OKE - Top-Tier Income: ONEOK's Undervalued 6% Yield

2023-07-22 10:05:07 ET

Summary

- ONEOK Inc. is a top high-yield energy stock with a 6% yield, strong balance sheet, and substantial presence in the natural gas space.

- The company benefits from stable cash flow with over 90% fee-based income, making it appealing to income-focused investors.

- ONEOK's strategic growth plans, including the potential acquisition of Magellan Midstream Partners, support its long-term performance and dividend growth outlook.

Introduction

While I do not own ONEOK, Inc. ( OKE ) personally, it's a holding in a lot of portfolios that I advise, and a lot of friends of mine own it - even the ones who aren't even focused on dividend income.

While OKE has a very volatile history, I believe that the company is one of the best high-yields in the energy space. This midstream C-corporation (it does NOT issue a K-1 form!) not only comes with a 6% yield, but it also has improved balance sheet health, its footprint in the North American energy industry, and its ability to generate long-term growth, paving the road for consistent dividend growth.

In this article, I'll share my thoughts on this stock and explain why ONEOK might be the right pick for income-focused investors.

Natural Gas Is The Place To Be

OKE isn't for the faint of heart. At least not in the past. In the past ten years, the company has been through two major sell-offs. The first one started in 2014, when energy commodity prices fell off a cliff, raising doubts about whether midstream operators would run into troubles with lower volumes. At that time, most had very high debt loads due to investments in growth and barely (if any) positive free cash flow. It was truly a horrible period for investors in this space. Needless to say, OKE survived and bounced back quickly.

FINVIZ

The 2020 sell-off isn't that far ago. Back then, the pandemic triggered caused a scenario where nobody knew how bad things could get.

While the initial panic was bad, OKE quickly bounced back again as it became clear that the world was, in fact, not ending.

Now, OKE is now in a much healthier situation - both financially and when it comes to its business environment.

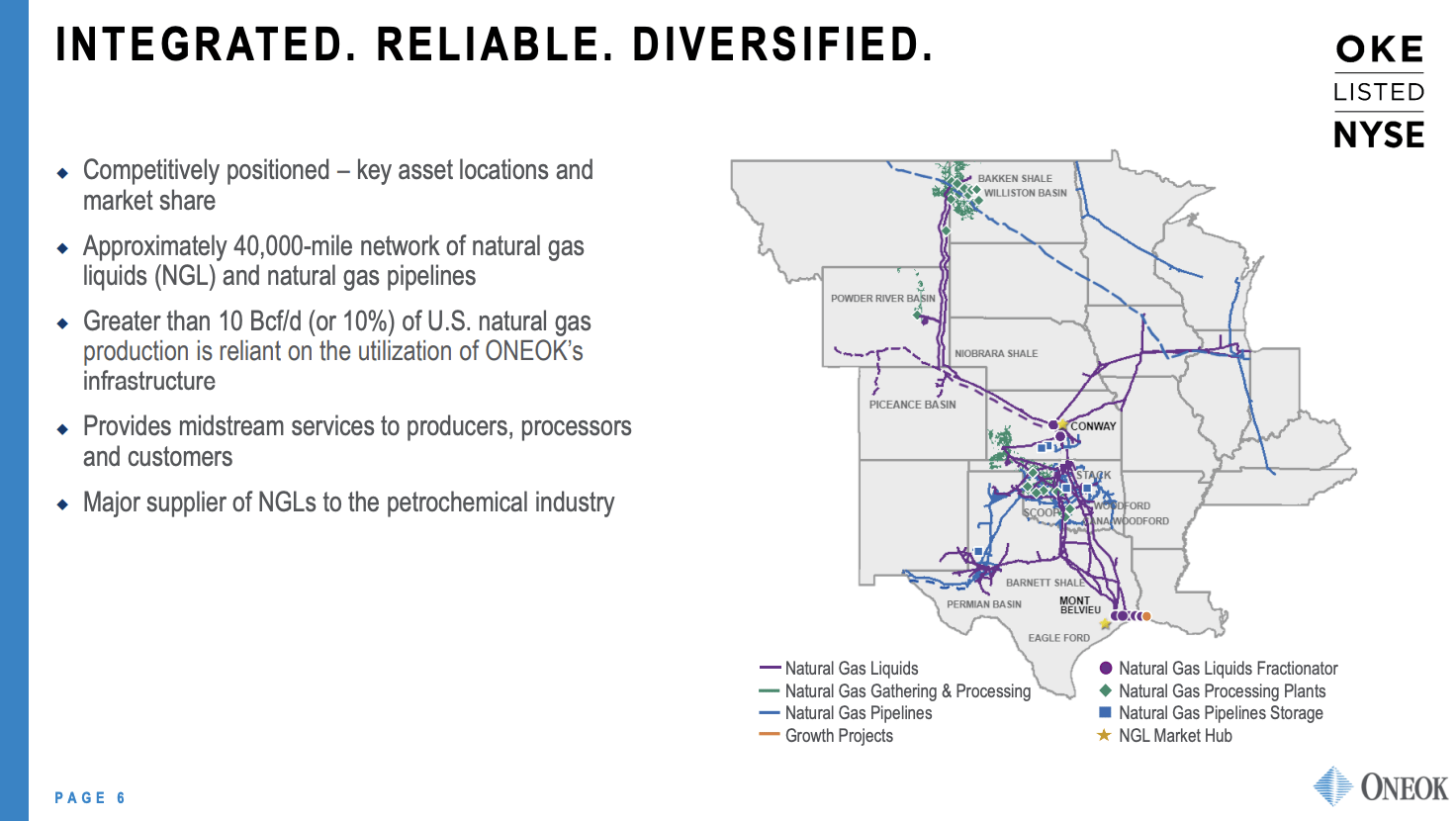

Having said that, OKE isn't just a random midstream company that connects producers to customers. OKE is a giant in the natural gas space.

According to the company (emphasis added):

We are connected to supply in natural gas and NGL producing basins and have significant basin diversification, including the Williston, Permian, Powder River and DJ Basins, and the SCOOP and STACK areas. In our Natural Gas Gathering and Processing segment, we have more than 3 million dedicated acres in the Williston Basin and approximately 300,000 dedicated acres in the SCOOP and STACK areas. In our Natural Gas Liquids segment, we are the largest NGL takeaway provider in the Williston and Powder River Basins; Oklahoma, including the SCOOP and STACK areas; Kansas; and the Texas Panhandle . We also have a significant presence in the Permian Basin.

{kind=link}

I believe that the company and its shareholders have at least two major tailwinds.

- Natural gas and related products are in a great spot. Long-term demand is strong, and demand for midstream services will continue to rise.

In its 2022 Annual Energy Outlook , the EIA estimated that natural gas production would continue to rise consistently towards 45 trillion cubic feet in 2050. While production growth rates are coming down rapidly, output isn't declining for at least another 20-30 years.

Energy Information Administration

By 2050, we project that approximately 25% more natural gas will be produced than consumed in the United States. - EIA

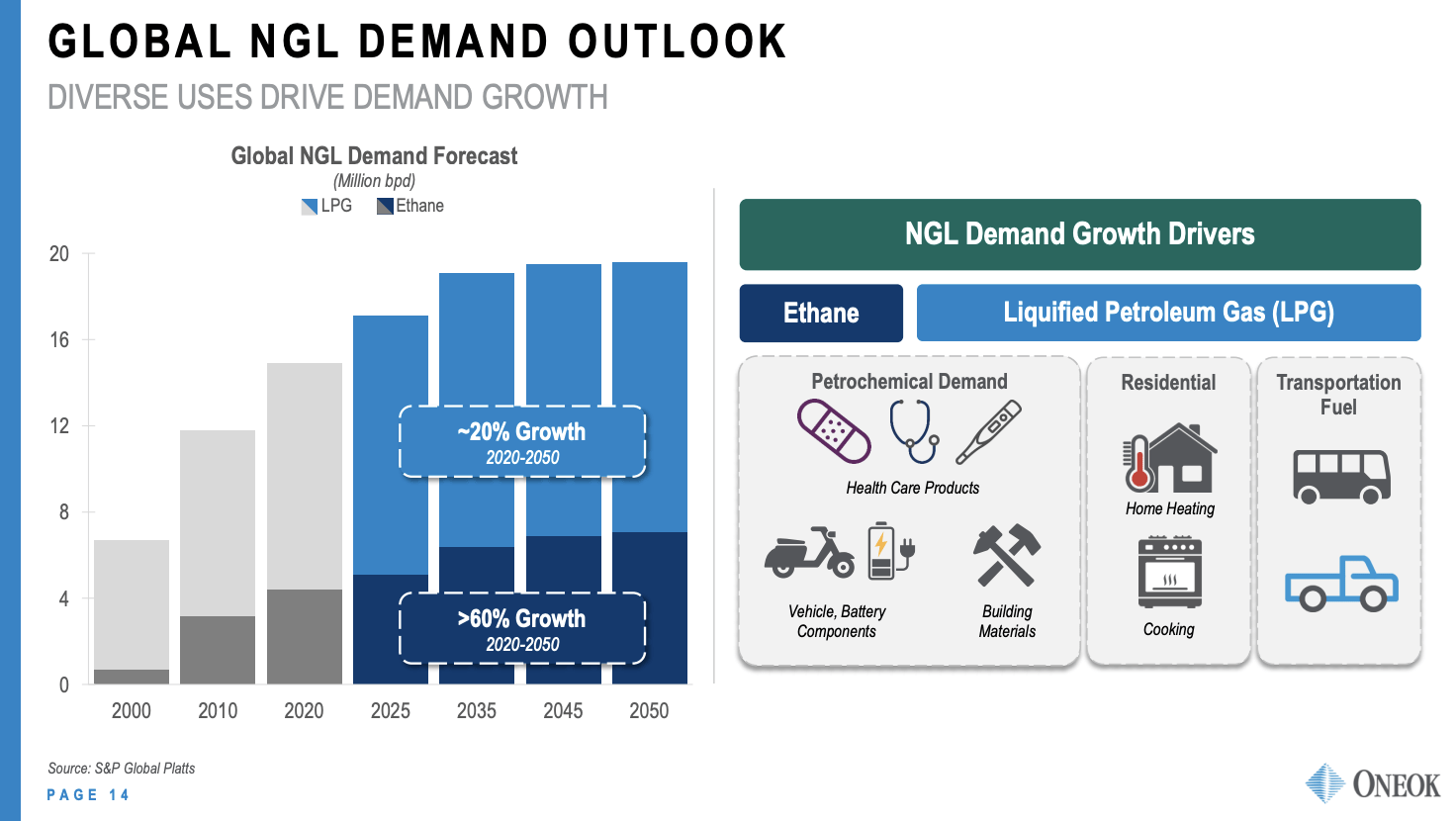

The same goes for global natural gas liquids demand. According to OKE, we can expect roughly 20% demand growth between 2020 and 2050, boosted by petroleum demand, residential demand, and pollution reduction efforts in transportation industries.

{kind=link}

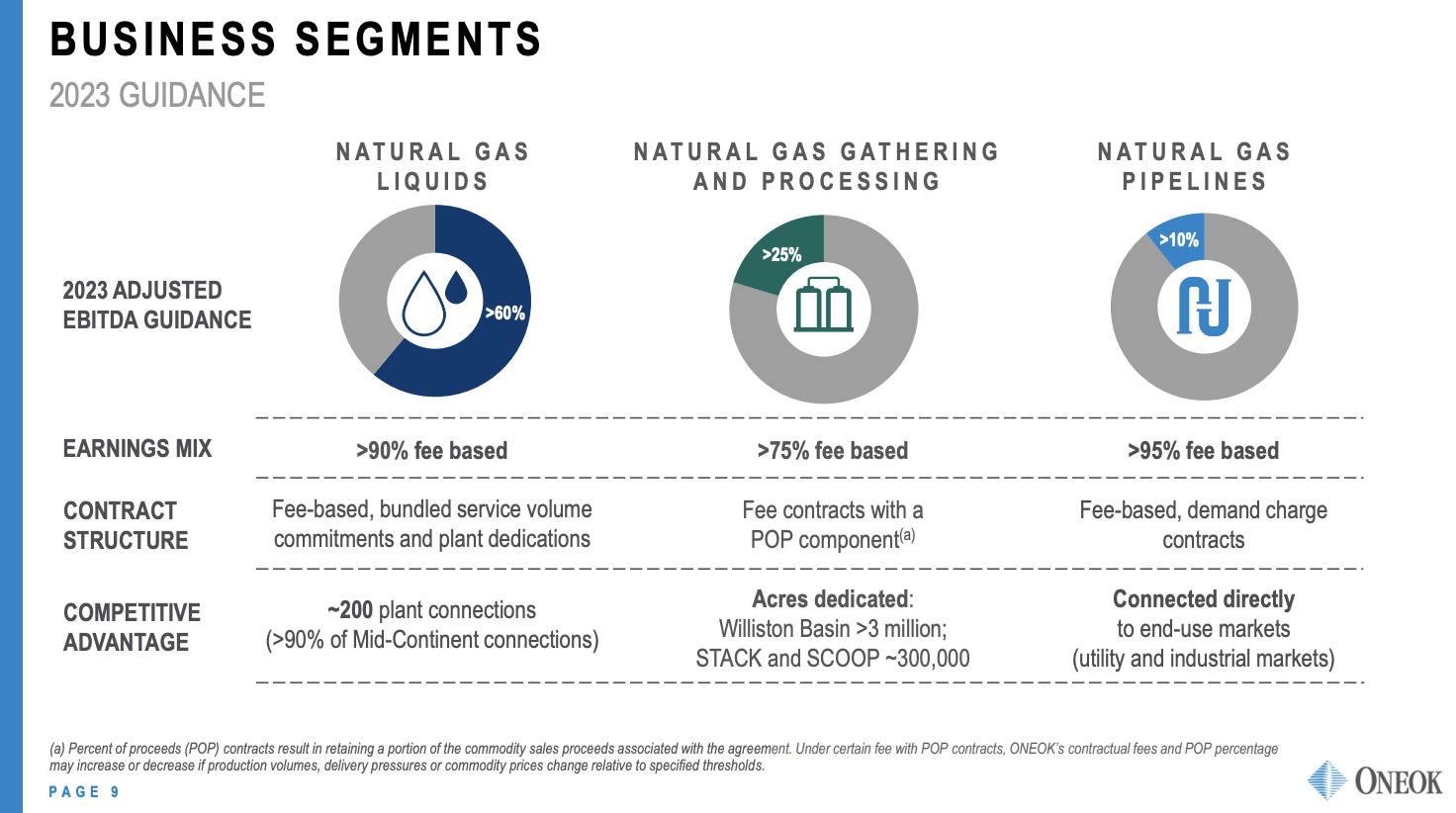

- Most of its income is dependent on fees. Unlike oil and gas drillers (upstream), OKE is not directly dependent on the price of commodities. While a steep slump in prices could harm output growth, the company has a much more stable cash flow profile than most of its customers. Although this does move the advantage to investors in upstream companies during periods of rising commodity prices, it needs to be said that midstream is a source of more predictable income, which is worth a lot to most income-focused investors.

In its NGL segment, more than 90% of flows are fee-based. In the natural gas pipelines segment, that number is above 95%.

{kind=link}

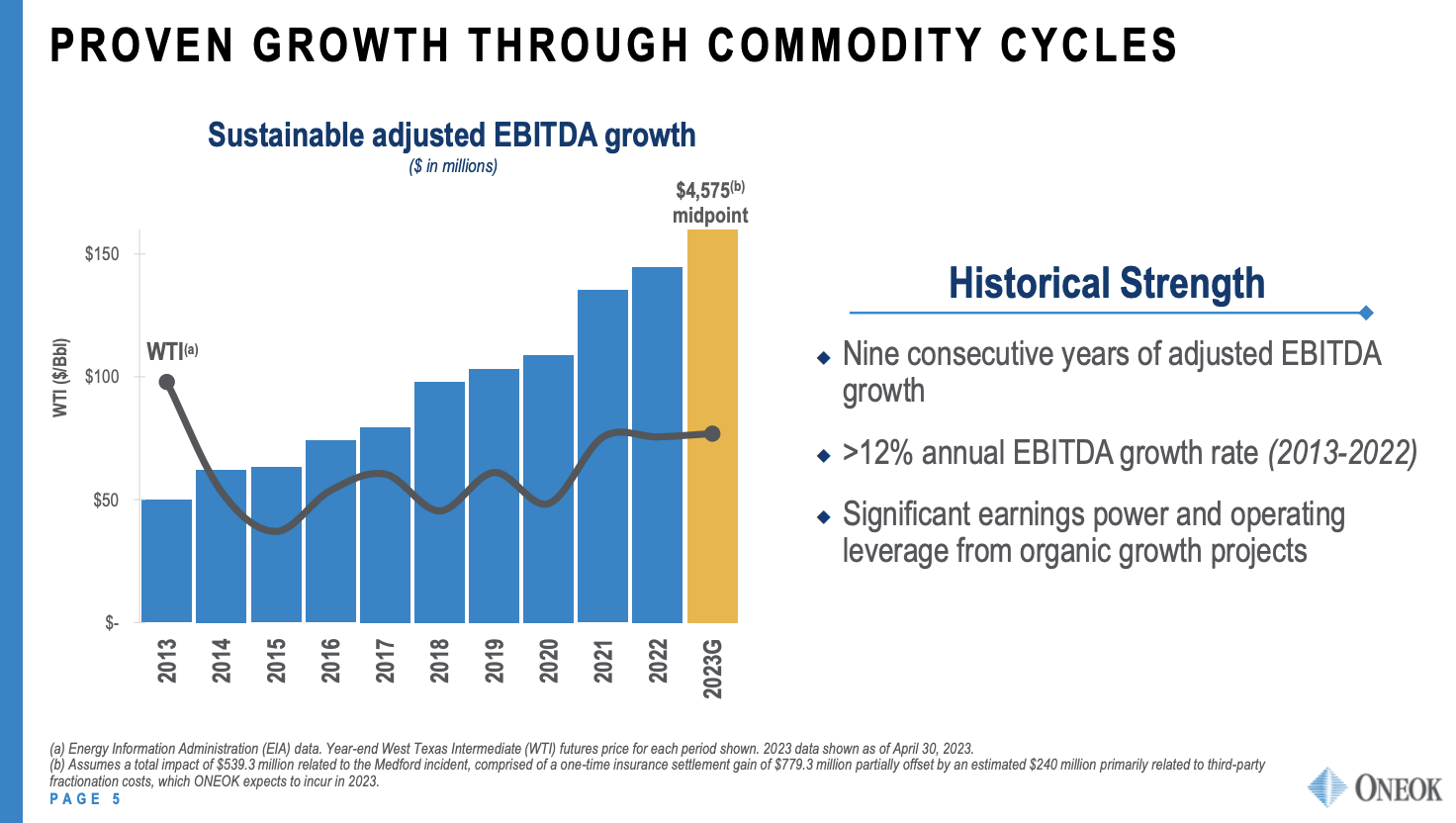

This is what EBITDA growth looks like compared to the smoothed WTI crude oil price:

{kind=link}

To further benefit from opportunities in its industry, the company is expanding.

OKE Is Growing Strategically

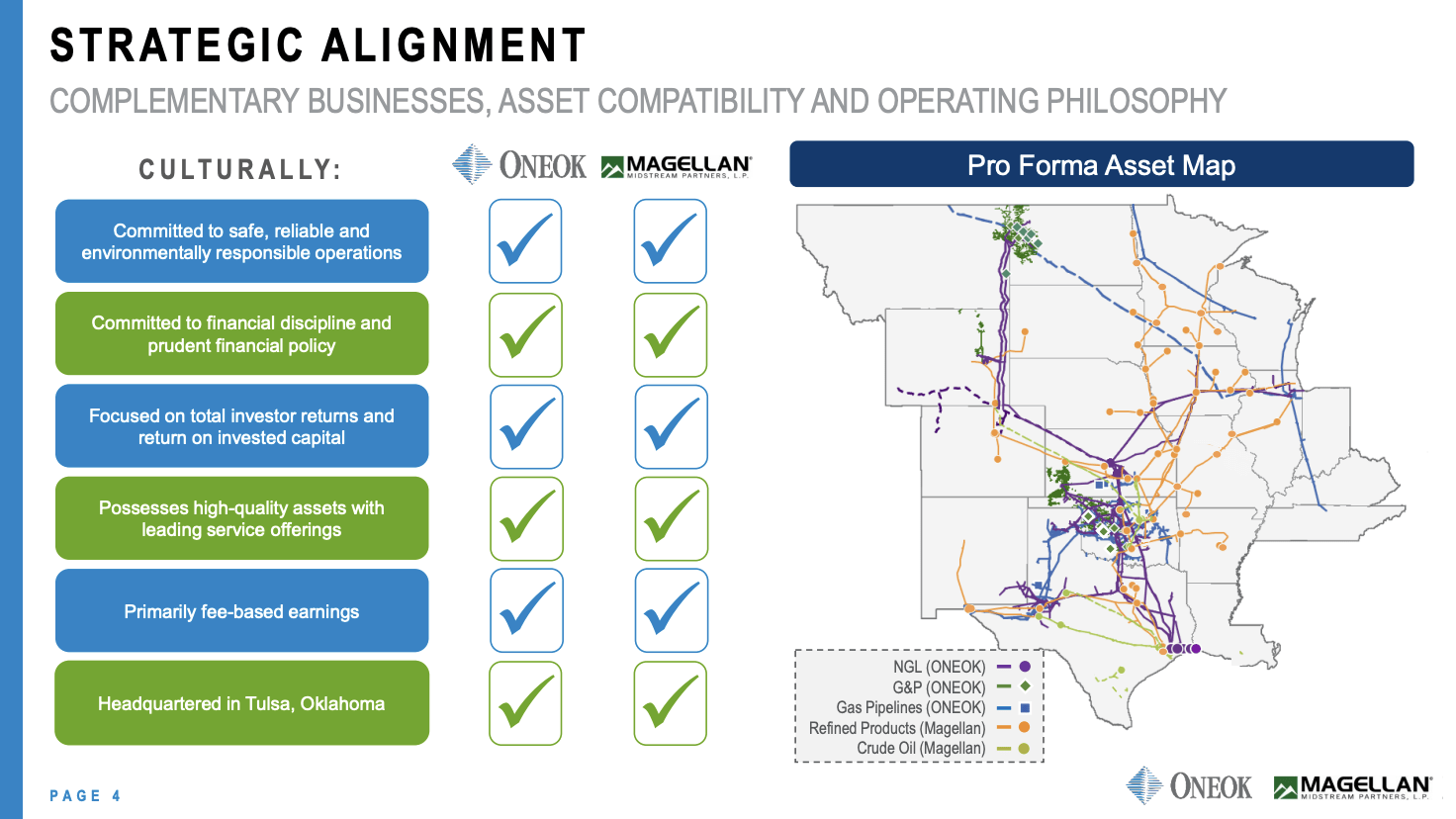

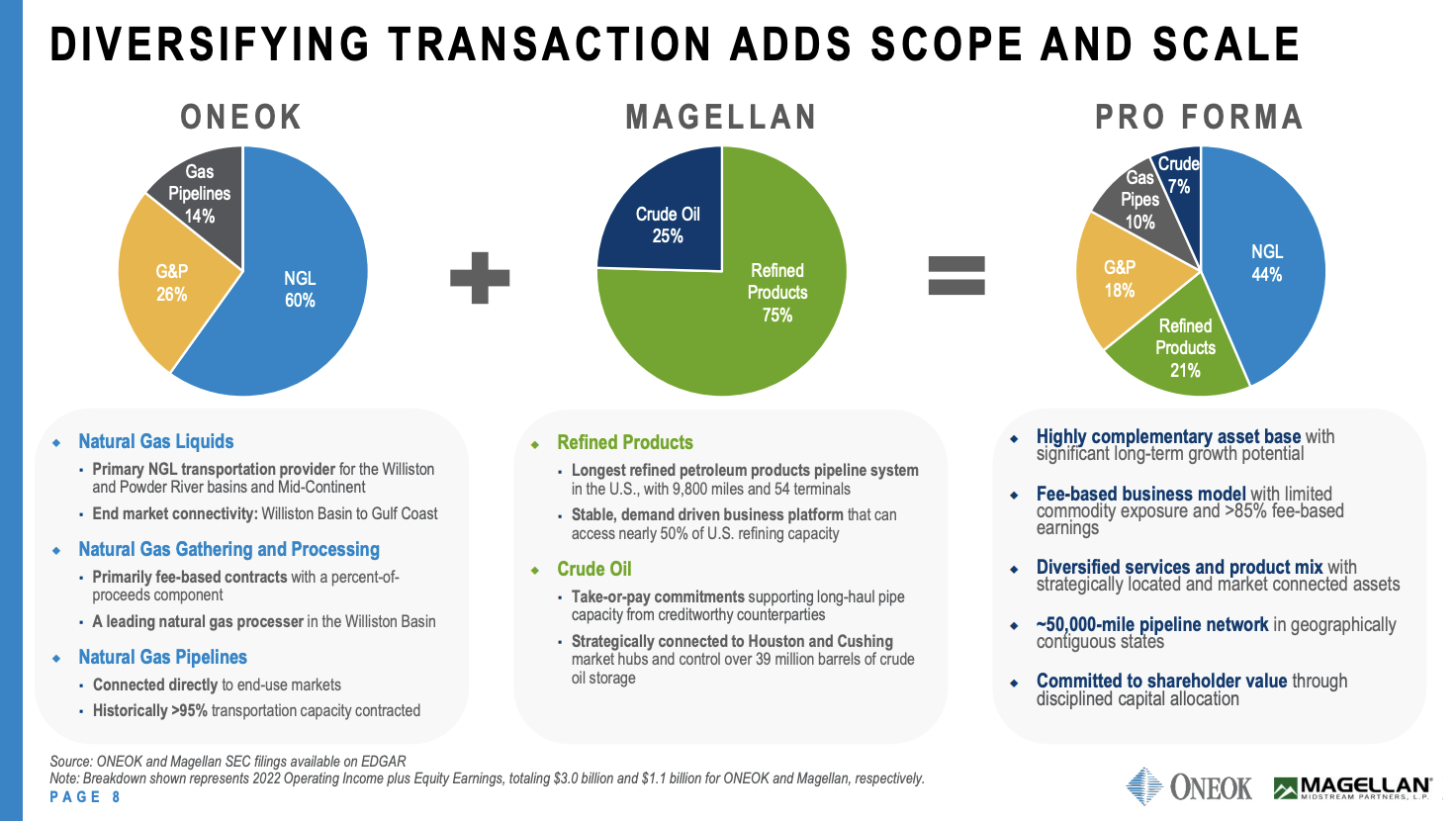

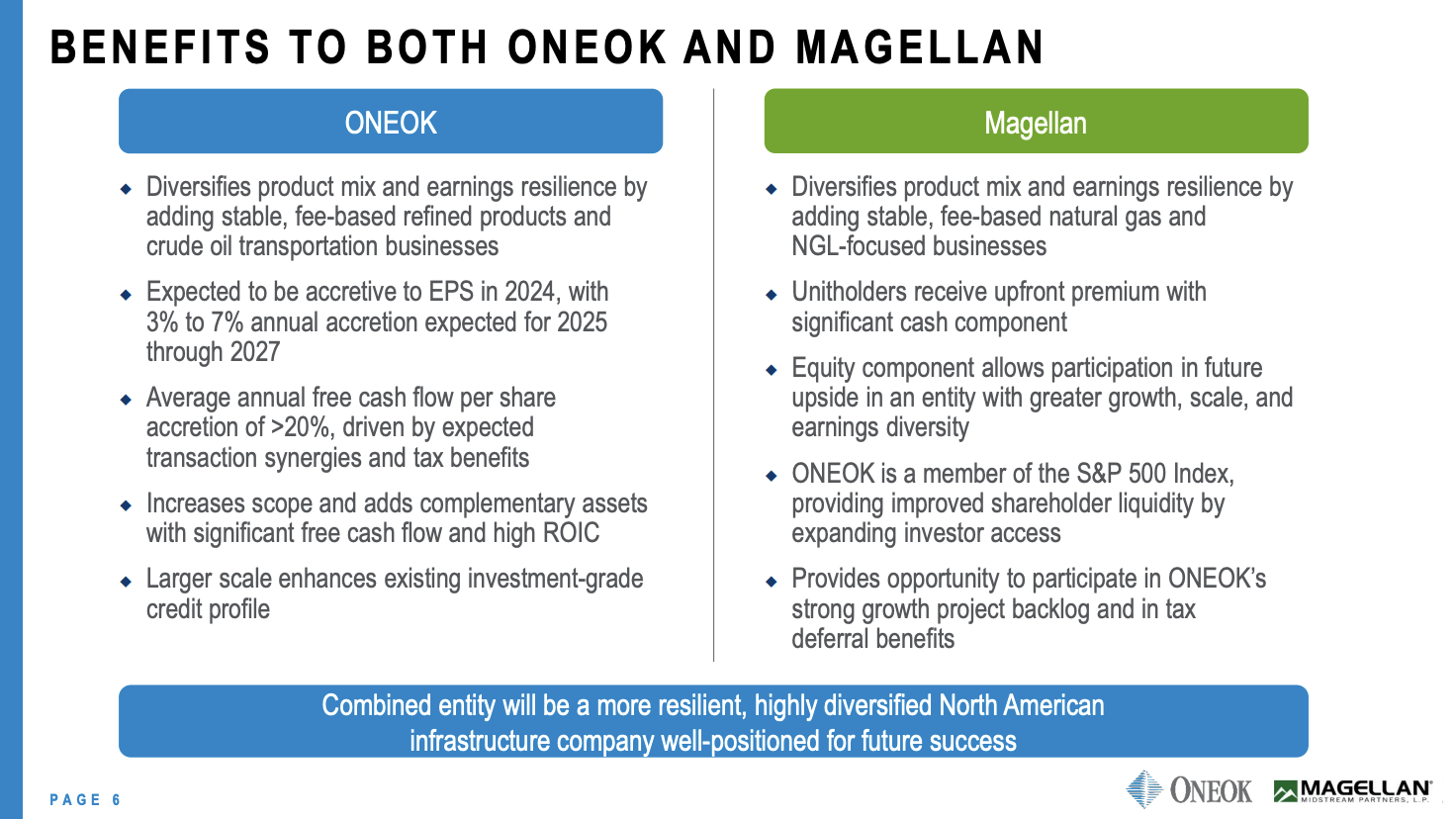

As most readers will know by now, OKE is buying Magellan Midstream Partners ( MMP ). Or at least, it is trying to, as the deal hasn't been voted on, and a major shareholder is trying to get a majority to vote against it.

So please bear in mind that my OKE thesis is not based on the MMP acquisition. Even if it were to fail, I would not change my view on OKE - I liked it way before the company announced its intentions.

{kind=link}

Having said that, during this year's Bernstein Strategic Decisions Conference, the company elaborated on its plans to buy MMP.

Essentially, the strategic rationale for the Magellan acquisition is based on four key factors:

- addressing risk,

- expanding scope,

- increasing scale, and

- seizing new opportunities.

ONEOK recognized the need to diversify its portfolio to achieve a more balanced approach, which led to the acquisition of Magellan.

{kind=link}

Instead of merely adding to its existing assets, this move introduces a new platform, extending the company's reach to serve new customers and products.

Furthermore, the larger scale resulting from the merger was acknowledged positively by rating agencies, providing the company with greater resilience and stability.

The combination of two substantial liquid systems allows ONEOK to move more volume and cater to the increasing market demand.

{kind=link}

The acquisition would also allow them to offer refined products and crude to the same customers, which increases synergies.

Speaking of synergies, the company sees between $200 and $400 million in annual synergy potential and a path to lower net debt to less than 3.5x (EBITDA) by 2026.

With this in mind, the company is also growing organically.

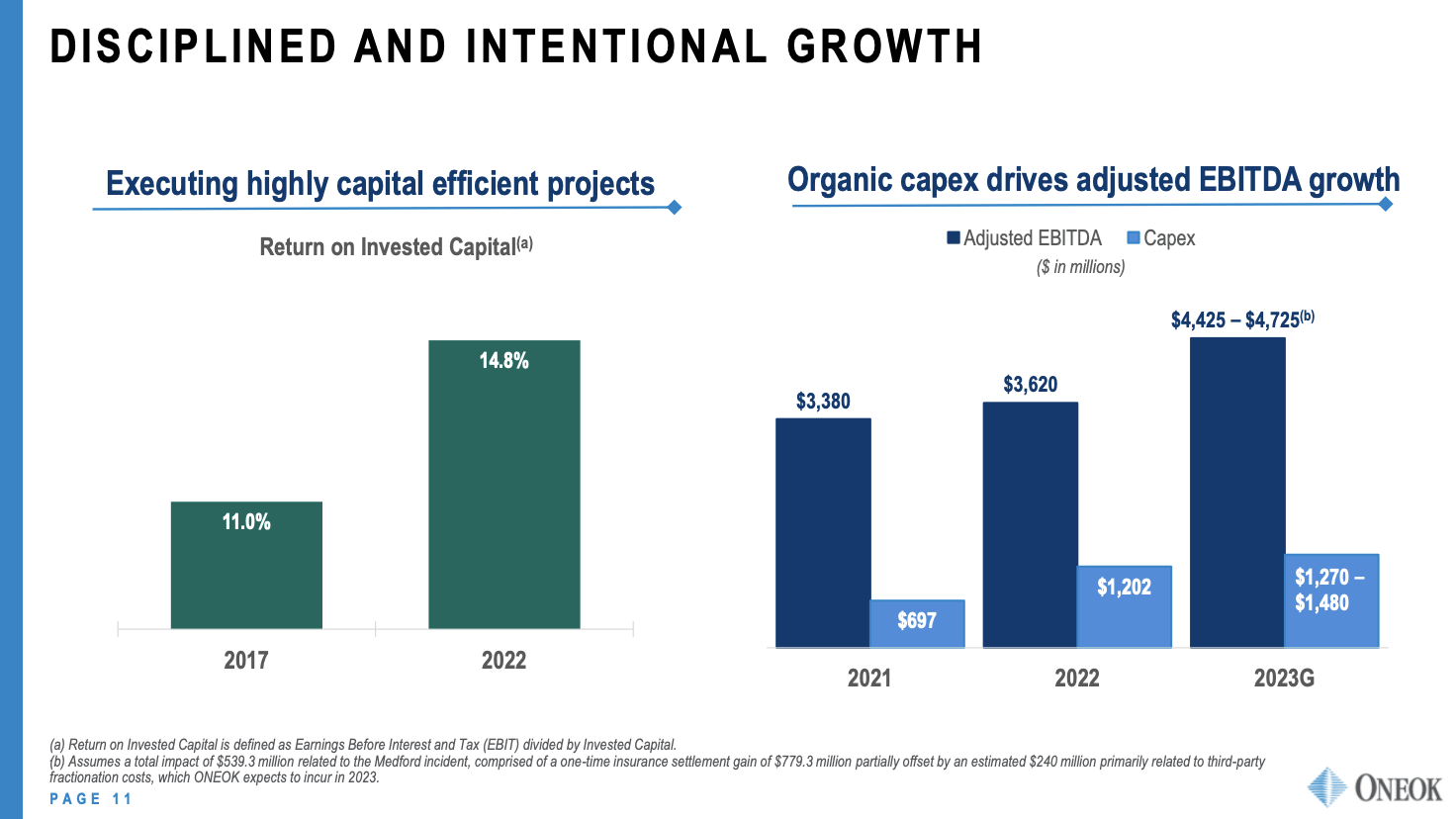

OKE, which has a history of successful organic growth, is adding to its capabilities in the Bakken region.

{kind=link}

During the aforementioned Bernstein conference, OKE discussed its capacity in the Bakken region, specifically focusing on processing and NGL takeaway.

The company mentioned having 1.9 Bcf per day of processing capacity, with around 400-500 million cubic feet per day of available capacity.

On the NGL side, they have 440,000 barrels a day of capacity, with an option to expand Elk Creek by an additional 100,000 barrels a day.

They also discuss residue gas takeaway capacity and potential expansion plans by Northern Border to take gas down to a Cheyenne-type market.

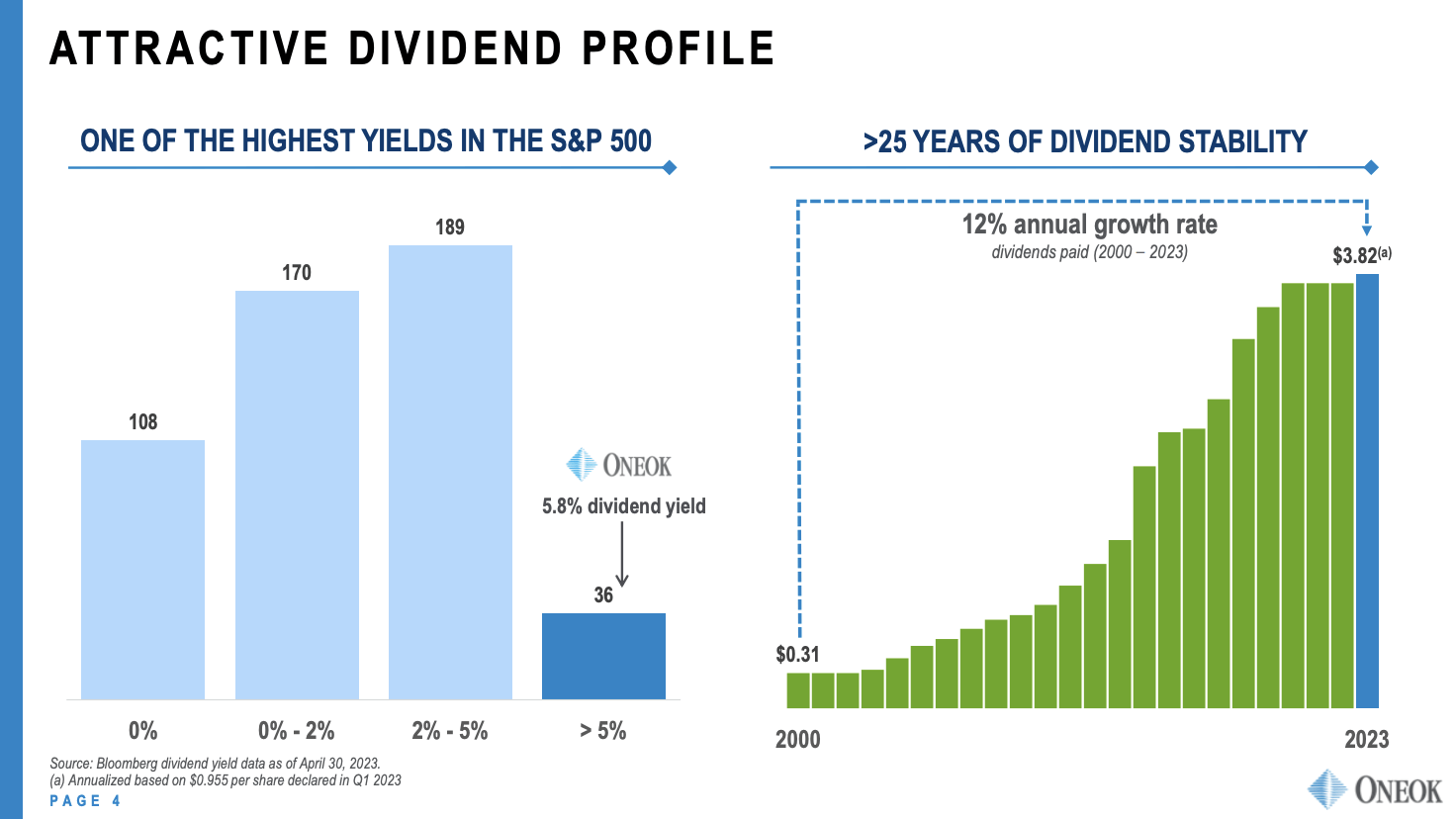

The OKE Dividend

OKE currently has a 5.8% dividend yield. Since the initiation of its dividend, the company has never cut its dividend, which sets it apart from a lot of peers who couldn't do the same.

Since 2000, the dividend has grown by 12% per year, although dividend growth has come down a lot in recent years.

{kind=link}

The most recent hike was announced on January 18, when the company hiked by 2.1%.

While it's hard to predict dividend growth, I expect dividend growth to remain subdued - especially if the company ends up buying MMP. If that is the case, I think it could take until 2026 when dividend growth picks up again.

The dividend payout ratio is 71%, which means unless we enter a devastating and prolonged recession that does a number on energy flows, the dividend is safe.

Outperformance & Valuation

Going back to 2017, OKE has returned 88%, including dividends. This beats the Alerian MLP ETF ( AMLP ) by a wide margin. As OKE isn't a limited partnership, I also added all other major C-corp midstream companies. OKE beat these companies too.

While I do not believe that OKE will outperform its peers by a wide margin in the future, I have little doubt that this Oklahoma-based company will remain among the top performers.

Valuation-wise, we're dealing with an attractive valuation. OKE shares are trading at 9.2x NTM EBITDA and a 12.4x free cash flow multiple (using $2.4 billion in 2023E free cash flow). Not only does this indicate an 8.1% free cash flow yield, which protects the dividends and allows for debt reduction, but it also shows that investors are not overpaying. Needless to say, these numbers exclude MMP.

The current price target is $70. This is 6% above the current price.

I think that target is fair and expect target prices to be hiked the moment economic growth conditions improve. After all, we're currently dealing with a steep deterioration in economic growth expectations.

Hence, it's impressive that OKE is just 7% below its 52-week-high, which shows the resilience of its business - even in this economy.

This bodes very well for the long-term outlook!

Takeaway

ONEOK is a standout choice for income-focused investors seeking resilience and consistent dividend growth in the energy sector. Despite its volatile history, OKE has transformed into one of the best high-yield options in the industry.

Its strong position in the natural gas space, backed by long-term demand and stable fee-based income, offers a steady cash flow profile.

With a dividend yield of 5.8% and a track record of never cutting dividends since its initiation, OKE sets itself apart from its peers. While recent dividend growth has slowed, the payout ratio of 71% ensures the dividend remains safe even in challenging times.

Furthermore, the (potential) strategic acquisition of Magellan Midstream Partners and organic growth initiatives position OKE for continued success and resilience.

Trading at an attractive valuation, OKE has outperformed its competitors historically and shows remarkable business resilience, which bodes well for its long-term prospects.

For further details see:

Top-Tier Income: ONEOK's Undervalued 6% Yield