TORXF - Torex Gold: Grades Slip In Q3 But Guidance Still Within Reach

2023-10-13 11:07:24 ET

Summary

- Torex Gold reported Q3 production, which came in at its lowest levels since Q2 2020, with a ~30% decline from the year-ago period.

- Unfortunately, this will significantly impact the company's upcoming financial results with a low denominator, elevated stripping costs and a stronger MXN/USD ratio.

- In this update, we'll dig into the Q3 production results, the outlook for the Q3 financials, and whether the disappointing recent quarterly result is priced into the stock.

The Q3 Earnings Season for the Gold Miners Index ( GDX ) is quickly approaching, and several companies have now reported their preliminary results. One of the first gold producers to report was Torex Gold ( TORXF ), and unfortunately, we saw a rare miss from the company, with Q3 production coming in at the lowest levels since Q2 2020 which was affected by a COVID-19 related shutdown, and a ~30% decline from the year-ago period. In fairness, the company was up against difficult comparisons, especially given that it was having to lap these comps with a focus on waste stripping in Q3. That said, the results were disappointing and would have been even worse if not helped by a record quarter from ELG Underground in the period. Let's inspect the quarter below and how the year is shaping up relative to annual guidance.

El Limon-Guajes Operations - Company Website

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q3 Production & Sales

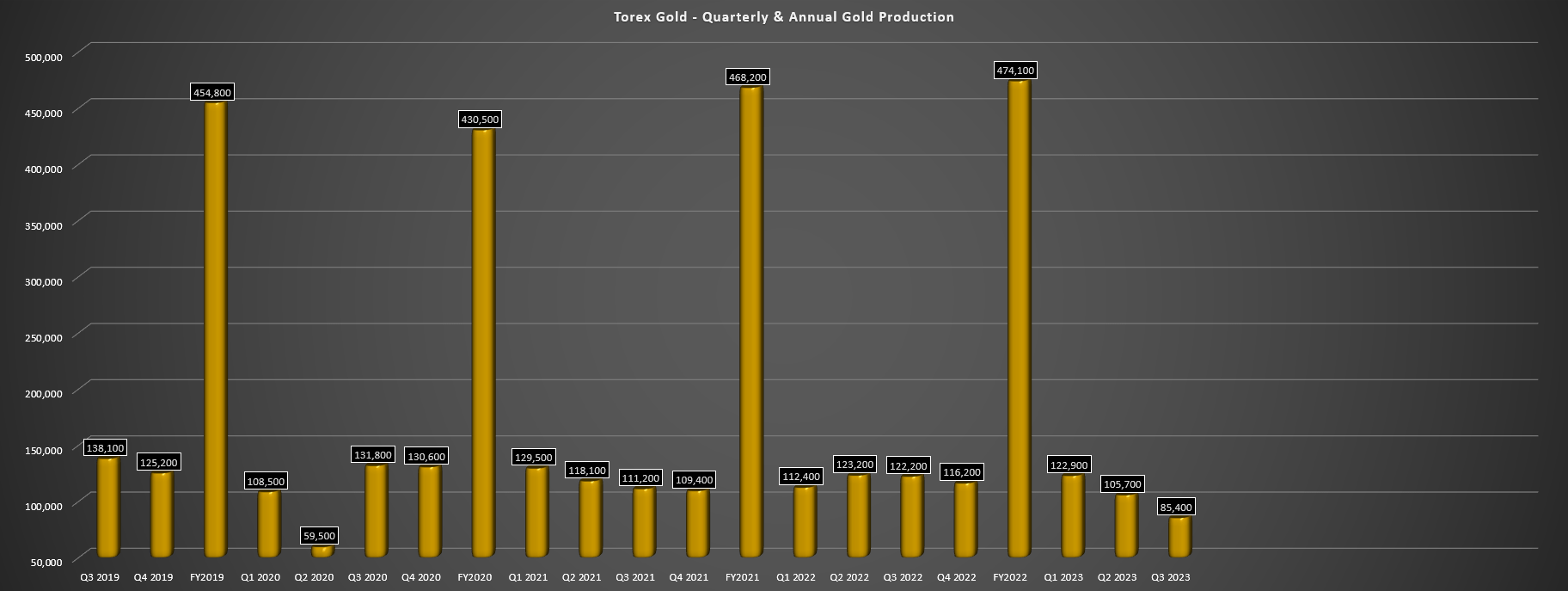

Torex Gold ("Torex") released its Q3 results this week, reporting quarterly production of just ~85,400 ounces, a 30% decline from the year-ago period, and a significant dip vs. my expectation of 100,000+ ounces in the quarter. The company noted that the weaker quarter was related to continued stripping that began in Q2 related to the layback to extend the El Limon Pit to provide a smoother transition to Media Luna, with the company noting previously that the Q3 mine plan would entail "a heavy focus on waste stripping and a drawdown on stockpiles" . However, I was expecting grades to come in closer to 2.90 grams per tonne of gold, not the ~2.47 grams per tonne of gold reported in the period. So, despite the solid processing rates at ~13,100 tonnes per day, production slid sharply, with Torex set up to deliver at the low end of guidance (440,000 ounces) vs. the potential for a beat on its mid-point (455,000 ounces) previously.

As it stands, Torex has produced ~315,800 ounces year-to-date, translating to 69.4% of its guidance midpoint.

Torex Gold - Quarterly & Annual Production - Company Filings, Author's Chart

{kind=link}

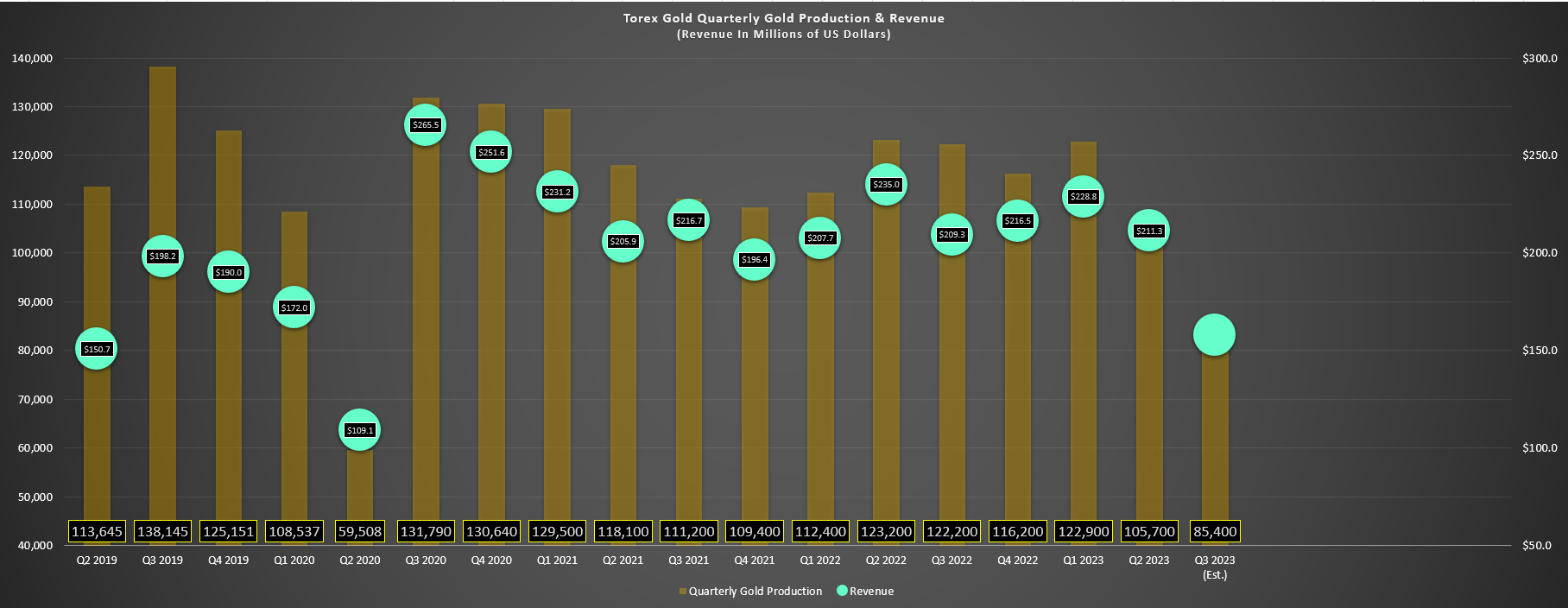

Unfortunately, this miss on production will also significantly affect the company's financial results, with the elevated sustaining capital in the period being divided by much fewer ounces, plus the additional negative impact of a stronger Mexican Peso in the period, suggesting AISC is likely to come in above $1,550/oz. Meanwhile, while the company was up against tough comps on production/sales, it was up against relatively easy comps from an average realized gold price standpoint (Q3 2022: $1,715/oz), with Torex previously set up to see a high single-digit decline in revenue assuming production of ~100,000 ounces at $1,930/oz or better. However, assuming ~81,800 ounces sold at $1,925/oz (sharp decline in gold prices late in the quarter), sales are now likely to drop over 20% to roughly ~$158 million. This will translate to a ~23% decline in sales year-over-year, setting up a weak quarter from a top-line standpoint as well. And from a margin standpoint, Torex is likely to report some compression, with AISC margins likely to come in below $370/oz.

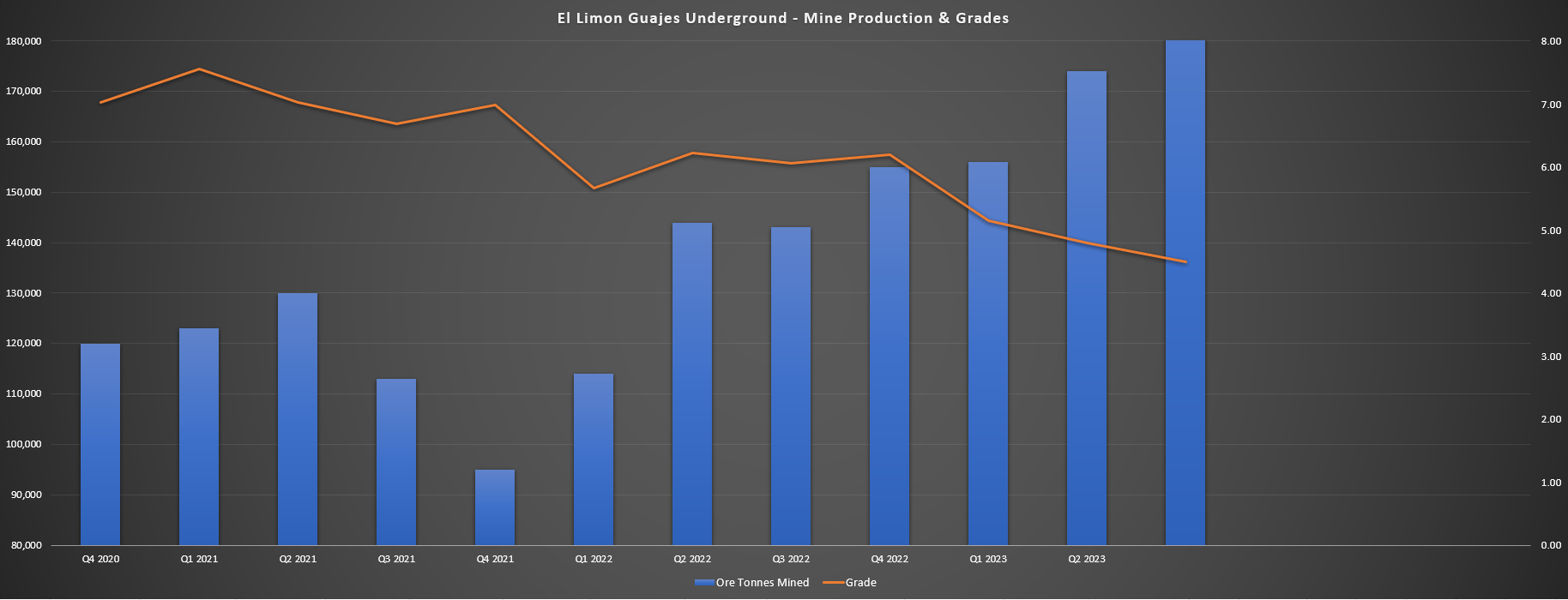

El Limon Guajes Underground Tonnes Mined - Company Filings, Author's Chart Torex Gold - Quarterly Production & Estimated Revenue - Company Filings, Author's Chart

{kind=link}

{kind=link}

On a positive note, Torex expects Q4 to be the strongest of the year, implying production of at least 123,000 ounces vs. the ~122,900 ounces reported in Q1. And assuming the company can deliver on this plan (which seems likely given its tendency to over-deliver on promises), production will come in right next to the low end of FY2023 guidance. However, more exciting was the fact that Torex delivered a monster Q3 at El Limon-Guajes Underground, with an average daily production rate of 2,321 tonnes per day, smashing the company's goal of exiting 2024 at 2,000 tonnes per day previously. And as Torex's CEO, Jody Kuzenko noted in the Q2 Conference Call, it was hoping to beat 1,800 tonnes per day in Q3 with similar to better than Q2, with it normalizing a little in Q4. And with production up 21% vs. Q2 (2,321 tonnes per day vs. 1,913 tonnes per day) and upwards of 200,000 tonnes of ore mined.

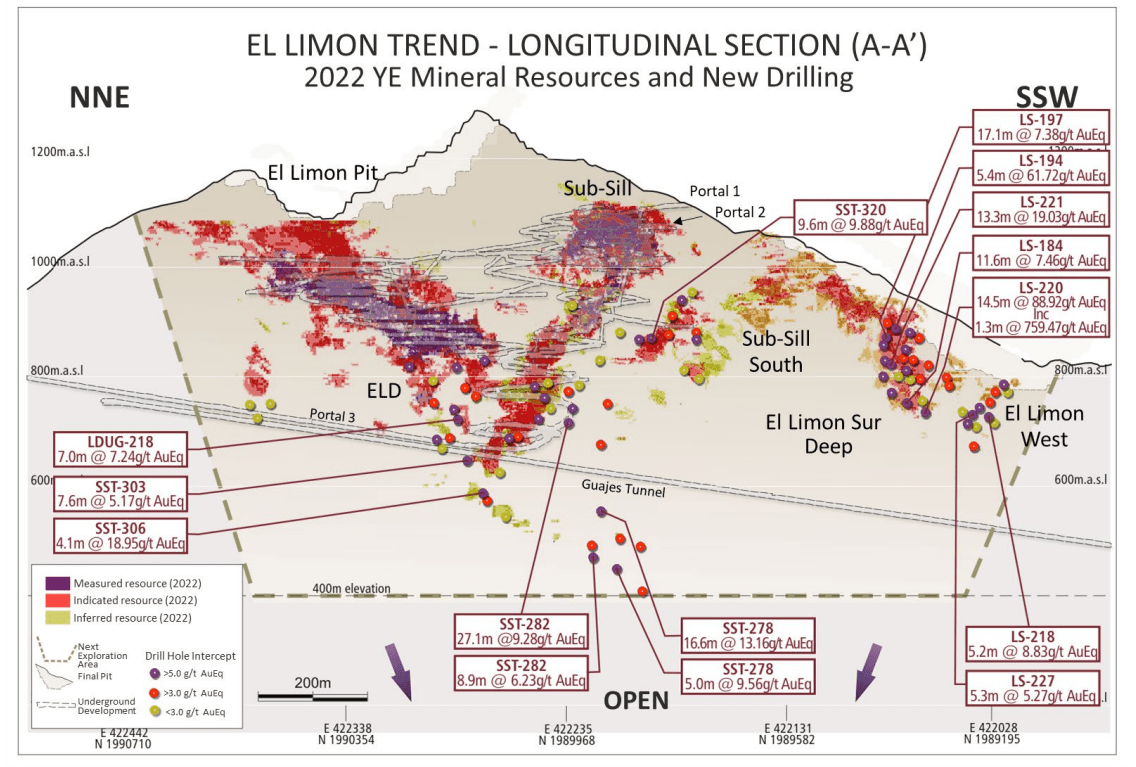

ELG Drill Highlights - Company Website

{kind=link}

This is important because one way to beef up the production profile following the cessation of open-pit mining at ELG (year-end 2025) is to lean on ELG Underground and also look at other feed sources to displace lower-grade stockpiles. And the difference between 2,000 tonnes per day and ~1,500 tonnes per day (2022 UG mining rate) is an extra ~26,000+ ounces per annum or just shy of $50 million of additional revenue per year which is a nice sweetener for the production profile. So, the company's ability to ramp up mining rates here and continue making new underground discoveries is certainly encouraging, with this suggesting higher underground production for longer vs. a previous outlook of ~1,400 tonnes per day until 2027. In summary, there looks to be some meaningful upside to NAV vs. the most recent TR.

Recent Developments

Moving over to recent developments, Torex hasn't been getting any help from the Mexican Peso, and being a solely Mexican operator in the middle of a massive growth project (~$480 million uncommitted as of Q2 2023). However, the MXN/USD has finally begun to pull back recently, providing some relief for Torex in what's been a worse than expected year for inflation for most of the producer group. Unfortunately, the timing of this pullback which will reduce the short-term impact on margins and negative impact on growth capital has coincided with a sharp pullback in the gold price, which has now spent three full weeks below $1,900/oz after a record 22 consecutive weeks above $1,900/oz. And while this is a price where Torex can do very well given its relatively low costs, it will be a drag on margins in Q4 if we don't see a recovery soon, and could impact FY2024 cash flow depending on how long this correction continues.

{kind=link}

The good news is that the company has sufficient liquidity to complete construction between future cash flow, net cash, and its undrawn revolving credit facility ($250 million with plans to increase to $300 million), so unlike other miners, it won't need to sell assets or equity to complete Media Luna construction. In addition, Torex is much less sensitive to the gold and silver prices than its peers, so while the Peso is pushing some of its peers all-in cost margins into negative territory like Endeavour Silver ( EXK ), Torex will survive this correction as it has several others, and could easily stomach a deeper correction in the gold if this were to occur. Hence, given that it's a less sensitive miner due to its sub $1,200/oz AISC and sub $1,000/oz post-2025 with Media Luna, the deep discount to the peer group on a valuation standpoint continues to be a head-scratcher.

Valuation

Based on ~87 million fully diluted shares and a share price of US$9.90, Torex trades at a market cap of ~$860 million, making it one of the lowest capitalization names in the mid-tier space, trading at a fraction of the value of peers like Lundin Gold ( LUGDF ) and Alamos Gold ( AGI ). We can attribute much of this discount to the fact that it operates out of one of the less attractive states (Guerrero) within a jurisdiction that's already declining in attractiveness over the past few years, Mexico. In addition, while the company is generating considerable cash flow, it's not generating any free cash flow, being in the middle portion (~40% complete) of a major build as it transitions from mining ELG Open Pit & Underground to Media Luna UG and ELG Underground post-2024. And while the project is tracking in line with budget and schedule, with the company having sufficient liquidity, the strength in the Peso hasn't helped from a capex standpoint (45% exposed).

Although this makes Torex less attractive from a P/FCF standpoint to peers like Lundin and Alamos that are generating significant free cash flow currently, this discount relative to peers is getting extreme, with Torex now sitting just above ~3.0x P/CF using conservative FY2024 estimates of $3.40 and at just ~0.60x P/NAV based on an estimated net asset value of ~$1.45 billion. So, while the stock may never trade at the premium multiples that Alamos enjoys, unless it can add one or two Tier-1 jurisdiction assets longer-term to diversify its NAV, it is becoming extremely cheap relative to peers and on an absolute basis relative to where it's traded historically. In fact, even if we use an ultra-conservative multiple of ~4.7x P/CF in line with its 10-year average, Torex would trade at US$16.00 - 60% upside from current levels. And using what I believe to be a fair value of US$15.70 (65/35 weighting to NAV vs. P/CF at 0.90x and 5.0x, respectively), Torex has just shy of 60% upside to fair value.

Summary

Torex Gold has quickly gone from nearly fully valued in May to one of the more attractively valued producers as of this week, with the stock getting closer to its updated low-risk buy zone of US$9.55. And while this was a riskier story 18 months ago, when it wasn't how much of an increase we'd see in upfront capex and whether the company could execute a smooth transition to mining at Media Luna with no gap, the company remains on budget and schedule with sufficient liquidity to fund construction even if we see minor cost creep because of the stronger Mexican Peso. Meanwhile, the story has got a massive upgrade from an exploration standpoint, with results from EPO, ELG Underground and Media Luna far exceeding my expectations. So, if I were looking for exposure to a mid-tier producer, I would strongly consider Torex on any pullback below US$9.55 before year-end.

For further details see:

Torex Gold: Grades Slip In Q3, But Guidance Still Within Reach