FSLR - Top Value Stock 2024: Daqo New Energy

2024-01-01 07:50:17 ET

Summary

- Solar stocks have suffered in 2023, but the recent momentum driven by expected rate cuts from the Federal Reserve could move solar stocks higher in 2024.

- Daqo New Energy is facing a fierce oversupply environment, which is pressuring profits, the average selling price of polysilicon, and the stock price.

- However, new initiatives to manufacture their own silicon metal and a dive into the world of semiconductor-grade polysilicon can positively impact profit margins.

- The stock is a net-net investment with more net cash on hand than the market value of the business, and management is considering an arbitrage play to buy back more shares.

2023 has been a devastating year for solar stocks. If not for the recent Santa Claus rally, most solar stocks would've been down more than 40%. The new momentum is caused by the expected rate cuts of the Federal Reserve in 2024. Solar investments are costly and even more when you have to pay 5% interest on a loan. Therefore, solar investments have become less interesting in both America and Europe. Further, changes in government incentive programs made decision-making even worse with consumers unsure of the benefits they would receive.

On the other hand, the demand for utility-scale solar and global demand excluding the U.S. and Europe has been really strong as a result of lower solar module prices.

Daqo New Energy ( DQ ) is a stock that I have covered the most on Seeking Alpha and for good reasons. The stock is incredibly cheap. However, the polysilicon industry is facing oversupply constrains, which caused a contraction in polysilicon prices. Yet, there are catalysts that 2024 could move Daqo's stock price higher.

Industry environment

The environment is enormously fierce at the moment with only a few companies demanding market share from smaller players. The four largest players include Tongwei (600438.SS), GCL Technology ( GCPEF ), Xinte Energy (1799.HK), and Daqo New Energy. Although the polysilicon industry is facing an oversupply phase, all four of them are still increasing production capacity, resulting in a price war.

{kind=link}

Tongwei 's capacity is expected to grow from 420,000MT to 800,000MT by the end of 2024. Their latest factory is expected to deliver 200,000MT polysilicon in the first phase by the end of 2025. If all of their capacity will be operational is another question, because profits are plummeting industry-wide. In addition, Tongwei has its own solar cell business capable of manufacturing 102 GW by the end of 2023.

GCL Technologies is another gigantic polysilicon manufacturer, who uses the silane fluidized bed ((FBR)) technology. This technology is known for more efficient electricity usage compared to the Siemens TCS process. Nonetheless, the carbon concentration is higher than the value of the Siemens process players. As a result of this, the Siemens TCS process is generally preferred for producing high-quality polysilicon for solar cells. GCL is rapidly purifying the carbon concentration in their products and could soon have the same quality products. In July 2023, GCL's production cost was RMB35.68/kg or $5-5.5/kg in their Leshan factory, which is lower than Daqo's $6.5/kg.

However, Daqo New Energy has announced to expand its manufacturing capabilities in Shihezi, Xinjiang, where the rest of their Xinjiang production is located. The first phase of the project consists of 150,000MT silicon metal, 50,000MT polysilicon, and 1.2 million pieces of silicon seed rod. The second phase will have a similar expansion. The plan is to vertically integrate the silicon metal manufacturing to reduce dependence on external firms, price volatility and to decrease production costs. While coal was the main driver to low electricity prices in Xinjiang, green energy is now king and the factory will receive green electricity. After the completion of the project, the company expects to produce all the silicon metal raw materials that it needs.

One reason for the big four to keep increasing capacity is to prevent newcomers from entering the market and to pressure smaller companies in the industry to halt manufacturing. Still, this will be at the cost of profit margins and the internal rate of returns of the investments as they are blindly putting precious capital at work.

PVTime

Over the holidays and the Chinese New Year, solar panel demand weakens and workers enjoy some weeks off. As a result, polysilicon prices could drop even further in the first quarter of 2024 in combination of more polysilicon production capacity that comes online. I expect more capacity expansion projects to get halted in the first half of the year with the pressure of lower polysilicon prices.

{kind=link}

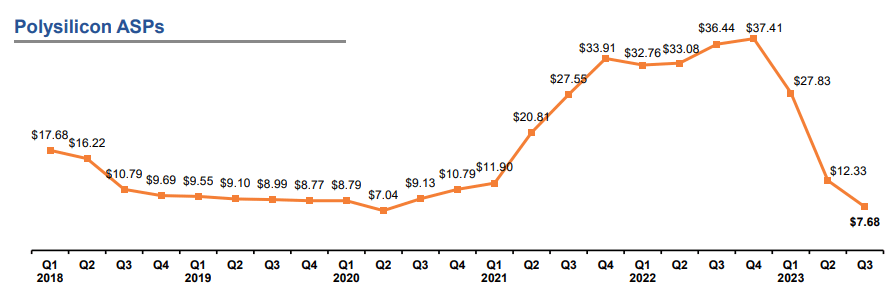

Daqo New Energy's average selling price was $7.68 in the third quarter of 2023. Consequently, EBITDA margin dropped to 14.5% and it lost $6 million in earnings due to fixed costs. The good news is that the company can decrease its production cost by almost $1/kg with the usage of its own silicon metal. The bad news is that we might see lower polysilicon prices for a while.

{kind=link}

Valuation

Diving deeper into the value aspect of Daqo New Energy, we can see an extremely undervalued stock. This will partly be caused by lower polysilicon prices, but also by the general selling of solar or renewable energy stocks in 2023. Back in 2022, we can see that investors were already anticipating lower polysilicon prices and showing no love while the business was breaking record after record. The stock is now priced at 3x price to earnings and 0.4x book value. The market is underpricing the stock since the value of its assets would be 2.5x greater than the market price of the shares, in case they sold the assets.

Financially, Daqo is in the best shape it has ever been. The company paid off all debt and has $3.28B in cash and short-term investments. Their liquidity position is $1.2B higher than their actual market value, which makes Daqo New Energy a net-net investment. Since the stock is so undervalued, the management is prioritizing share buybacks to increase shareholder value.

Catalysts

Despite the oversupply situation, there are a few catalysts that can push the stock higher in 2024.

One of those would be the allowance of Chinese polysilicon in America . Despite only banning Xinjiang polysilicon, the U.S. has not allowed any solar panels made with Chinese polysilicon into the country. Recently in December the US Customs Borders and Protection ((CBP)) did release solar modules made with non-Xinjiang Chinese polysilicon.

Although Daqo New Energy has a large part of their production in Xinjiang, this news could change the whole demand and supply market. Right now, non-Chinese polysilicon is selling at a premium price, since Chinese solar panel manufacturers like JinkoSolar ( JKS ) have to buy polysilicon from Wacker Chemie ( WKCMF ) to be able to ship their panels into America. Once Chinese polysilicon is allowed into the U.S. three dynamic changes will happen. One, the gap between Chinese polysilicon prices and non-Chinese polysilicon prices will disappear and might cause non-Chinese manufacturers to cease activity as their cost of production is a lot higher. Two, the solar panel prices in the U.S. will finally go down and the demand for solar investments will increase heavily as a result. Three, the oversupply will be considerably less, and Chinese polysilicon makers will be profitable. The impact could boost sales for Enphase ( ENPH )'s microinverters, but might set enormous pressure on First Solar ( FSLR )'s market position in America. Daqo New Energy will benefit from higher polysilicon prices, but might also be able to sell polysilicon to the U.S. through their newest plant in Baotou city, Inner Mongolia.

The second positive catalyst coming into 2024, is the manufacturing of semiconductor-grade polysilicon and the in-house manufacturing of silicon metal. Both the manufacturing of semiconductor-grade polysilicon and the silicon metal can positively impact profits. The company is moving away from a solar polysilicon-only company, by diversifying product-wise into one of the most booming industries globally.

The third catalyst would be a dividend announcement. In 2023, multiple U.S.-listed Chinese companies have declared a dividend, like JinkoSolar and Alibaba ( BABA ). Management left the chance open for a dividend in 2024 and this could be a very positive signal to investors towards the willingness to provide shareholder value.

Yet, the main priority should be on the buyback program, while the stock is trading at these undervalued prices. Therefore, the fourth catalyst is share buybacks. After telling shareholders they will buy back as much shares as they can in the fourth quarter of 2023, management is looking to pull off another arbitrage play. Daqo New Energy's subsidiary (72.4% Daqo owned) is trading on the Shanghai exchange at a substantial premium compared to the New York-listed shares of DQ. In July 2024, Daqo New Energy is allowed to sell a part of their stake in the subsidiary that could be used to buy back "cheaper" U.S. listed shares, which they have done in the past.

Daqo's CFO, Ming Yang, mentioned this in the 23Q3 earnings call :

So, it is still early to say or to estimate what the program size might be like. But starting in July of 2024, after the three-year lockout period for our Asia listing, so the U.S. Daqo New Energy is able to start to sell down some of its shares of the Asia listing. So I'll just spell out some numbers, right? So let's assume that we say sell down even a minor 10% stake, based on the current valuation of the Asia listing, which is roughly RMB70 billion, right, so we could potentially raise somewhere in the range of RMB7 billion or so in capital. And I would expect that majority of this could be used for share purchase in the U.S. NYSE listing.

To put in perspective, RMB7 billion equals $1 billion, which accounts for 50% of the current market cap. Of course, this sale will be relevant to the market value of Xinjiang Daqo in July 2024, so it's hard to say what the real sale value would be. Anyway, a 50% share buyback is enormous value and it would be hard to temper the stock price from going higher.

Risks

Investors need to keep in mind that Daqo New Energy has been identified by the SEC under the Holding Foreign Companies Accountable Act . This means the company will be delisted in 2024, if they do not show the right auditing under the rules of the United States.

If a delisting must happen management would consider to bring Daqo New Energy to the Hong Kong exchange as a dual listing. This would mean you can convert your U.S. shares to Hong Kong-listed shares.

In case of long-term oversupply and low polysilicon prices, Daqo New Energy might need to cease part of their production lines and this will impact their profitability. At the moment, the company is perfectly healthy and Daqo New Energy would likely be one of the last men standing as none in the industry has a balance sheet like Daqo.

Takeaway

The polysilicon industry is in a cyclical downturn, where manufacturers are heavily investing, even overinvesting, for the sole reason of consolidation in the industry and taking market share. It is still a wait-and-see situation who can push his foot the longest on the pedal forward. Shareholders won't remain silent on the blind investments in the industry at the cost of profits.

Even while the environment is not great, the market always reacts 6 months beforehand. Daqo New Energy stock is valued below cash and asset value. In addition, the management is looking to make share buybacks a high priority for 2024. A share buyback program with a value of 30-50% of the market cap will move the stock higher. Furthermore, if interest rates get cut there is a high chance Daqo New Energy will move higher along with the other solar stocks. Obviously, any sign of recovery in polysilicon prices will also affect the stock price.

I believe Daqo New Energy is one of the most undervalued companies in the market right now. The worst is priced in for the company, whilst positive catalysts are nearing. Therefore, I maintain my rating of 'Strong Buy'.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which ran through December 31. If you are interested in becoming a contributor, submit your article today!

For further details see:

Top Value Stock 2024: Daqo New Energy