ALGM - Top 5 Stocks For Earnings Season

2023-04-19 06:00:05 ET

Summary

- Expect the unexpected has been a theme over the past two years as economies continue to fend off recession.

- From the global pandemic to the war in Ukraine, a banking crisis, insane inflation, swings in oil, and OPEC+ production cuts, investor sentiment is back and forth.

- Investors want to know where to invest. In this uncertain environment, it’s crucial to identify stocks where crowdsourced professional analysts anticipate that a company can deliver on earnings.

- Notably, amid macro pressures, some companies have beaten earnings expectations, weathering the storms and rallying during good and bad times.

- Consider five stocks using SA’s data-driven Quant Rating System, drawing on the best collective characteristics of analysts' earnings revisions, valuation, growth, profitability, and momentum.

Is A Recession Coming in 2023?

I previously wrote about expecting the unexpected, as 2022 was the year of volatile price swings that gave way to talks of recession. In light of the March Fed Minutes ’ indication of a “mild recession” starting later this year as a result of the banking crisis and credit downturns, it's crucial to consider investing in companies with strong fundamentals, able to generate stable and consistent free cash flow with strong capital structures and little debt. Notably, as investors need to consider how the economy will impact stocks, it is essential not to disregard what’s working and where professional analysts have tremendous confidence that a company can deliver results.

2-year Treasury Surge and Plenty of Volatility

2-year Treasury Surge and Plenty of Volatility (Mohamed A. El-Erian, Bloomberg)

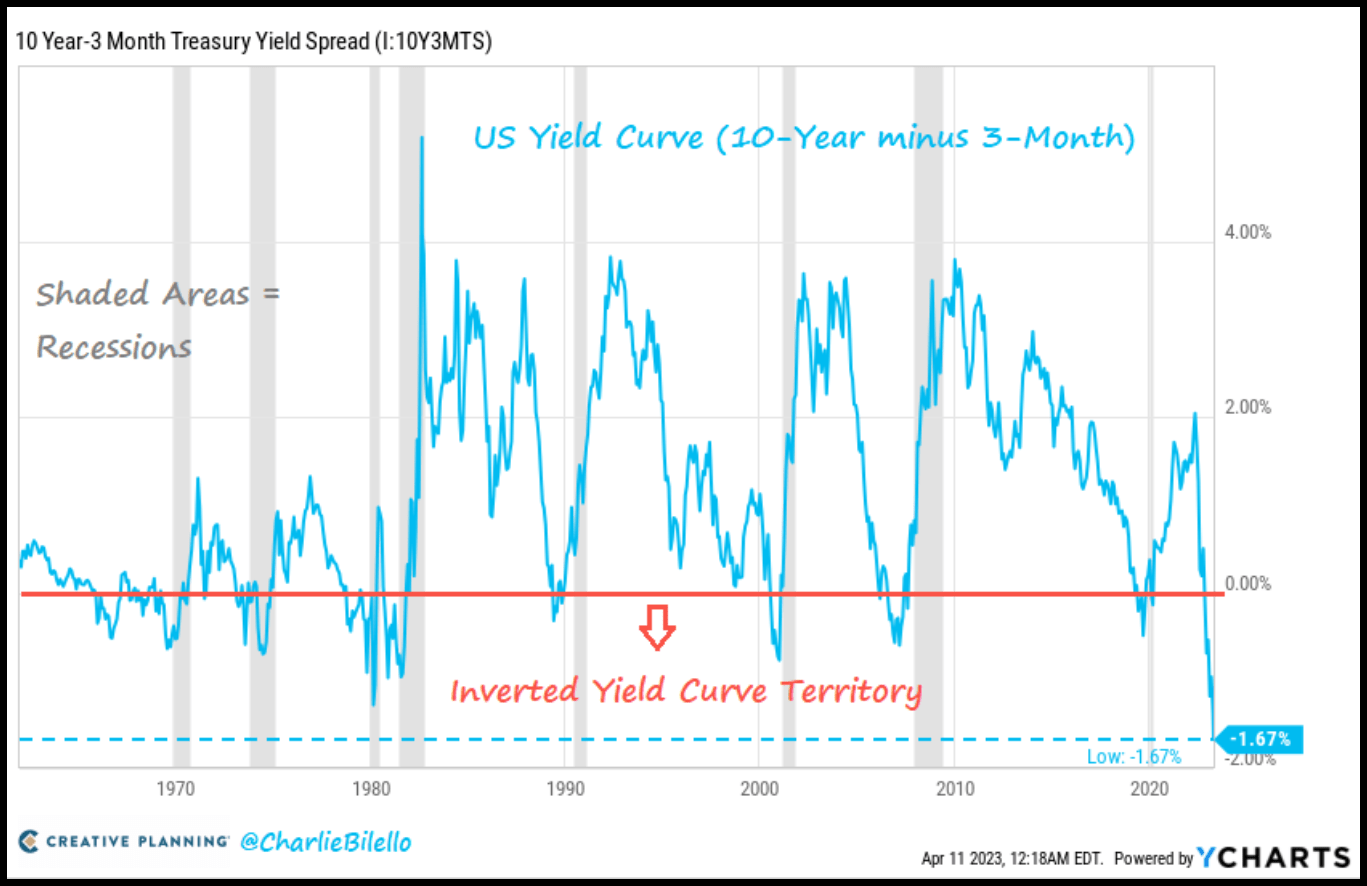

Despite the latest CPI figures indicating some signs of moderation, there’s been substantial volatility regarding the yield spreads. An official recession, as determined by the National Bureau of Economic Research, is projected to happen in the next twelve months. On average, when the yield curve spread between the 10-year and two-year Treasury goes negative – or inverts – a recession occurs within 12 to 18 months.

{kind=link}

10 Year-3 Month Treasury Spread & Inversions (Charlie Bilello)

While inverting for about a week in April 2022, it stayed inverted in July 2022, indicating that by December 31, 2023, we could be in a recession. Consider also the following precursors for impending recession:

-

The banking crisis

-

Banks shutting down credit to commercial and retail customers adds to contractionary pressures on businesses and consumers.

-

The above 10 Year-3 month Treasury spread inversion in the fourth quarter – the most inverted it has ever been beyond since 1980 and ‘81.

-

Tightening financial conditions

-

The Fed increasing rates and reducing its balance sheets

-

Soaring credit card defaults

-

Homeowners are unable to pay their mortgages

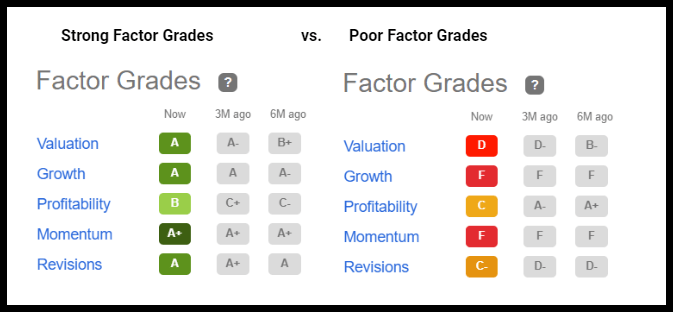

Headwinds like the aforementioned give investors the opportunity to prepare, especially with Earning season at hand. Having the tools to focus on companies that can withstand significant headwinds and are profitable is a great way to hedge against a recession. Those companies that possess vital collective metrics, highlighted by Seeking Alpha’s Factor Grades, which rate investment characteristics on a sector-relative basis, are important.

{kind=link}

Strong Factor Grades vs Poor Factor Grades (SA Premium)

While cash may be king in some instances, putting cash to work can allow for investment in companies that have continued their growth and profitability amid headwinds. As inflation eats away at portfolios, these companies can prove beneficial. As such, I’ve selected five stocks that have done just that and possess strong factor grades for the earning season, along with positive analysts' earnings revisions. Wall Street analysts are increasingly optimistic about these companies and have revised their earnings estimates, which we will indicate below.

5 Stocks For the 2023 Earnings Season

Talks of recession, softening inflation, and increases in jobless claims have increasingly made the Fed’s job more difficult, especially when you factor in geopolitical tensions and OPEC’s oil cuts. With the oil production cuts, we will likely see another fuel price surge. In gearing up for potential headwinds, we’ve selected five stocks to consider for the 2023 earnings season. Our quant ratings highlight strong buys amid storms and collectively take the best in collective metrics.

1. Allegro MicroSystems, Inc. ( ALGM )

-

Market Capitalization: $8.30B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 4/18): 3 out of 592

-

Quant Industry Ranking (as of 4/18): 1 out of 68

One of my favorite industries offering growth tech stocks, I’ve selected Allegro MicroSystems, Inc. ( ALGM ), a semiconductor company. Not only has Allegro maintained bullish momentum as other growth stocks have been pummeled over the last two years, but ALGM also experiences robust growth , having consecutively beaten consensus earnings estimates.

Allegro has capitalized on the demand for electric vehicles (EVs), one of its top-performing segments. As a global leader in application-specific algorithms focused on power and sensing solutions, Allegro is focused on the secular trend of e-Mobility and expanded its applications to a record 43% of Q3 auto sales.

Allegro is the top-ranking stock in the semiconductor industry , despite shares trading at a premium valuation. The valuation framework is crucial when buying stocks to assess whether a stock is over- or undervalued based on its current price. Although ALGM’s valuation is a bit stretched, evidenced in its ‘D’ grading, its all-important underlying forward PEG of 0.74x is grade-A. Compared to the sector median of 1.68x, ALGM is offering a 55% discount.

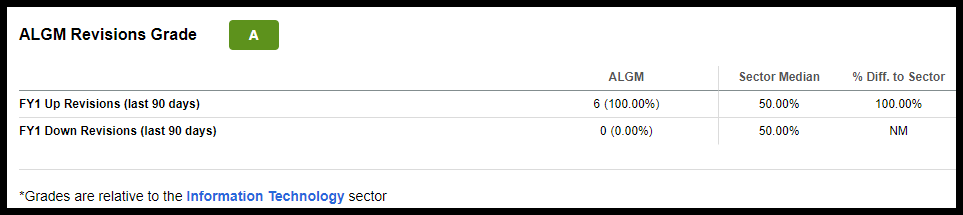

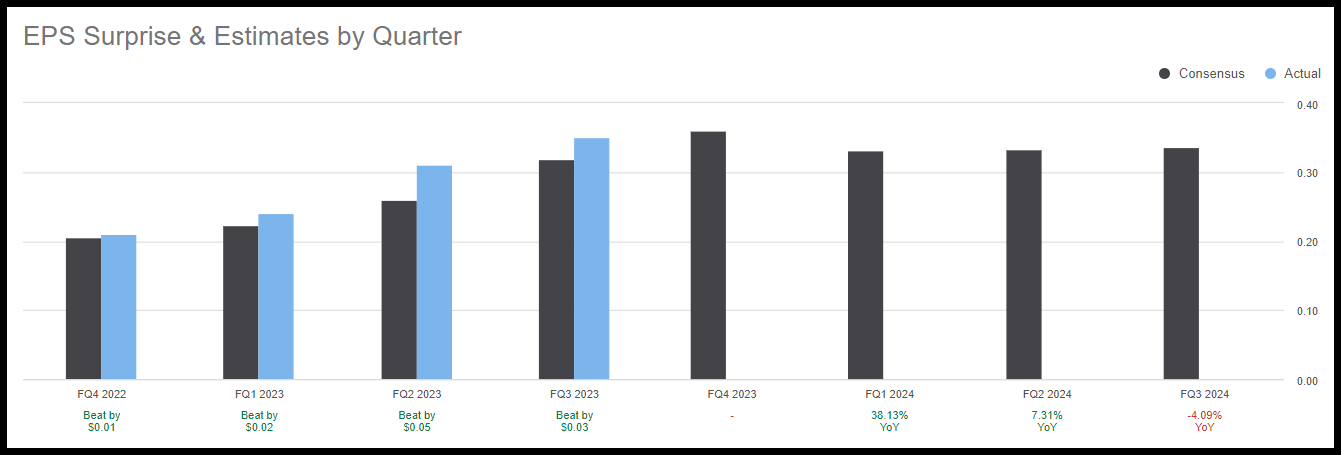

When you factor in tremendous growth grades supported by consecutive top-and-bottom line earnings beats, ALGM is a ‘Strong Buy’ stock. In addition to near-high Q3 earnings, which include EPS of $0.35 that beat by $0.03 and revenues beating by 33.31% Y/Y, ALGM had gross margins of 58% resulting in six FY1 Up revisions over the last 90 days.

ALGM experienced 6 analysts’ upward revisions and 0 downward

{kind=link}

ALGM experienced 6 analysts’ upward revisions and 0 downward (SA Premium)

ALGM Has Consecutively Beaten Estimates Over Multiple Quarters

{kind=link}

ALGM Has Consecutively Beaten Estimates Over Multiple Quarters (SA Premium)

Growth driven by momentum in the e-mobility segment and industrial markets allowed sales to increase 11% sequentially and 56% Y/Y, and EV production is projected to jump another 50% increase in fiscal 2023. While currency fluctuations may hurt some companies, ALGM has benefited, expanding its margins to deliver record Q3 operating margins of 30%. Looking to the future, during the Q3 Earnings Call, Allegro CFO Derek D'Antilio said,

“Turning to our Q4 outlook, we expect sales in the fourth quarter to be in the range of $260 million to $270 million, and at the midpoint of this range, we are projecting a full-year sales increase of 26%. We expect Q4 gross margins to be approximately 57%. And expect operating expenses to be between 27% and 28% of sales.”

Strong words from its executive team, which expects to see continued upside from its one-year share price that’s +81%. Consider this stock for a portfolio, along with my next pick that has gone from Hold to Strong Buy.

2. Salesforce, Inc. ( CRM )

-

Market Capitalization: $197.08B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 4/18): 13 out of 592

-

Quant Industry Ranking (as of 4/18): 4 out of 213

I recently wrote about cloud-computing Salesforce’s Return of the Jedi comeback, given its dominant presence as a Mega-Tech stock that went from boom, to Hold, back as a Strong Buy quant-rated stock. Maintaining tremendous profitability and gross margins of 73%, Salesforce’s $7B in cash from operations offers a cushion, should the rumors of a potential recession play out.

Salesforce continues to make structural changes in management and its business model, which has prompted shares of the stock to rise. Following strong Q4 results that sent the stock up 15% before its release, Evercore ISI analyst Kirk Materne wrote :

"Importantly, [fiscal 2024] operating margin guidance came in at 27%, or [roughly 450 basis points of year-over-year] expansion vs. our/Street estimates of [roughly] 23%/22.9% as activist pressure to improve profitability remains prevalent, and management has clearly gotten the message"

Salesforce Q4 Revenue Segments (CRM Q4 2023 Investor Presentation)

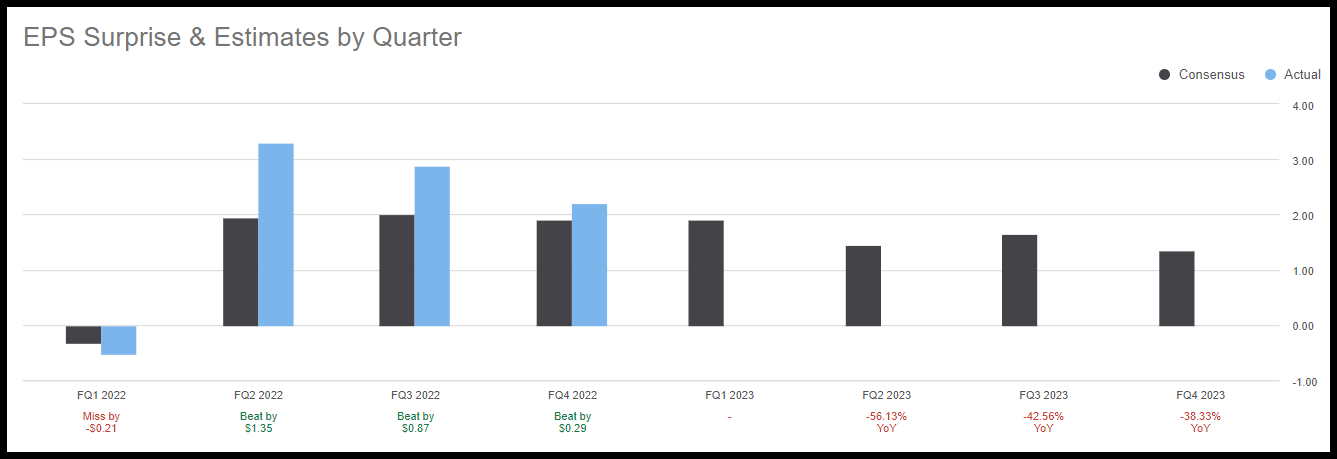

In the same publication, Needham analyst Scott Berg upgraded Salesforce to buy amid its strong outlook on the heels of EPS of $1.68, beating by $0.32, and revenue of $8.38B, beating by $391.62M.

Salesforce Beats Expectations For the Quarter

Salesforce Beats Expectations For the Quarter (SA Premium)

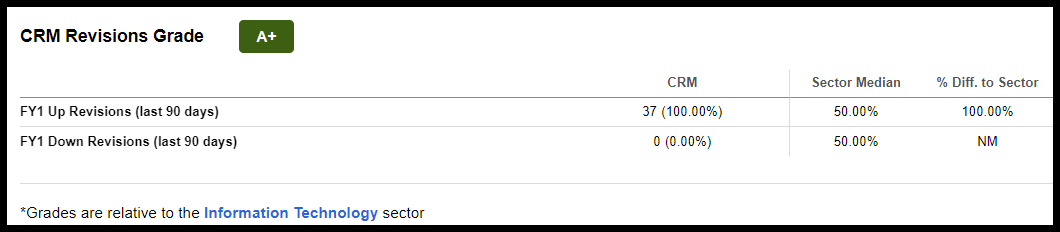

Salesforce Experienced 37 Analysts' Upward Earnings Revisions and 0 Down

{kind=link}

Salesforce Experienced 37 Analysts' Upward Earnings Revisions and 0 Down (SA Premium)

With operating margins above forecasts and delivering +$31B in revenue for the full year, the CRM king has made quite the comeback and maintains bullish momentum. Despite its valuation being priced at a premium, CRM’s forward PEG ratio of 1.13x is a B+, trading at nearly a 33% discount from its peers. Consider Salesforce for your portfolio, along with my next pick looking to take advantage of oil and gas prices.

3. Par Pacific Holdings, Inc. ( PARR )

-

Market Capitalization: $1.48B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 4/18): 6 out of 249

-

Quant Industry Ranking (as of 4/18): 2 out of 23

Houston, Texas-based energy company Par Pacific Holdings is “fueling excellence” with sustainability in mind. An energy company that operates in three segments: Refining, Retail, and Logistics, PARR’s integrated downstream network is focused on bringing energy and infrastructure from its diverse locations and operations, primarily to Hawaii.

Par Pacific Holdings Locations (Par Pacific)

With a discounted valuation highlighted by a forward P/E ratio at a -50.56% difference to the sector, forward EV/Sales, and Price/Sales more than an -83% difference to the sector, PARR is undervalued. Factor in its longer-term uptrend that has experienced a gradual incline in quarterly momentum has allowed it to rebound from pandemic lows while remaining strong as analysts revise estimates up.

Par Pacific Experienced 5 Analysts' Upward Earnings Revisions and 0 Down

Par Pacific Experienced 5 Analysts' Upward Earnings Revisions and 0 Down (SA Premium)

PARR had an excellent fourth quarter after already crushing the previous quarter’s results. A fourth-quarter EPS of $2.20 beat by $0.29, and revenues beat by nearly 40%. PARR strengthened its cash on hand and balance sheet and paid down nearly $65M in debt.

PARR Crushes Earnings for three consecutive quarters

{kind=link}

PARR Crushes Earnings for three consecutive quarters (SA Premium)

Despite declines in natural gas prices, with the reopening of China, jet fuel demand and air travel increased. PARR’s YTD share price is up 12%; over one year, its price performance is +58%. PARR is a ‘Strong Buy’ stock that continues to capitalize on its breakthrough year, repurchased $8M in stock, and generated +$450M in cash from operations. As its CFO, Shawn Flores, said during the Q4 Earnings Call , “As a growth-oriented company, we will continue to identify attractive development opportunities to enhance our integrated supply network across our core markets.” For similar reasons, investors should consider identifying attractive opportunities for investment to enhance their portfolios, including my next two picks.

4. Fastly, Inc. (FSLY)

-

Market Capitalization: $1.97B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 4/18): 19 out of 592

-

Quant Industry Ranking (as of 4/18): 2 out of 26

Cloud-based platform Fastly, Inc. (FSLY) delivers the optimized speed, security, and scale businesses want for their websites. With a discounted valuation that includes a forward Price/Book of 2.19x at a 40% difference to the sector and bullish momentum, Fastly’s consistent revenue growth and cutting-edge technology are quickly moving this company to the forefront of the digital world. Because of its modern approach to content delivery, revenues have advanced, given the organic growth of existing customers and new customers that have increased their spending levels. Fastly’s enterprise customers spend more than $100,000 annually – the big money drivers.

As the stock trends higher, Fastly boasts a superior tech network and delivery that outperforms the competition. Its advanced capabilities have proven to generate more revenue streams, especially from its Edge Computing , which allows the processing of data closer to its end users even faster, giving an advantage over Content Delivery Networks (CDNs).

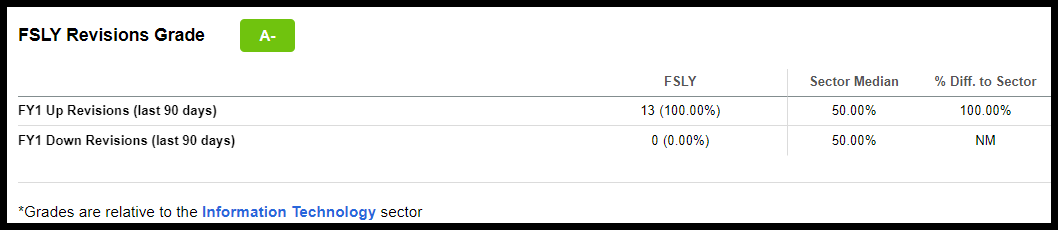

Fastly Experienced 13 Upward Revisions and 0 Down

{kind=link}

Fastly Experienced 13 Upward Revisions and 0 Down (SA Premium)

Having already crushed earnings on a consecutive basis, FSLY is up 100% YTD. With an A- revision grade as 13 analysts revised up over the last 90 days, and Q4 EPS of -$0.08 that beat by $0.05, and revenues that beat by 22%, with market expansion, FSLY should experience increasing margins as it adds greater value and operating leverage for customers, who will likely add and upgrade their security products, another bonus for Fastly. Although Fastly has more debt and less cash from operations than my other picks, the company’s market capitalization of $1.97B, revenue generation, and the decision to avoid the return of capital to shareholders is allowing it to have a solid balance sheet. With its strategic 2020 acquisition of Signal Sciences to offer more security solutions, we believe Fastly is well positioned to continue in a positive direction, cementing a competitive advantage over its rivals. Consider this stock for your portfolio and my final pick, a well-known energy behemoth.

5. Marathon Petroleum Corporation (MPC)

-

Market Capitalization: $57.10B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 4/18): 3 out of 249

-

Quant Industry Ranking (as of 4/18): 1 out of 23

Saving the best for last, oil and gas behemoth Marathon Petroleum Corp. (MPC) is back on an uptrend, capitalizing on the “golden age of refining.” Refining products are posting some of the highest seasonal demand in five years. BofA Managing Director Head of US Oil and Gas Doug Leggate said ,

"We find a single trend for all names under coverage: record 1Q23 earnings for what is normally the lowest seasonal earnings of the year and a set-up we see potentially supporting continued strength in the run-up to the driving season."

As refiners capitalize on gains, despite concerns of crude oil losing steam , Marathon has not lost momentum. Volumes of MPC are trending higher as the stock posts a YTD +16% and a one-year price performance of +49%.

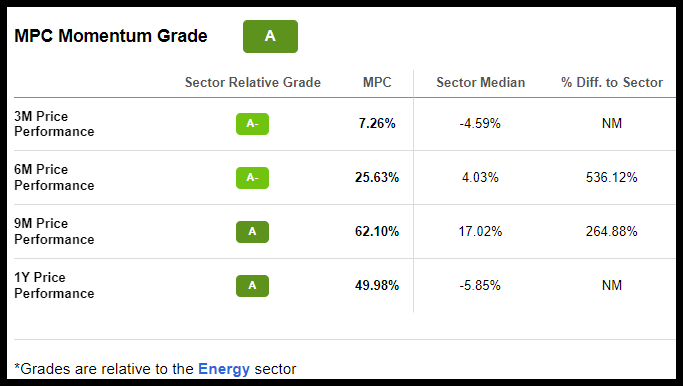

{kind=link}

MPC Stock Momentum Grade (SA Premium)

Although the stock trades near its 52-week high of $138 per share, its price is still undervalued. With an overall ‘C+’ valuation grade supported by a forward P/E ratio of 6.23x versus the sector median of 9.14x and a trailing PEG ratio difference to the sector of -92%, this stock has upside potential. When you factor in Marathon’s tremendous growth and profitability, allowing it to maintain its dividend safety and regular payouts, investors can appreciate the ability to offset some of the inflation eating away at portfolios.

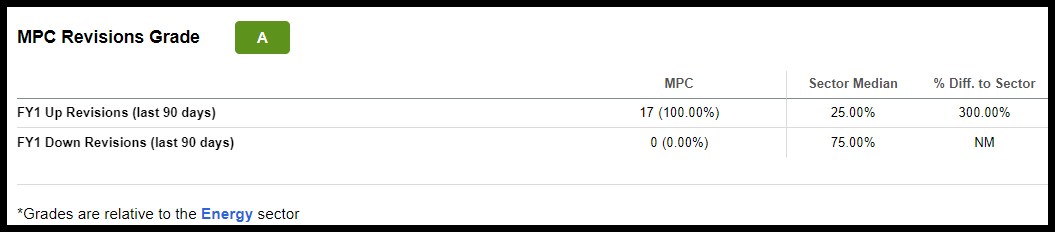

Marathon has experienced 17 analysts' upward revisions

{kind=link}

MPC Stock Revisions Grade (SA Premium)

When you factor in consecutive top-and-bottom line earnings beats that resulted in 17 FY1 Upward revisions from analysts over the last 90 days and an EPS of $6.65 that beat by $1.02, and revenue of $40.09B beat by more than 12% Y/Y despite a challenging environment, look no further than the energy company whose name coincides with its long-running operations and ability to create the largest U.S. refiner to diversify its footprint and optimize supplies.

The key with these companies is finding those with strong fundamentals and the ability to consistently deliver returns, regardless of market conditions. Although the markets have been volatile and recession indicators have all but guaranteed we’ll see one in the near future, stocks with healthy balance sheets and lower debt levels, generating strong free cash flows, are likely to be the most profitable. Look for profitable companies which offer a cushion during downturns. Consider ALGM, CRM, PARR, FSLY, and MPC for your portfolio.

Consider 5 Top Strong-Buy Rated Stocks With Wall Street Analysts' Upward Earnings Revisions

A banking crisis and the Fed raising interest rates to nearly 5% in one year are two of the biggest headlines surrounding fears of an impending recession. Despite the latest CPI showing signs of deflation, tighter monetary and fiscal policies are key aspects in the mission to bring down inflation, but they can affect corporate earnings.

Many companies have experienced a fall in growth and profitability. Still, year-to-date, each of my recommended stocks have outperformed the S&P 500, showcasing strong fundamentals to withstand the Fed’s hawkish stance and may benefit in the long term from a return to growth environment. Regardless of the economic cycle, quality investment fundamentals are the best way to choose stocks. Consider stocks like the five highlighted, with fair valuations backed by solid fundamentals and strong growth. Although we’re facing recession concerns through next year, the stocks we’ve selected have positive demand factors to outweigh headwinds, which is why Wall Street analysts are increasing their earnings estimates for these stocks.

In addition, Seeking Alpha Quant Ratings and Factor Grades help ensure investors are furnished with the best resources to make informed decisions. In light of corporate actions, liquidity, and an ample supply of underlying metrics, we added some parameters to tighten up the criteria used for our rating system. If you are interested in Strong Buy recommendations outside our Top 5, here are some Seeking Alpha top-rated stocks.

For further details see:

Top 5 Stocks For Earnings Season