TRMLF - Topaz Energy: Growth Defence And A 6% Dividend Yield

Summary

- Topaz is a triple-track growth story with great infrastructure assets and prime fee lands in both the Montney and Clearwater plays.

- Topaz offers a 6% dividend yield, following five dividend increases since 2019.

- Compared to other royalty companies, Topaz has more resilient cash flow owing to its long-term contracted infrastructure revenue.

- This resilient and diversified cash flow supports predictable dividend growth for the long term.

- With leverage to both oil and gas, Topaz offers a defensive way to gain exposure to strong energy demand.

Author's note: All figures in Canadian currency unless otherwise noted.

Investment Thesis

Topaz Energy Corp ( TPZ:CA ) is a royalty and infrastructure company focused on shareholder returns. It's unique combination of gas-weighted fee lands and midstream infrastructure offer both resilient recurring revenue and commodity-driven growth.

The company has strong tail winds at both of its major land holdings, Clearwater and the Montney plays, where leasing and production continue to grow. Further catalysts include the continued diversification away from Tourmaline Oil Corp. ( TRMLF ) ( TOU:CA ) properties and the expansion of the company's infrastructure portfolio.

The company has raised its dividend five times since 2019 and offers a 6% yield that is poised to grow. I expect that Topaz will command a higher multiple over its peer as its infrastructure earnings offer long-term dividend stability.

Company Profile

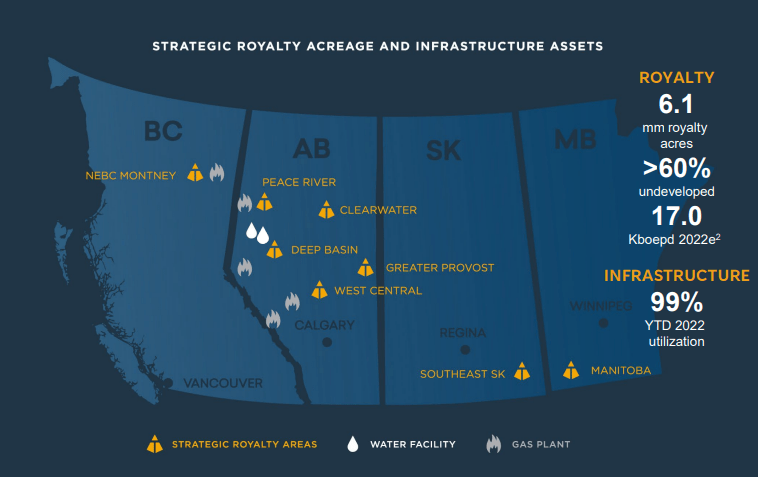

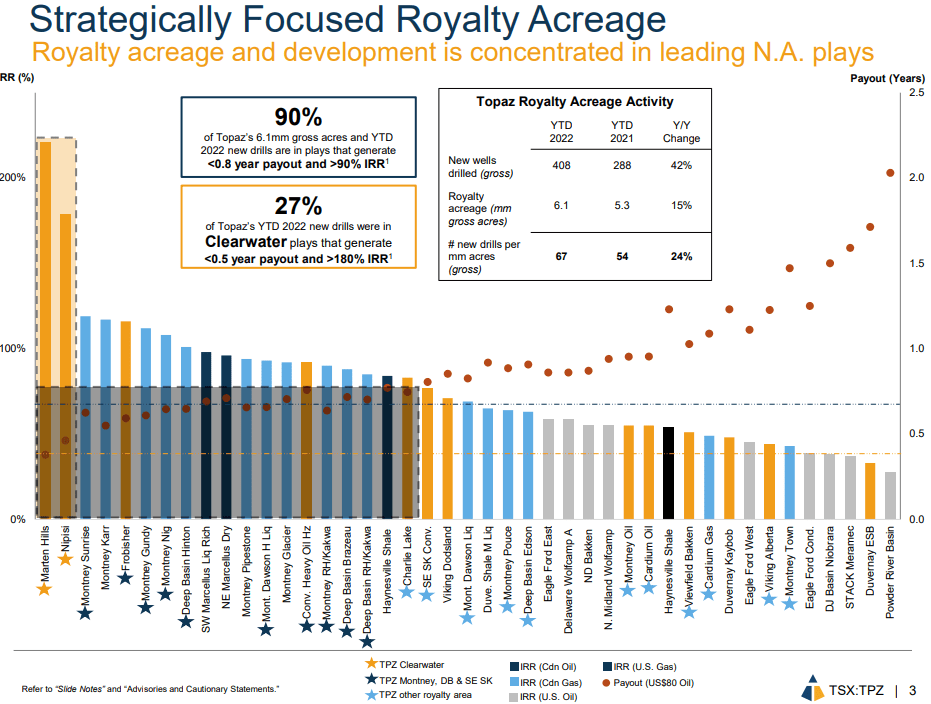

Topaz was formed as a public company in 2019 through the transfer of royalty and midstream infrastructure assets from sponsor, Tourmaline. With a market capitalization of approximately $3B, Topaz is the newest and second largest of the three large publicly traded royalty companies in the western Canadian sedimentary basin. Topaz owns 6.1 million gross royalty acres across premium oil and gas plays in British Columbia, Alberta, Saskatchewan and Manitoba.

The company's royalty revenue stream is approximately 75% gas-weighted with a significant presence in the Montney formation, Western Canada's most important natural gas play. On the oil side, with 700,000 royalty acres, Topaz has the second largest leverage to the Clearwater oil play of the large royalty companies. Clearwater is one of North America's fastest growing production regions with shallow drilling opportunities that provide high IRR and quick payback periods.

Topaz's ownership of infrastructure includes ownership in five natural gas plants and a 50% stake in two water facilities. These assets contributed 36% of estimated 2022 cash flow and offer revenue stability through long-term contracts.

{kind=link}

While the company continues to diversify away from Tourmaline as its major counterparty, Tourmaline's development of the Montney region will continue to be a catalyst for growth. Tourmaline is Canada's largest producer of natural gas. Its shares are up 72% since I recommended the company in Dec 2021. Topaz continues to have close ties with Tourmaline, with Tourmaline owning 31.3% of Topaz's outstanding common shares as of September 30, 2022. As a continued vote of confidence for the company he spun out from Tourmaline, Tourmaline CEO Mike Rose, recently purchased 10,000 shares of Topaz.

Royalty Structure

Along with Topaz, the three large publicly traded royalty companies in Canada are PrairieSky Royalty Ltd. ( PREKF ) (PSK:CA) and Freehold Royalties Ltd. ( FRU:CA ). In my recent coverage of PrairieSky: This Royalty Company Just Doubled Its Dividend , I provide an overview of Fee Simple, GORR royalty structures.

Royalty companies differ from exploration and production oil and gas firms in that they do none of their own drilling or production. This exempts royalty firms from capital outlays related to production and the risks associated with exploration and marketing. Royalty companies lease land and earn revenue through production. The mineral rights ownership of these properties has the potential to produce revenue in perpetuity as the land can continue to be leased multiple times.

Dividend Growth

In November 2022, Topaz increased its dividend for the fifth time since the IPO in 2019. The increase to quarterly dividend to $0.30 per share represents a 7% increase from the third quarter dividend of $0.28. For shareholders who have held Topaz since the IPO, the annualized dividend of $1.20 per share represents a 9.2% yield on cost. At current levels, Topaz offers a forward yield of 6%, which compares to PrairieSky and Freehold Royalty with yields of 4.2% and 6.3% respectively.

Topaz Energy Dividend Growth (Author)

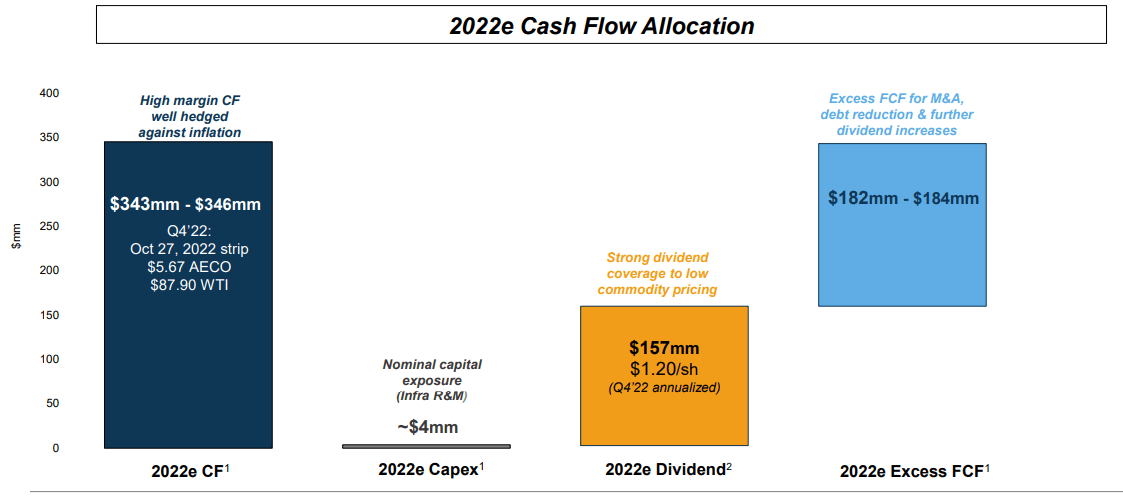

Topaz has indicated that the majority of its free cash flow will be used to pay dividends with a long-term payout ratio target of 60% to 90%. The current payout ratio of 48% leaves significant room for further increases. The rapid cadence of dividend increases reflects growing optimism in free cash flow. At October 2022 strip prices, Topaz was generating more than $180M of free cash flow in excess of the dividend and its nominal capital requirements. This is cash flow that can be used to continue dividend growth, pay down debt or fund an infrastructure acquisition.

{kind=link}

Topaz is unique among its royalty peers in its dividend stability. In 2020, both PrairieSky and Freehold cut their dividends and have been playing catch up since. Topaz has a shorter dividend history, with its first dividend payment in March 2020. While it is unclear if Topaz would have been in a similar position to its peers had the company's IPO been a year or two earlier. It is probable that Topaz's stable infrastructure revenue helped it avoid having to trim the dividend during this economic downturn. I would suggest that Topaz's revenue mix being less exposed to commodity cycles than its peers, will allow it to provide a more steady dividend growth trajectory. I tend to prefer dividend track records that reflect steadily growing cash flows and avoid cuts or sudden jumps.

Montney Play

The Montney formation, centered in northeastern British Columbia, accounts for 45% of all the natural gas produced in Western Canada. Topaz holds approximately 1.1 million gross acres of acreage in the Montney play covering all of Tourmaline's approximately 7,000 horizontal future drilling locations in the play. Tourmaline has dedicated an average of $1.9B in capital annually from 2023 to 2028 to support production growth in the Montney area.

The growing global demand for natural gas is fueling increased drilling activity and production on Topaz's key Montney fee lands. This play is increasingly connected to egress and export facilities through the development of projects like TC Energy's ( TRP ) Costal Gas Link project and LNG Canada's terminal development at Kitimat, BC,

A settlement between the provincial government and the Blueberry River First Nation announced in January 2023 paves the way for new leasing in the Montney play. This is welcome news after a nearly two-year moratorium on new drilling in this area. This agreement will result in Tourmaline boosting its production volumes with no incremental cost to Topaz.

Clearwater Play

The Clearwater play located in Northern Alberta has some of the best economics in North America for oil exploration and production. Shallow reservoirs harnessed with the technology to drill tightly spaced multilateral wellbores quickly and accurately has propelled Clearwater to be one of the highest IRR and quickest payback period plays for conventional oil.

{kind=link}

Topaz owns approximately 700,000 royalty acres in Clearwater centered around the Marten Hills, Nipisi and Canal regions. Topaz's position in Marten Hills & Nipisi are estimated to contain 52% of the estimated 14.4B bbls of oil in place across the play. As of Q3, 2022, 27% of Topaz's new drilling activity YTD was in the Clearwater play. In September 2022, Topaz announced the acquisition of a new 5% royalty on 138,000 gross acres in top tier properties in Clearwater for $265.3M. Following this acquisition from Deltastream Energy, Topaz should see a near doubling in volumes.

Infrastructure Assets

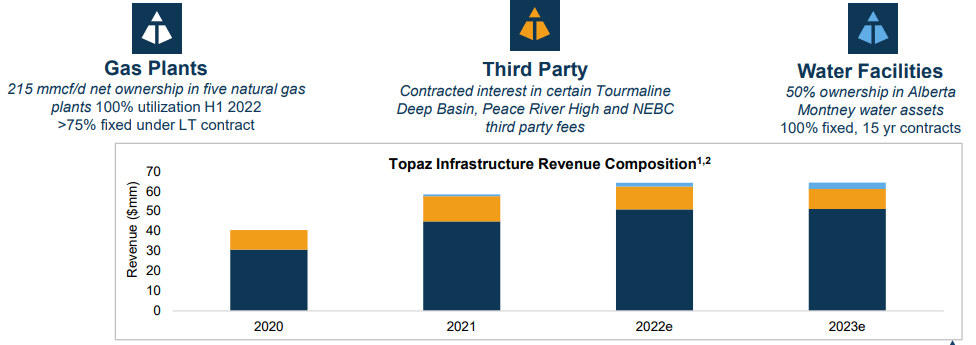

Topaz holds non-operating working interests in five natural gas processing facilities running at 99% utilization. These arrangements for 75 mmcf/d of natural gas processing capacity are largely underpinned by 10-15 year take-or-pay contracts. Topaz also owns a contracted interest in a portion of Tourmaline's third-party revenues in the Alberta Deep Basin and Peace Hiver areas. The company has 49.5% interest in a pipeline-connected water handling facility where it has an opportunity to acquire an additional $25M in 2023 at the same rate of return without incurring capital or operating costs. The operating margins on these infrastructure assets are very attractive with Topaz anticipating generating $56M in free cash flow on approximately $64.5M in revenue with $6M in operating costs and $3-4M in maintenance capital.

{kind=link}

Topaz targets a long-term 50/50 EBITDA split between its infrastructure and its royalty segments. According to Luke Davis, Equity Analyst with RBC Capital Markets, Topaz is likely to evaluate and potentially pursue M&A activity to further develop its infrastructure footprint. The most likely path towards this goal is further drop down activity from Tourmaline. Tourmaline is the fifth largest operator of midstream assets in Canada. Topaz could have the opportunity to acquire interests in additional Tourmaline assets or increase its working interest in the facilities it already has interest in.

According to a recent analyst note from Desjardins' Chris MacCulloch:

From our perspective, a properly priced infrastructure deal providing additional scale and ratable cash flow would be a strategically positive development for TPZ. All the more so if it generates greater awareness in the story among infrastructure-focused inventors seeking protection from inflationary pressures by way of the company's commodity price exposure.

Risk Analysis

Like all royalty companies, Topaz is exposed to indirect commodity price risk. Commodity price weakness could lead to a slowdown in leasing and production, which could have a material impact on royalty revenue. While sheltered from the everyday costs of exploration and the capital costs associated with production, Topaz will still catch a cough if the energy industry gets a cold.

Topaz went public in 2019 at the beginning of this current commodity cycle, unlike PrairieSky, which had the unfortunate timing of launching an initial public offering with high expectations just months before the composite price collapse of 2014. Topaz's more favourable timing along with committed sponsorship from Tourmaline set Topaz up for more realistic expectations and valuation.

Topaz owns non-operated facility interests which are underpinned by long-term fixed fee take-or-pay commitments. This is a low risk operation model that requires fees to be paid regardless of actual throughput volume. Topaz's gas and water plants generate approximately $65M annually, enough stable cash flow to cover 36% of the company's 2022 dividend. While Topaz's infrastructure assets reduce cash flow volatility through utility-like earnings, infrastructure, unlike fee lands they require maintenance capital overtime. Unlike a pure play royalty company, Topaz will need to invest maintenance capital into its infrastructure assets.

The company has a healthy balance sheet with net debt of approximately $397M for the end of 2022. Starting 2023 with a net debt/EBITDA ratio of 1.1X, the company expects to finish 2023 with a net debt/EBITDA ratio 0.6X. The business model's high margins provide optionality with free cash flow to pursue acquisitions or pay down debt.

Valuation

Topaz has a reasonable valuation at is 8.4X 23EP/CF and is 8.7X 23E EV/DACF. This compares favourably to PrairieSky Royalty with a 2023E P/CF of 11.1X and a 2023E EV/DACF of 11.0X and Freehold at 8.0X and 7.9X respectively.

| Company |

| 23E P/CF |

| 23E EV/DACF |

| Topaz |

| 8.4X |

| 8.7X |

| PrairieSky |

| 11.1X |

| 11.0X |

| Freehold |

| 8.0X |

| 7.9X |

Source: RBC Capital Markets

Of the 15 analysts with one-year price targets, the average target is $28.97 suggesting a 47% upside to current levels. With a valuation multiple similar to PrairieSky around 11X, Topaz would trade in the ~$30 range. I expect that is a reasonable multiple valuation given the firm's cash flow stability and high margins.

Note for U.S. Shareholders

Topaz expects that it may be classified as a passive foreign investment company ("PFIC"). Canadian Dividends can be sheltered from the 15% tax withholding when held in U.S. retirement accounts. Please consult a tax professional if needed.

Investor Takeaways

Topaz's great royalty properties in the Clearwater and Montney region give the company significant leverage to the advantages and production growth catalysts in these plays. Topaz is poised to generate significant free cash flow from these assets at current commodity prices. The company's ownership of infrastructure assets provides cashflow stability and predictably which supports steady dividend growth. Topaz is a defensive way to participate in this commodity cycle while providing growing dividend income.

For further details see:

Topaz Energy: Growth, Defence And A 6% Dividend Yield