TNP - Top Picks For Today's Product Tanker Market

2023-05-03 09:00:00 ET

Summary

- Product tanker equities have generated tremendous returns over the past year and certain names remain attractive for those with a positive view on future market balances.

- INSW and STNG are my favorites today, whereas TRMD and ASC are not very appealing at current pricing. I believe TNP, D'Amico, and Hafnia also are attractive at this time.

- Product tanker rates have been under pressure over the past few weeks, in-line with usual seasonality. However, ton-mile demand is still forecasted to increase materially this year.

- The orderbook (forward supply) remains near record lows and environmental regulations are likely to further constrain future supply.

Note: This report was previously shared with members of Value Investor’s Edge on April 29, 2023.

Product Tanker Sector Overview

A year has passed since I published the report titled “ Why Is It Time To Invest in Product Tankers ?” Since then, product tanker rates have remained at extraordinarily elevated levels, which has led to outstanding performance from publicly traded equities in the sector. Relative valuations have improved materially, but there are still some companies trading at enticing discounts if someone has a positive view of the current or future market.

My top pick from last year’s public report was TORM Plc ( TRMD ), which has returned 280% (nearly 4x) in just over a year. At current pricing, my favorites are now Scorpio Tankers ( STNG ) and International Seaways ( INSW ). Additionally, D’Amico Shipping (traded in the Italian exchange), Hafnia Tankers (traded in Oslo), and Tsakos Energy Navigation ( TNP ) are attractive on their own account. Ardmore Shipping ( ASC ) and TORM Plc, which I recommended as buys last year, are now trading at notably higher valuations than peers, and I believe they are currently not as attractive and are generally "hold/avoid" vs. peers.

In the next few sections, I will review current product tanker demand and supply fundamentals, followed by a brief recap of my favorite picks at this juncture.

Product Tanker Demand

Product tankers are part of the backbone of the global economy and are used to haul clean petroleum products (CPP, or refined products) from refineries in net exporting regions to net importing countries. Considering seaborne transport implies an extra cost (and is more expensive than pipeline flows where available), product tankers are used to transport the marginal barrels.

This makes shipping inherently volatile, which can lead to significant boom and bust cycles when times are good or bad respectively. Therefore, and although CPP consumption is somewhat inelastic, a recession has the potential to lower demand, disproportionally affecting product tanker market balances (as those are the assets used to haul the marginal barrels).

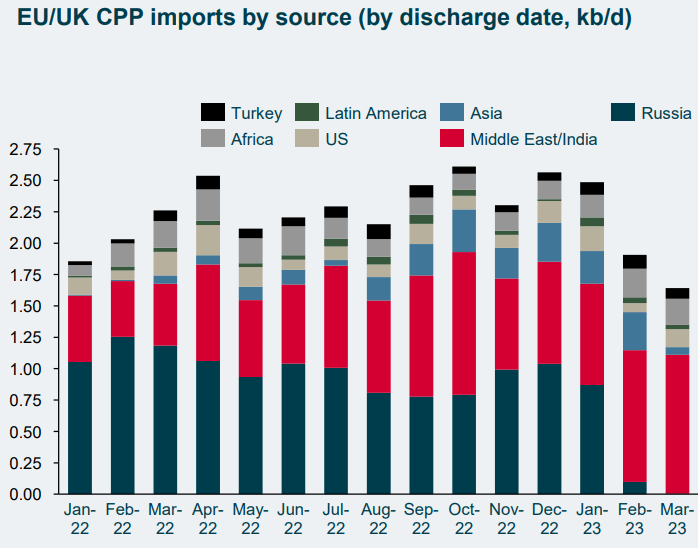

Interestingly, what made 2022 an extraordinarily strong year for product tanker rates was not impressive economic growth but changing trade patterns on the back of sanctions (be it formal sanctions or self-sanctioning by companies) on Russian CPP exports. As can be seen in the image below, before the invasion of Ukraine, Russia was Europe’s largest supplier of seaborne CPP volumes (even during H2-22). However, this recently changed as, on Feb. 5, Europe’s ban on Russian CPP imports became effective.

{kind=link}

TRMD’s Q4 Earnings Presentation, slide 7.

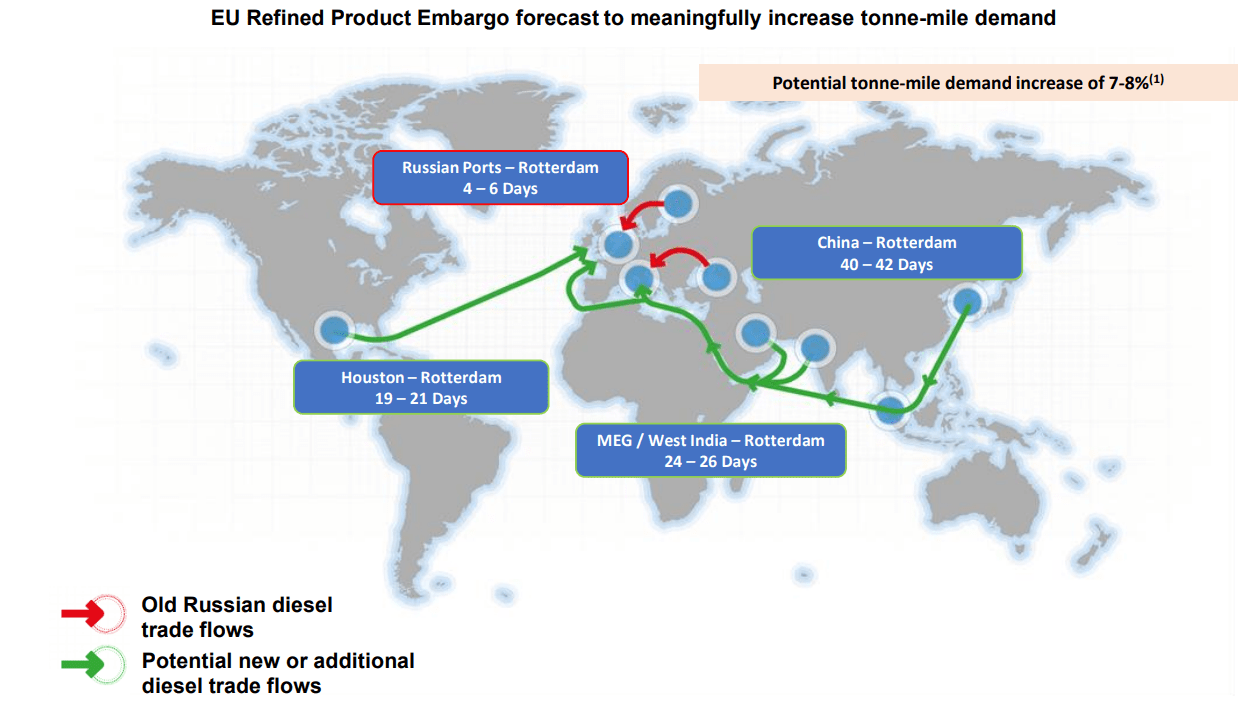

Russia’s Baltic and Black Sea ports were extraordinarily close to Europe, which made those routes very ton-mile demand light. As Europe shifts toward other exporters to secure volumes (which are all further away), ton-mile demand is forecasted to increase materially. Furthermore, considering how sanctions on Russian oil and products are structured, additional inefficiencies are arising, also leading to incremental ton-mile demand gains.

{kind=link}

ASC’s Q4 earnings presentation, slide 31.

For instance, it was recently reported that India was importing Russian CPP, blending them, and re-exporting those to Europe. Some may view that as sanctions "evading," or even "cheating," but I believe that's not the case. The intent of the sanctions on Russian oil and products was to reduce Russia’s income from energy sales while keeping the world market well supplied, and in that regard, it seems sanctions are working.

Overall, shifting trade patterns are expected to support ton-mile demand throughout 2023 on the back of sanctions on Russian CPP exports as well as due to the closure of refining capacity in net importing regions coupled with refinery additions in net exporting countries. However, a potential recession remains a significant risk (and recent weakness in crack spreads is not a step in the right direction), whereas a normalization of trade with Russia would also weigh on market balances.

Product Tanker Supply

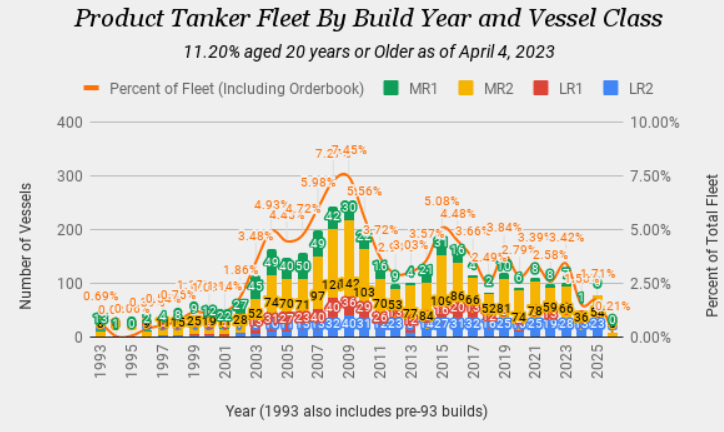

The product tanker supply side remains extremely attractive, with the orderbook currently sitting at just 5.99% of the fleet. Although it has increased slightly since the record lows reached last May at around 5.26%, fleet growth is still forecasted to be abnormally low over the next few years.

A breakdown of the product tanker fleet by age and vessel class is provided below (which also includes gross fleet growth estimates until 2026). Over the next few years, supply additions are forecasted to be limited, whereas the substantial amount of vessel deliveries witnessed starting in 2004 will soon become 20-years-old (which should undermine its competitiveness, and ultimately lead to scrapping).

{kind=link}

Value Investor’s Edge.

Year-to-date, a total of 34 LR2, six LR1, and 32 MR2 orders have been placed, which compares to 20 LR2 and 53 MR2 orders placed in 2022. This represents a substantial increase and warrants close monitoring going forward, but it has not yet become substantial enough to shift market balances going forward.

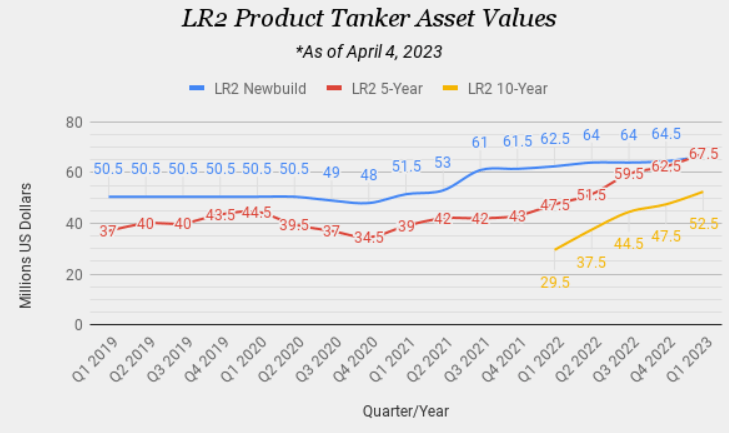

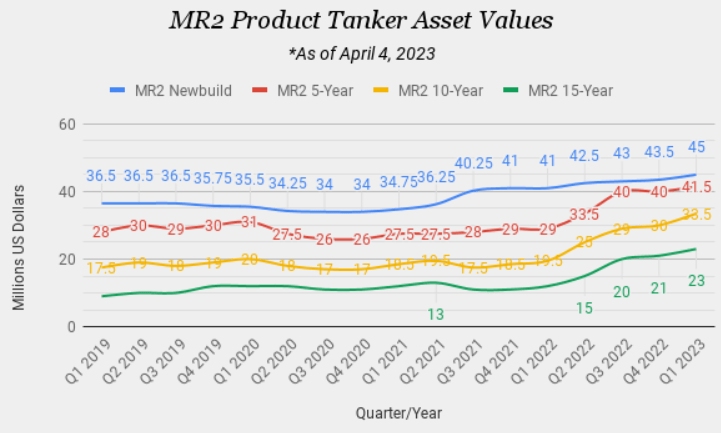

Interestingly, LR2 ordering has picked up materially more than interest on MR2s, and that’s attributable to how the asset pricing curve is currently situated. As can be seen in the image below, five-year-old LR2s are valued above newbuild parity, whereas MR2s are not there yet. If second-hand assets are cheaper than newbuilds, owners will likely favor the former considering the strong FCF these assets are generating in current markets.

{kind=link}

Value Investor’s Edge.

{kind=link}

Value Investor’s Edge.

Although newbuild ordering has started to pick up, the supply side of the product tanker sector remains attractive due to the low orderbook and ageing fleet, which should result in scrapping should rates weaken going forward (year-to-date, only four MR2s have been scrapped, which amounts to virtually nothing). Additionally, major environmental regulations (EEXI and CII) are poised to slow down the global fleet with incremental annual impacts expected from 2024 through 2027. These regulations have the impact of a synthetic supply reduction and are likely to more than offset the anemic current orderbook.

Without further ado, let’s delve into the public tanker equities and my current view on them:

TORM: Best-in-Class, but Overvalued Relative to Peers

When I published the “ Why is it Time to Invest in Product Tankers ” article, I mentioned TORM was my top pick in the product tanker sector, and returns have been phenomenal since (nearly a 4x total return when including dividends). However, this outperformance has stretched its relative valuation, and the company is now trading at a sizable premium to peers.

I still believe the company is best-in-class, with an extraordinarily solid operating platform and a competitive cost breakeven, whereas their dividend policy (consisting of distributing all excess FCF on a quarterly basis) is also industry leading, but the valuation has gotten a bit stretched, especially considering the Oaktree overhang.

In late March, TRMD announced a secondary offering by Oaktree (which owns 66% of the company) for 5M shares, or about 6% of the outstanding. However, share pricing dived on the news, and Oaktree ultimately pulled the plug on the offering the next day . Oaktree has a good track record in the shipping industry, and their disposals have been nimble (be it in Star Bulk Carriers, Hafnia, or the recent attempt in TRMD). However, this puts a lid on how high TRMD’s relative valuation could get in a very strong market, as I expect Oaktree to attempt additional disposals if TRMD trades at a sizable premium to NAV.

On the other hand, TRMD’s management has started to take advantage of their premium valuation by pursuing vessel acquisitions (and financing the equity portion with share issuance). The company owns the oldest fleet among product tanker pure-plays (INSW owns a mixed fleet that is slightly older), which also means that at some point they will have to pursue a fleet renewal program.

Overall, my view on TRMD’s operational efficacy and managerial expertise has not changed, but its higher relative valuation coupled with the Oaktree overhang will most likely weigh on its relative performance going forward and TRMD is an avoid at this juncture relative to peers.

Ardmore Shipping: Expensive Relative to Peers

Ardmore Shipping ( ASC ) now has the second highest relative valuation in the product tanker sector, slightly trailing TRMD. The company is trading at a slight discount to NAV, but at current pricing I favor several of its peers.

ASC recently initiated a shareholder returns program consisting of the distribution of one-third of net income. Although the announcement of a returns program is always a step in the right direction, I personally expected management to take a more aggressive stance. Given their ultra-low leverage ratio (the lowest in the sector) coupled with a decently-aged fleet, they could be distributing a far higher percentage of net income and still be in a rock-solid financial position. I would prefer to see 50-75% payouts at this stage in the cycle.

Going forward, I would not be surprised to see ASC pursuing some second-hand acquisitions. On the other hand, there's also the potential for higher payouts considering they own a solid fleet (100% MRs). On the latest conference call, they mentioned they were open to distributing special dividends if they were not able to pursue attractive/accretive acquisitions. At current pricing, the company is trading at a premium to most of its peers, which leads me to avoid ASC in favor of other equities.

Scorpio Tankers: Attractive Discount, but Uncertain Shareholder Returns

Scorpio Tankers ( STNG ) owns the most modern fleet in the sector while also having the highest scrubber prevalence among peers. Operational performance over the past few years has been decent, but the company has seemingly not been able to fully leverage its eco + scrubber component (at least relative to peers such as TRMD, which has fetched similar results with an older fleet).

Before the Russian invasion of Ukraine, STNG was in a dire financial position due to its heavily indebted balance sheet. However, the company has focused most FCF generation over the past year toward debt reduction (and share repurchases), and its balance sheet is now night-and-day relative to one-year ago.

The company is once again trading at a very enticing discount to NAV, especially considering I expect them to shift towards heavy dividend payouts during H2-23 if the product tanker market remains strong. Management has been clear they like being able to allocate excess cash toward share repurchases at current pricing, but as leverage continues to fall, I expect a shift towards large dividends (or maybe a mix between dividends and repurchases if they continue to trade at a large discount to NAV).

STNG reported Q1 earnings yesterday. Operational performance was aligned with our expectations, whereas forward Q2 guidance was solid as well. Management's overall market commentary was also positive, underlining that they believe recent "weakness" is attributable to refinery maintenance.

Since STNG owns the most modern fleet in the sector, fleet renewal is not in the cards, which provides more leeway for capital returns, be it share repurchases or dividends). The company’s leverage has fallen materially y/y, and I believe a shift toward heavy returns is likely going forward. However, uncertainty regarding what kind of shareholder returns policy they will ultimately pursue most likely weighs on relative valuation.

International Seaways: Cheap, but Lacks Clear Returns Policy

International Seaways ( INSW ) owns a mixed fleet with exposure to most tanker classes, from MRs on the product side to the larger VLCCs on the crude segment. After briefly attaining a reasonable valuation, the company is now back to trading at a large discount to NAV, which makes INSW very attractive at current pricing.

The company does not have a clear shareholder returns program, considering they are only distributing $0.12/sh on a quarterly basis, which represents a negligible portion of FCF. However, the board declared a special dividend on Q3 and on Q4 earnings, distributing $1.00/sh and $1.88/sh respectively (on top of the recurring $0.12/sh dividend). Their current policy leaves shareholders guessing and a clearer commitment to distributing perhaps 50-60% of earnings would be preferred.

Looking at upcoming Q1 results (scheduled for this Thursday, May 4), I expect the company to distribute a similar $1.00 to $2.00/sh dividend (although that is a guess considering there is no firm shareholder return policy). The company has selectively used share repurchases to accrete value over the past few years, but they have taken a more conservative approach over the past few quarters; however, at current pricing I would hope to see some share buybacks considering the large discount to NAV shares currently trade at.

Although I hope the company will institute a firm returns policy going forward, I do not expect it to be overly ambitious (i.e., based on distributing 100% of FCF) since INSW owns an arguably old fleet, especially on the products side. A policy of minimal returns of 50%-60% of quarterly EPS would be a great fit for this firm.

Overall, I believe INSW is a well-managed company trading at an outsized discount relative to peers. The lack of a clear shareholder returns policy is a negative, but the board declared a decent dividend alongside recent Q3-22 and Q4-22 earnings. Going forward, I expect to see additional dividends (and hopefully large share repurchases). Furthermore, I believe the institution of a firm shareholder returns policy would go a long way in improving the company’s relative valuation.

Honorable Mentions: TNP, Hafnia, and D’Amico Shipping

Tsakos Energy Navigation Overview

Tsakos Energy Navigation ( TNP ) owns a mixed fleet with exposure to crude and product tankers as well as three LNG carriers. TNP is trading at an enormous discount to NAV and to peer valuations, but that's arguably attributable to weak communication around Q4 earnings and an inferior governance structure.

Although the upside potential is significant, performance going forward is virtually entirely contingent on management's willingness to pursue shareholder returns (i.e., dividends or share repurchases). Although the company employs several of its assets on time-charters, if rates remain at elevated levels TNP will generate outstanding FCF. However, it remains to be seen whether management will allocate this excess FCF towards meaningful dividends.

In a Capital Link event in early January , management mentioned they intended to distribute between 25% and 50% of net income as dividends, but alongside Q4-22 earnings, they declared a far lower distribution, which weighed materially on sentiment. Going forward, I expect the company to use excess FCF to reduce debt, repurchase preferred shares, and hopefully distribute meaningful dividends to shareholders.

Hafnia Overview

Hafnia is a product tanker company listed in the Oslo exchange. I believe the company is best-in-class (similar to TRMD) with very solid corporate governance. Hafnia pursued heavy fleet expansion before the recent upturn, acquiring CTI Tankers Limited (with a fleet of 32 vessels), buying 12 LR1s from STNG, and they also ordered several newbuilds.

The acquisition of CTI Tankers Limited resulted in Oaktree emerging as a significant shareholder in Hafnia, although they have pursued an exit plan (and they are now virtually out of the company, with only a ~5% stake remaining). The lockup from the most recent secondary recently expired, so I would expect to see the disposal of one last block going forward, which might temporarily weigh on pricing.

Hafnia has a competitive fleet with a low average age (similar to that of STNG). The company has a returns policy in place based off leverage. They distributed 60% of Q4 earnings, but the payout ratio is set to increase to 70% once net LTV falls below 30%, and to 80% once it stands below 20% (likely achieved in mid- and late-2023).

Considering the company is trading at a decent discount to NAV, I currently favor it over TRMD, which I view as a direct peer regarding quality. The company’s returns policy will allow it to deleverage while distributing substantial dividends if markets remain strong. Last year, the company was arguably overvalued (and TRMD was undervalued). Now the market has shifted, offering investors a clear change to reallocate!

D’Amico Shipping Overview

D’Amico Shipping is listed in the Italian market and is a pure play product tanker play. The company has undergone a comprehensive fleet renewal plan over the past few years, and they now own one of the most modern fleets in the sector.

Over the past year, management has allocated excess FCF toward deleveraging and exercising purchase options on leased vessels to lower their cash breakeven. However, they still have the highest leverage among pure play product tankers (only surpassed by TNP, which owns a mixed fleet).

The company is trading at a sizable discount to NAV, which makes it an attractive pick for investors with a positive view on modern product tanker tonnage. DIS employs its vessels on a mix between spot and time charters, which weighed on operational performance throughout 2022, but should not be a major factor in 2023.

Despite 2022 being a very strong year, shareholder returns lagged due to a focus on deleveraging, with the company only distributing a $0.0153/sh dividend (net of the 15% withholding tax) so far. Going forward, I expect management will continue to allocate excess capital towards deleveraging and exercising purchase options and they will hopefully turn toward larger dividend distributions by late-2023.

Conclusion

At current pricing, my favorite “buys” in the product tanker sector are Scorpio Tankers and International Seaways ( INSW ), whereas I believe d’Damico Shipping (Milan: DIS), Hafnia (Oslo: HAFNI), and Tsakos Energy Navigation are also attractive (although the latter has governance concerns and must pivot towards higher shareholder returns or shares will continue to lag peers).

Ardmore Shipping and TORM Plc have fared very well over the past year, but they are now trading at a premium to peers (especially TRMD), which makes them somewhat unattractive. These two firms are avoids or “holds” at this juncture. I'm not outright bearish, but it certainly makes sense to take profits here and allocate toward the more attractive peers mentioned above.

The low-hanging fruit in the product tanker sector is gone, but if market balances remain tight, most companies in the sector are set to distribute significant dividends going forward and we might still see substantial stock price appreciation. Spot rates have been under pressure over the past few weeks, but this appears mostly in-line with seasonal patterns.

The medium-term product tanker outlook remains positive if the sanctions on Russian products remain intact and newbuild ordering does not get out of hand. We have seen some owners head towards newbuild orders over the past few months, but this is not yet concerning, especially since most delivery dates land between late-2025 and 2026; however, forward supply must be closely monitored.

For further details see:

Top Picks For Today's Product Tanker Market