MDLZ - Top 2024 Picks From Beaten Down Sectors To Create Passive Dividend Income

2023-12-04 14:01:04 ET

Summary

- Treasury Rates receded in November, leading to a rebound in equities, particularly in interest rate-sensitive sectors like utilities and real estate.

- The market anticipates that the Fed will maintain its pause on rate hikes in December and January, with a possibility of rate cuts coming much sooner than originally thought.

- It's time to make a move to build your passive income in these beaten-down dividend names as November gave us a taste of how hard and swiftly they can rally.

Written by Nick Ackerman.

With Treasury Rates receding this past month, equities (and fixed-income) can rebound from some of the pressures in the prior two months. In fact, the November rally saw broader participation.

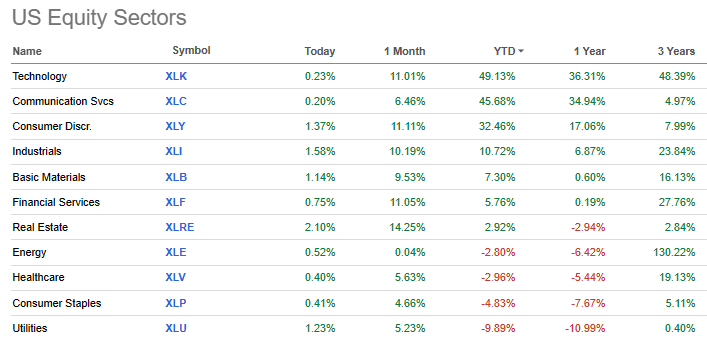

That includes the beaten down interest rate sensitive sectors such as utilities and real estate finally getting some relief. The Real Estate Select Sector SPDR Fund ETF ( XLRE ) last month was down up now 2.92% YTD, erasing all losses for the year. Utilities Select Sector SPDR® Fund ETF ( XLU ) was down -9.89%, but while still down saw a dramatic cut to their losses.

Equity Market Sector Performance (Seeking Alpha)

{kind=link}

This rally was helped, driven primarily by the CPI report that showed inflation was continuing to trend lower and came in flat for the month of October . There is even discussion that deflation could be a possibility before too long, which deflation comes with its own problems. Of course, that might be getting ahead of ourselves, but that didn't stop the market from anticipating that there will be no more increases from the Fed.

The market expects at the December Fed meeting that there is a 100% chance the Fed maintains their pause, which means the current 525 to 550 basis point range. This is the same for January 2024, as we enter the new year. In March 2024, we start to see that the probability of the Fed cutting first shows up. There is a 28% probability that the Fed would cut 25 basis points.

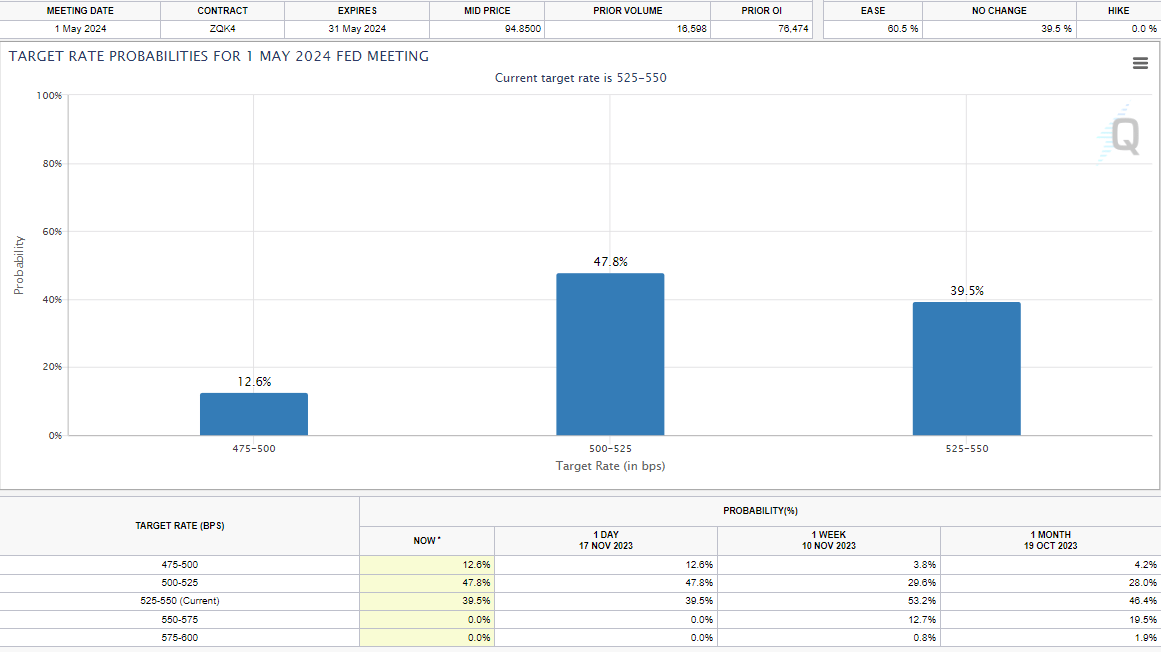

What is really surprising is when we get to the May 2024 Fed meeting, which now has a higher probability chance of 47.8% that the Fed will have to cut by 25 basis points, compared to 39.5% expecting rates to stay in the 525 to 550 range. That leaves another 12.6% that believe a 50 basis point cut could be on the table. That's quite the change because only a week ago, the probability was still in the cards for a 25 basis point hike. Albeit a fairly slim chance, but a chance nonetheless.

Fed Rate Target Expectations May 2024 Fed Meeting (CME FedWatch Tool)

{kind=link}

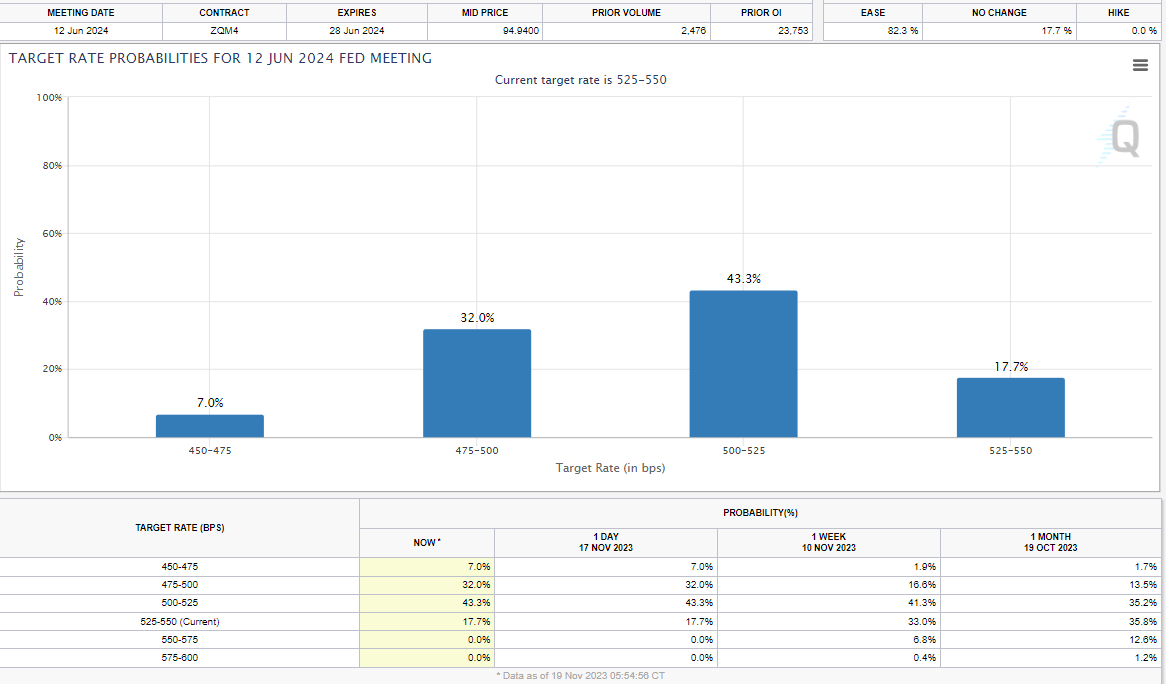

By the June 2024 meeting, the market is pricing in that the chance for a cut between 25 to 75 basis points from current levels is highly expected.

Fed Rate Target Expectations June 2024 Fed Meeting (CME FedWatch Tool)

{kind=link}

Of course, take this with a grain of salt because literally, ANYTHING could happen in this period. All it would take is one CPI report that's a bit hotter than expected, and raises could be back on the table. However, this is what is driving the market to rally this month.

We are also entering the time of year when the market generally tends to trend higher. November has historically been the strongest month of the year since 1950, and then we get into the Santa Claus rally at the end of December. So, given historical trends - and the fact that 2023 had been following those trends in September and October - we could be set to finish off the year strong.

What's a bit interesting about this year is that the S&P 500 Index itself is up so strongly, but it's been tied to only a very narrow set of stocks, the Magnificent 7. While there has been broader participation for this month, those 493 other stocks in the index still aren't even close, with the Invesco S&P 500® Equal Weight ETF ( RSP ) lagging far behind.

YCharts

The theme of potentially seeing rate cuts and, thus, lower risk-free rates would continue to bode well for utilities, real estate and REIT investments. Utilities and REIT investments often contend with Treasuries as income-oriented investments. They often have high relative debt loads, which means when their debt is coming due for refinancing, they are facing steeper yields.

The consumer staples sector is looking appealing as it was also beaten down this year with higher inflation, causing the cost of goods to rise. That then comes with the knock-on effect of pushing those companies to increase the prices of their products.

In particular, I follow mostly food packaging companies, and those names have been having a tough time this year, with volume dropping at most of these companies. However, that excludes Mondelez ( MDLZ ), which was able to buck that trend and see higher volume in its latest quarter.

With the 10-Year Treasury Rate (US10Y) giving up some of its gains after surging the last couple of months, we've already got just a taste of the rebounding these sectors can do.

YCharts

With that being said, here are several choices that I believe represent considerations at this time. Even if rates stay higher, I believe these are solid long-term investments, regardless of whether they face short- or medium-term headwinds of higher rates. Of course, if rates do come down as the probabilities show, then that would be a continued tailwind for these names.

WEC Energy Group, Inc. ( WEC )

WEC is a multi-utility company with operations through subsidiaries throughout Wisconsin, Minnesota, and Michigan, as well as parts of Illinois. The company has delivered a strong trend of earnings growth over time that has allowed the company to grow its dividend for 20 years in a row as well.

WEC Dividend History (Seeking Alpha)

{kind=link}

The current yield is at 3.82%, with expectations that the company will grow the dividend around 6.5% to 7% going forward, as they noted it should be in line with earnings growth. Shares currently trade well below their fair value range historically, which is expected with interest rates rising. However, as we saw rates come down, the shares started to rebound, and that should continue.

WEC Fair Value Range (Portfolio Insight)

{kind=link}

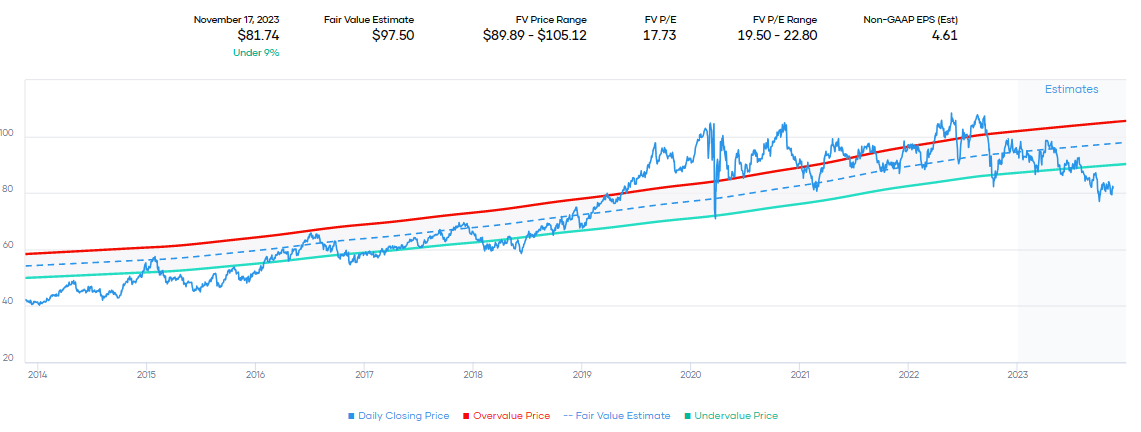

NextEra Energy, Inc. ( NEE )

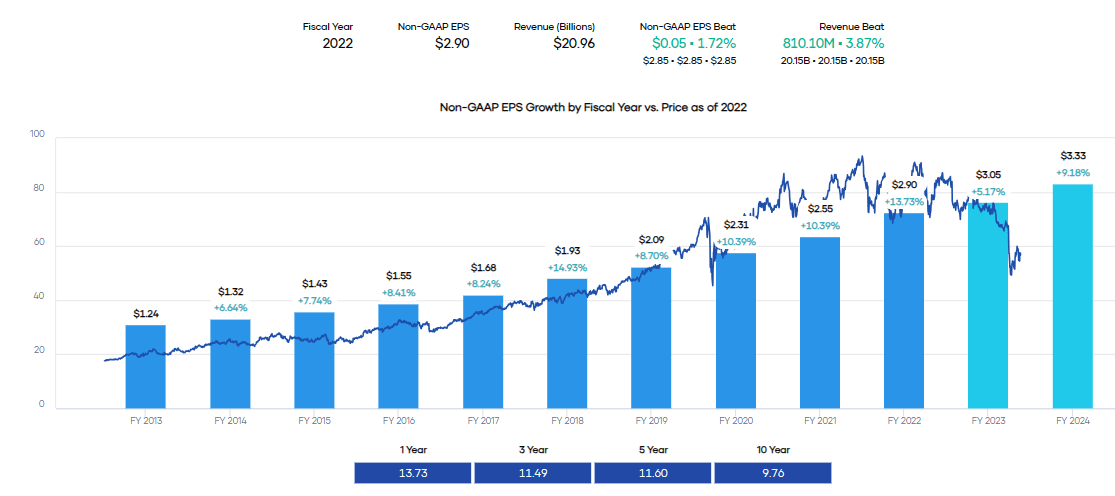

Despite NEE getting a fair value downgrade from Morningstar recently from $82 to $74 based on lower regulated allowed returns, shares trade substantially below the target level. This utility company is also facing additional pressures outside of just interest rate sensitivity as its growth engine, NextEra Energy Partners, takes a tumble. Earnings growth for this company has been strong.

NEE Earnings History (Portfolio Insight)

{kind=link}

The company also noted that they don't expect a slowdown for NEE, despite NEP having to cut its growth significantly earlier in the year. Here's what they had to say for NEE in their last earnings call :

Turning now to our third quarter 2023 consolidated results, adjusted earnings from corporate and other decreased by $0.01 per share year-over-year. Our long-term financial expectations remain unchanged. We will be disappointed if we are not able to deliver financial results at or near the top end of our adjusted EPS expectation ranges in each year from 2023 through 2026.

From 2021 to 2026, we continue to expect that our average annual growth and operating cash flow will be at or above our adjusted EPS compound annual growth rate range, and we continue to expect to grow our dividends per share at roughly 10% per year for at least 2024 off a 2022 base. As always, our expectations are subject to our caveats.

Adjusted EPS growth is expected to be in the range of 6-8% over the next few years. That's about in line with where WEC also expected their earnings growth to come in.

NEE EPS Growth Expectations (NextEra Energy)

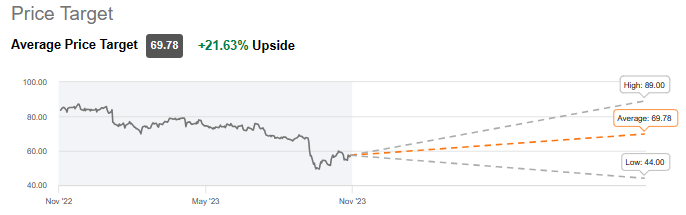

Despite the challenges, the company is still highly popular on Wall Street, with significant potential upside.

NEE Average Price Target (Seeking Alpha)

{kind=link}

NEE currently sports a 3.26% dividend yield that has been growing for the last 27 years. With the plummeting share price, the forward P/E has also come down substantially to just 18.35x. That might appear expensive, but it is off from the nearly 30x the shares traded at the beginning of 2023.

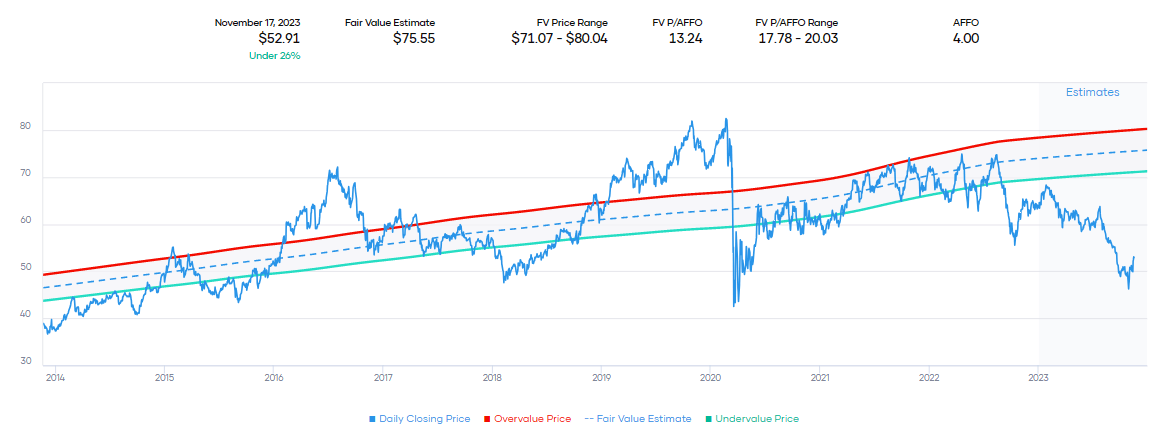

Realty Income Corporation ( O )

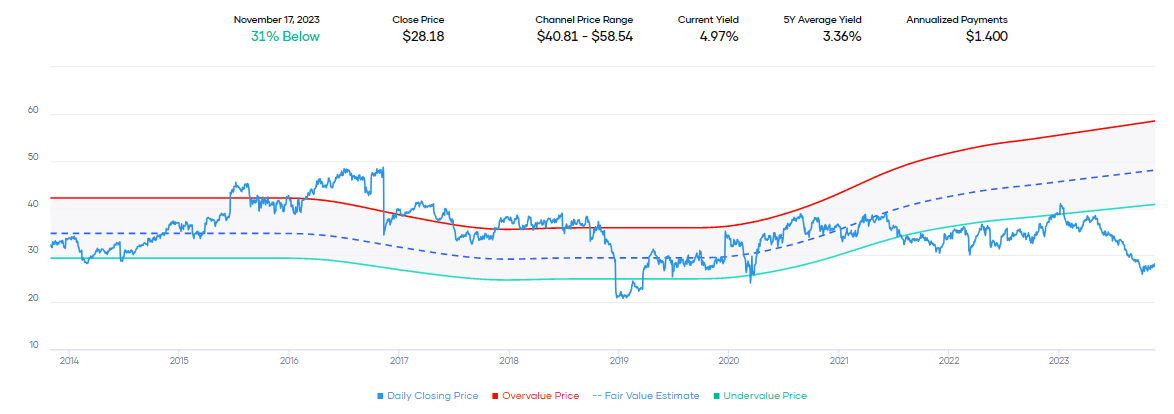

Turning to REITs, I would continue to find O attractive at this time. Again, this wasn't all interest rate driven. Instead, this REIT announced an acquisition of Spirit Realty Capital ( SRC ) recently, and investors initially panicked and sold it down massively. We took that opportunity to write deep out of the money puts, and those paid off nearly immediately as shares ripped higher. They rebounded from the acquisition announced fueled drop and even more. Still, shares of O trade at a deep discount to its historical fair value range. I'd say that it is pricing in the higher interest rate environment and then substantially more.

O Fair Value Range (Portfolio Insight)

{kind=link}

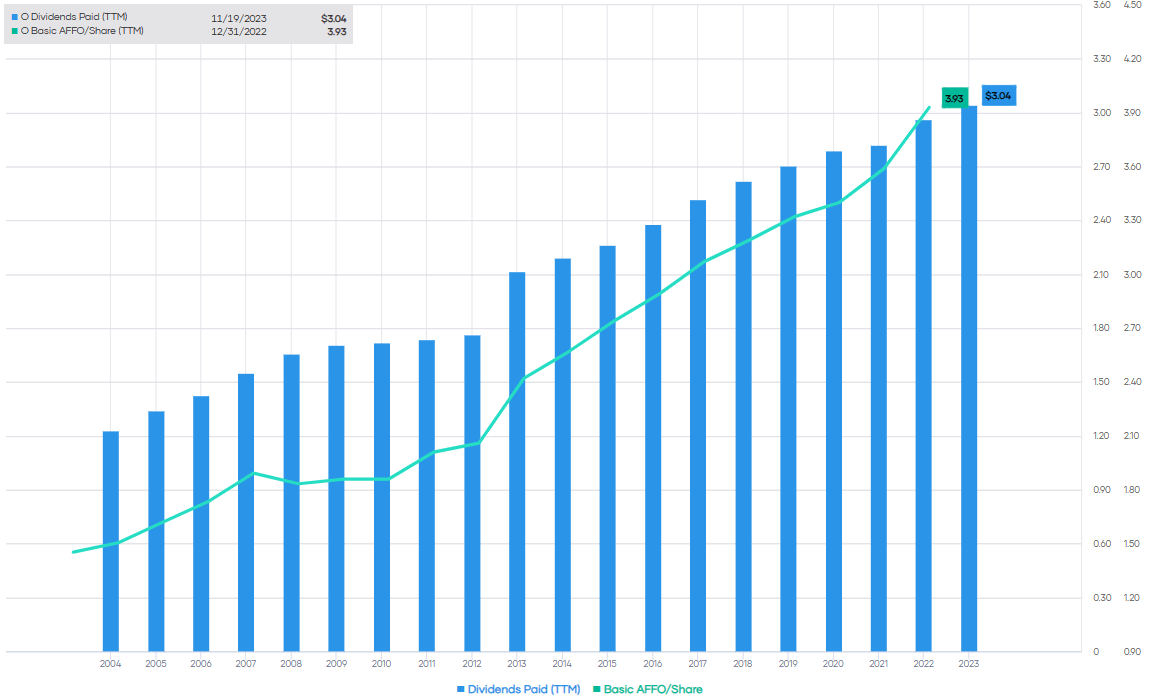

At a 5.81% yield, O is still a solid income generator that pays a monthly dividend. They coined themselves as "The Monthly Dividend Company," and they've delivered for decades - boasting "640 consecutive common stock monthly dividends throughout its 54-year operating history..." In addition to that, they've grown the dividend for 104 consecutive quarters, or nearly 9 years. With the expectation of adjusted funds from operations, or AFFO, hitting $4 this year, the dividend is well covered, and the accretive acquisition of SRC should see that coverage become even stronger.

O Dividends Paid vs. AFFO Per Share (Portfolio Insight)

{kind=link}

As an all-stock deal, there is no new capital being raised to consummate this O/SRC marriage. That's attractive, as reducing debt should be a focus in a higher-rate environment. In fact, they noted that the SRC deal should help in that department, as it was highlighted as one of the benefits.

Expect to benefit from Spirit's $4.1 billion(1) of debt with weighted average cost of 3.48% and term of 4.9 years and $173 million of freely-callable 6.00% preferred stock

Conagra Brands, Inc. ( CAG )

Finally, I wanted to highlight CAG as a potentially attractive name to consider for the long-term and even short-term should rates be cut heading into 2024. This name never seems to quite get any respect for its brands, and that was noted with Morningstar recently slashing its fair value estimate. They took it down from $46.50 to just $33 - albeit shares are still trading below that level, so it could still suggest some upside.

CAG has had to increase its prices dramatically, like most packaged food companies. The last quarter showed that even the price increases weren't enough to offset the volume declines and clearly showed that they are facing challenges in their business. This was for their Q1 fiscal 2024 results.

The 0.3% decrease in organic net sales was driven by a 6.6% decrease in volume largely due to industry-wide slowdown in consumption and recent consumer behavior shifts, partially offset by a 6.3% improvement in price/mix.

Fiscal 2024 earnings are expected to decline slightly, according to analysts' consensus. On the other hand, the company is guiding for adjusted EPS between $2.70 and $2.75. Fiscal 2023 adjusted EPS came in at $2.77, so we could be seeing an essentially flat earnings year.

With the additional pressures from interest rates that pushed down the share price, that, of course, led to the yield rising dramatically. At this time, it would suggest there is a significant upside for shares of CAG.

CAG Fair Value Range (Portfolio Insight)

{kind=link}

The company is not richly priced at a forward P/E of just 10.53x, which factors in the relatively lackluster expected growth (or lack thereof). Any positive news and the tailwind of lower rates could cause shares of Conagra to continue to rebound significantly into the short term. They've also been looking to reduce their debt and leverage ratio, with net debt of 3.55x as of their latest quarter, down from 3.9x a year ago.

For further details see:

Top 2024 Picks From Beaten Down Sectors To Create Passive Dividend Income