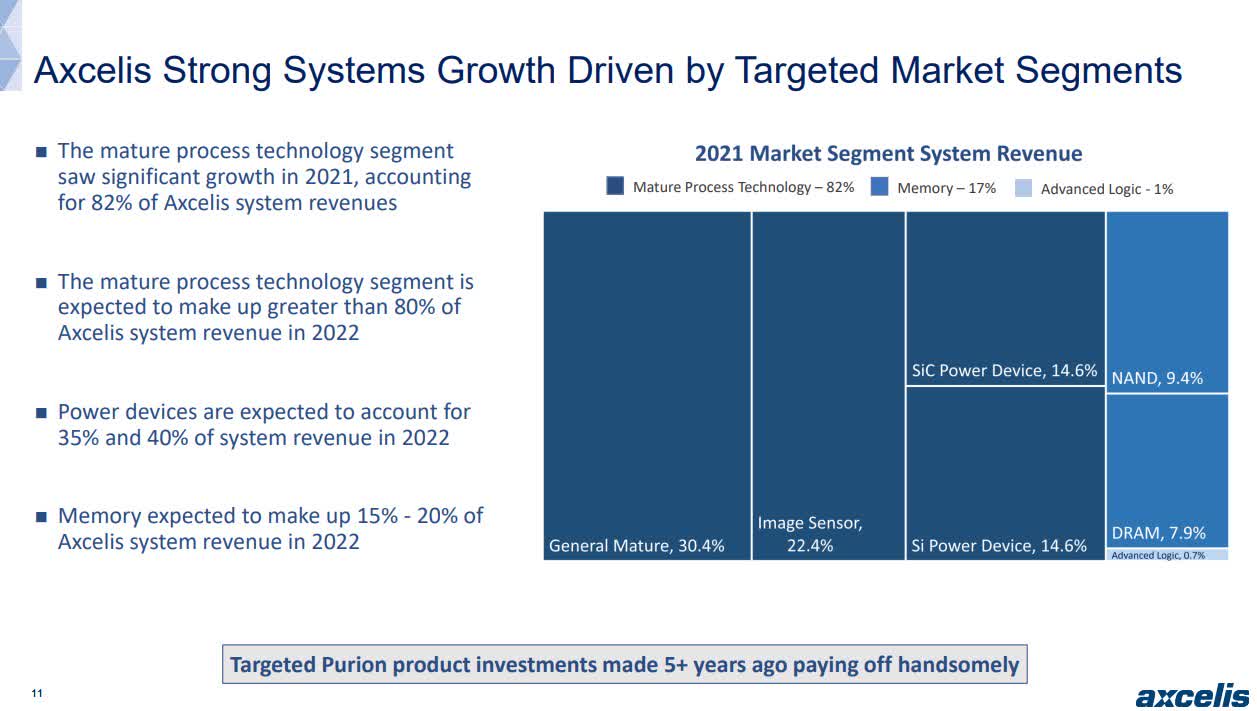

Expecting to achieve nearly $1B in revenue over the next few years on the heels of growth drivers like the electrification of automobiles and advancements in communications technology. ACLS’s targeting of specific markets has helped advance its revenues.

{kind=link}

ACLS Targeted Market Segments (ACLS November 2022 Investor Presentation)

With its Q3 2022 earnings showcasing top-and-bottom-line beats for the 12th consecutive reporting, it should be no surprise that analysts are revising up and that I selected this stock as one of the top 10 for 2023. EPS of $1.21 beat by $0.06, and revenue of $229.18M beat by nearly 30% Y/Y. With Q3 gross margins of 45.1%, well above guidance, and a backlog and strong consumer demand into 2023, Axcelis is well positioned to grow, according to President & CEO Mary Puma , despite an anticipated slowdown in the industry for 2023.

6. Himax Technologies, Inc. ( HIMX )

-

Market Capitalization: $1.25B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 17 out of 659

-

Quant Industry Ranking (as of 1/12/23): 4 out of 29

My final semiconductor stock pick is Himax Technologies, Inc. ( HIMX ), a small-cap semiconductor company expected to exceed Q4 guidance . Headquartered in Taiwan, Himax is a fabless semiconductor company, meaning that it designs and sells the hardware for chips, but doesn’t manufacture the actual wafer or chip itself.

Himax Stock Valuation & Momentum

Trading at an extreme discount, Himax possesses an A+ valuation grade, showcasing a forward P/E ratio of 5.47x, a -77.64 difference to the sector, and forward metrics like EV/Sales (1.23x) and EV/EBITDA 5.18x also at extremely discounted levels.

HIMX Stock Valuation Grade (SA Premium )

Despite a challenging political environment between the nations of Taiwan and China, coupled with the U.S. imposing restrictions on the exporting of semiconductors, Taiwan continues to be the leading chip market. Bullish momentum continues pushing Himax on an uptrend, with analysts calling the stock overbought as its price rises. With demand persisting for the industry and positive guidance anticipated, 2023 could spell tremendous results for Himax's profits and growth.

Himax Stock Growth & Profitability

With over 3,000 active patents and a dominant force in the automotive industry, Himax’s Q3 earnings showcased an EPS of $0.17, beating by $0.09, with revenue of $213.63, beating by $14.81M. HIMX had better-than-expected sales, and the company implemented greater inventory control measures in anticipation of a slowdown. Representing more than 35% of sales was HIMX’s auto business, HIMX offers a diversified mix of products which includes imaging and 3D technologies. With plans to introduce an ultralow power Ai batter-operated surveillance camera, HIMX is looking toward the future, and as Himax President & CEO, Jordan Wu said ,

“Partnering with Novatek is a win-win as it allows us to leverage each other’s strength in AI. In addition to both parties' collective years of know-how on panel display and in the emerging enormous AI fields, it also allows us to jointly engage with multiple global vendors for their next-generation product launches…We are proud to be at the forefront of innovation, bringing our WiseEye, embedded with proprietary pre-roll functionality and smart image sensing to lower device power consumption while improving system security and overall user experience at the same time.”

Consider Himax for a portfolio, along with the next stock pick, in Application Software .

7. Model N, Inc. ( MODN )

-

Market Capitalization: $1.55B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 24 out of 659

-

Quant Industry Ranking (as of 1/12/23): 2 out of 213

Offering cloud revenue management solutions to help minimize overpayments and risks involved in payment processing, Model N, Inc.’s ( MODN ) business model is helping curb the price erosion of products for high-tech and life science companies. By implementing artificial intelligent controls, MODN can control price concessions for deals, and its revenue solutions utilize enterprise resource planning (ERP) and customer relationship management ( CRM ) to maximize workflows to help grow revenue.

Model N, Inc. Bullish 1-Year Price Performance

Model N, Inc. Bullish 1-Year Price Performance (SA Premium)

As showcased by its one-year price performance, MODN is on an uptrend, +46%, while also trading at a relative discount. Let’s dive into the figures.

MODN Stock Valuation & Momentum

MODN has strongly bullish momentum with an A+ grade, as its 200- and the 10-day moving average is rising. One of the few tech stocks that experienced a rise in share price in 2022, MODN is trading near its 52-week high of $42.45 per share. Despite this, the stock still is relatively undervalued, posting a C+ valuation grade. Despite less-than-ideal underlying valuation metrics, MODN’s earnings continue to impress, an indication that there may be continued upside with this stock offering solid overall fundamentals, including growth and profitability.

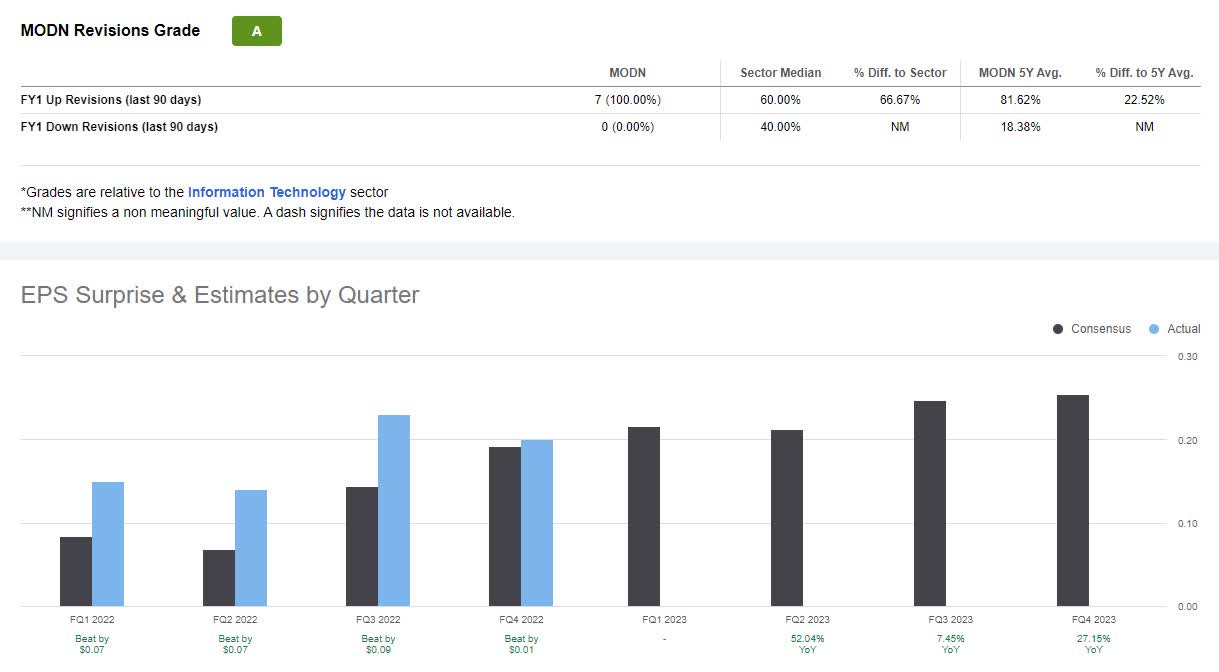

MODN Growth & Profitability

Seven analysts have revised estimates amid tremendous earnings in the last 90 days, bringing its recent B+ revisions grade up to a solid ‘A.’ Model N’s Q4 2022 EPS of $0.20 beat by $0.01, and revenue of $58.17M beat by $1.79M, a year-over-year increase of 13%.

{kind=link}

MODN Stock EPS & Revisions (Seeking Alpha Premium)

Following a record SaaS net dollar rate of 129% for its full year that ended September 30th, MODN President & CEO Jason Blessing said:

"At the start of the fiscal year, we set a target to exit the year at a 20% SaaS ARR growth rate, and I'm pleased to report that we have exceeded this goal. SaaS revenue growth for the full year eclipsed 23% and accelerated throughout the year to 31% in Q4, up seven points from 24% just last quarter. One of the key drivers to our subscription growth has been the fact that Model N provides a high ROI mission-critical solution, which among other things, results in very strong renewal rates."

With cloud computing top-of-mind, MODN is focused on transitioning more clients to this money-maker. Guidance remains strong, with the company consecutively exceeding the top-end of its projections. Subscription and professional services revenues were up $42.9M, and SaaS ARR climbed in Q4 to 31% over the last year, making a case for this quant Strong Buy-rated stock.

8. Harmonic Inc. ( HLIT )

-

Market Capitalization: $1.61B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 11 out of 659

-

Quant Industry Ranking (as of 1/12/23): 1 out of 51

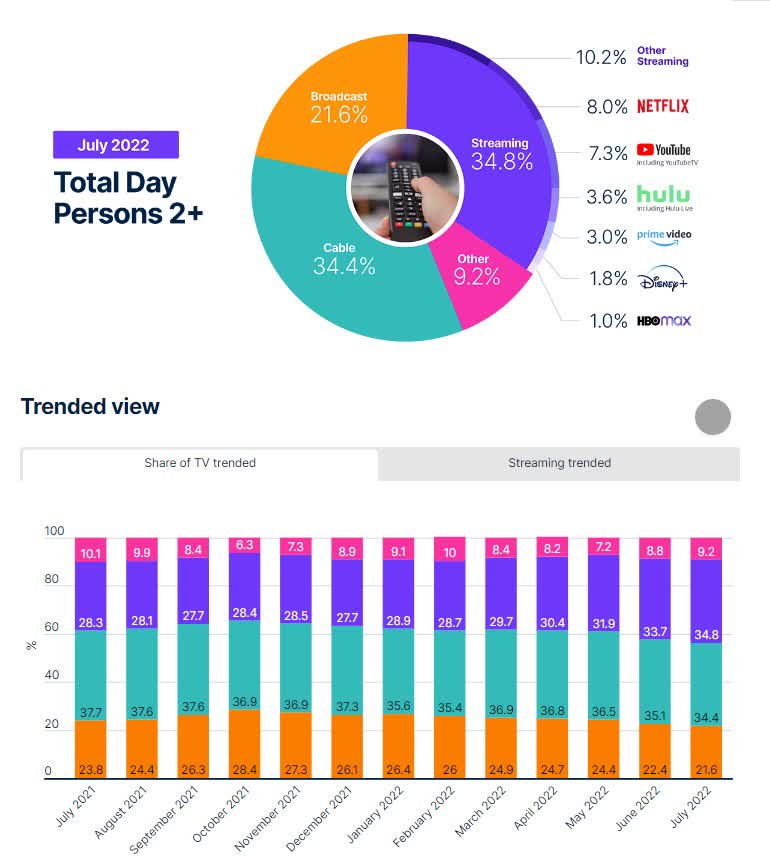

Since my last writing about this stock in November, it has gained +8%, and has continued to be on an uptrend as Jeffries analyst upgrades it to a buy. Although Communications ( XLC ) was one of the worst-performing sectors of 2022 (-32.90%), Harmonic Inc. ( HLIT ), together with its subsidiaries, is a Communications Equipment company in the IT sector, offering video delivery software, products, and services for the streaming world.

{kind=link}

Streaming As Dominant TV Viewing (Nielsen Report)

Streaming is the dominant form of U.S. TV viewing, according to a July 2022 Nielsen report , and HLIT has managed to take advantage, gaining +32% over the last year. With over 5,000 media companies spread across the globe, HLIT provides next-gen technology that has allowed it to profit and grow.

HLIT Stock Growth and Profitability

Ten consecutive top-and-bottom-line earnings beat capitalizing on market trends and excellent business strategies. Harmonic Inc. reported Q3 EPS of $0.13, which beat by $0.03, and revenue of $155.74, which beat by nearly 24% Y/Y. Strong earnings and the popularity of streaming prompted the company to expand its customer footprint to Latin America, EMEA, and APAC, on the heels of high-profile live sporting events. Latin America has one of the fastest-growing streaming markets, so HLIT teamed with DirecTV GO to deliver ultra-fast services.

"Latin America is the second fastest-growing streaming market in the world, and we're excited to help DirecTV GO unlock the power of the cloud while delivering video content to more screens. As DirecTV GO expands its streaming service, our cloud SaaS platform will enable linear channel delivery reliably and at scale, ensuring the best linear experience for subscribers," said Diego Scillama , VP of Video Sales and Services, Latin America, at Harmonic.

HLIT Stock Growth Grade (SA Premium)

Responsible for 20% of Harmonic’s growth figures, HLIT’s video segment is a money-maker, along with its underlying SaaS +69% Y/Y, Cable Access, which produced $81.2M in revenue or +62% Y/Y. Tremendous results have led to a rise in full-year 2022 EBITDA guidance and six analysts' FY1 Upward revisions over the last 90 days. By staying at the forefront of the market, Harmonic continues to meet consumer demand while trading at a relative discount.

Harmonic Inc. Valuation and Momentum

On a bullish trend with shares trading above their 200-day moving average, analysts call the stock overbought as investors actively purchase shares, driving the price higher. With a trailing PEG of 0.09x, a -84.14% difference to the sector, which is heavily weighted relative to its other underlying valuation metrics, the quant ratings indicate the stock is discounted. However, some prudence is required when investing in this stock at its current price, as it is trading near its 52-week high with room for improvement along other valuation metrics. Considering the overall fundamentals of Harmonic, which include A+ momentum, and A’s for EPS Revisions and Growth, this stock is one to consider for a portfolio.

9. Sanmina Corporation ( SANM )

-

Market Capitalization: $3.37B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 16 out of 659

-

Quant Industry Ranking (as of 1/12/23): 1 out of 17

Electric manufacturing services company Sanmina Corporation ( SANM ) offers product designs, engineering, and repair for original equipment manufacturers (OEM). Using advanced technology, SANM provides end-to-end services for supply chain management and logistics in industries that include but are not limited to medical, communications, industrial, and defense & aerospace. With impressive fourth-quarter performance that beat revenue and EPS expectations, SANM’s growth and profitability look promising.

SANM Stock Growth & Profitability

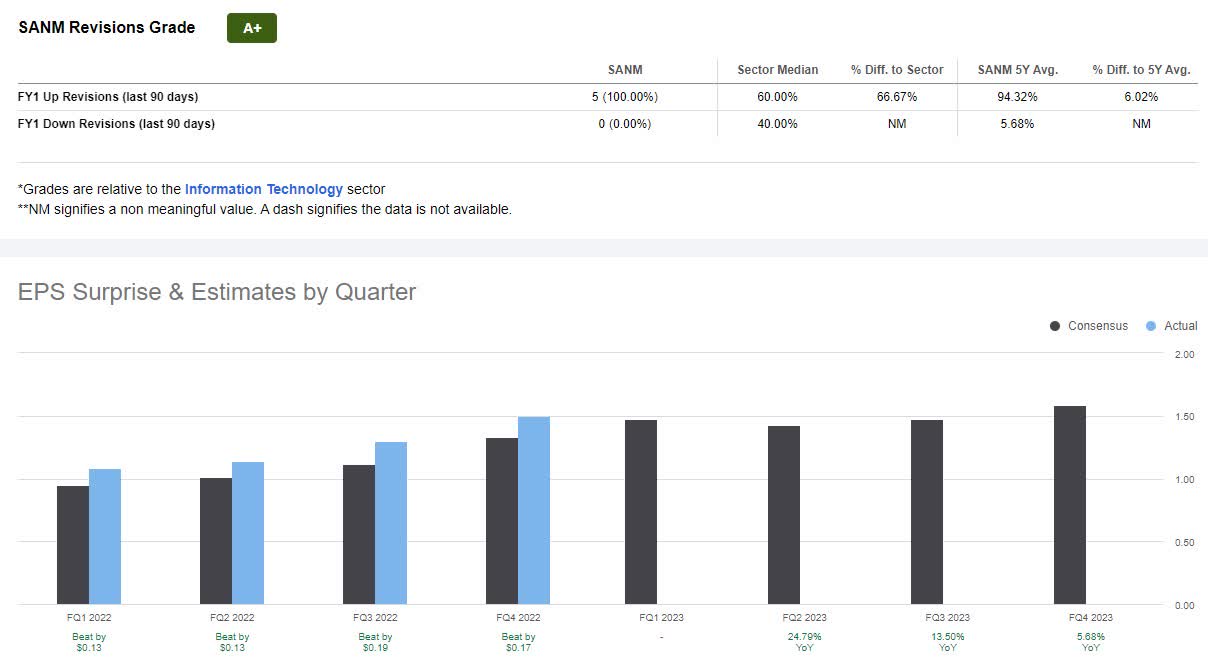

Amid a challenging macroeconomic environment, SANM delivered consistent and robust results that included margin expansion, strong cash flow, and an EPS of $1.50 that beat by $0.17 and revenue of $2.20B that beat by $191.40M (33.98% Y/Y).

{kind=link}

SANM Stock EPS & Revisions (SA Premium)

Showcasing consecutive earnings beats, five analysts revised earnings up within the last 90 days, reflecting an A+ revisions grade. Strong customer demand and relationships with suppliers have helped mitigate any challenges posed. Operating margins improved by 5.3%, and the company has nearly $1.4B of liquidity.

SANM Valuation & Momentum

With a solid outlook and fundamentals, SANM possesses stellar valuation and bullish momentum. With a forward P/E ratio of 11.61x, a -52.53% difference to the sector, and EV/Sales of more than a -80% difference, Sanmina trades at an extreme discount. Up more than 48% over the last year and on a bullish trend, shares are above their 200-day moving average. As investors continue to pay higher prices for shares, and it trends higher, consider this stock for a portfolio, along with our final pick, Fabrinet.

10. Fabrinet ( FN )

-

Market Capitalization: $4.93B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/12/23): 23 out of 659

-

Quant Industry Ranking (as of 1/12/23): 4 out of 17

Headquartered in the Cayman Islands, Fabrinet ( FN ) specializes in precision optical packaging and electronic manufacturing services globally for some of the world’s most demanding OEMs. In addition, FN offers engineering, supply chain management, testing, and integration services.

Quant-rated a strong buy, Fabrinet was recently given a favorable outlook by JP Morgan analyst Samik Chatterjee , citing that “we could see the scenario of [second-half 2023] growth appearing to be robust helped by macro recovery and easier comps.” Trading at a relative discount and possessing bullish momentum, let’s dive into the figures.

Fabrinet Stock Valuation & Momentum

At its current $134.72 per share, FN is trading at a relative discount. Although it's near its 52-week high of $136.08, trailing P/E of 22.77x and PEG of 0.59x indicate the stock is discounted compared to its sector peers. The company has made significant strides in 2022, as noted in the below chart, and its price performance since June of 2022.

FN Stock One-year price performance

{kind=link}

FN Stock One-year price performance (SA Premium)

Up 12% over the last year, FN is continuing its bullish trend. With a 200-day moving average that is upwards-sloping, the stock is outperforming the S&P 500 (-15.55%) and offers excellent grades for growth, profitability, and EPS revisions.

FN Growth & Profitability

With improving profit margins and rapid growth, Fabrinet continues to showcase solid earrings. With consecutive top-and-bottom-line earnings beats, FN’s recent Q1 2023 EPS of $1.97 beat by $0.23, and revenue of $655.43M beat by more than 20% Y/Y. With its diverse markets, seasoned management team, and strong client relationships, Fabrinet continues demonstrating its track record of growth and profitability.

{kind=link}

Fabrinet Stock Consolidated Revenue (FN Stock's Q1 2023 investor presentation)

Although supply chain constraints and a slowdown in the economy could limit growth, strong demand trends are making the overall outlook optimistic. As Fabrinet Chief Executive Officer Seamus Grady said during the recent Earnings Call:

“Looking at the second quarter, we remain optimistic that strong demand trends will continue to drive growth both year-over-year and sequentially after factoring the additional week in the first quarter. We also remain confident that we can continue to realize incremental operating efficiencies as revenue grows faster than expenses. In summary, we had a strong first quarter with results that exceeded our guidance. We are optimistic about continued demand in our markets, and we’re well-positioned to extend our track record of success as we look ahead.”

Despite economies anticipating a slowdown amid high inflation and geopolitical impact worldwide, each of my stock picks offers a unique risk-reward opportunity that is quite favorable. Consider each in creating a portfolio.

Conclusion

As investors look to the future and the Fed works to tame inflation, consider our top ten tech stocks, SMCI, TSM, AMKR, ON, ACLS, HIMX, MODN, HLIT, SANM, and FN, for the new year. These recommendations possess robust fundamentals – better than most of the beaten-down mega-tech stocks that were historically driving the Nasdaq and S&P 500.

Many of the above-mentioned picks have better growth rates and valuation frameworks, and showcase profitability metrics, rising earnings revisions, and strong fundamental tailwinds. Seeking Alpha’s quant ratings and investment research tools helps to ensure you are furnished with the best resources to make informed investment decisions. We have other technology stocks with strong buy recommendations and larger market caps that can be found in our ranking of Top Technology stocks . Consider creating Stock Screens to suit your specific investment objectives, or browse some of our other Top Rated Stocks if those mentioned here do not fit your investment preferences.

For further details see:

Top 10 Tech Stocks For 2023