NDAQ - Top-Tier Financial Dividend Growth With Nasdaq

2023-08-31 10:33:48 ET

Summary

- Nasdaq Inc. is a strong technology proxy with a competitive dividend yield, low payout ratio, and high dividend growth.

- The company's transformation into a leading technology provider for the financial system has been successful, with investments in cloud computing, AI innovation, and strategic acquisitions.

- Nasdaq's focus on market modernization, ESG trends, and anti-financial crime initiatives enhances its cross-selling potential and presents an attractive opportunity for long-term investors.

Introduction

While there are certainly exceptions, I would make the case that it can be quite tough to find good dividend growth stocks in technology-related sectors. The fastest-growing companies tend to come with very low yields, while the companies with higher yields are often companies with slow growth.

Although Nasdaq Inc. (NDAQ) isn't an official member of the technology sector, I believe it's a great technology proxy for several reasons.

- Tech bull markets support higher IPO volumes and related activities.

- Technology stocks benefit from lower rates and subdued inflation. This also goes for NDAQ, which is increasingly focused on offering new services to tech/financial companies.

What makes NDAQ so interesting is the fact that it has a competitive dividend yield of 1.7%, a low payout ratio, and high dividend growth backed by rapid diversification into financial tech and related services.

Although economic headwinds could keep a lid on the stock, I believe that on a longer-term basis, we're dealing with an undervalued opportunity for investors seeing diversified dividend growth in the tech sphere.

I used to own NDAQ a while ago. However, I sold it to focus on other dividend growth opportunities and expand my CME Group ( CME ) position, which is a futures-focused peer of NDAQ.

Now, I want back in.

Let me explain why that is.

Well-Diversified & Consistent Growth

While I'm a big fan of all major NDAQ peers, the transformation of Nasdaq is the most fascinating to watch.

Nasdaq's transformation started in 2017 by focusing on becoming a leading technology provider for the global financial system, which sounds quite ambitious.

This shift involved capital allocation to growth opportunities and realigning businesses with key economic trends.

Since then, Nasdaq has invested in cloud computing and AI innovation across its products and markets while divesting over $700 million in non-core assets.

{kind=link}

Earlier this year, the company also acquired Adenza, which aligns with Nasdaq's vision to be a trusted fabric of the financial system.

According to Nasdaq on June 12:

The addition of Adenza to Nasdaq's trusted brand and platform of mission-critical solutions complements Nasdaq's Marketplace Technology and Anti-Financial Crime solutions and significantly enhances Nasdaq's offerings across an even broader spectrum of regulatory technology, compliance, and risk management solutions . With Adenza, Nasdaq will also be able to provide comprehensive support to financial institutions, establishing a multi-asset class, full trade lifecycle platform with unmatched regulatory technology solutions.

Nasdaq believes that Adenza's capabilities enhance its serviceable addressable market by about 40%, addressing regulatory challenges and offering solutions for risk management.

During the recent Oppenheimer Annual Technology, Media, Internet & Communications Conference, Nasdaq CEO Friedman explained that Adenza's strength lies in its flexible module-based strategy.

For example, Adenza's platforms offer a modular approach that begins with addressing a specific need for clients and then expands by adding modules that cater to broader requirements.

This strategy mirrors Nasdaq's Market Tech business model and allows for incremental growth by upselling to existing clients.

About half of Adenza's growth comes from upselling, with the rest attributed to new client sales and pricing strategies.

With regard to synergies, CapEx for Adenza is around $20 to $30 million annually, and Nasdaq itself is capital-light, with $150 to $200 million CapEx each year.

The potential for margin expansion comes from achieving synergies, leveraging Adenza's high-gross-margin platform, and cloud adoption.

The goal is to efficiently deliver services and build a leverageable platform for future growth and margin expansion.

I believe there's definitely potential here.

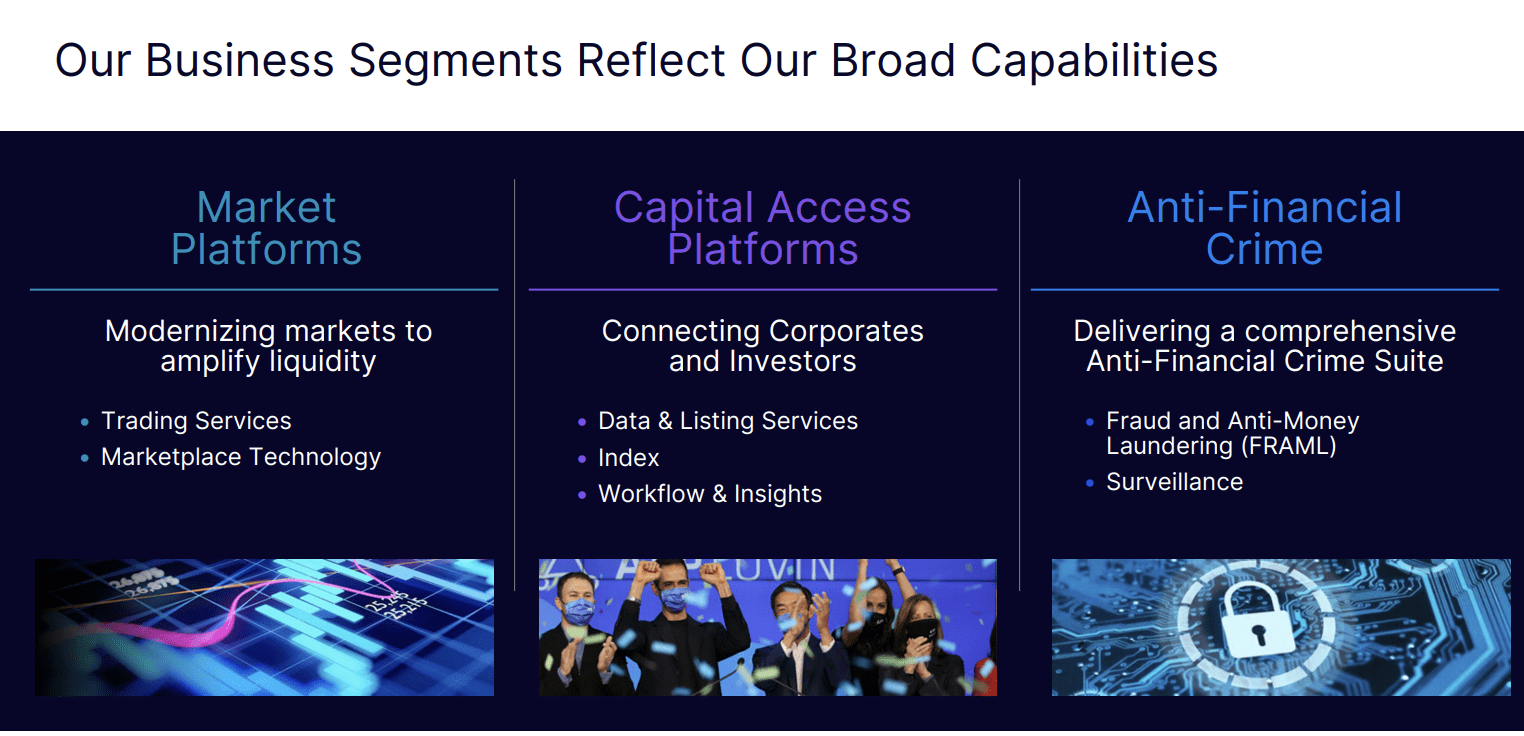

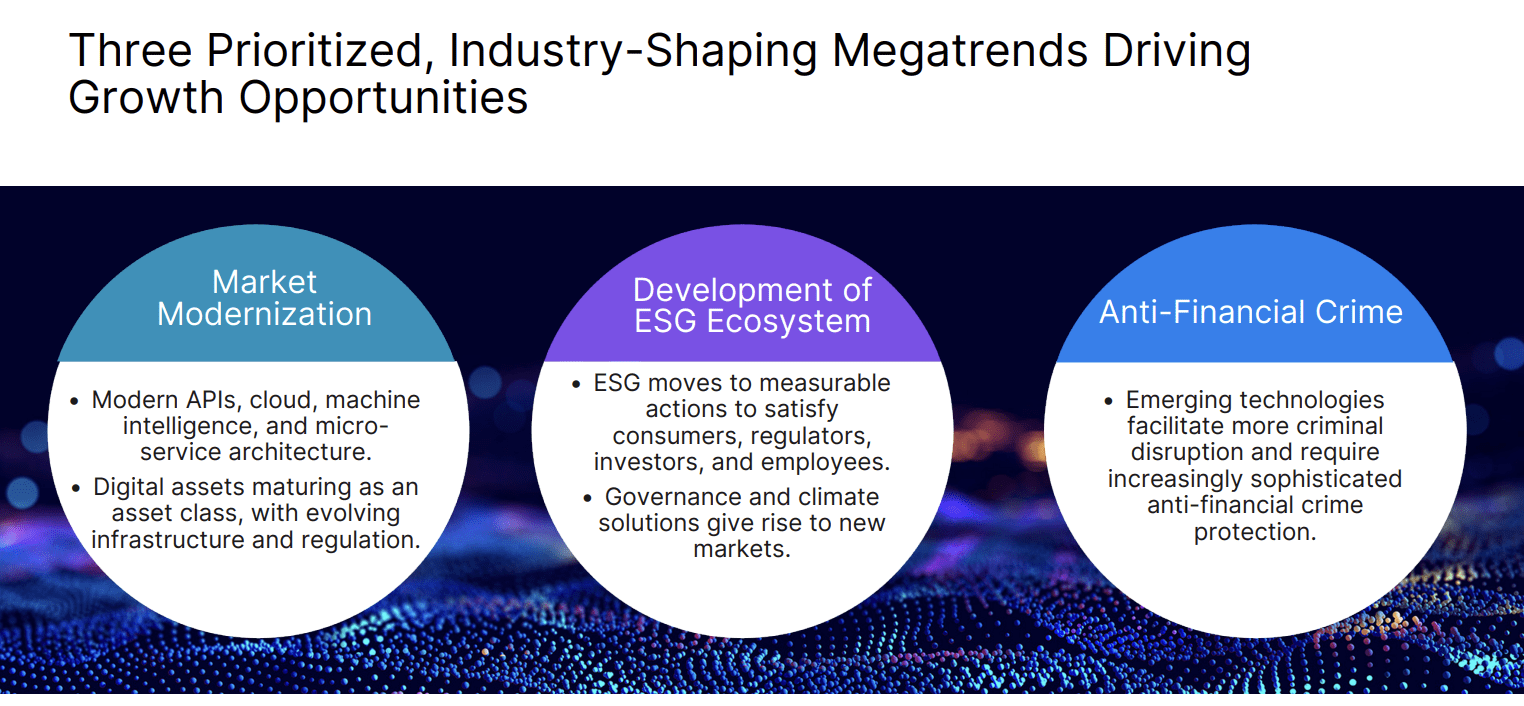

On top of that, the company is working on benefiting from three megatrends to grow its business over time. This includes Adenza.

- Market modernization.

- Development of an ESG ecosystem.

- Anti-financial crime.

{kind=link}

These opportunities involve another major benefit: cross-selling.

The cross-selling potential is especially strong in areas like risk management, surveillance, and trading analytics.

Different decision-makers and roles within financial institutions create opportunities for introducing and integrating Nasdaq's offerings.

The broader one's product portfolio is, the easier it is to build long-lasting relationships with customers that make it easier to up and cross-sell.

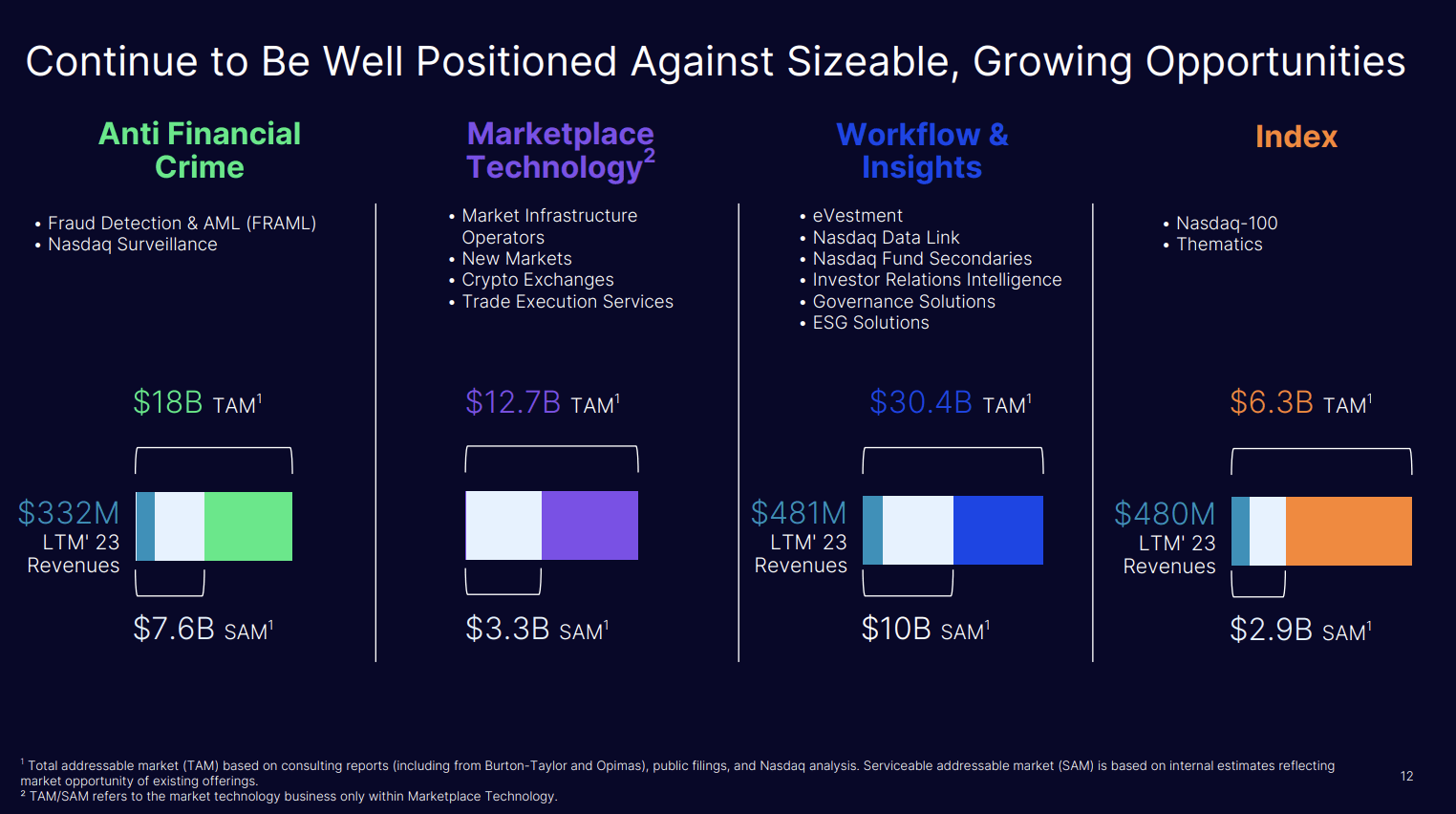

Looking at the numbers below, the company believes it has barely scratched the surface of big addressable markets in anti-financial crime, marketplace technologies, and related solutions.

{kind=link}

Having said that, Nasdaq continues to do well.

In the second quarter, Nasdaq generated $925 million in net revenues, reflecting a 4% increase compared to the prior year, both on a reported and organic basis.

- Revenue from Solutions businesses reached $674 million, up 6% organically.

- Total Annualized Recurring Revenue ("ARR") grew by 6.5% to $2.1 billion, with Annualized SaaS revenues of $755 million, representing an 11% annual growth rate.

- The SaaS revenues constituted 36% of the total company ARR.

- The Capital Access Platforms division delivered $438 million in total revenue, a 4% increase, with Index revenues growing organically by 4%.

- Revenues within Workflow and Insights grew by 5% organically, driven by consistent demand for IR, ESG solutions, and analytics solutions.

Furthermore, during its 2Q23 earnings call, the company made clear that upon the completion of the Adenza acquisition, Nasdaq's focus will be on maximizing client and shareholder benefits.

The company plans to deleverage, increase dividends, and execute stock buybacks.

Shareholder Distributions

In light of the bigger picture, the company's plans include increasing dividends to achieve a 35-38% payout ratio over 3-4 years.

Currently, the company pays a 1.7% dividend yield with a 30% payout ratio. The 5-year dividend CAGR is 9.2%. On April 19, the company hiked its dividend by 10%.

The Adenza acquisition is expected to generate around $300 million in unleveraged pre-tax cash flow in 2023.

Debt financing for Adenza's acquisition will result in annual interest payments of about $325 million.

Nasdaq aims to use Adenza's incremental free cash flow to fund debt repayment and share buybacks.

So far, net buybacks had a muted impact.

Over the past ten years, net buybacks were 2%, which is subdued due to acquisitions and share-based compensation.

For example, last year, the company bought back stock worth $310 million. It had a share-based compensation of $106 million.

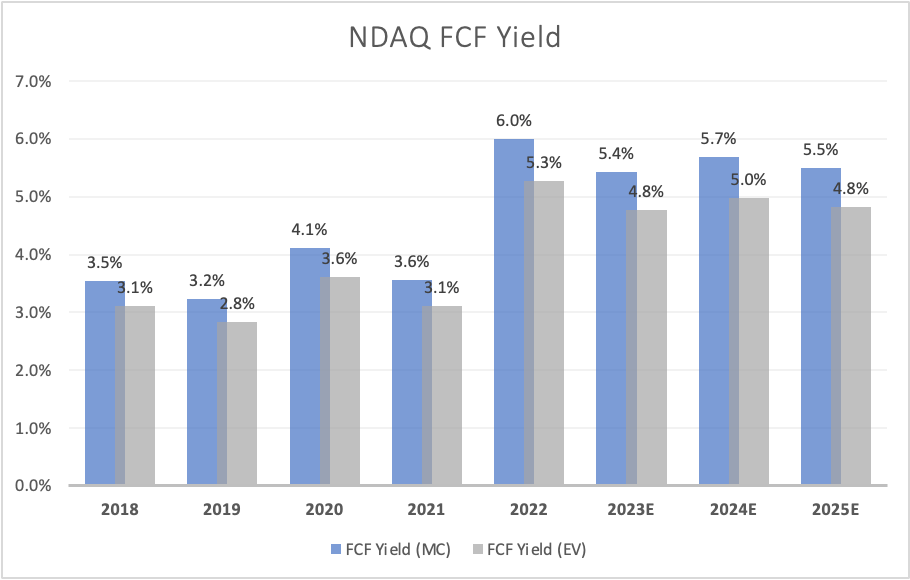

Looking at free cash flow expectations, we see that the company is in a good spot to accelerate dividend payments and debt reduction.

The company is expected to maintain an FCF yield close to 6%. In other words, the company has a cash payout ratio of roughly 31%.

Leo Nelissen (Based on analyst estimates)

{kind=link}

The company is also upbeat about its balance sheet.

In the second quarter, the adjusted total debt to trailing 12 months non-GAAP EBITDA ratio remained at 2.6x.

Hence, NDAQ believes it is well positioned to support growth with a strong balance sheet and cash flow generation, which I agree with.

Valuation

NDAQ shares haven't done so well over the past 12 months, underperforming the S&P 500, the tech-heavy ETF ( QQQ ), and its Broker-Dealers & Securities Exchanges ( IAI ) peers.

I believe this is partially caused by uncertainty surrounding the company's transformation. The market is trying to assess what kind of company Nasdaq may be a few years from now.

Given what I discussed in this article so far, I am very confident the transformation will bear fruit.

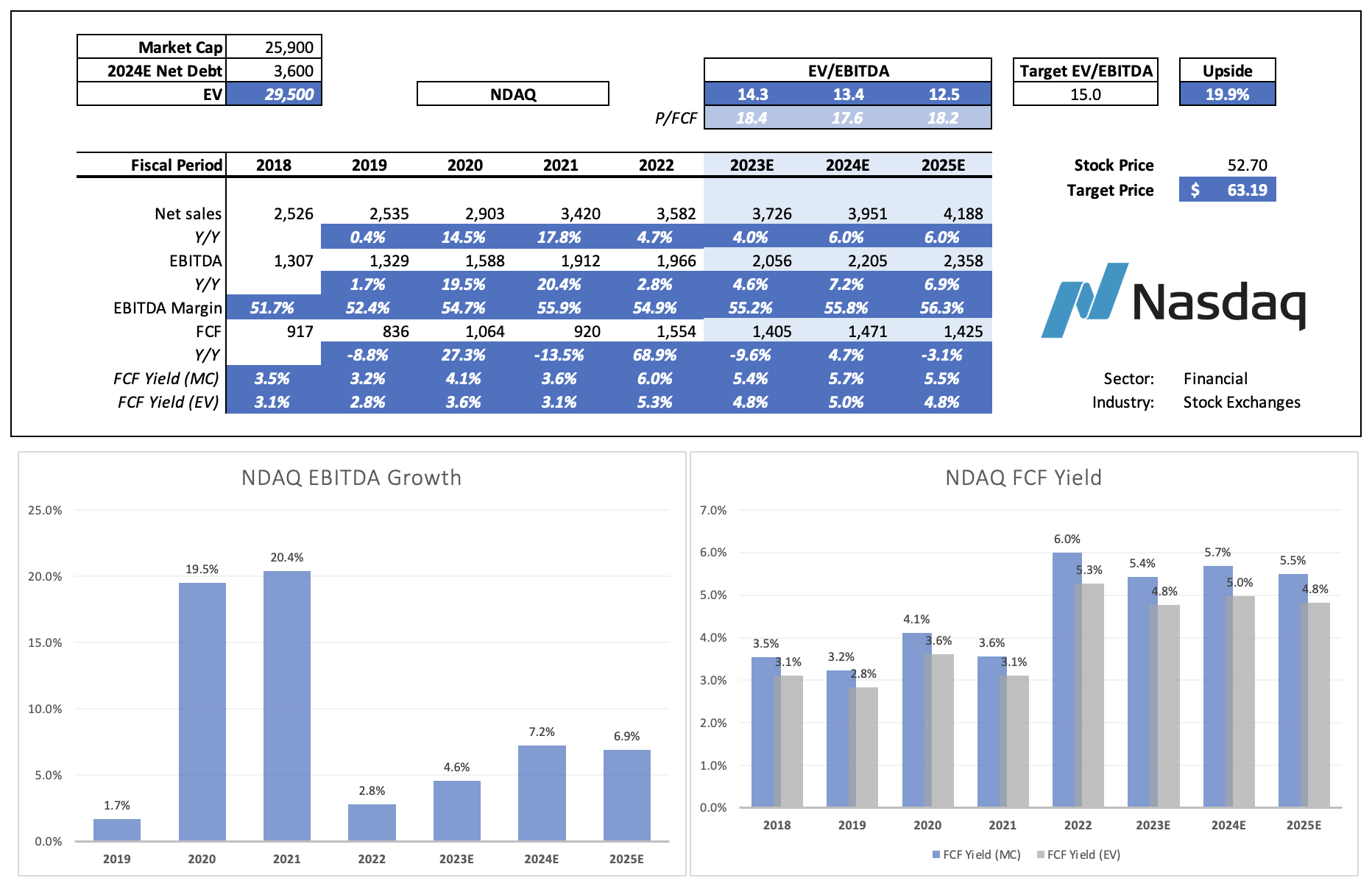

Having said that, NDAQ is trading at 14.7x NTM EBITDA. It is now trading at its lowest valuation since pre-pandemic levels, which is fair, as the valuation between 2020 and 2022 was a bit inflated by low rates and buying panic in tech stocks.

Going forward, Nasdaq is upbeat about its environment. The economy is still solid enough to provide high growth rates, the IPO pipeline is strong, and analysts suggest that high single-digit EBITDA growth in both 2024 and 2025 is likely.

If we apply a 15x longer-term EBITDA multiple, the company has roughly 20% upside to what I believe is its fair value. On a longer-term basis, if services growth accelerates, I think we'll see a higher multiple than that.

Leo Nelissen (Based on analyst estimates)

{kind=link}

The current consensus price target is $60, which is 14% above the current price.

FINVIZ

I'll give Nasdaq a Buy rating based on its longer-term potential.

However, I do not rule out a bit more weakness before we get a meaningful uptrend. We're seeing tremendous stress on the economy.

If a potential rebound in inflation forces the Fed to keep rates elevated despite weakening economic fundamentals, I believe that fundamentals in NDAQ's business could weaken enough to reduce the mid-term outlook.

Hence, long-term investors interested in buying NDAQ might be better off buying in intervals. Start small and buy more gradually over time. That way, if NDAQ falls, investors can average down. If it takes off, investors have a foot in the door.

This is how I currently deal with all of my investments.

Takeaway

With a resilient dividend yield of 1.7%, robust dividend growth, and a strategic shift towards financial tech and related services, Nasdaq emerges as a solid technology proxy.

The company's transformation, marked by investments in cloud computing, AI innovation, and strategic acquisitions like Adenza, positions it for significant growth.

Nasdaq's ability to capitalize on market modernization, ESG trends, and anti-financial crime initiatives enhances its cross-selling potential.

Nasdaq's lower valuation and optimistic growth projections present an attractive opportunity for long-term investors.

While market uncertainties persist, gradually building a position in Nasdaq allows investors to navigate potential fluctuations.

As I navigate my investments, I view Nasdaq as a Buy with promising long-term potential.

For further details see:

Top-Tier Financial Dividend Growth With Nasdaq