ESCA - Topgolf Callaway Brands: Still A Great Play But Not As Great

Summary

- Topgolf Callaway Brands continues to grow nicely on both its top and bottom lines.

- That trend is set to continue and the market has responded positively to this.

- Shares still look attractively-undervalued, but they aren't as appealing as they were during my previous coverage though, in part due to recent upside.

Although golf may be fun to many individuals, myself included, it may not seem like the most obvious investment space to consider when the economy is on rocky ground. Having said that, one company in this space that is doing incredibly well at the moment is Topgolf Callaway Brands ( MODG ). From both a revenue and cash flow perspective, the company continues to grow, and that trend is expected to continue through at least the 2023 fiscal year. On an absolute basis, shares of the company do look attractively priced, though they may be a bit pricey relative to similar firms. All things considered, I would make the case that the company should be a solid 'buy' prospect at this time.

A revision in sentiment

Back in the middle of July of 2022, I wrote an article that took a very bullish stance on Topgolf Callaway Brands. Strong growth on both its top and bottom lines, combined with an attractive share price and a plan to continue growing the business over the next few years, led me to feel very optimistic about the firm's prospects. At the end of the day, this led me to rate the business a 'strong buy', which is a rating that reflects my view that shares should drastically outperform the broader market for the foreseeable future. Since then, the company has managed to outperform the S&P 500. But I wouldn't exactly call the performance disparity drastic. While the S&P 500 is up 2.8%, shares of Topgolf Callaway Brands have generated upside for investors of 8.3%.

{kind=link}

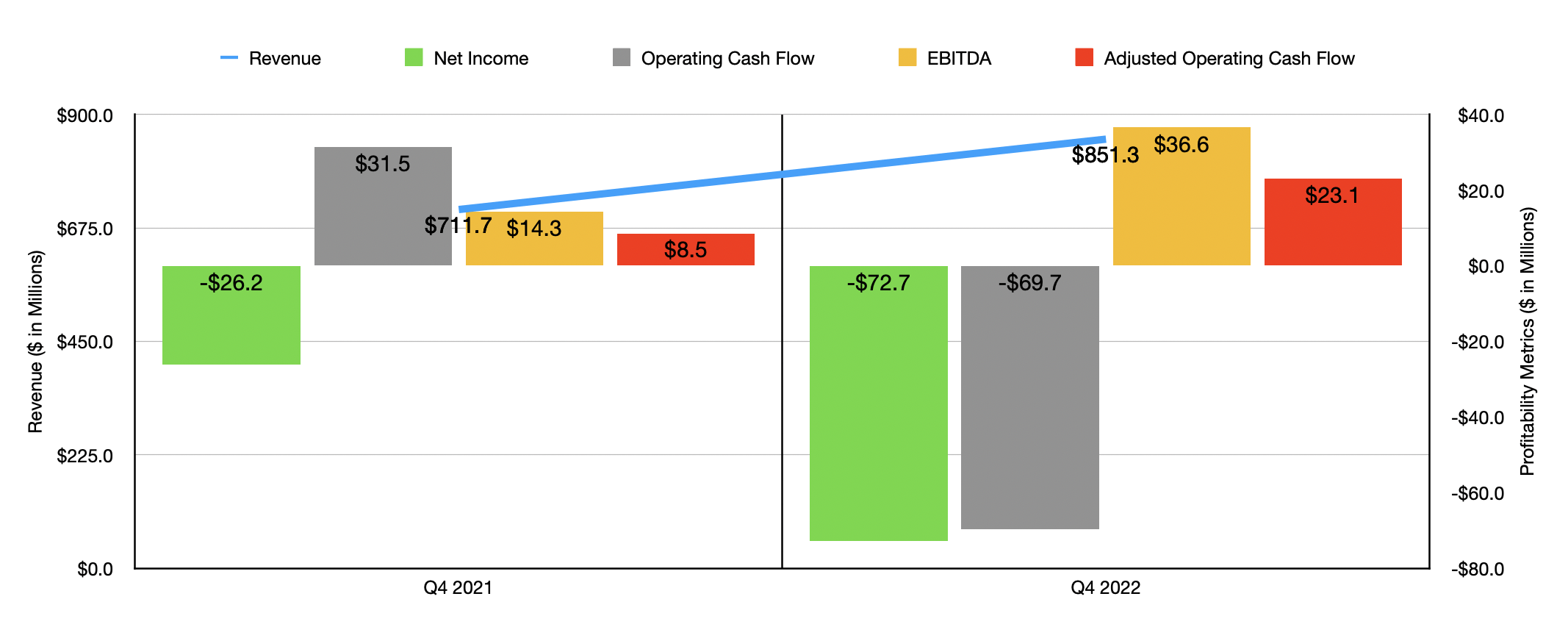

Relatively speaking, this is solid performance. And it has not been as a result of some fluke. Instead, it has been driven by robust financial data reported by management. Consider the final quarter of the company's 2022 fiscal year. During that time, revenue came in at $851.3 million. That's 19.6% higher than the $711.7 million the company generated one year earlier. This significant upside was achieved even in spite of a $37.8 million negative impact associated with foreign currency fluctuations. Management attributed the upside to growth all across the major categories that the company operates in. But undoubtedly the most impressive side of the business was its Topgolf brand. Sales here spiked 21.9%, climbing from $335.8 million to $409.5 million. Golf equipment sales grew a more modest 17.7%, while revenue under the active lifestyle category increased 17.4%. It's worth noting that, under the Topgolf brand, the company benefited from a same-venue sales growth of 11% compared to the pre-pandemic levels experienced in 2019. The company also benefited from the opening of six new owned and operated venues under this umbrella.

On the bottom line, the picture for the company was a bit mixed. The firm actually went from generating a net loss of $26.2 million in the final quarter of 2021 to generating a net loss of $72.7 million in the final quarter of 2022. A big portion of this swing, however, was driven by a much larger tax benefit than the company reported in the final quarter of last year relative to the same time this year. On a pre-tax basis, the net loss for the company would have improved from $95.7 million to $76.2 million. Other profitability metrics were also somewhat mixed. Operating cash flow, for instance, came in negative to the tune of $69.7 million for the final quarter of 2022. This was down from the $31.5 million positive reading reported one year earlier. If we adjust for changes in working capital, however, it would have improved from $8.5 million to $23.1 million. Meanwhile, EBITDA for the business expanded from $14.3 million to $36.6 million.

{kind=link}

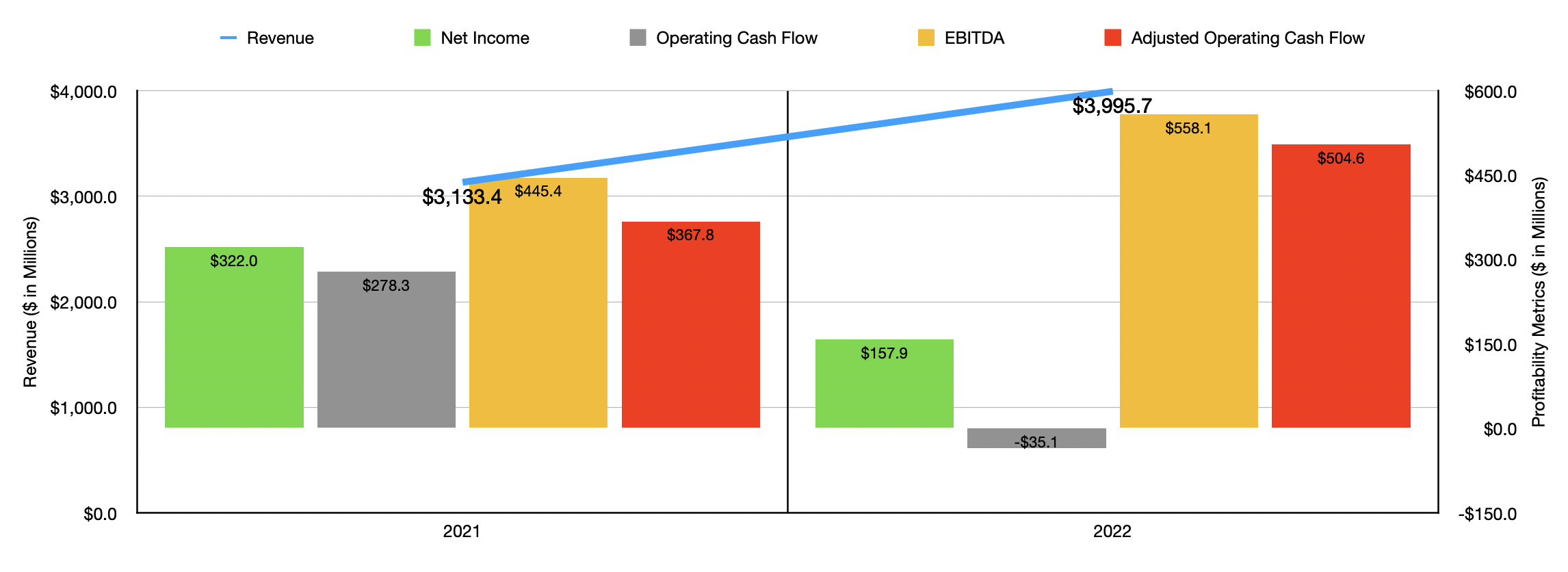

If some of these bottom line results look unappealing, keep in mind that golf is a seasonal activity. For 2022 as a whole, the company looked fantastic. Revenue of nearly $4 billion dwarfed the $3.13 billion reported one year earlier. Once again, the Topgolf brand led the way, with sales spiking 42.4% year over year. It is true that net income during this time dropped from $322 million to $157.9 million. In addition to there being wild swings in taxes, the company also benefited from a $252.5 million gain on its Topgolf investment back in 2021. Operating cash flow fell year over year as well, dropping from $278.3 million to negative $35.1 million. But if we adjust for changes in working capital, it would have risen from $367.8 million to $504.6 million, while EBITDA for the business grew from $445.4 million to $558.1 million.

For the 2023 fiscal year, management has provided some solid guidance. Revenue, for instance, should be between $4.415 billion and $4.470 billion. That should translate to a year-over-year growth rate of between 10% and 12%. Meanwhile, EBITDA is expected to come in at between $620 million and $640 million. That's up between 11% and 15% compared to what the company reported one year earlier. No guidance was given when it came to other profitability metrics. But if we assume that they will increase at the same rate that EBITDA it's forecasted to, then we should anticipate net income of $178.2 million and adjusted operating cash flow of $569.6 million.

{kind=link}

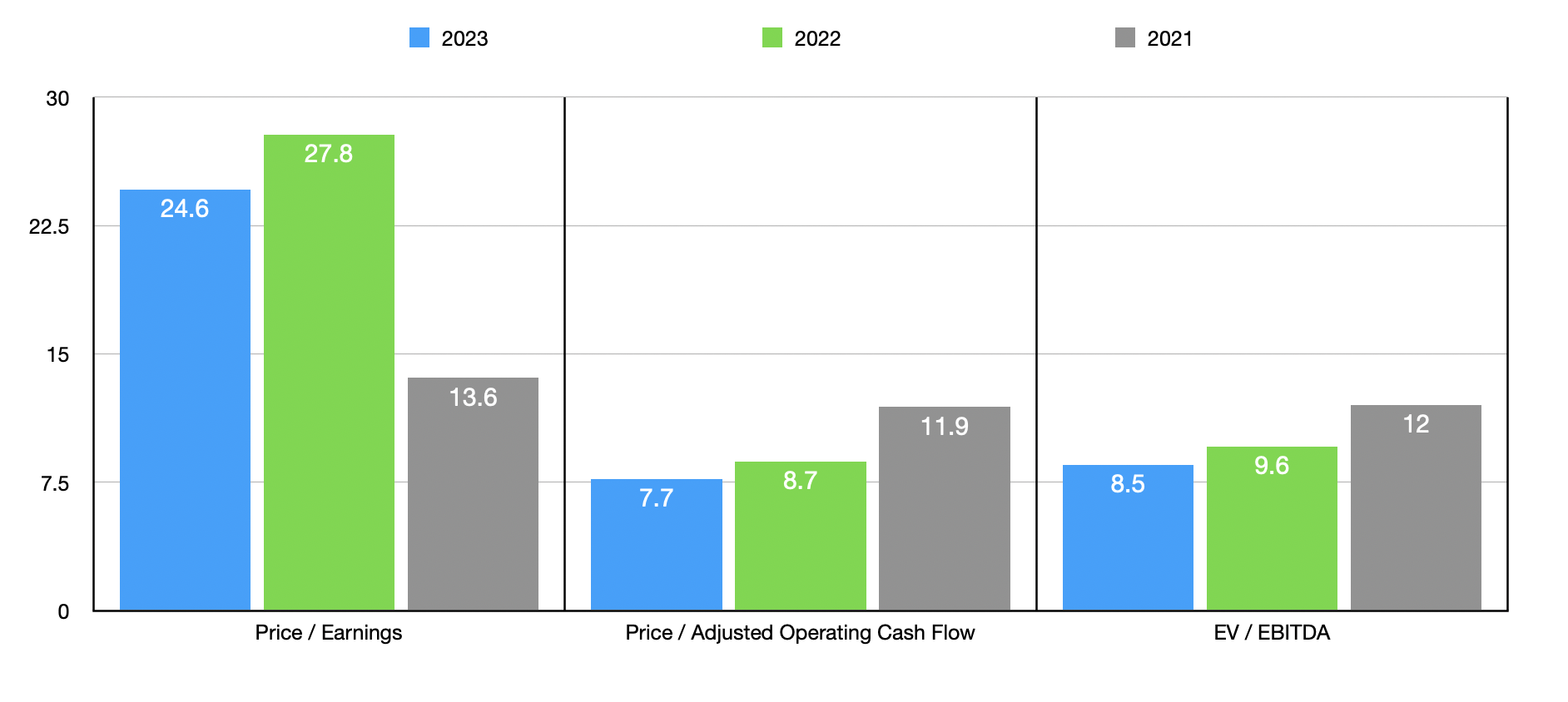

Based on these figures, the company is trading at a forward price-to-earnings multiple of 24.6. That compares to the 27.8 reading that we get using data from 2022. While these numbers look a bit lofty, the cash flow numbers look much better. The price to adjusted operating cash flow multiple should come in at around 7.7. That's actually down from the 8.7 reading that we get using data from 2022. When it comes to the EV to EBITDA approach, we should expect a multiple of 8.5. By comparison, using data from 2022, we would get a multiple of 9.6. As part of my analysis, I compared the company to five similar firms. I did this using the data from 2022 for all parties involved. On a price-to-earnings basis, these companies ranged from a low of 4.2 to a high of 20.7. In this case, Topgolf Callaway Brands was the most expensive of the group. Using the EV to EBITDA approach, the range would be from 4.3 to 13.7. In this case, three of the five companies were cheaper than our target. And finally, when it comes to the price to operating cash flow approach, the range is between 4.1 and 2,976.4. I would make the case that at least three of the five under this valuation approach are outliers. But regardless, only one of the five firms was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Topgolf Callaway Brands |

| 27.8 |

| 8.7 |

| 9.6 |

| Acushnet Holdings Corp. ( GOLF ) |

| 20.7 |

| 46.9 |

| 13.7 |

| YETI Holdings ( YETI ) |

| 17.4 |

| 2,976.4 |

| 11.9 |

| Escalade ( ESCA ) |

| 8.7 |

| 123.6 |

| 8.2 |

| Johnson Outdoors ( JOUT ) |

| 16.7 |

| 119.2 |

| 8.3 |

| Vista Outdoor ( VSTO ) |

| 4.2 |

| 4.1 |

| 4.3 |

Takeaway

Fundamentally speaking, I do believe that Topgolf Callaway Brands remains a solid company and I think that the future of the business will be quite bright. As I highlighted in my prior article on the firm, attractive growth should continue over the next few years. From a cash flow perspective, shares are quite cheap on an absolute basis, especially when factoring in the growth is experiencing. Though shares are a bit lofty relative to similar firms. Given the fact that shares have already risen nicely and that there is some additional economic uncertainty, plus when factoring in the relative valuation of the firm, I do think a slight downgrade to a 'buy' from the 'strong buy' I had it at previously is warranted.

For further details see:

Topgolf Callaway Brands: Still A Great Play, But Not As Great