TORXF - Torex Gold: Ignore The Weak Q3 Results

2023-11-20 04:56:38 ET

Summary

- Torex Gold's Q3 production declined by 30% because of elevated waste stripping related to its planned layback, resulting in lower head grades and weaker margins.

- ELG UG mining rates continue to trounce stated goals (2k TPD). The Company continues to release some of the best drill intercepts sector-wide and ML is tracking on budget/schedule.

- In this update, we'll dig into the Q3 results, recent developments, and where TORXF stock's updated low-risk buy zone lies.

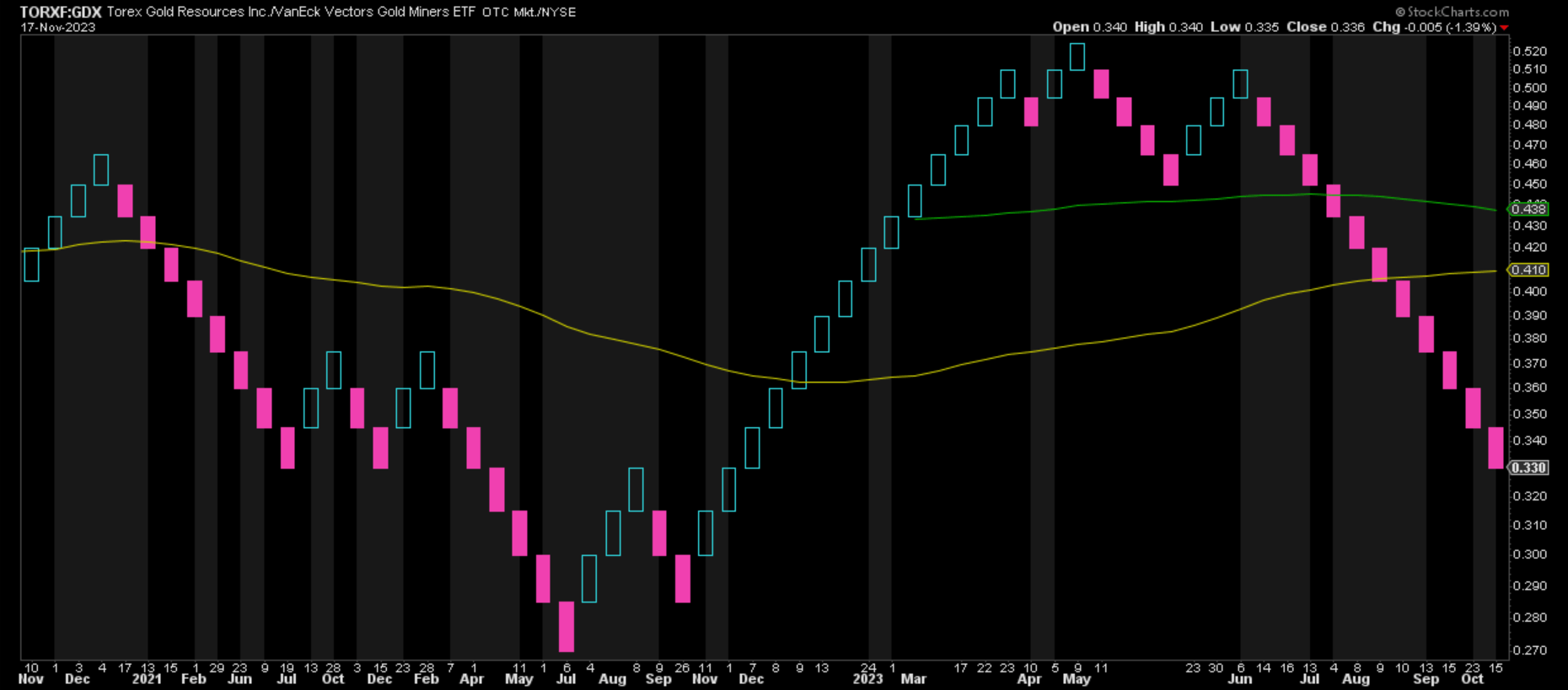

Just over five months ago, I wrote on Torex Gold (TORXF), noting that the significant outperformance in the stock was providing an opportunity to book more profits into strength. This is because the stock was up ~45% year-to-date as of May at US$17.50 per share and while it was continuing to execute near flawlessly (production & exploration success), it was trading near 0.90x P/NAV which made it look fully valued for a Tier-2 jurisdiction single-asset producer. Since then, Torex has significantly underperformed its benchmark with a ~45% share-price decline, reversing its trend of outperformance. And while some of this softness can be related to an upward revision in annual cost guidance, the company continues to make solid progress on resource/reserve growth and Media Luna construction, suggesting upside to its Morelos Complex NPV and a smooth transition to production from Media Luna in 2025. In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated low-risk buy zone lies.

Torex Gold vs. Gold Miners Index Performance - StockCharts.com

{kind=link}

All figures are in United States dollars.

Q3 Production & Sales

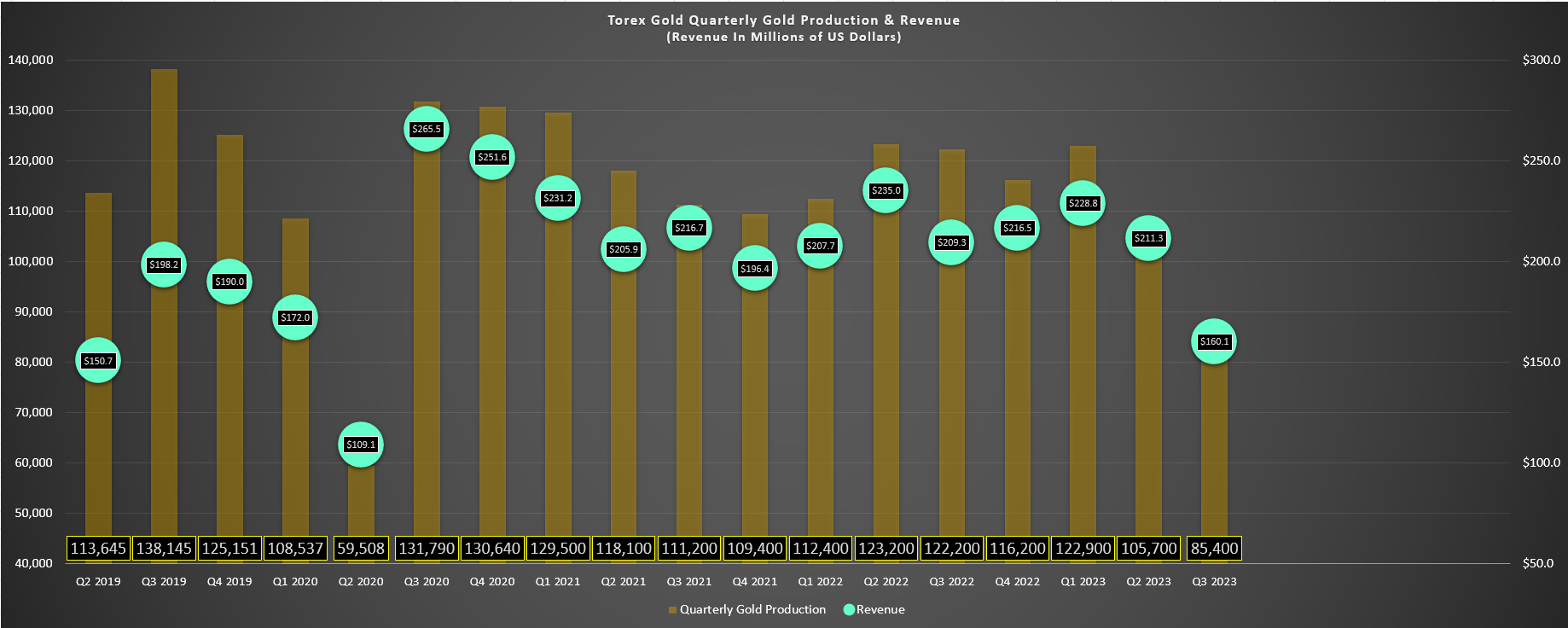

Torex Gold ("Torex") released its Q3 results earlier this month, reporting quarterly production of ~85,400 ounces of gold, a ~30% decline from the year-ago period. However, the most recent period saw elevated waste stripping as the company worked to complete the layback of the El Limon Pit (filling the gap in the mine plan to smooth out its production profile ahead of Media Luna production), which resulted in an increased on lower grade and stockpiled ore. The result was that feed grades fell materially to 2.47 grams per tonne of gold (Q3 2022: 3.38 grams per tonne of gold), offsetting the impressive plant performance and the record mining rates at El Limon Guajes Underground [ELGUG] which were tailwind for grades. So, while the headline results were certainly not all that exciting (~30% lower production at much higher costs), this was an abnormal quarter and does not reflect regular operations at its Morelos Complex (average quarterly production of 100,000+ gold-equivalent ounces).

Torex Gold - Quarterly Production & Revenue - Company Filings, Author's Chart

{kind=link}

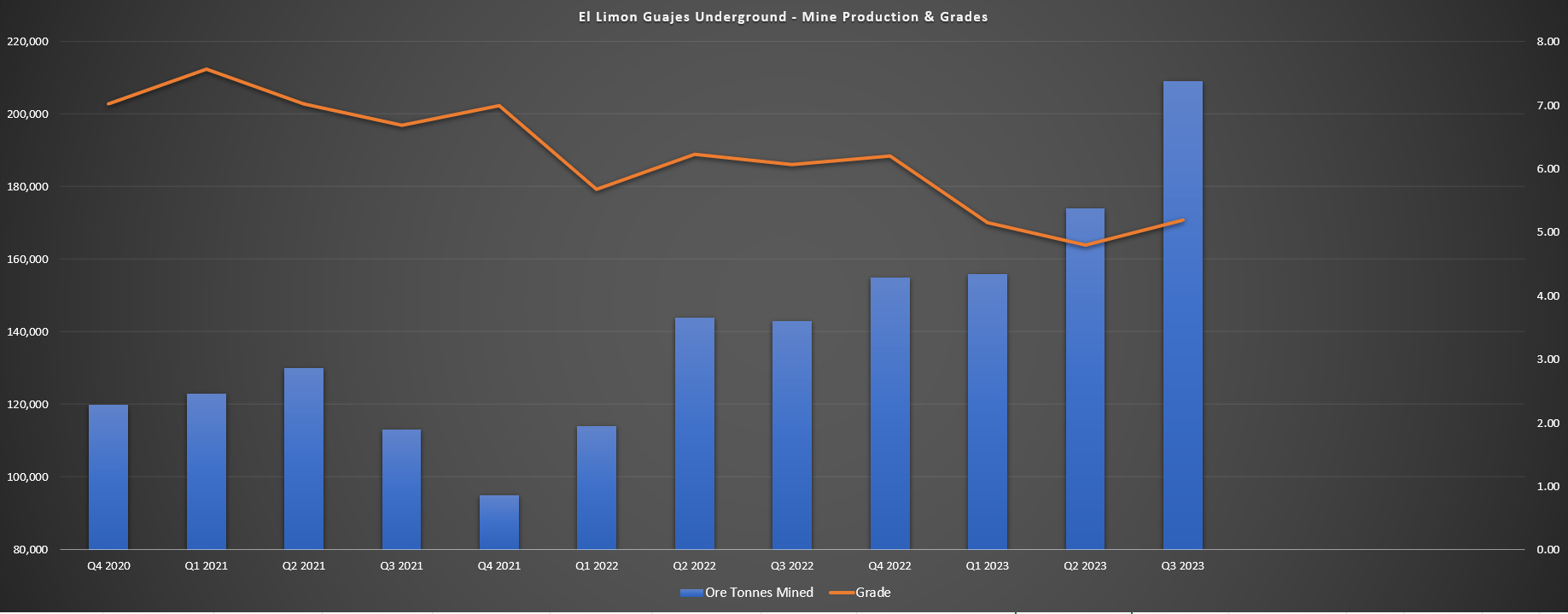

Digging into the quarter a little closer, there were multiple positive takeaways. For starters, the plant continues to operate above its design of 13,000 tonnes per day (~13,200 tonnes year-to-date) which helped to offset the lower grade profile in Q3. Second, underground mining rates at ELGUG have continued to trounce my estimates (Q3: 209,000 tonnes) with a record ~214,000 tonnes mined in Q3 (2,321 tonnes per day) at an average grade of 5.19 grams per tonne of gold. In fact, Torex's mining rates in Q3 have well surpassed the company's goal of exiting 2024 at 2,000 tonnes per day previously and they're providing nice economies of scale underground, with underground mining costs of $79.61/tonne down sharply year-over-year (Q3 2022: $91.89/tonne / Q1-Q3 2022: $87.30/tonne) despite the impact of a stronger Peso and inflationary pressures. As noted in past updates, this is a big deal because the plant will have excess capacity and higher mining rates at ELGUG could provide another source of high-grade feed to the plant.

El Limon Underground - Mine Production & Grades - Company Filings, Author's Chart

{kind=link}

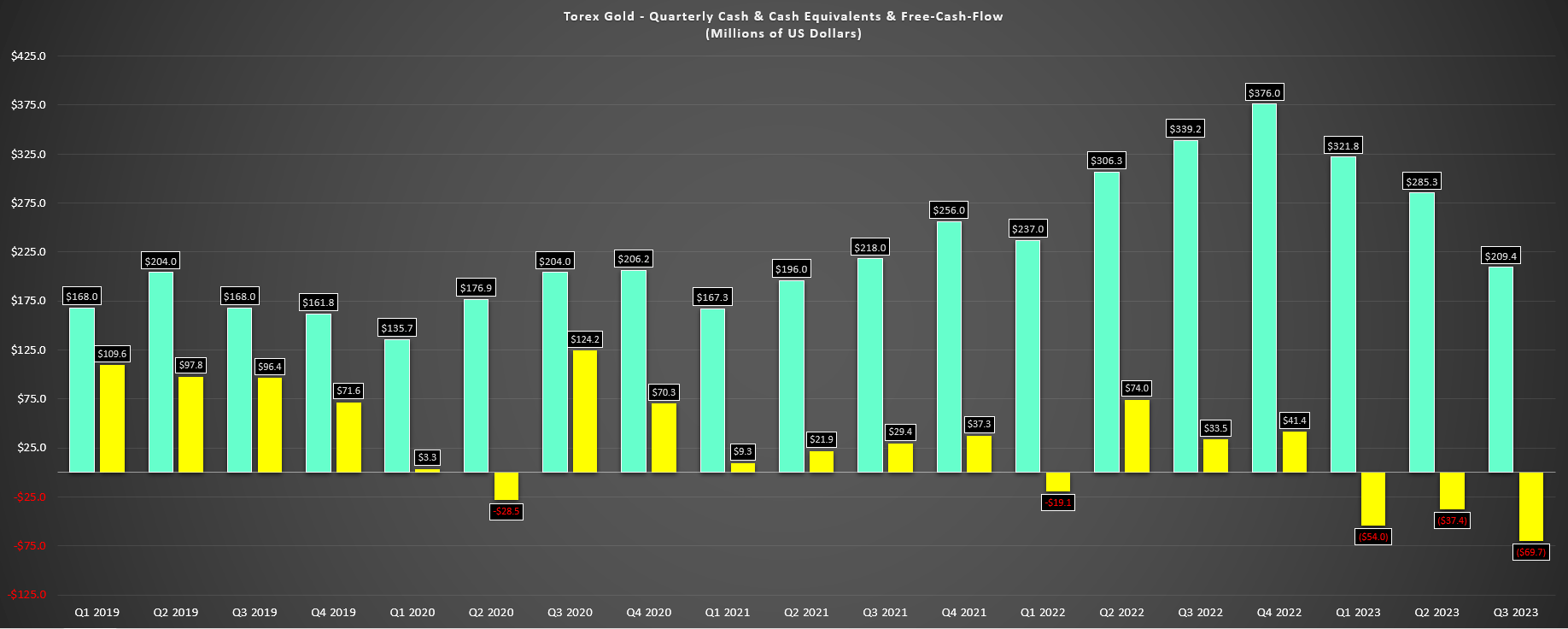

Although these figures are certainly positive, they didn't show up in the financial results, with revenue down over 23% year-over-year to $160.1 million despite the benefit of a higher average realized gold price ($1,944/oz). Meanwhile, operating cash flow sunk to $44.2 million (Q3 2022: $102.4 million), adjusted earnings slid to $11.1 million and Torex reported a free cash outflow of $69.7 million. That said, elevated capital expenditures affected the latter figure as the company works to develop its second mine on the south side of the Balsas River, with $98.7 million spent at Media Luna vs. $32.5 million in the year-ago period. Finally, it's worth noting despite the cash outflow, Torex is well positioned to fund Media Luna with ~$292 million in available credit and ~$209 million in cash (~$501 million liquidity) with continuing cash flow generation over the next 15 months vs. remaining expenditures of $508 million.

Torex - Quarterly Free Cash Flow & Cash/Cash Equivalents - Company Filings, Author's Chart

{kind=link}

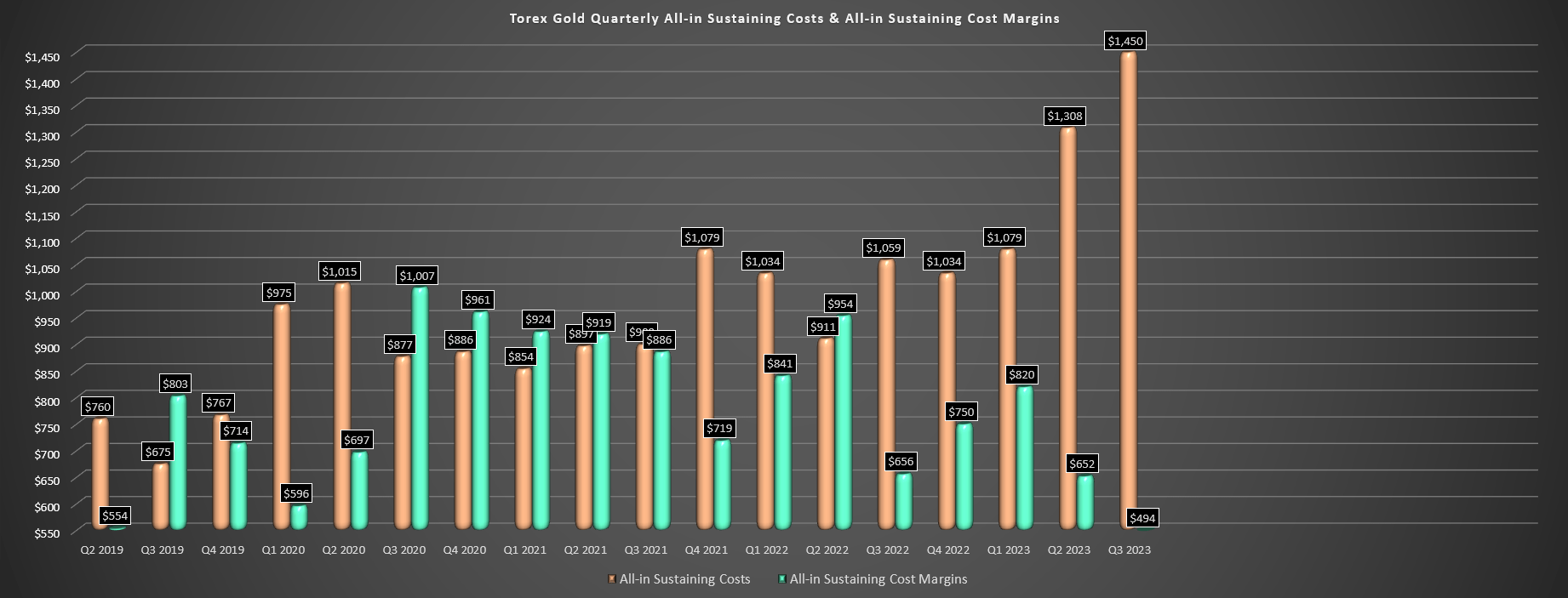

Costs & Margins

Moving over to costs and margins, it's no surprise that Q3 was a high-cost quarter for the company, and cash costs and all-in sustaining costs [AISC] soared to $1,086/oz and $1,450/oz, respectively. This translated to a 43% and 37% increase year-over-year, respectively, and the higher costs prompted Torex to raise its cost guidance to $840 to $870/oz on cash costs ($95/oz increase at the mid-point) and $1,160/oz to $1,200/oz for AISC ($75/oz at the mid-point). Obviously, this is disappointing, as was Q3 cost performance, but it's important to note that this is partially out of Torex's control and is the same thing we're seeing for all Mexican producers due to rally in the Mexican Peso. The difference for Torex though is that while many producers like Endeavour Silver ( EXK ), First Majestic ( AG ) and Guanajuato Silver ( OTCQX:GSVRF ) have negative or razor-thin AISC margins, Torex is still generating significant cash flow and not diluting shareholders every other quarter given that it built a massive cash position and buffer ahead of its growth plans.

{kind=link}

Moving over to margins, Torex's AISC margins fell to their lowest levels in years at $494/oz, but I would expect a meaningful improvement in the coming quarter[s], with grades up sharply in October which translated to production of 41,000 ounces and the low end of guidance implies production of ~122,000 ounces. Plus, Torex's margins were impacted further by fewer ounces sold than produced in Q3 and AISC would have come in closer to $1,390/oz if not for the unfavorable shortfall. Finally, although the Mexican Peso has continued its rally in Q4 after a brief pause, the company has added hedges to reduce its exposure subsequent to quarter-end in the period from September 2023 to December 2024. So, while margin performance was certainly below my expectations in Q3, this will likely mark the trough for margins, and the company has further visibility into maintaining strong margins as costs normalize with ~141,000 ounces of gold hedged at ~$1,955/oz.

Recent Developments

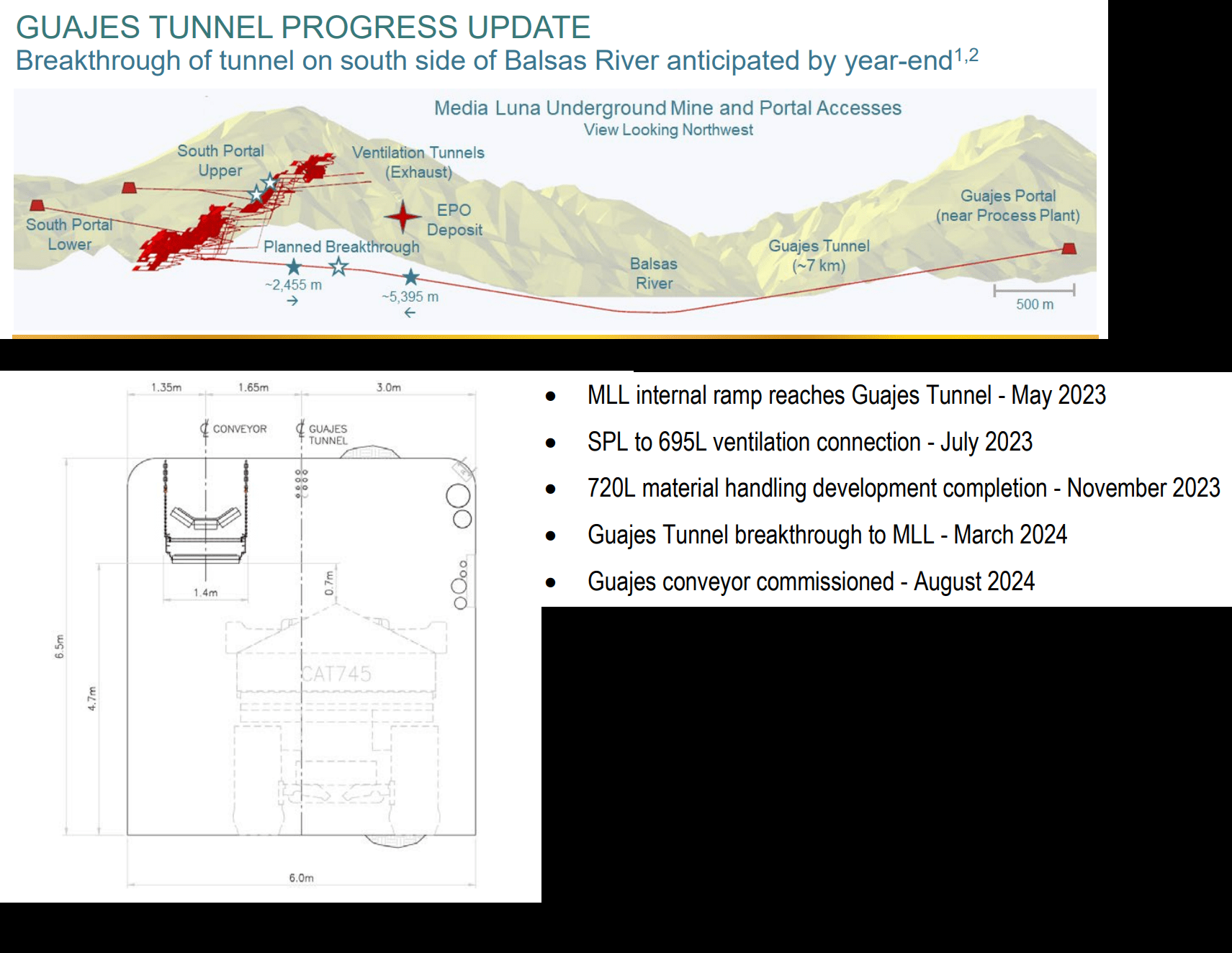

Moving over to recent developments, there's certainly lots to be positive about. For starters, the Guajes Tunnel under the Balsas River has advanced ~5,400 meters and South Portal Lower is at over ~2,400 meters, with breakthrough expected three months ahead of schedule by year-end (March 2024 previously) helped by improving advance rates over the past three months. Second, although each 1 point in the MXN/USD vs. the US Dollar ( UUP ) translates to a ~$15 million headwind on costs, the project is tracking on budget and schedule for the time being. Third, Torex noted that the installation of the 7-kilometer conveyor (~1.1 meter wide) in the tunnel will begin shortly after, and seems to be on schedule for commissioning in August 2024. And as for overall project progress, Media Luna is now 49% complete and the in-pit tailings deposition for the Guajes Pit was received earlier this month, further de-risking the investment thesis.

Media Luna Progress - Company Presentation & Technical Report

{kind=link}

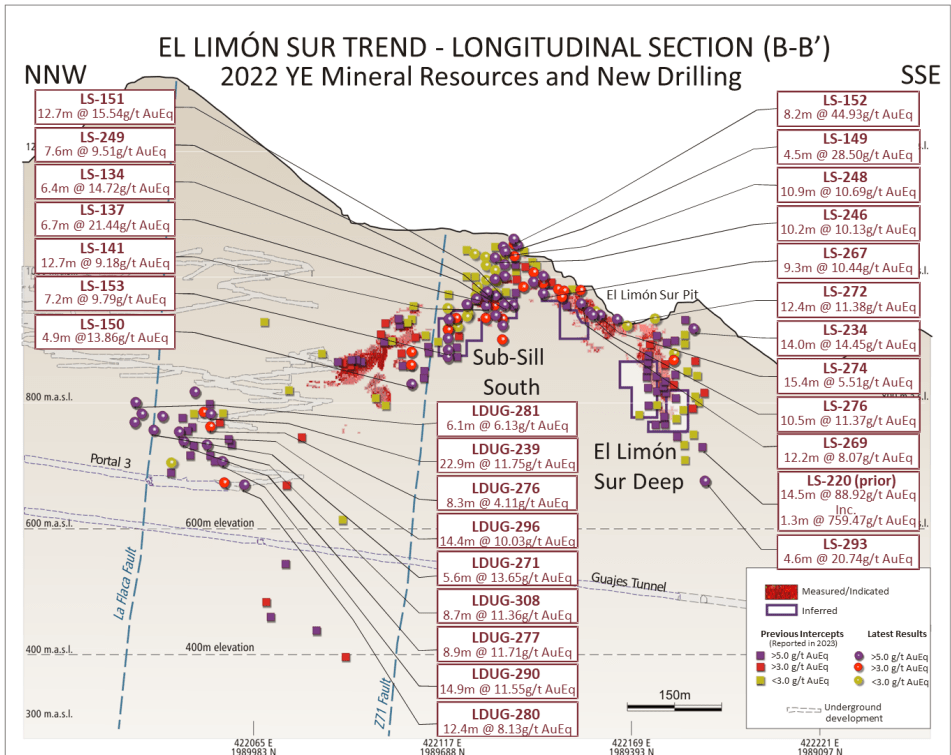

While these developments are positive, arguably the most exciting developments were from an exploration standpoint. In fact, outside of what looks to be a setup for material resource growth at EPO (south side of Balsas River), exploration success on the north side of the Balsas River near the plant continues to exceed my expectations in multiple areas. Beginning with El Limon Sur, Torex extended mineralization a further 100 meters at depth at ELS Deep with an intercept of 4 meters at 20.74 grams per tonne gold-equivalent, confirming the phenomenal grades here (with a previous intercept at shallower depths of 14.5 meters at 88.92 grams per tonne gold-equivalent). Meanwhile, drilling at the intersection of the ELS Trend and the La Flaca fault has also been highly encouraging and is yielding elevated copper grades, suggesting a potential lift to company-wide copper production (when combined with higher recoveries from new copper/iron sulphides flotation circuit) in this area with no resources currently.

El Limon Sur Trend Drilling (El Limon Sur Trend Drilling - Company Website)

{kind=link}

Meanwhile, Torex has also focused on upgrading and expanding resources at Sub-Sill South, and grades have been impressive, with highlight intercepts of 4.9 metres at 13.86 grams per tonne gold-equivalent, 12.7 meters at 15.54 grams per tonne gold-equivalent, and 6.7 meters at 21.44 grams per tonne gold-equivalent, with Torex noting that grades were "better than anticipated" . Finally, Torex has seen strong results from El Limon Deep (highlight of 4.8 meters of 35.81 grams per tonne gold-equivalent and 9.1 meters at 33.91 grams per tonne gold-equivalent) and also shared that it will be looking to test the continuity of mineralization down to the 600-meter level across the ELS Trend. So far, the results at the La Flaca Fault well below Sub Sill South are quite encouraging with exceptional grades and thicknesses. If continuity is confirmed, Torex noted that it would validate its geological concept of NNW trending structural corridors and prompt drilling to replicate these results on the Sub-Sill Trend, ELW Trend, and at depth along the ELS Trend.

Overall, these exploration results certainly suggest that growth in NAV is likely at its Morelos Complex, and displacing stockpiles with higher-grade resources later this decade should not be a problem with consistent high-grade mineralization wherever Torex drills across its large land package in Guerrero State.

Summary

Torex Gold will need a solid Q4 to deliver at the lower end of its FY2023 guidance considering that it's tracking at just ~71.7% (~315,800 ounces vs. 440,000 ounces), but this looks doable with a significant improvement in grades in October. Meanwhile, although it's disappointing that the company's multi-year streak of meeting cost guidance will end this year, this was largely out of its control because of a sharp move higher in the Mexican Peso, and Torex's margins are still well above the industry average even assuming costs at the high end of guidance. Most importantly, though, Media Luna construction remains on budget and schedule and Torex has ample liquidity to complete construction with no need for share dilution. So, with the stock trading at a deep discount to its peer group (~3.0x FY2024 operating cash flow estimates) and a near 40% discount to an estimated fair value of US$15.40, I would view any pullbacks below US$9.20 as buying opportunities.

For further details see:

Torex Gold: Ignore The Weak Q3 Results