NLCP - Top Cannabis Picks To Buy And Celebrate 4/20: MSOS And NewLake Capital

2023-04-20 12:21:04 ET

Summary

- It is April 20th - happy cannabis day!

- U.S. cannabis stocks are down as much as 90% since 2021 highs.

- I discuss the elevating risks of the multi-state operators.

- I discuss my top stock to buy in the cannabis sector.

It is April 20th, a day many take to celebrate their love for cannabis. The origins of why this day is connected to cannabis is sometimes disputed, but it is typically credited to a group of Californian high schoolers in the 1970s who called themselves “Waldos” that set the time 4:20 pm as their consistent time to meet up and enjoy the plant. For stock investors, it may be a day to revisit the cannabis sector and search for opportunities to invest in the long-term growth opportunity.

Cannabis Stocks Have Crashed

The stocks of the U.S. multi-state operators ("MSOs") have imploded ever since they reached highs in early 2021. These include the largest names: Green Thumb Industries ( GTBIF ), Curaleaf Holdings, Inc. ( CURLF ), Trulieve Cannabis Corp. ( TCNNF ), Cresco Labs ( CRLBF ), and Verano ( VRNOF ). These names form the majority of the well-known cannabis exchange-traded fund ("ETF") AdvisorShares Pure US Cannabis ETF ( MSOS ).

While it may be tempting to pound the table on these MSOs stocks, especially considering that they are now trading at low single-digit multiples of EBITDA, I mustn’t understate the elevated risks in the sector. Besides the significant burden of 280e taxes, in which U.S. operators are prohibited from deducting operating expenses from taxable income, these companies are suffering from the high interest rate environment. In hindsight, these management teams pursued a “growth at any cost” strategy over the past few years and are now saddled with highly leveraged balance sheets while price compression is placing downward pressure on margins.

Instead, today I will like to highlight a profitable cannabis real estate investment trust ("REIT") in NewLake Capital Partners, Inc. ( NLCP ), which I previously made my top pick of 2023 . Unlike the stocks of MSOs which are unlikely to enjoy a return of shareholder capital over the next decade, NLCP pays a generous and growing dividend that is only made more valuable from the lower stock prices.

Top Cannabis Picks To Buy

NLCP is an internally managed net lease REIT focused on the cannabis sector.

{kind=link}

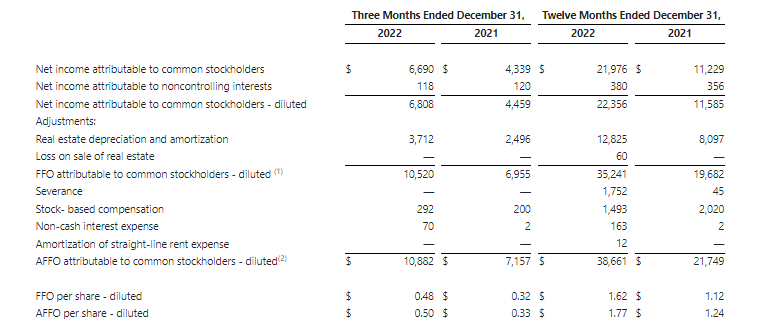

NewLake Capital closed out 2022 with typical financial strength. Adjusted funds from operations ("AFFO") is the main financial metric to focus on here, because it adds back depreciation & amortization to GAAP net income. Recall that net lease REITs generate high free cash flow margins because it is their tenants that are responsible for real estate taxes, insurance, and maintenance expenses (the "triple nets"). NLCP grew AFFO per share by 52% to $0.50 in the fourth quarter. For the year, AFFO grew 42.7% to $1.77 per share.

Most of the growth simply came from putting cash to work in high ROI investments.

{kind=link}

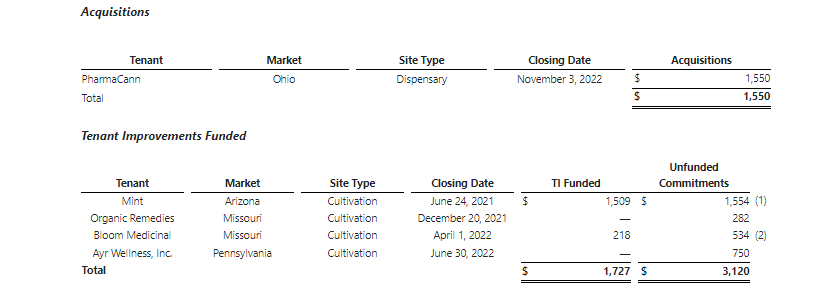

The quarter saw modest investment activity with NLCP acquiring one PharmaCann dispensary property in Ohio and funding 4 tenant improvements in Arizona, Missouri, and Pennsylvania.

{kind=link}

NLCP had previously authorized a $10 million share repurchase program but noted that it had not yet repurchased any stock. The first quarter is also looking to be a quarter with modest investment activity, as the company acquired a property in Missouri for $350,000 from tenant C3 industries - the plan is to eventually expand the existing cultivation facility for $16.2 million. NLCP also has plans to fund tenant improvements to a cultivation facility in Arizona for tenant The Mint Cannabis.

The slow pace of investment activity is not the problem considering the low valuations and the 3% annual lease escalators. Instead, it was the surprise shortfall in rent collection. NLCP had previously noted that its Pennsylvania tenant Calypso was facing a difficult period, but noted on the conference call that Calypso:

“has done a nice job of adjusting their operations since last summer’s reorganization and continues to pay their originally contracted rents although we have allowed them to temporarily pay on a weekly schedule to better match their cash flow.”

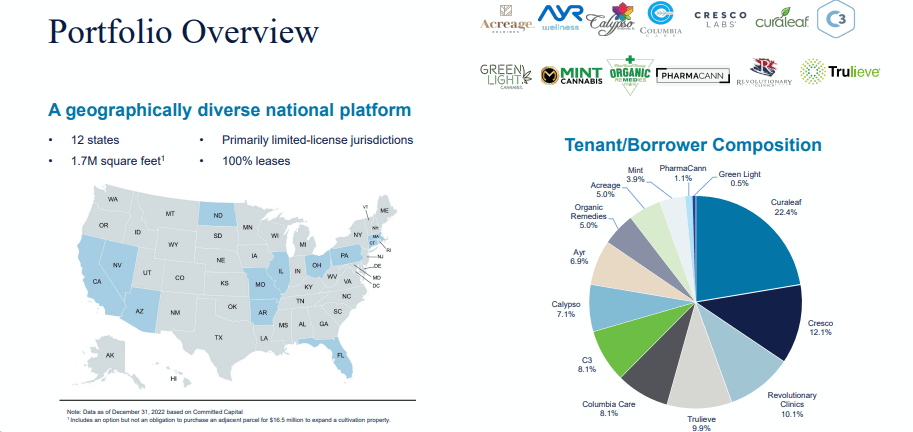

Instead, it was tenant Revolutionary Clinics in Massachusetts which has not paid rent in the first quarter. Due to that, NLCP anticipates rent collection to be 90% to 93% for Q1 which based on commentary seems to include application of 3 months security deposit as rent. This is not a good sign, but management noted that this should be a short term issue as Revolutionary Clinics faced issues due to delays in opening their adult-use dispensaries and their recent harvest. Revolutionary Clinics is their third largest tenant, representing 10% of their overall portfolio. We will have to see over the coming quarters if this really proves to be a near term headwind, but this is a market which has little patience to wait that long.

While management noted that their “pipeline is slightly smaller today than it has been historically,” they also noted that recent debt transactions imply an “effective cost of capital in excess of 15% for even the top MSOs.” I continue to expect sale and leaseback transactions to pick up especially as it comes time for these MSOs to refinance maturing debt.

Is NLCP Stock A Buy, Sell, or Hold?

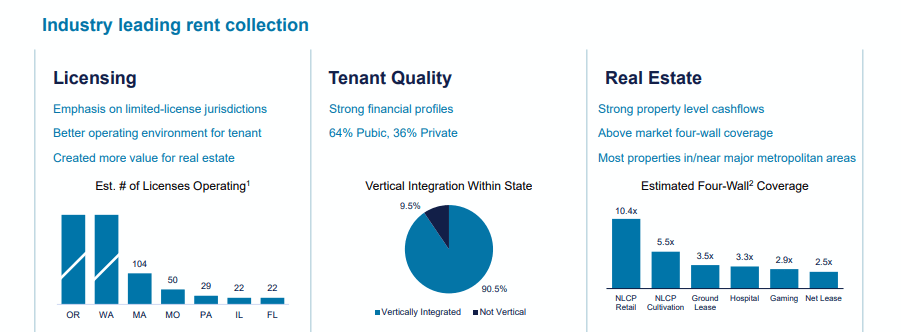

While the cannabis REIT sector - mainly made up of NLCP and Innovative Industrial Properties, Inc. (IIPR) - has seen its valuations dip to deep discounts relative to traditional NNN REIT peers, this remains a high-growth industry as more and more states legalize the plant. Due to cannabis being illegal on the federal level, NLCP is able to earn superior financing terms, including 13% acquisition cap rates and higher annual lease escalators.

{kind=link}

This is not an issue with financing. NLCP still has access to a $100 million revolving credit facility which bears interest at a 5.65% rate. Given where the equity stands, future acquisitions will likely be financed primarily with this credit facility and secondarily by retained free cash flow. After the recent plunge, the stock is now trading around a 12% dividend yield. Even if we assume that 50% of its revenue disappears overnight (leading to AFFO to decline by 56% to $0.88 per share, then NLCP would be trading at 14.6x AFFO.

For reference, Realty Income Corporation ( O ) is trading at around 15x FFO and Agree Realty ( ADC ) at 17x FFO. I find it highly unlikely that 50% of NLCP’s revenues will disappear - it is likely to be able to get significant recovery upon tenant difficulties, not to mention that NLCP has focused on properties in limited license states. If anything, "worst case" scenarios should be modeled based on 50% of tenants defaulting and getting a 50% recovery, for a 25% decline in revenues. NLCP would still be trading at just 8.8x that roughly $1.46 in AFFO per share. What’s more, NLCP deserves to trade at a premium to traditional NNN REIT peers like O due to higher acquisition cap rates (13% versus 5.5%), annual lease escalators (3% versus 1%), and overall pipeline of growth.

While it is likely that NLCP will see some sort of tenant troubles over the coming years, the stock price already reflects worst case scenarios. One mustn’t rule out the possibility that NLCP should be able to offset any troubled tenants through external growth (in this rising interest rate environment, I’d assume acquisition cap rates have expanded from the 12.7% average). Unlike MSOs, NLCP is not subject to 280e taxes and is able to generate 90% free cash flow margins (as defined as AFFO divided by revenue). NLCP then returns around 80% of that to shareholders, retaining the remaining to fund new investment opportunities. Compare that with MSOs, which are lucky if they can generate 30% adjusted EBITDA margins, with absolutely no cash to reward shareholders in spite of the low stock price valuations.

While one may find it “sexier” to buy the MSOs, at these valuations NewLake Capital Partners, Inc. is offering as much upside with far lower risk, as NLCP is higher on the capital structure and is paying shareholders already. NLCP remains my top pick in the cannabis sector, and this is reflected by the portfolio’s outsized allocation to the name.

For further details see:

Top Cannabis Picks To Buy And Celebrate 4/20: MSOS And NewLake Capital