TFC - Top 9 High-Yield Alternatives That Outshine Verizon's 7%: Don't Miss Out

2023-05-12 07:45:00 ET

Summary

- Verizon Communications Inc. is a wonderful choice for anyone seeking a safe 7% yield and ultra-low volatility in bear markets.

- Verizon's average peak decline in bear markets since 1985 is 11%, 40% less than a 60/40 retirement portfolio.

- Verizon is trading at the 2nd highest yield in history and is 36% undervalued, just 7X cash-adjusted earnings.

- It's priced for -3% growth, and analysts expect 0.5% long-term growth, along with 70% returns in the next 3 years, and 110% in the next six. That's 2X better than the S&P 500 consensus.

- This article showcases nine better Verizon alternatives for those looking for even better yield and stronger growth. Including my two favorites, such as a 7.3% yielding Buffett-style 60% undervalued table-pounding buy, and an A-rated 7.7% yielding dividend aristocrat growing 7X faster than Verizon.

This article was published on Dividend Kings on Wed, May 10th.

---------------------------------------------------------------------------------------

In a recession, defensive high-yield blue chips like Verizon Communications Inc. ( VZ ) are a favorite among income investors.

After all, with the debt ceiling crisis threatening a 45% market crash (from here) within the next four months, a low volatility blue chip that pays a safe 7% might be just what you need to ride out the coming market mayhem.

Verizon & AT&T During Every Bear Market Since 1985

| Bear Market |

| VZ |

| 60/40 |

| S&P |

| 2022 Stagflation |

| -20% |

| -21% |

| -28% |

| Pandemic Crash |

| -12% |

| -13% |

| -34% |

| 2018 |

| 7% |

| -9% |

| -21% |

| 2011 |

| -1% |

| -16% |

| -22% |

| Great Recession |

| -34% |

| -44% |

| -58% |

| Tech Crash |

| -52% |

| -22% |

| -50% |

| July 1998 to October 1998 |

| -3% |

| -10% |

| -22% |

| 1990 Recession (May To October) |

| 3% |

| NA |

| -20% |

| 1987 Black Monday Period |

| -15% |

| NA |

| -36% |

| Average |

| -14% |

| -19% |

| -32% |

| Median |

| -12% |

| -16% |

| -28% |

(Sources: Portfolio Visualizer Premium, Charlie Bilello.)

Verizon averages 14% declines in bear markets, 56% less than the S&P 500 (SP500), and 40% less than a 60/40 retirement portfolio.

Its median peak decline is just 12%, and in the 2011 debt ceiling crisis, it fell just 1%, 95% less than the S&P.

So let's take a look at the biggest reasons some high-yield investors might want to buy Verizon today, but also consider nine superior higher-yielding faster-growing options.

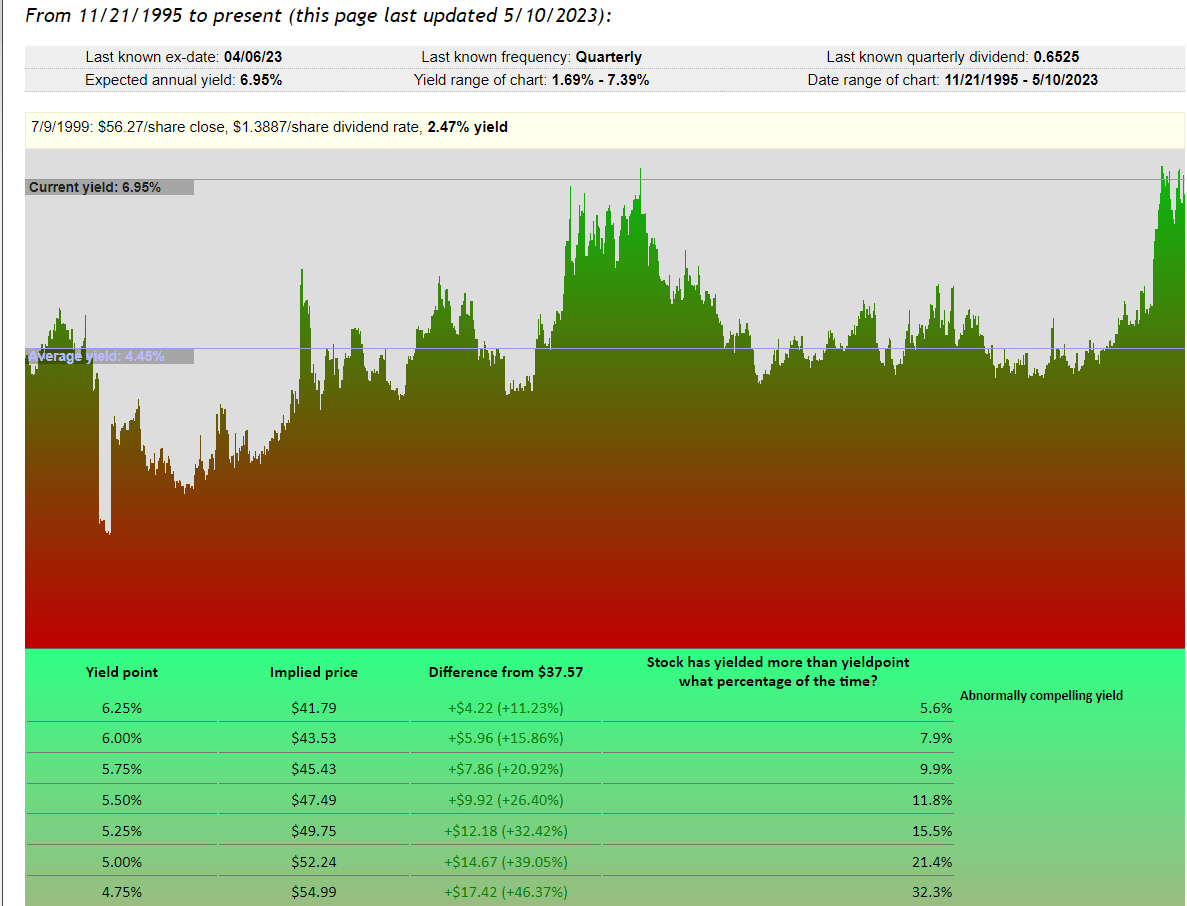

Verizon's Valuation Is Outstanding...

Let's start with yield, the only reason anyone ever buys Verizon.

{kind=link}

Verizon's 7% yield is the 2nd highest it's ever been, surpassed barely by the darkest days of the Great Recession.

| Metric |

| Historical Fair Value Multiples (9-Years) |

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 12-Month Forward Fair Value |

| 5-Year Average Yield |

| 4.46% |

| $58.07 |

| $58.52 |

| $58.52 |

| $61.43 |

| $62.11 |

| Earnings |

| 12.02 |

| $62.26 |

| $56.37 |

| $56.49 |

| $57.58 |

| $60.22 |

| Average |

| $60.09 |

| $57.43 |

| $57.49 |

| $59.44 |

| $61.15 |

| $57.45 |

| Current Price |

| $37.57 |

| Discount To Fair Value |

| 37.48% |

| 34.58% |

| 34.65% |

| 36.80% |

| 38.56% |

| 34.60% |

| Upside To Fair Value |

| 59.95% |

| 52.85% |

| 53.02% |

| 58.22% |

| 62.76% |

| 59.86% |

| 2023 EPS |

| 2024 EPS |

| 2022 Weighted EPS |

| 2023 Weighted EPS |

| 12-Month Forward EPS |

| 12-Month Average Fair Value Forward PE |

| Current Forward PE |

| Cash-Adjusted PE |

| $4.69 |

| $4.70 |

| $2.98 |

| $1.72 |

| $4.69 |

| 12.2 |

| 8.0 |

| 7.0 |

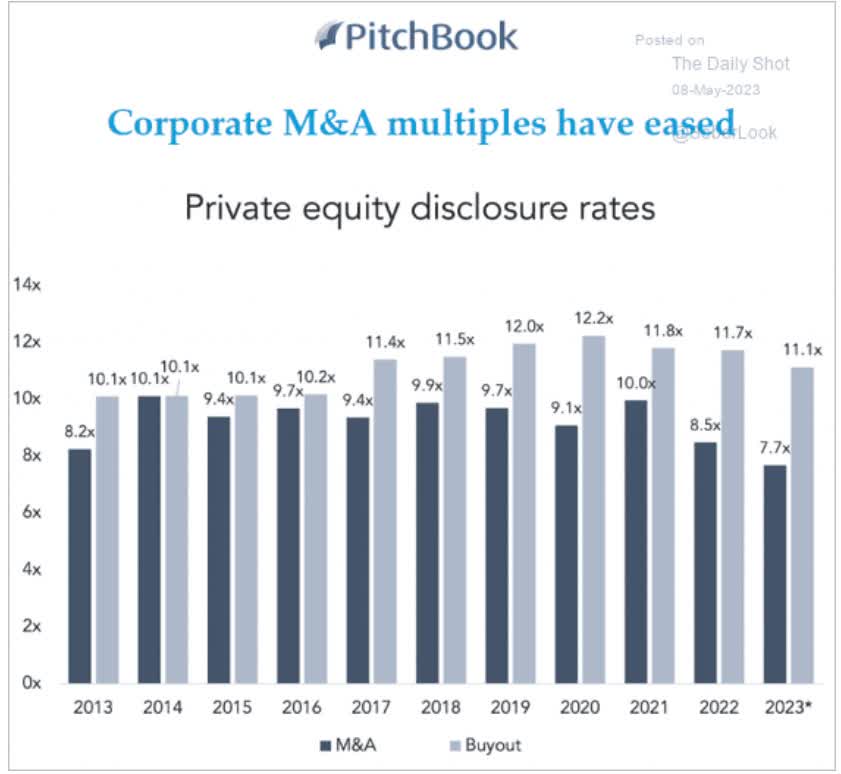

Verizon is conservatively worth 12X earnings, trades at an anti-bubble 8X, and its cash-adjusted earnings is 7X.

{kind=link}

Private equity is paying 11X for companies right now, meaning Verizon is dirt cheap by even private equity standards.

In fact, in the first ten seasons of Shark Tank, the average multiple for a deal was 7X.

Verizon isn't just a good deal; it's a Shark Tank-level good deal that pays a relatively safe 7% yield.

What does a 7X multiple mean? That Verizon is priced for -3% permanent growth.

You'll make a lot of money if it grows faster than that. The dividend will be safe forever if it grows 0% or faster.

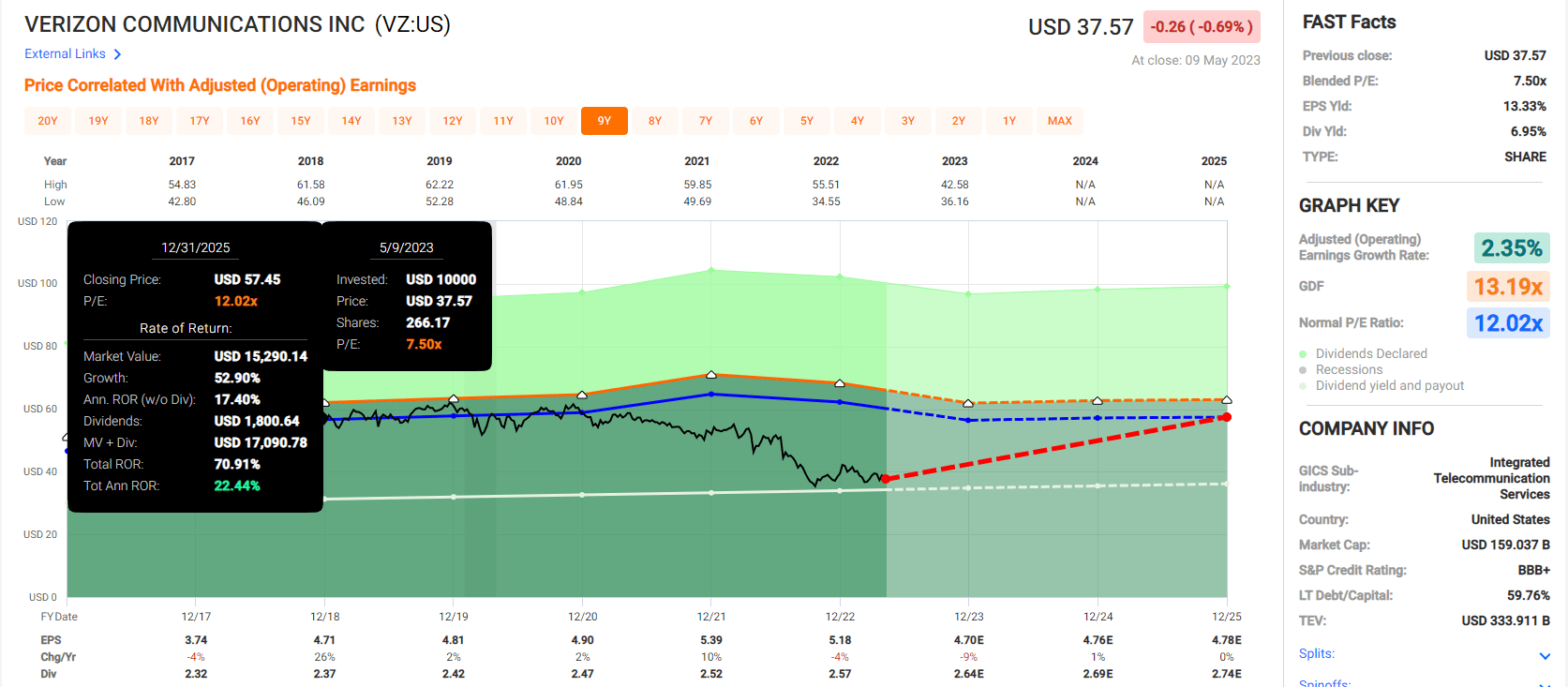

Verizon 2025 Consensus Total Return Potential

{kind=link}

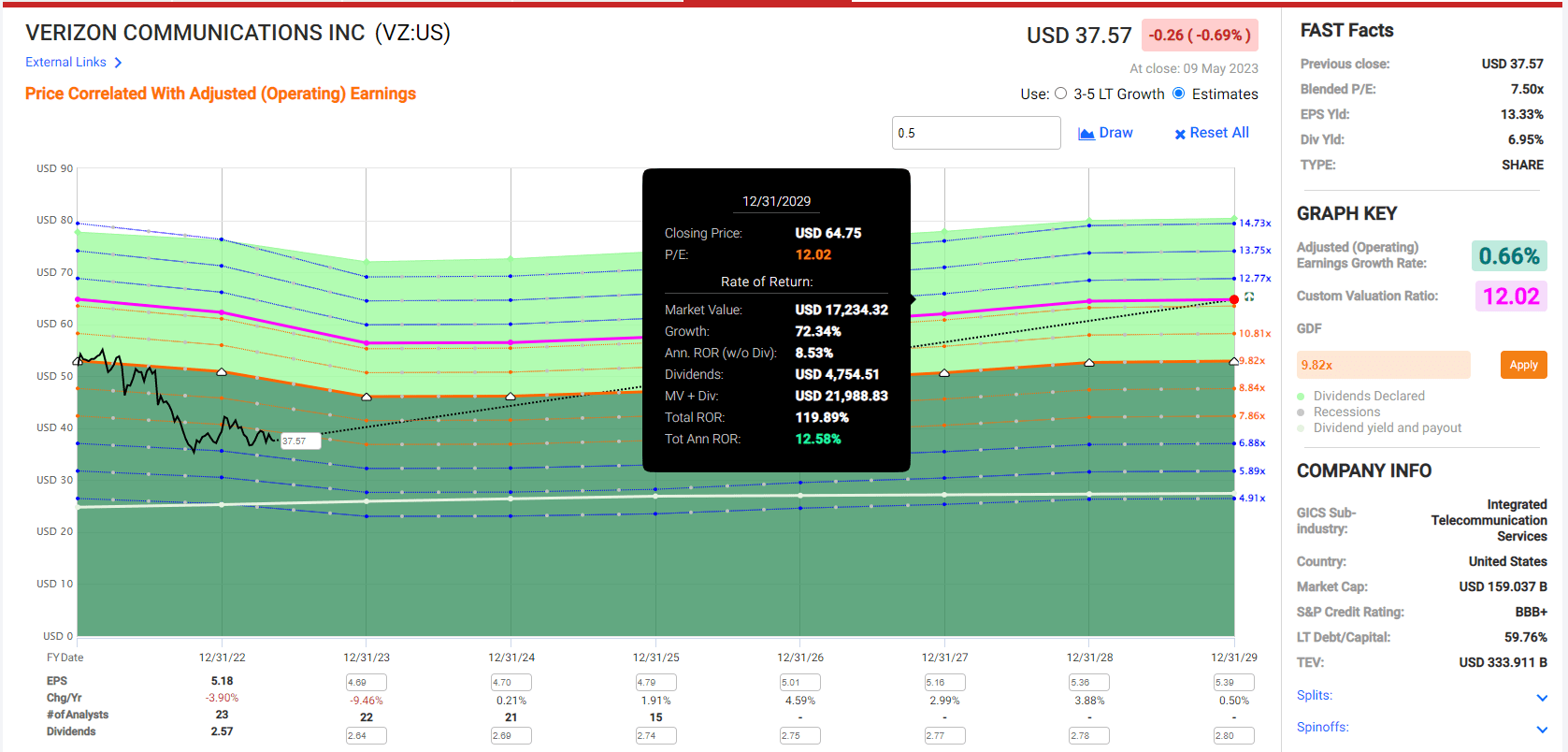

Verizon 2029 Consensus Total Return Potential

{kind=link}

Verizon isn't growing right now, but it's so undervalued that in the next three years, it could deliver 70% returns, or 22% annually.

- Warren Buffett-like return potential from an anti-bubble blue-chip bargain hiding in plain sight.

In the next six years, even with less than 1% annual growth, it could deliver 120% returns or 13% annually.

- about 2X the S&P consensus.

But Its Growth Prospects Are Not

Verizon has never been a fast-growing company, but thanks to higher interest rates, its growth prospects have dimmed to levels that are anemic by even its standards.

- 20-year growth rate: 3.4%

- 4-year growth rate: 2.4%.

What about the next few years?

| Metric |

| 2022 Growth |

| 2023 Growth Consensus |

| 2024 Growth Consensus |

| 2025 Growth Consensus |

| Sales |

| 1% |

| -1% |

| 1% |

| 0% |

| Dividend |

| 2% |

| 2% |

| 2% |

| 2% |

| EPS |

| -4% |

| -9% |

| 1% |

| 0% |

| Operating Cash Flow |

| -7% |

| -4% |

| 1% |

| 2% |

| Free Cash Flow |

| 2% |

| 2% |

| 2% |

| 5% |

| EBITDA |

| -3% |

| 0% |

| -1% |

| 2% |

| EBIT (operating income) |

| -6% |

| 0% |

| 2% |

| 2% |

(Source: FAST Graphs, FactSet.)

Verizon Communications Inc. is expected to deliver a very steady 2% growth rate in free cash flow and dividends. But its sales growth is basically zero.

That's a problem, because there is only so much cost-cutting that VZ can do. Free cash flow ("FCF") will benefit from a decrease in 5G spending, but that is a one-time benefit.

{kind=link}

In 2022, VZ hit peak 5G spending, and by 2028, $5.5 billion in less annual spending will help boost free cash flow significantly.

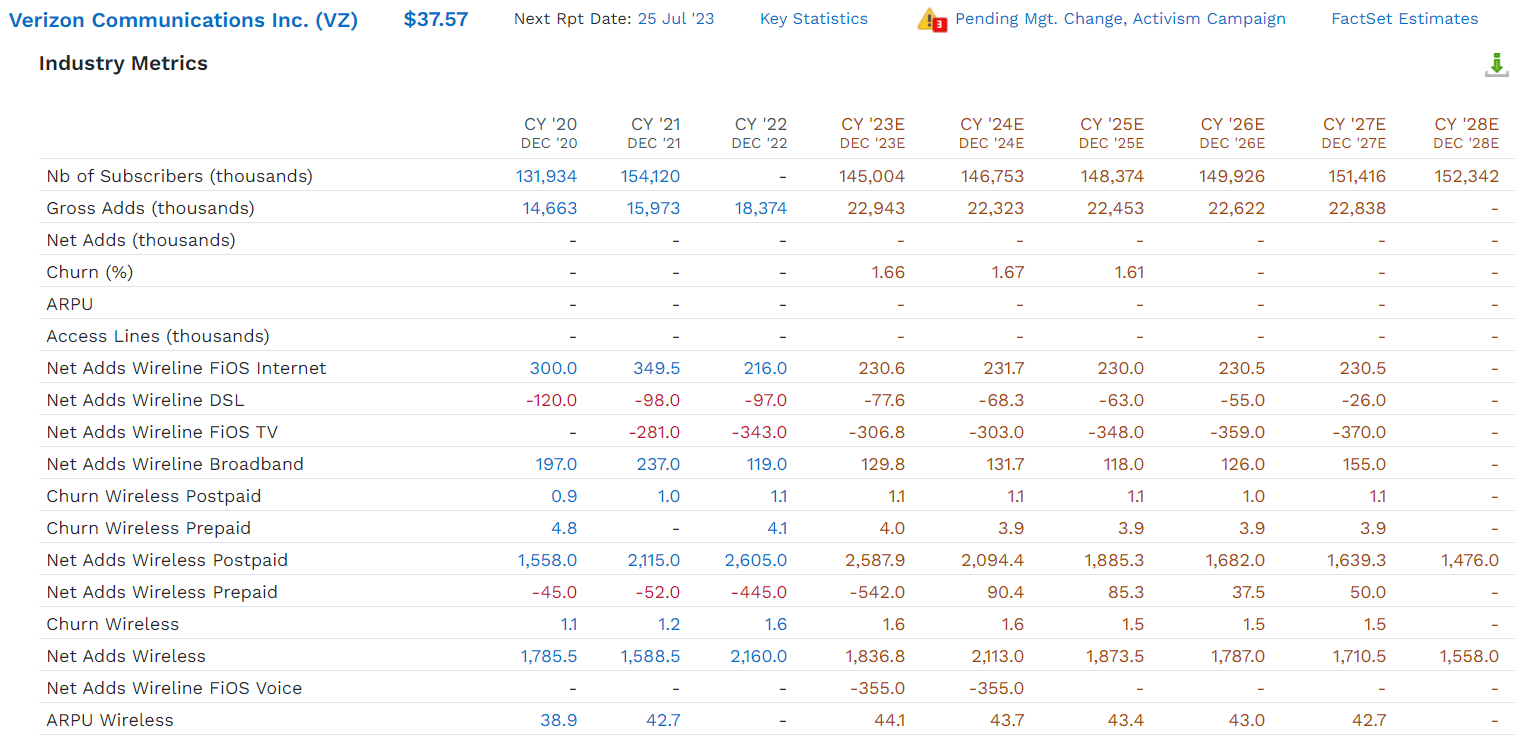

But the company is facing a large headwind with cord cutting, specifically.

{kind=link}

Verizon's internet and pay TV subscribers are expected to slowly shrink in the coming years.

Its wireless business is expected to grow slowly but steadily, but competition from T-Mobile is expected to cap its ability to raise prices.

Starting in 2029 or 2030 , VZ is going to have to start ramping up 6G spending to compete with the next generation of wireless.

So what does that mean long-term for VZ?

{kind=link}

Thanks to higher interest rates than in the last decade (expected to be a permanent feature of the new economy) and 6G spending, analysts think VZ's long-term growth rate will be 0.5%.

- -1.8% adjusted for inflation.

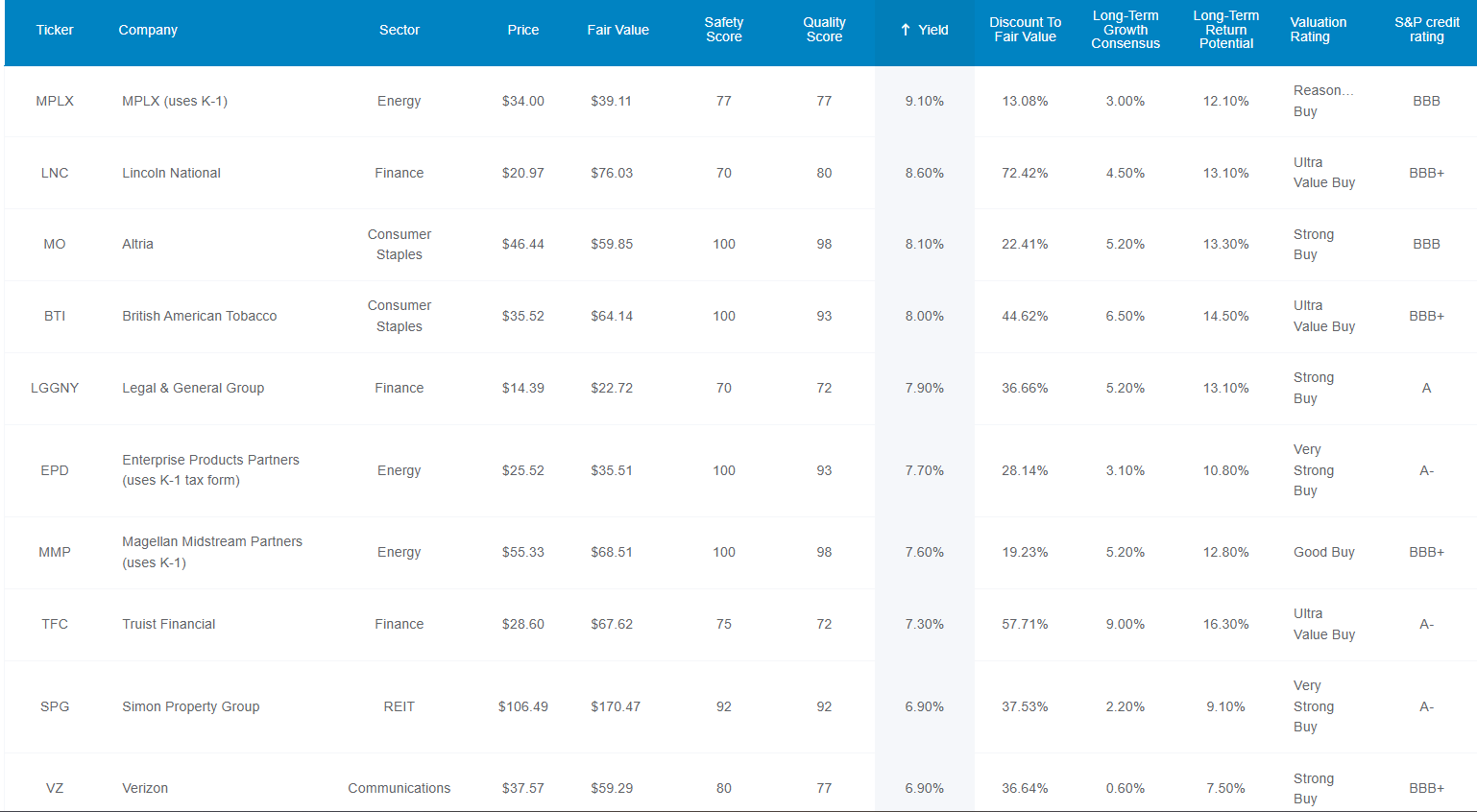

Consensus Long-Term Return Potential

| Investment Strategy |

| Yield |

| LT Consensus Growth |

| LT Consensus Total Return Potential |

| Long-Term Risk-Adjusted Expected Return |

| MPLX (K1 tax form) ( MPLX ) |

| 9.1% |

| 3% |

| 12.1% |

| 8.5% |

| Lincoln National ( LNC ) |

| 8.6% |

| 4.5% |

| 13.1% |

| 9.2% |

| British American Tobacco ( BTI ) |

| 8.2% |

| 6.5% |

| 14.7% |

| 10.3% |

| Altria ( MO ) |

| 8.1% |

| 5.2% |

| 13.3% |

| 9.3% |

| Legal & General ( LGGNY ) |

| 7.9% |

| 5.20% |

| 13.1% |

| 9.2% |

| Enterprise Products Partners (K1 tax form) ( EPD ) |

| 7.7% |

| 3.4% |

| 11.1% |

| 7.8% |

| Magellan Midstream (K1 tax form) ( MMP ) |

| 7.6% |

| 5.2% |

| 12.8% |

| 9.0% |

| Truist Financial ( TFC ) |

| 7.3% |

| 6.4% |

| 13.7% |

| 9.6% |

| Verizon |

| 7.0% |

| 0.50% |

| 7.5% |

| 5.3% |

| Schwab US Dividend Equity ETF ( SCHD ) |

| 3.6% |

| 7.6% |

| 11.2% |

| 7.8% |

| S&P 500 ( VOO ) |

| 1.7% |

| 8.5% |

| 10.2% |

| 7.1% |

(Sources: DK Research Terminal, FactSet, Morningstar.)

Verizon has a lot of upside in the short-term from a dirt-cheap valuation. And a 7% safe yield growing at 2% is attractive for some income investors seeking very low volatility in bear markets.

But there are many higher-yielding blue-chip alternatives to consider.

8 Better Higher-Yielding Alternatives To Verizon

Dividend Kings Zen Research Terminal

{kind=link}

While Simon Property Group, Inc. (SPG) doesn't have a superior yield to VZ, its growth rate is 4X faster.

Here are my top three recommendations for the best higher-yielding alternatives to Verizon, with superior yield, far better growth prospects, and good to excellent dividend safety.

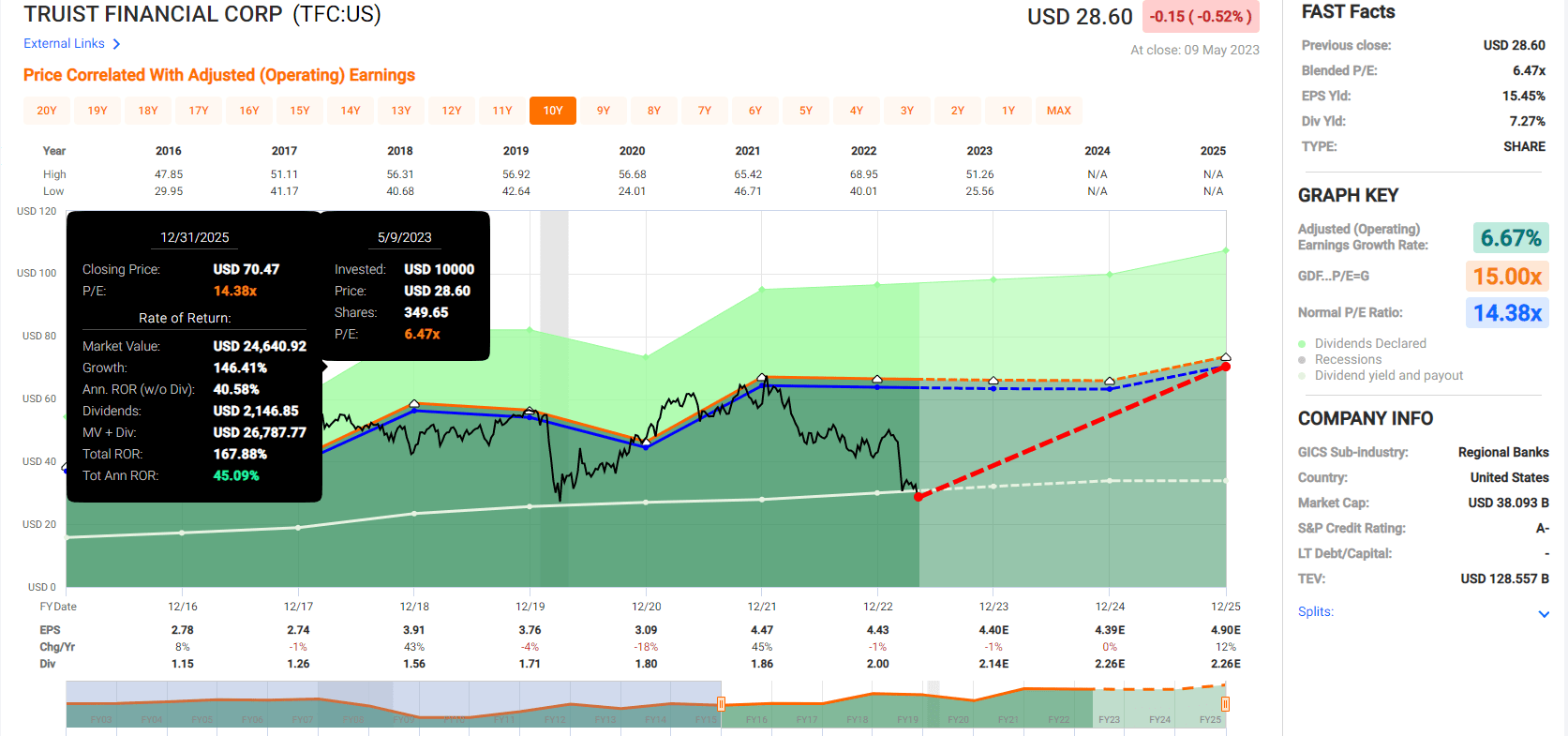

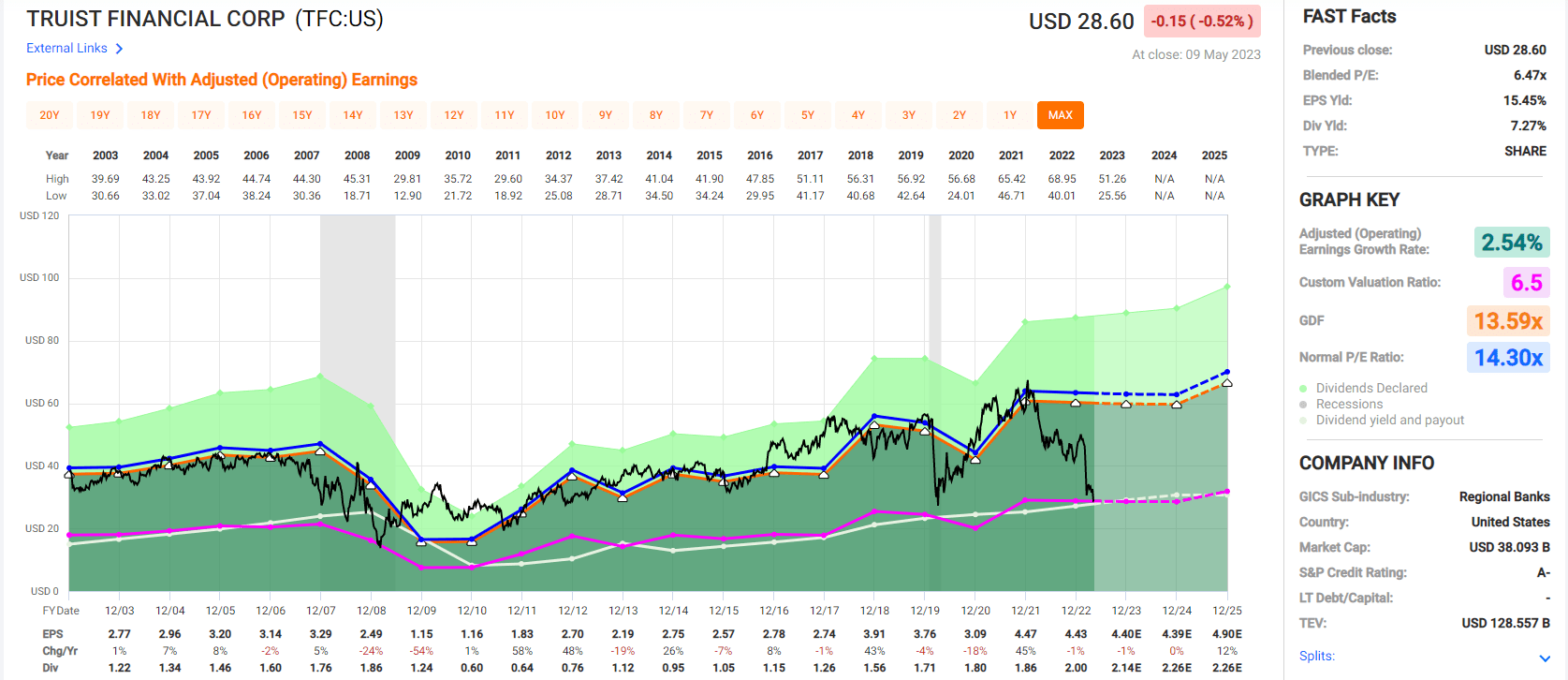

Truist Financial: A Buffett-Style, Table-Pounding "Fat Pitch" Ultra Value Buy

Further Reading

Why TFC Is A Great Buy Today

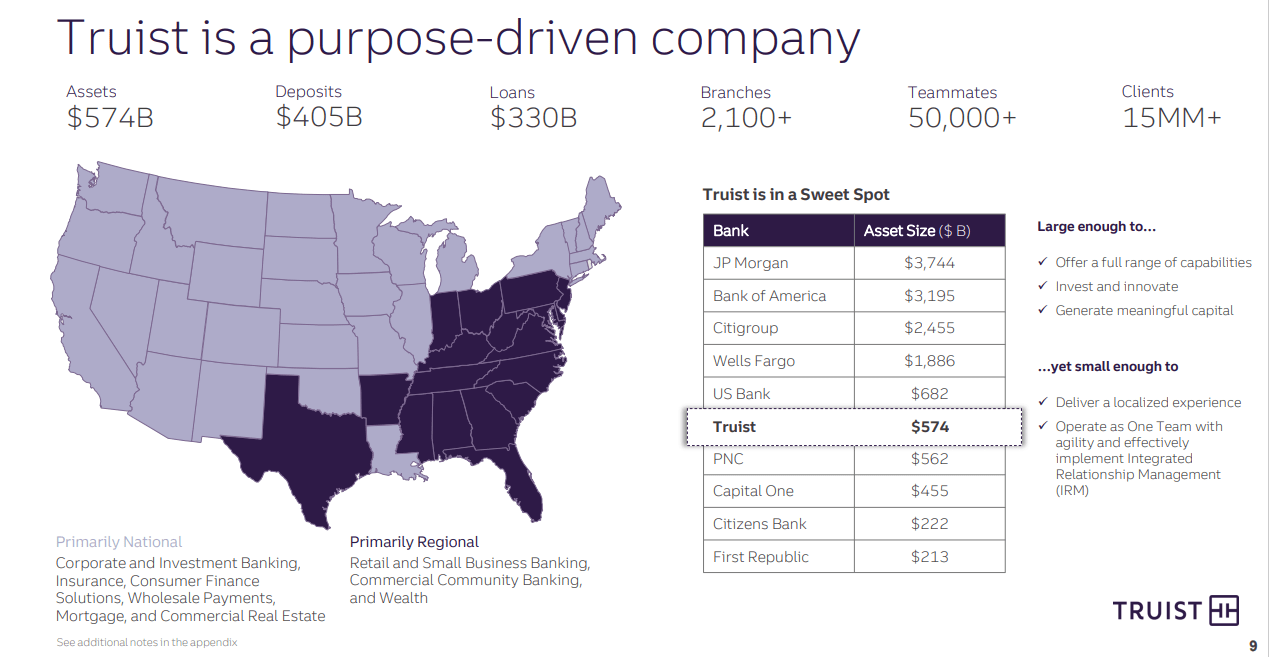

Truist was created by the merger of Suntrust and BB&T in 2019, the largest in a decade.

{kind=link}

It's the 6th largest bank in the U.S., with $574 billion in assets and 2,123 branches in 15 states and DC.

Bloomberg

TFC is one of the three super-regional banks and one of the 11 strongest banks in the country, according to the U.S. government. That's why it was asked to participate in the First Republic rescue coalition.

Now that JPMorgan Chase (JPM) has bought First Republic Bank (FRCB), each customer is getting deposits back.

{kind=link}

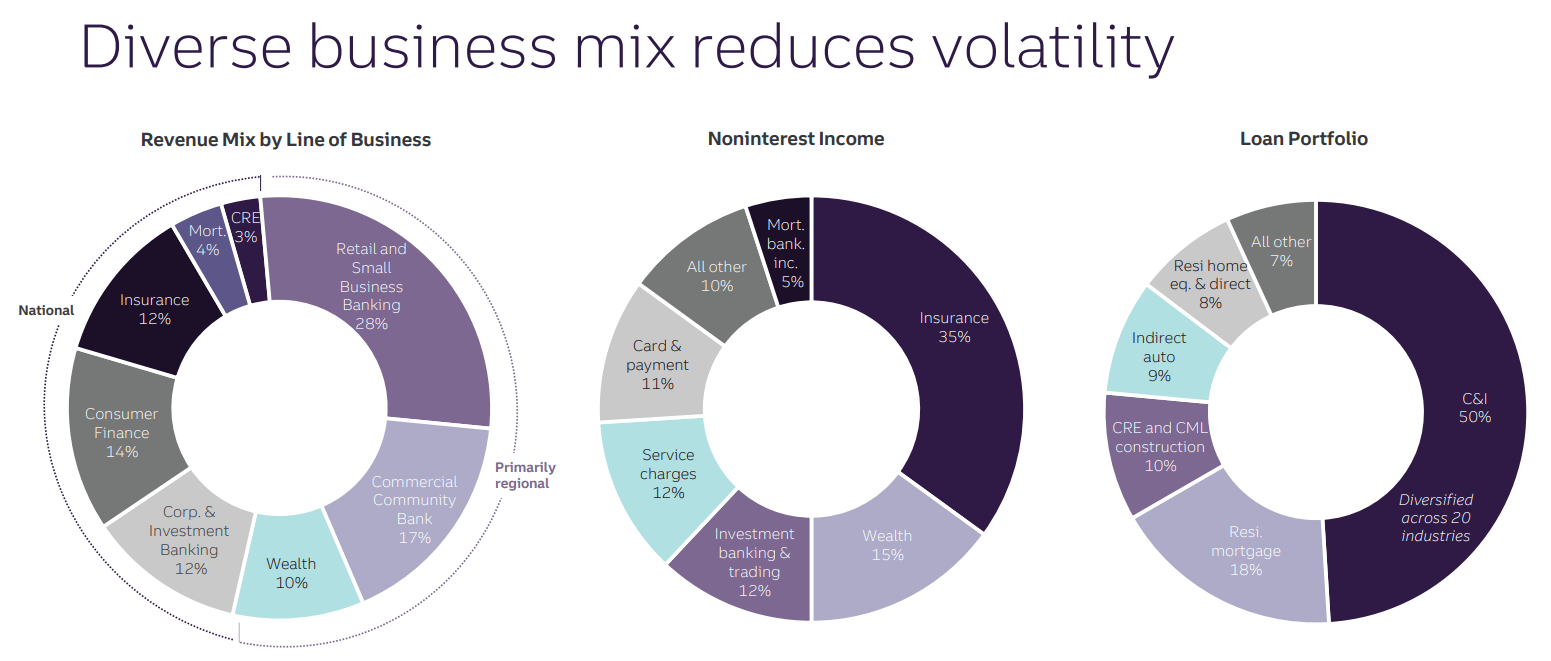

TFC is nothing like First Republic; it's a highly diversified bank that's a mini JPMorgan.

If this A- rated bank fails (2.5% risk according to S&P and Moody's), I will eat my hat. We'll all be eating our hats because it will be the apocalypse, the living will envy the dead, and money will have lost all value. ;)

Fundamental Summary

- DK quality score: 72% low risk 10/13 blue chip super regional bank

- DK safety score: 75% safe dividend (2.6% dividend cut risk in severe recession)

- Historical fair value: $67.41

- Current price: $28.60

- Discount to fair value: 58%

- DK rating: potential Ultra Value Buy, Buffett-style "fat pitch"

- Yield: 7.3%

- Long-term growth consensus: 6.4%

- Consensus long-term return potential: 14.3%.

{kind=link}

TFC isn't expected to grow until 2025 due to the recession. But it's so undervalued, trading at 6.5X earnings, that it could deliver 150% returns in less than three years.

That's a Buffett-like 45% annualized return.

In fact, it's almost as good as Buffett's best investment ever, AXP's 400% gain over four years following the Great Salad Oil Swindle of 1963 (49% annual return).

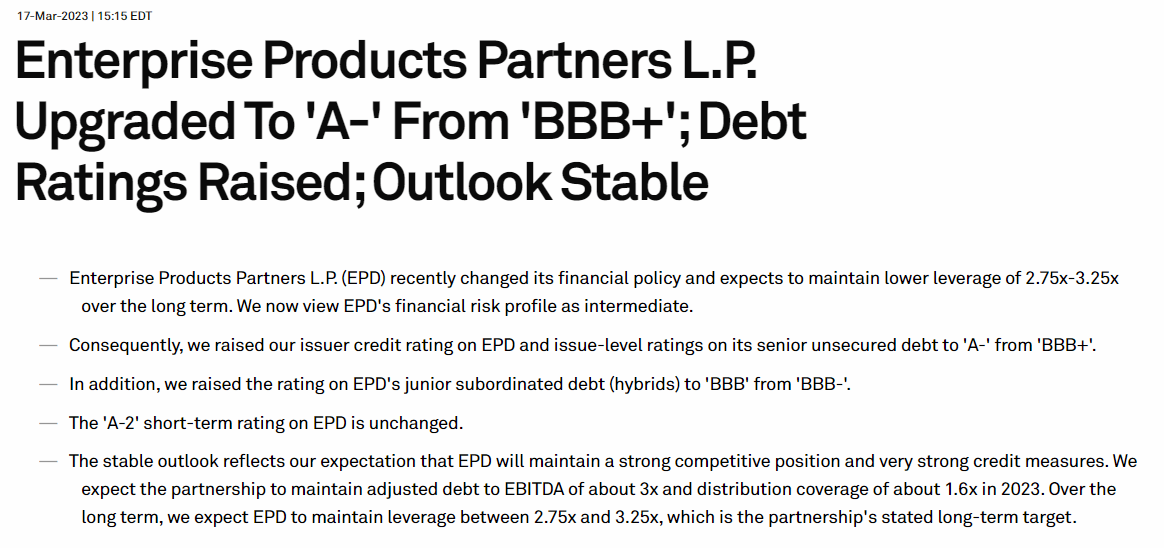

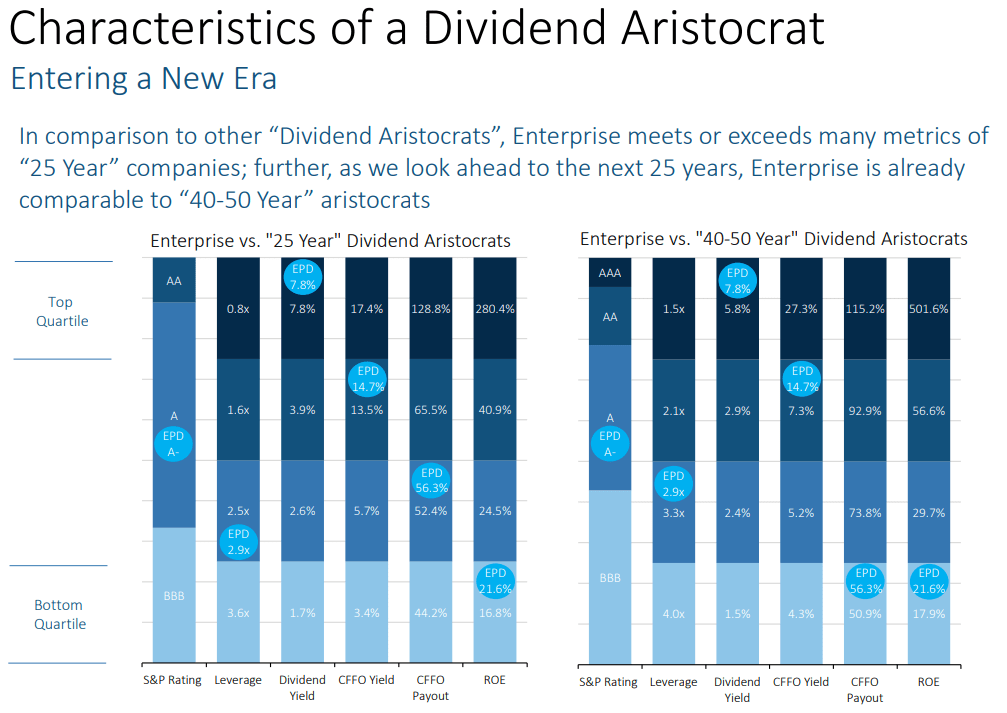

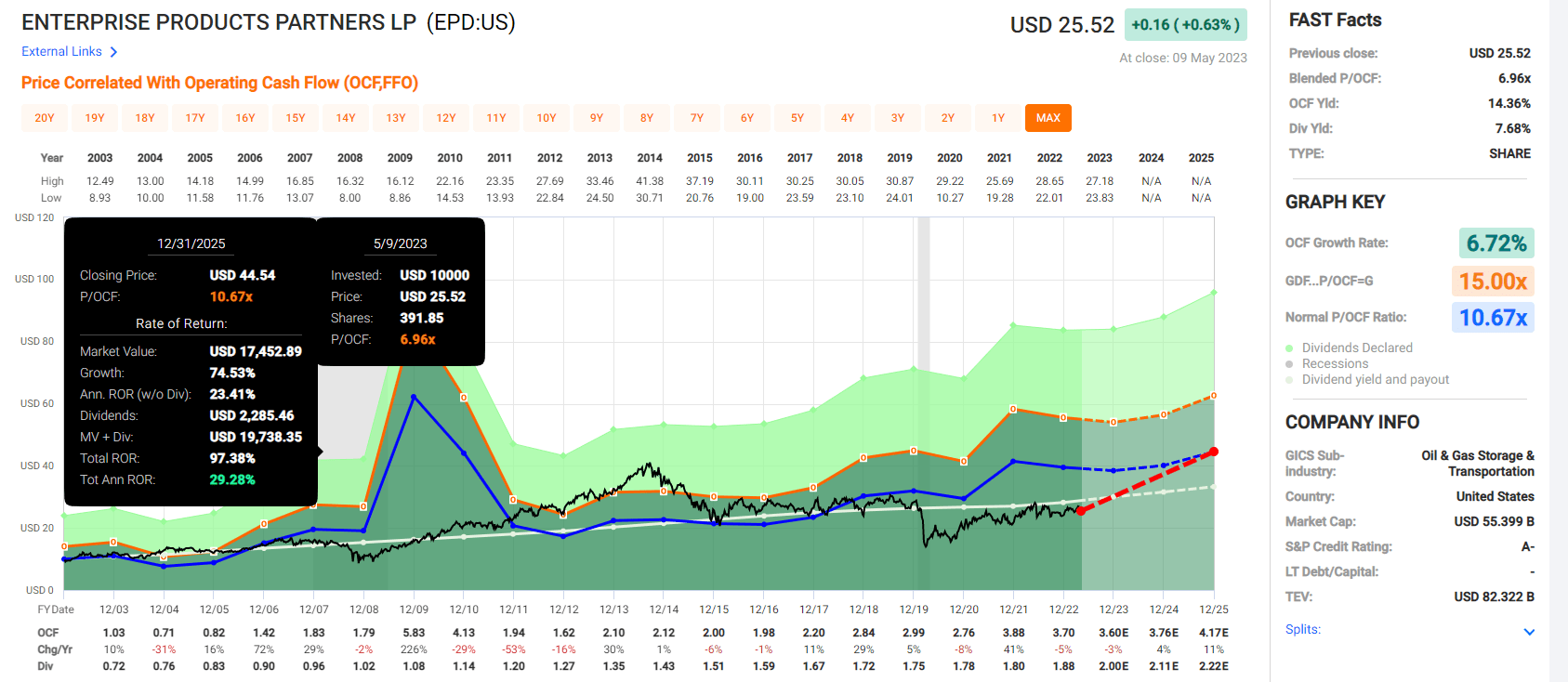

Enterprise Products Partners: A Dividend Aristocrat With The Strongest Balance Sheet In Industry History

Further Reading

Why EPD Is A Great Buy Today

EPD is the JPM of its industry, the Mac daddy of great management, and a bulletproof, fortress balance sheet.

{kind=link}

It's the first midstream in history with an A- credit rating.

That means a 2.5% 30-year bankruptcy risk, half that of other midstream quality titans such as TRP, ENB, and MMP.

Among the best-managed names in this industry, EPD stands a cut above. Morningstar describes the best management team in the industry as "chess masters in an industry where everyone else is playing checkers."

{kind=link}

In 2023 EPD becomes an aristocrat (technically a champion, but it's the same thing other than S&P inclusion), and management has a strong long-term plan to become a dividend king in 2048.

It's the only midstream that has stated plans to become a dividend king.

Fundamental Summary

- DK quality score: 93% low risk 13/13 Ultra SWAN aristocrat

- DK safety score: 100% very safe dividend (1.0% dividend cut risk in severe recession)

- Historical fair value: $35.37

- Current price: $25.52

- Discount to fair value: 28%

- DK rating: potential very strong buy

- Yield: 7.7%

- Long-term growth consensus: 3.4%

- Consensus long-term return potential: 11.1%.

{kind=link}

EPD offers the potential to double your money over three years while enjoying 50% better long-term returns than Verizon.

- 3.6% better long-term returns = 189% better 30-year inflation-adjusted returns.

Bottom Line: Verizon's 7% Yield Is Great, But Here Are 9 Better Alternatives

Let me be clear: I'm NOT calling the bottom in Verizon, Enterprise, Truist, or any of these Verizon alternatives. (I'm not a market-timer).

Even the world's best companies can fall hard and fast in a bear market.

Fundamentals are all that determine safety and quality, and my recommendations.

- over 30+ years, 97% of stock returns are a function of pure fundamentals, not luck

- in the short term; luck is 25X as powerful as fundamentals

- in the long term, fundamentals are 33X as powerful as luck.

But here is what I can tell you about Verizon and MPLX, LNC, MO, BTI, LGGNY, EPD, MMP, TFC, and SPG.

Verizon is a great low volatility ultra-yield blue-chip choice for those who are looking for wonderful income and 2% long-term income growth.

It's 36% undervalued and could deliver 70% returns in the next five years and 110% returns in the next six.

But the prospect of higher rates and 6G spending has analysts rather underwhelmed by its 0.5% long-term growth prospects.

If steady, boring, and recession resistant is your goal, VZ is a potentially very strong buy.

If you want both safe ultra-yield and superior growth than the nine alternatives presented here are all worth considering.

I personally like TFC for its incredible, once-in-a-decade buying opportunity.

The Only Time TFC Was This Undervalued Was The Great Recession Lows

{kind=link}

Unless you expect a worse economic disaster than the Great Recession (less than 5% chance, according to Moody's) you shouldn't expect TFC to get much cheaper.

And if you want ultimate balance sheet safety and a relatively recession-resistant business along with the industry's best management, Enterprise Products Partners is the safety king of midstream.

It is a dividend aristocrat with plans to become a dividend king that boasts 7X the growth prospects of Verizon.

For further details see:

Top 9 High-Yield Alternatives That Outshine Verizon's 7%: Don't Miss Out