TORXF - Torex Gold: Another Major Beat But Tough Comps Ahead

Summary

- Torex Gold released its Q4/FY2022 results last week, and true to form, delivered into guidance and is on track to meet cost guidance despite a difficult year for the sector.

- Meanwhile, it continues to make solid progress on Media Luna development and mine plan optimization, reporting development rates in the Guajes Tunnel and is set to add high-grade resources at ELG-UG.

- That said, the stock looks fully valued short term at a market cap of $1.18 billion, and I see this rally above US$13.50 as an opportunity to book profits into strength.

While it was a rough year for investors in gold miners ( GDX ) in 2022, one name that most investors probably didn't have on their bingo card for 2022 outperformance had a massive year. This was mid-tier producer Torex Gold ( TORXF ), which spent most of 2022 in a steep downtrend but launched higher starting in November to end the year well in positive territory (11% return vs. negative return for the GDX). The solid performance can be attributed to Torex executing phenomenally from an operational standpoint, leading to a beat on 2022 guidance. Notably, this beat was achieved from both an output and cost standpoint judging by where full-year costs should land, making this beat even more impressive amid a year of double-digit inflation sector-wide.

Meanwhile, although Torex had a strong 2022 operationally, it also saw immense success from an exploration standpoint, hitting some solid intercepts in Sub Sill South and El Limon Sur Deeps. Also of note were high-grade intercepts from its EPO South Target, with highlight intercepts including 17.25 meters at 7.29 grams per tonne of gold and 16.48 meters at 9.63 grams per tonne of gold at the EPO South Extension. The recent drilling suggests that the market isn't giving Torex enough credit regarding exploration upside, and there is the potential to optimize its mine plan with opportunities to top up the mill post-2027. Let's take a closer look at the Q4 results and the recently announced multi-year outlook below:

Q4 & FY2022 Production

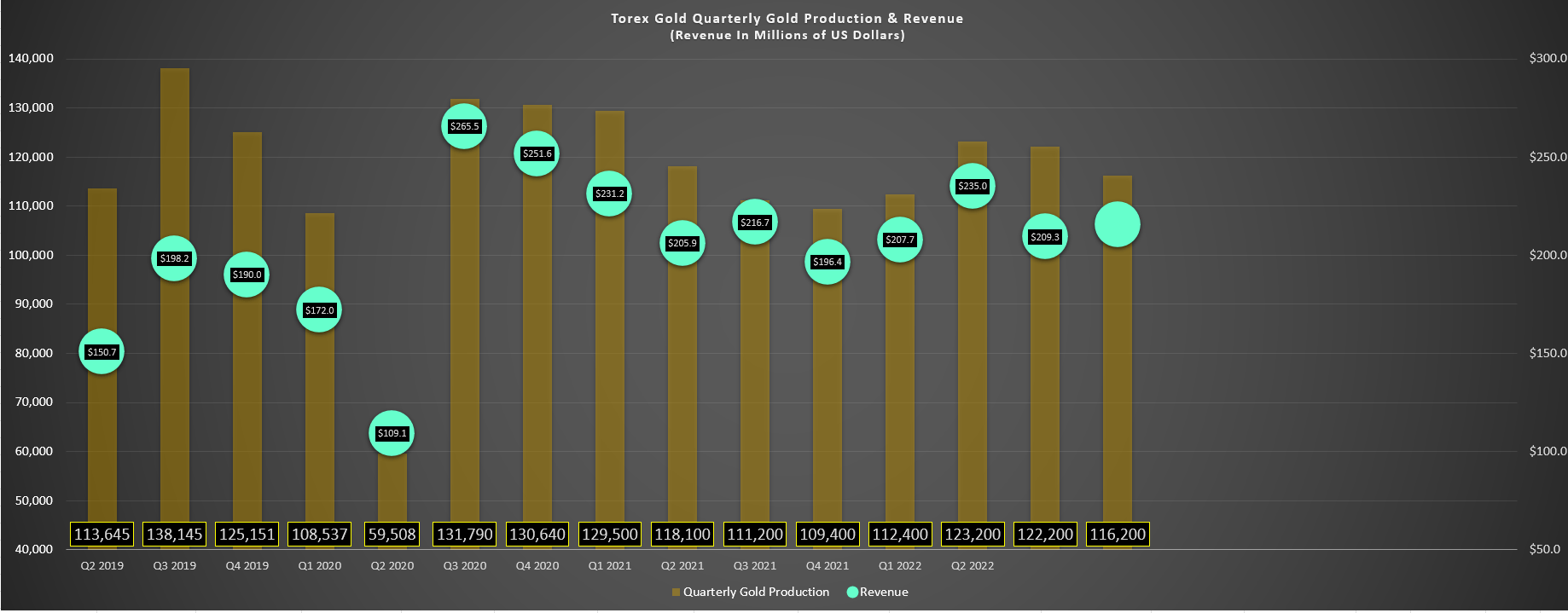

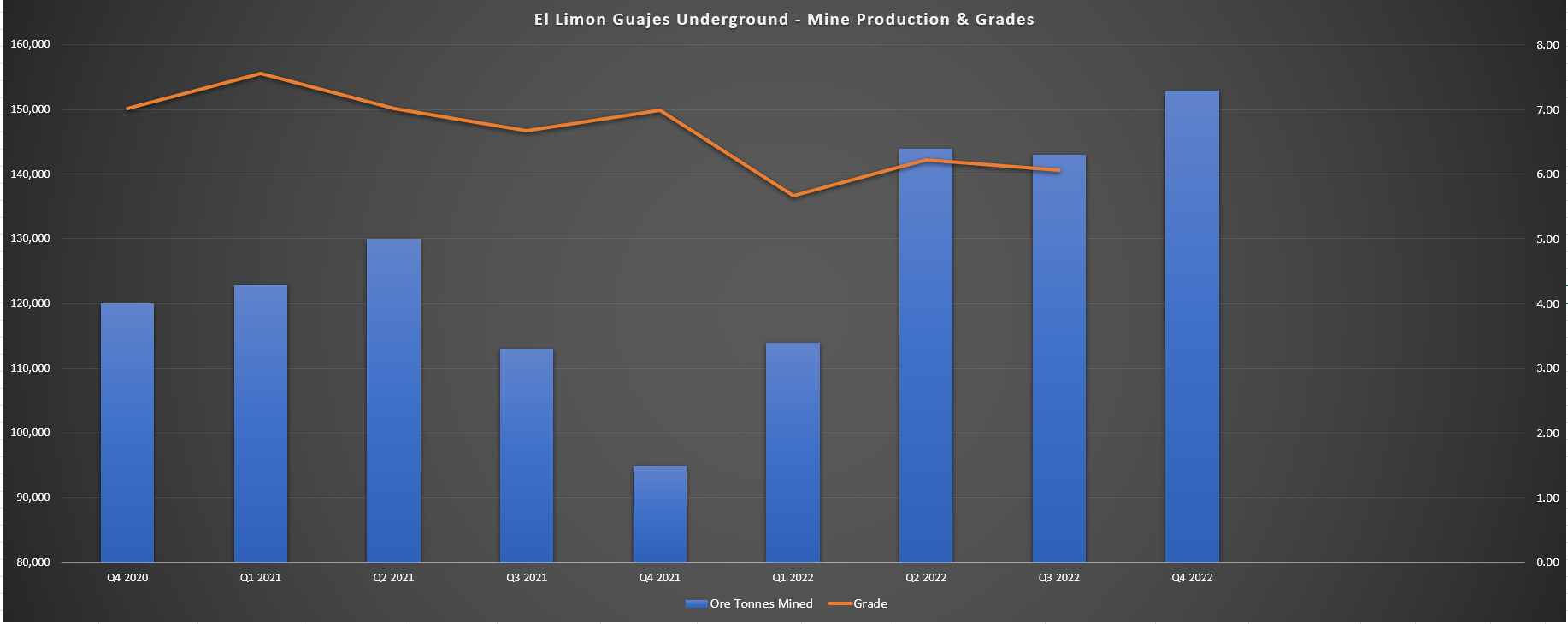

Torex Gold released its Q4 results earlier this month, reporting quarterly production of ~116,100 ounces of gold, a 6% increase from the year-ago period. This solid finish for the year helped Torex to deliver above the top end of its FY2022 guidance (430,000 to 470,000) ounces and log a more than 6% beat vs. its guidance mid-point, reporting FY2022 production of ~474,000 ounces. The strong performance was helped by record quarterly underground mining rates at El Limon Guajes [ELG] Underground, with an average of 1,685 tonnes per day mined, which should translate to 150,000+ tonnes for the quarter, also a new record.

Torex -- Quarterly Gold Production & Revenue (Company Filings, Author's Chart)

{kind=link}

Looking at the chart below, we can see that Torex has seen impressive progress at ELG underground, with tonnes mined increasing more than 20% on a two-year basis (Q4 2022 vs. Q4 2020), and further optimization is expected. Torex noted that it expects to exit 2023 with underground mining rates of 1,800 tonnes per day, and we could see mining rates improve further to ~2,000 tonnes per day in 2024. Combined with the additional pushback to smooth out the transition from ELG to Media Luna, these higher mining rates will help Torex to maintain a significant production profile during its peak year of investment (2023) and as mining at most of the ELG pits winds down in 2024.

ELG Underground - Mine Production & Grades (Company Filings, Author's Chart)

{kind=link}

Finally, Torex has proactively hedged approximately 25% of FY2024 production (108,000 ounces) at an average gold price of $1,939/oz, which adds to the 108,000 ounces of gold hedges at $1,924/oz this year. Although this may not appeal to some investors that want full leverage to the gold price, I think this is a very smart move during this period of elevated capital spend, and similar to the strategy that Northern Star ( NESRF ) is employing in Australia while it sees elevated capital spending as it works to optimize KCGM and completes expansion work at Jundee (TBO Mill Expansion). So, while other miners may have more upside in a $2,000/oz gold environment, I see this hedging as prudent, and it only limits exposure to 25% of ounces, a smart and defensive move in case the gold price were to slip back into an intermediate downtrend.

Recent Developments & Multi-Year Outlook

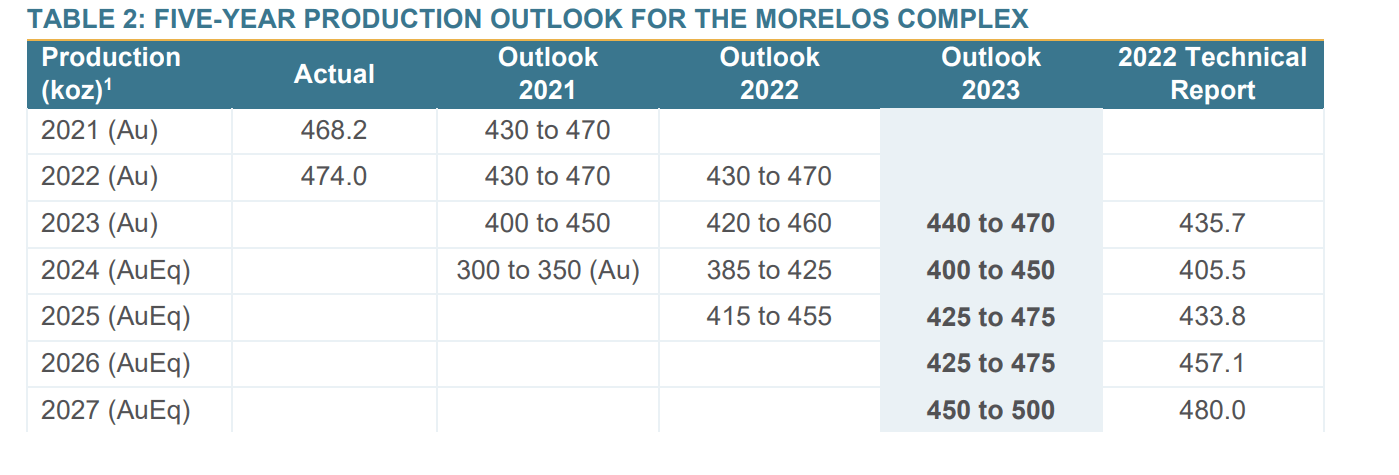

While the 2022 results were exceptional, the only negative is that they were so good that they will be hard to lap even with a slight increase in planned production vs. previous levels. This is because Torex should produce ~474,000 ounces at all-in-sustaining costs [AISC] of $995/oz in FY2022 based on its pre-reported production and cost estimates. However, FY2023 guidance suggests that we should see annual production of 455,000 ounces (mid-point) at an all-in-sustaining cost of $1,110/oz. So, even if we see a beat that wouldn't be surprising for this team given its track record of over-delivering, I would expect a best case of 457,000 to 463,000 ounces at ~$1,100/oz. The result would be a ~14,000-ounce dip in production vs. the mid-point with a $100/oz increase in costs year-over-year.

Torex - Multi-Year Production Outlook (Company Presentation) Torex - Quarterly & Annual Production + 2023 Outlook (Company Filings, Author's Chart & Estimates)

{kind=link}

{kind=link}

The difficult comps on deck are not ideal, and stocks can underperform when they have difficult comps ahead, similar to what we see from SSR Mining ( SSRM ) in 2022, which came off a monster in 2021 with record production but was fully valued after reporting its 2021 results. So, although Torex's higher costs are out of its control and related to inflationary pressures (cyanide, explosives, MBS, cement, and labor) plus increased capitalized stripping, the company will need the gold price to cooperate to deliver further growth on a year-over-year basis in FY2023. Meanwhile, from a free cash flow standpoint, growth capital is estimated at $430+ million, meaning Torex will go from being a steady free cash flow generator despite early spending on Media Luna in 2022 to being deeply free cash flow negative with ~$550 million in planned spending this year.

To summarize, sometimes a great year for a company combined with strong share price performance can be a negative from a forward return standpoint as it's tough to lap these strong results in the following year. Instead, it's often better to buy a company that's beaten up on the sale rack, which has guided too conservatively and is likely to beat and deliver significant growth on a year-over-year basis, assuming there are no major balance sheet issues. So, while Torex did an incredible job outperforming the sector last year and does have a solid year on the deck, I have a much lower conviction that the stock will be higher eleven months from now at year-end after already enjoying a ~130% rally off its lows.

{kind=link}

On the positive side, Torex had a record month regarding development rates in December, with an average advance rate of 7.2 meters per day, pushing the tunnel just past the Balsas River to finish the year. This is very encouraging as it suggests the tunnel is on pace for its breakthrough to Media Luna from its Guajes Portal by early 2024, giving it a nice runway ahead of planned commercial production by Q2 2025. Meanwhile, and as noted above, underground mining rates at ELG Underground continue to exceed expectations, and they could average north of 1,900 tonnes per day in 2024, which will help to pad production during this year of lower output as mining activities wind down at the Guajes pit in mid-2023 and the El Limon Sur Pit in late 2024.

{kind=link}

However, from a bigger-picture standpoint, the ability to maintain 1,800+ tonne per day mining rates and continue adding resources at ELG Underground could provide a nice lift to the company's planned production profile post-2027, especially if Torex is also successful in bringing its EPO deposit online (the other side of Balsas River just northwest of Media Luna). Assuming a 1,700 tonne per day mining rate and a slightly more conservative grade of 5.0 grams per tonne of gold would result in an incremental ~90,000 ounces per annum from ELG Underground alone, pushing production above 400,000 GEOs per annum (2028-2031) even without EPO. Hence, the continued exploration success and improving mining rates is a very positive development that cannot be overstated regarding the big picture for Torex.

Valuation & Technical Picture

Based on ~87 million fully-diluted shares and a share price of US$13.60, Torex is trading at a market cap of ~$1.18 billion. This is no longer an attractive valuation, with Torex trading closer to 0.85x P/NAV vs. an estimated net asset value of ~$1.34 billion. If we adjust for a more conservative 0.85 P/NAV multiple (given its status as a single-asset producer in a Tier-2 jurisdiction balanced by its industry-leading margins), Torex's fair value would come in at US$13.50, suggesting the stock is fully valued at current levels. Meanwhile, from a cash flow standpoint, Torex's near-parabolic rally has left the stock trading at ~4.9x forward cash flow estimates ($2.75) vs. less than 3.0x cash flow in September.

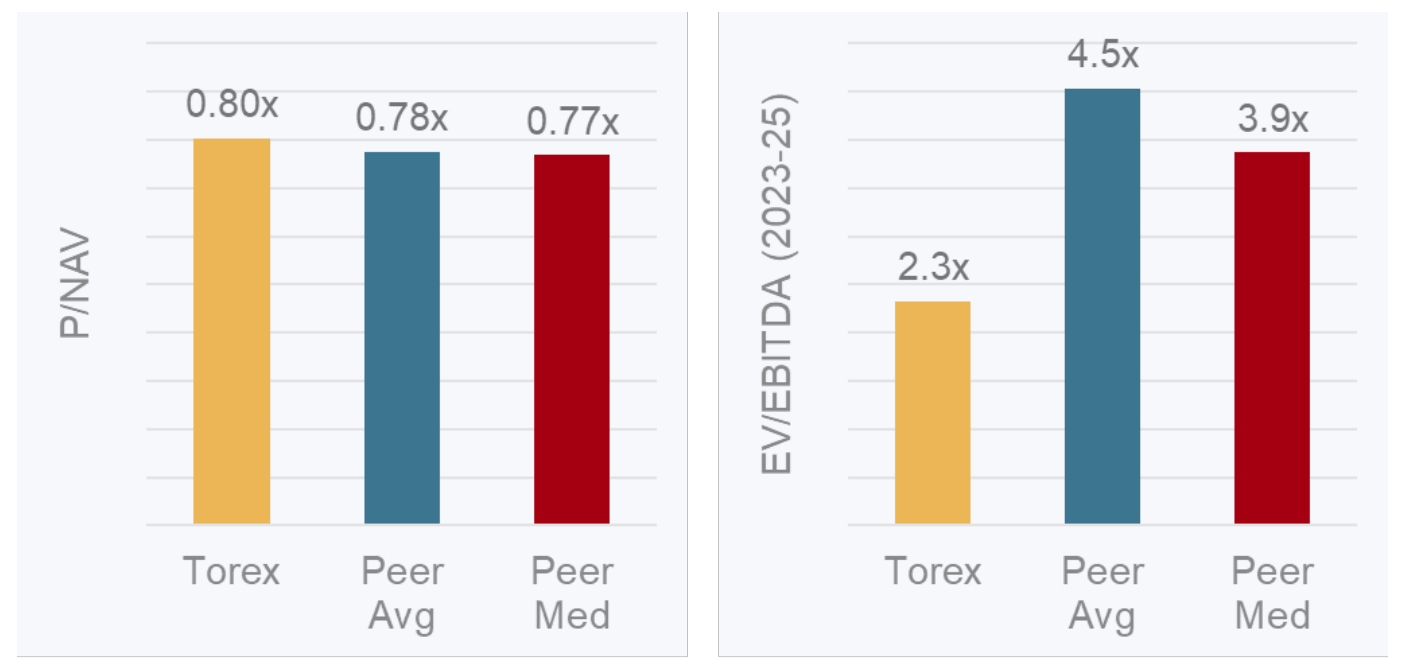

Torex P/NAV & EV/EBITDA Multiple vs. Peers (Company Presentation, S&P Capital IQ)

{kind=link}

Looking at Torex's valuation in the above chart, we can see that it's not just Torex's valuation that has become less attractive but also its relative valuation. This is because Torex now trades at a premium to its peer average, and this peer group includes a few producers with more attractive jurisdictional profiles and/or increased diversification. Torex's goal is to optimize its asset (filling the mill post-2027 and extending ELG Underground, which will increase net asset value if successful), and its long-term goal is to be a multi-asset business. Still, it is now in the most capital-intensive portion of Media Luna construction and is a single-asset miner today, even if it intends to add a second operation. Hence, with it no longer trading at a deep discount t fair value, I don't see any way to justify paying up for the stock here at US$13.60.

Finally, if we look at Torex's technical picture, we can see that the stock is even more extended above its strong support level at US$7.65, and it's now less than 10% away from multi-year resistance at US$14.80. This doesn't mean that the stock must fail here and that it can't go higher, but from a reward/risk standpoint, the reward/risk setup hasn't been this unattractive for the stock since May 2020, before it corrected more than 25% over the following two months. History doesn't have to repeat itself, and there's an outside chance that Torex will march higher over the short term, but I've never found value in being greedy in cyclical stocks. So, with Torex approaching strong resistance, I see this as an opportunity to book some profits.

Summary

Torex Gold has executed nearly flawlessly in challenging conditions under its CEO Judy Kuzenko, with record underground mining rates, solid progress on Media Luna development, and a phenomenal safety record with no real disruptions despite a tough time for its neighbor to the south at Los Filos. Hence, few companies are as deserving of the massive share-price outperformance that Torex enjoyed in Q4 (59% return). That said, the goal should be to buy high-quality companies at a deep discount to fair value, especially in a cyclical sector. So, while I see Torex as a solid buy-the-dip candidate (assuming we see a deep correction), I believe the best course of action here is booking some profits.

For further details see:

Torex Gold: Another Major Beat, But Tough Comps Ahead